IRS Form 3903 Instructions

In 2017, the Tax Cuts and Jobs Act (TCJA) suspended the moving expense deduction for most taxpayers. However, members of the armed forces and their military families can still claim the tax deduction for out-of-pocket expenses they incur during a permanent change of station (PCS) move.

This article will walk you how to file IRS Form 3903 to claim that deduction.

Let’s start with step by step guidance on how to claim the moving expense deduction using IRS Form 3903.

Table of contents

How do I complete IRS Form 3903?

Fortunately, Form 3903 is a straightforward, one-page form, which we’ll cover, step by step.

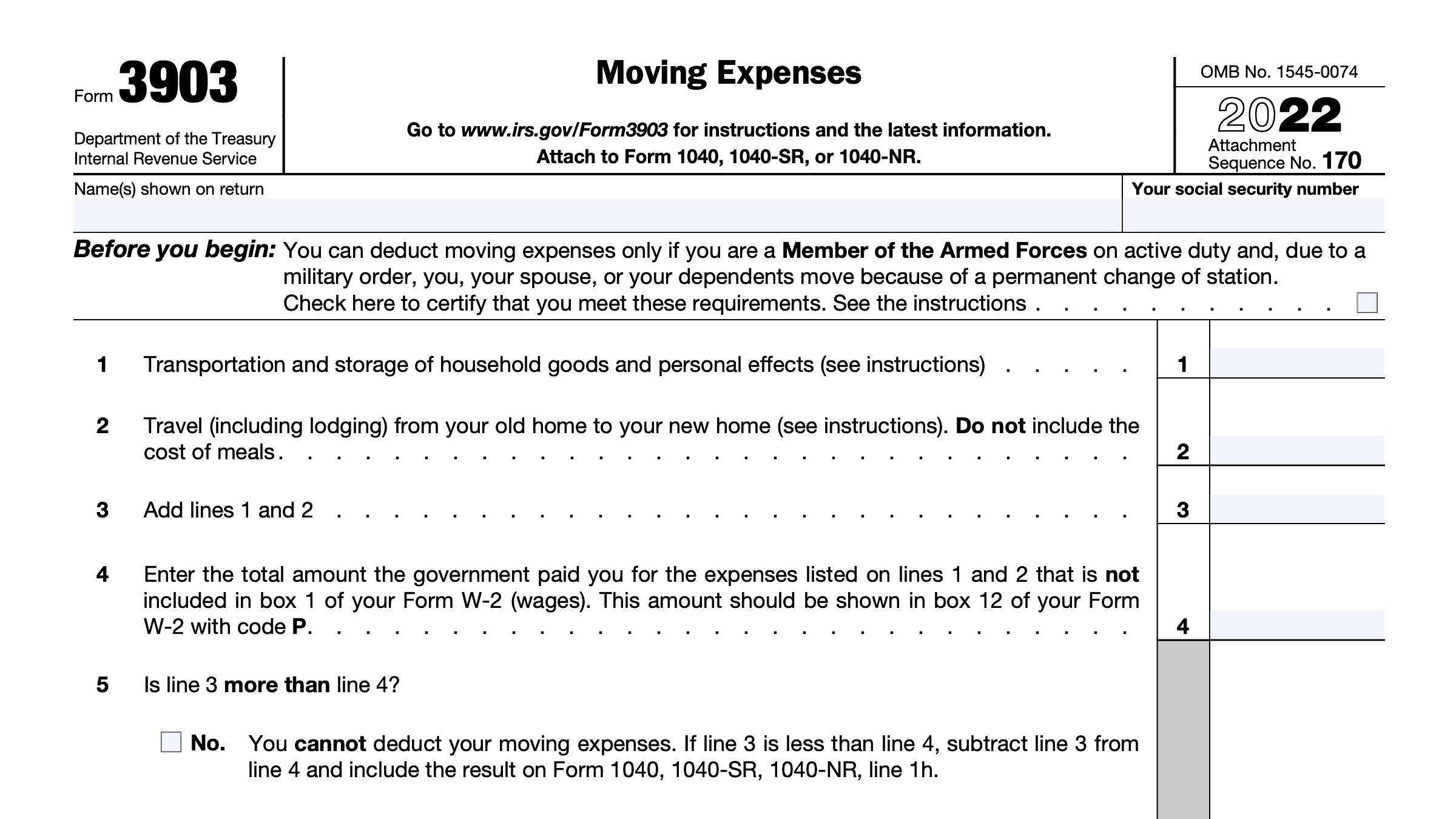

Line 1: Transportation and storage of household goods and personal effects

Complete Line 1 using your actual expenses.

