IRS Form 4136 Instructions

In the United States, most people are aware of the fact that the Internal Revenue Service (IRS) imposes federal excise taxes on the consumption of fuel. However, if you operate a business that consumes a significant amount of fuel, you may be eligible for a federal fuel tax credit under certain circumstances by filing IRS Form 4136.

This article will walk you through this tax form, so you understand:

- What IRS Form 4136 is used for

- What types of fuel use qualify for fuel credits

- How to complete IRS Form 4136

Let’s start by discussing exactly how to complete IRS Form 4136.

Table of contents

Please note: this article was written for educational purposes only. This should not be considered as tax advice or legal advice. Please consult with your tax professional for technical questions.

How do I complete IRS Form 4136?

We’ll go step by step through each line of this form. Odds are highly unlikely that a single taxpayer will use every line in this form.

Note: The images used here are from the 2021 version of this tax form. At the time of print, the 2022 tax form was available in draft form only. There appear to be a few minor changes from 2021 to 2022. These changes will be pointed out in the respective line.

Line 1: Nontaxable Use of Gasoline

Who can claim this credit

Generally, the ultimate purchaser is the only entity who can claim a tax credit on business use of gasoline.

Allowable uses

A taxpayer may only take a tax deduction for gasoline consumed for business purposes, not for personal purposes. Also, for Lines 1a and 1c, a taxpayer may not make any claim for gasoline used in a motorboat, unless used in commercial fishing (Type of Use 4, above).

For each use, enter the following:

- Type of use (if possible)

- Number of gallons of gasoline used

- Amount of the credit (gallons times applicable rate in Column b)

Additionally, there are only certain uses that qualify for a tax credit:

Off-highway business use

For Line 1a, the gasoline must have been used during the period of claim for a business use other than in a highway motor vehicle registered (or required to be registered) for highway use (type of use 2).

An example might be gasoline used in the operation of a landscaping business.

Use on a farm for farming purposes

For Line 1b, the gasoline must have been used during the period of claim on a farm for farming purposes (type of use 1).

Other nontaxable uses

For Line 1c, the gasoline must have been used during the income tax year for one of the following types of use:

- 4: In a boat engaged in commercial fishing

- 5: In certain intercity and local buses

- 7: School buses

- 11: Exclusive use by a qualified blood collector organization

- 13: Exclusive use by a nonprofit educational organization

- 14: Exclusive use by a state, political subdivision of a state, or the District of Columbia

- 15: In an aircraft or vehicle owned by an aircraft museum

For type of use 13 or 14, the claimant must not have waived the right to make a claim. If the ultimate purchaser waived their right to make a claim, then the registered ultimate vendor may make the claim.

For Line 1d, the gasoline must have been exported during the period of claim (type of use 3). Taxpayers making a claim for exported taxable fuel must keep proof of exportation with their records. Proof of exportation includes one of the following:

- A copy of the export bill of lading issued by the delivering carrier,

- A certificate by the agent or representative of the export carrier showing actual exportation of the fuel,

- A certificate of lading signed by a customs officer of the foreign country to which the fuel is exported, or

- A statement of the foreign consignee showing receipt of the fuel.

Line 2: Nontaxable Use of Aviation Gasoline

Who can claim this credit

Generally, the ultimate purchaser is the only entity who can claim a tax credit on business use of gasoline.

Allowable uses

For each use, enter the following:

- Type of use (if possible)

- Number of gallons used

- Amount of credit (gallons times applicable rate in Column b)

In Line 2b, the aviation gasoline must have been used during the period of claim for one of the following types of use:

- 1: On a farm for farming purposes

- 2: Off-highway business use (for business use other than in a highway vehicle registered or required to be registered for highway use)

- 9: In foreign trade

- 10: Certain helicopter and fixed-wing aircraft

- 11: Exclusive use by a qualified blood collector organization

- 13: Exclusive use by a nonprofit educational organization

- 14: Exclusive use by a state, political subdivision of a state, or the District of Columbia

- 15: In an aircraft or vehicle owned by an aircraft museum

For type of use 13 or 14, the claimant must not have waived the right to make a claim.

Use Line 2b to make a claim for aviation gasoline used outside the propulsion system of an aircraft.

For Line 2c, the taxpayer must have exported the aviation gasoline during the period of claim.

For Line 2d, the taxpayer must have used the aviation fuel in foreign trade to claim a credit for the LUST tax paid (type of use 9).

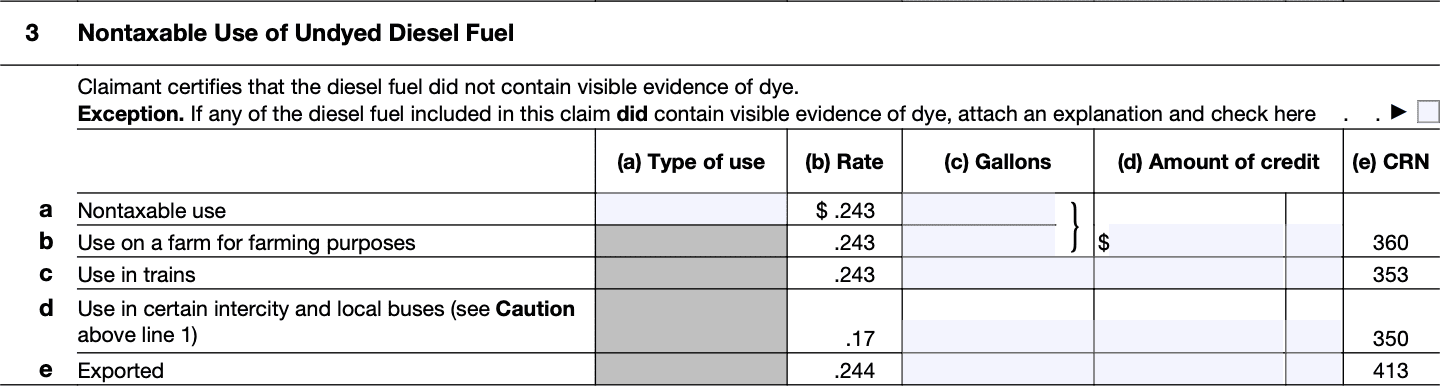

Line 3: Nontaxable Use of Undyed Diesel Fuel

Who can claim this credit

The ultimate purchaser of the diesel fuel is the only person eligible to make this claim.

Allowable uses

For each use, enter the following:

- Type of use (if possible)

- Number of gallons used

- Amount of credit (gallons times applicable rate in Column b)

In Line 3a, the taxpayer must have used the diesel fuel during the period of claim for one of the following types of use:

- 2: Off-highway business use (for business use other than in a highway vehicle registered or required to be registered for highway use)

- 6: In a qualified local bus

- 7: In a bus transporting students and employees of schools (school buses)

- 8: For diesel fuel and kerosene (not used in aviation) used as other than a fuel in the propulsion engine of a train or diesel-powered highway vehicle (not including off-highway business use)

- 11: Exclusive use by a qualified blood collector organization

- 13: Exclusive use by a nonprofit educational organization

- 14: Exclusive use by a state, political subdivision of a state, or the District of Columbia

- 15: In an aircraft or vehicle owned by an aircraft museum

For Line 3d, the claimant must not have waived the right to make a claim.

In Line 3e, the taxpayer must have exported the diesel fuel during the period of claim (type of use 3).