Don’t include any expenses for moving services provided by the government. Also, don’t include any expenses that were reimbursed by an allowance you don’t have to include in your income.

According to the form instructions, you may enter the amount you paid to pack, crate, move, store, and insure your household goods and personal effects. You may also enter the amount paid for storage under the following circumstances:

- Foreign move: The entire time your new principal workplace is outside the United States or its possessions

- Move within the United States or within its possessions: Up to 30 days between moves from your old home to your new location.

However, if you’re only claiming storage fees, you do not need to file Form 3903 if all of the following apply:

- You moved in an earlier year.

- You are claiming only storage fees during your absence from the United States.

- Any amount the government paid for the storage fees is included in box 1 of your Form W-2 (wages).

Instead, simply enter your storage fees on Line 14 of Schedule 1 and write “Storage” on the dotted line next to Line 14.

Line 2: Travel

Enter the amount you paid to travel from your old home to your new home. This includes transportation and lodging on the way. Include costs for the day you arrive.

The members of your household do not have to travel together or at the same time. But you can only include expenses for one trip per person.

Do not include any house hunting expenses.

Line 3: Total moving expenses

Add Lines 1 and 2.

Line 4: Government reimbursement

Enter the amount, if any, that the government paid you for moving expenses, that is not included in Box 1 of your Form W-2. This amount should be in Box 12 of Form W-2 with code P.

Line 5: Unreimbursed moving expenses

Is Line 3 greater than Line 4?

No: Line 3 is not greater than Line 4.

If Line 4 is greater than Line 3, you cannot deduct moving expenses. Since the federal government’s reimbursement was greater than your out of pocket expenses, you must declare the excess as income.

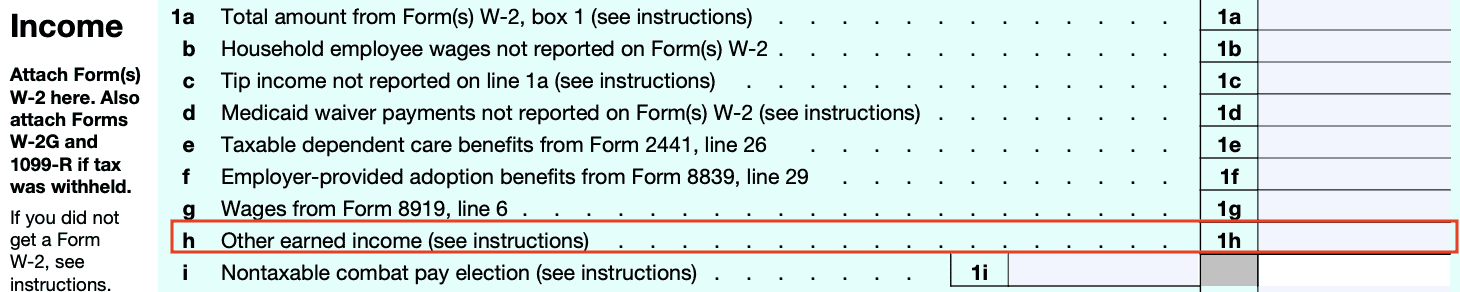

Subtract Line 3 from Line 4 and enter the result on Form 1040, Line 1h.

Yes: Line 3 is greater than Line 4.

If Line 3 exceeds Line 4, then subtract Line 4 from Line 3. Enter the difference in Line 5 and on Schedule 1, Line 14 as an adjustment to income. This will directly reduce your taxable income.

What is IRS Form 3903?

IRS Form 3903, Moving Expenses, is the federal form that eligible taxpayers may use to calculate the moving expense deduction. Currently, the moving expense deduction is an above the line tax deduction, as an adjustment to gross income listed on Schedule 1 of a federal return.

In other words, a taxpayer does not need to itemize tax deductions on Schedule A in order to claim this deduction on their personal tax return.

What is a permanent change of station (PCS) move?

For tax purposes, the Internal Revenue Service considers one of the following to qualify as a PCS move:

- A move from your old home to your first post of active duty

- A move from one permanent post of duty to another permanent post of duty, and

- A move from your last post of duty to your home or to a nearer point in the United States.

The move to your new home must occur within either of the following:

- 1 year of ending your active duty, or

- Within the period allowed under the Joint Travel Regulations

With that said, there are limitations to which moving costs are deductible expenses and which are not. Let’s begin with which moving expenses you can deduct.

Which moving expenses can I deduct on my federal tax return?

For military personnel moving on PCS orders, you can deduct reasonable unreimbursed expenses of moving yourselves and members of your household.

Moving household goods and personal effects

Below are examples of the deductible expenses for moving your household goods:

- Hauling a trailer

- Packing costs

- Crating

- In-transit storage

- Insurance

Storage costs

You can also include unreimbursed expenses related to the storage and insurance of household goods and personal effects. However, this deduction is limited to within any period of 30 consecutive days:

- After the day your goods and effects are moved from your former home, but

- Before they are delivered to your new home

Travel costs

You may deduct unreimbursed travel costs, including:

- Lodging expenses

- Airfare

- Parking fees and tolls

- Car expenses

There are two ways to deduct car expenses:

- Actual out-of-pocket expenses, such as gas and oil, or

- Standard mileage rate:

- 18 cents per mile before July 1, 2022

- 22 cents per mile July 1, 2022 and later

Which moving expenses are not tax-deductible?

You cannot include the costs of maintaining your vehicle, nor can you include depreciation as a tax deductible moving expense. Also, you cannot include the cost of meals as a travel expense.

You cannot include any expenses for which the federal government reimbursed you with a nontaxable allowance, nor can you deduct any expenses for moving services provided by the government.

Below is a list of other items that you cannot deduct as a moving expense:

- Any part of the purchase price of your new home

- Car tags

- Driver’s license

- Expenses of buying or selling a home (including closing costs, mortgage fees, and points)

- Expenses of entering into or breaking a lease

- Home improvements to help sell your home

- Loss on the sale of your home

- Losses from disposing of memberships in clubs

- Mortgage penalties

- Real estate taxes

- Refitting of carpet and draperies

- Return trips to your former residence

- Security deposits (including any given up due to the move)

- Storage charges except those incurred in transit and for foreign moves

What is a foreign move?

According to the IRS, a foreign move is either:

- A move from the United States or its possessions to a foreign country, or

- A move from one foreign country to another foreign country

A move from a foreign country to the United States or its possessions isn’t a foreign move.

For a foreign move, the deductible moving expenses described earlier are expanded to include the reasonable expenses of the following:

- Moving your household goods and personal effects to and from storage

- Storing these items for part or all of the time the new job location remains your main job location

- The new job location must be outside the United States

Video walkthrough

Watch this informative video to learn more about claiming moving expenses as a tax deduction on Form 3903.

Frequently asked questions

As part of the Tax Cuts and Jobs Act, only members of the armed forces and dependents of a member of the armed forces can use Form 3903 to claim a tax deduction. Also, the moving expense deduction must be related to a permanent change of station, or PCS move. Unless extended by law, the armed forces limitation is set to expire after the end of 2025.

Eligible military personnel can deduct expenses, if not reimbursed or provided in-kind for moving household goods (HHG) and personal effects, and travel-related expenses.

A member of your household is anyone who has both your former home and your new home as his or her main home. This does not include a tenant or employee unless you can claim that person as a dependent on your tax return.

Where can I find a copy of IRS Form 3903?

As with all federal tax forms, you may find a copy of this form on the IRS website. You can also select download the form at the bottom of this article.

Related tax articles

This tax form is one of the fillable tax forms provided by the Internal Revenue Service, to help taxpayers reduce their tax preparation costs. To see more forms like this, visit our free fillable tax forms page, where you’ll also find articles like this.

Unlike the IRS, our articles contain step by step instructions for each tax form, as well as video walkthroughs. You can also check out all of our videos by subscribing to our YouTube channel!