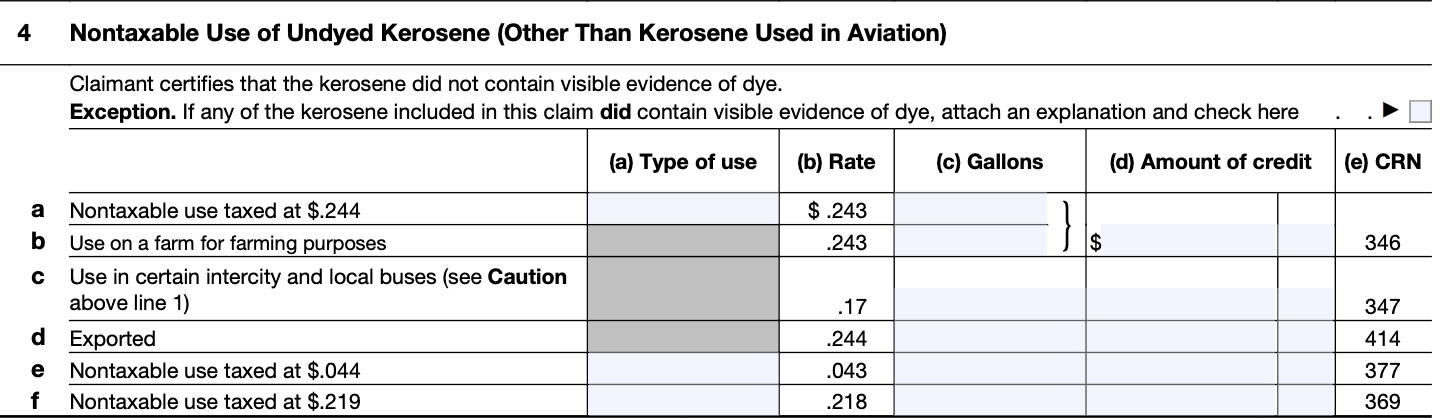

Line 4: Nontaxable Use of Undyed Kerosene (Other than Kerosene Used in Aviation)

Who can claim this credit

The ultimate purchaser of the kerosene is the only person eligible to make this claim.

Allowable uses

For Line 4a, the taxpayer must have used the kerosene during the period of claim for one of the following types of use:

- 2: Off-highway business use (for business use other than in a highway vehicle registered or required to be registered for highway use)

- 6: In a qualified local bus

- 7: In a bus transporting students and employees of schools (school buses)

- 8: For diesel fuel and kerosene (not used in aviation) used as other than a fuel in the propulsion engine of a train or diesel-powered highway vehicle (not including off-highway business use)

- 11: Exclusive use by a qualified blood collector organization

- 13: Exclusive use by a nonprofit educational organization

- 14: Exclusive use by a state, political subdivision of a state, or the District of Columbia

- 15: In an aircraft or vehicle owned by an aircraft museum

Line 4b does not contain kerosene used in aviation for farming purposes. Instead, use Line 5, Kerosene Used in Aviation, below.

For Line 4d, the taxpayer must have exported the kerosene during the period of claim.

For Lines 4e and 4f, the taxpayer must have used the kerosene during the period of claim for off-highway business use (type of use 2).

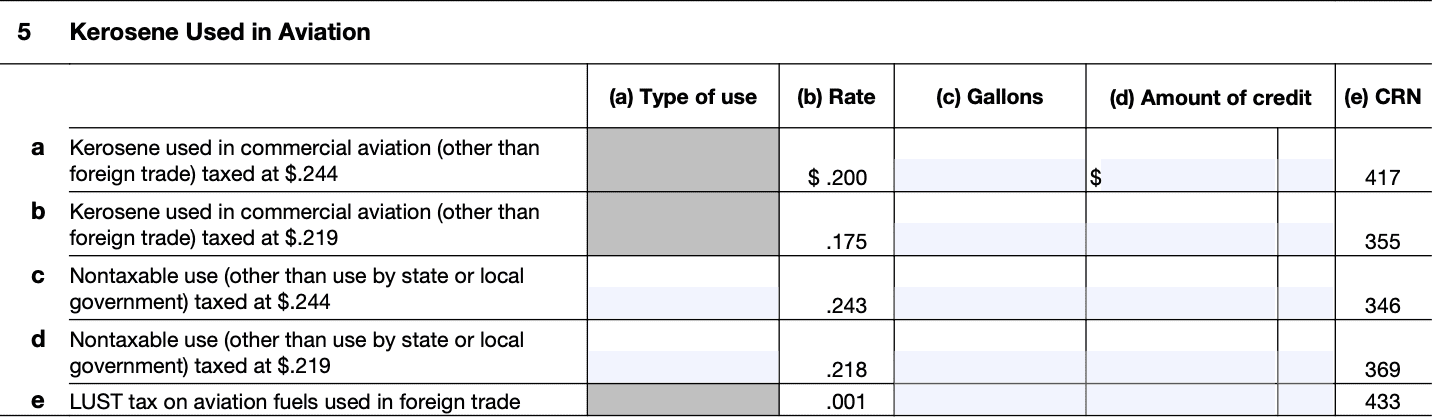

Line 5: Kerosene Used in Aviation

Who can claim this credit

For Lines 5a and 5b, the ultimate purchaser of kerosene used in commercial aviation (other than foreign trade) is eligible to make this claim.

For Lines 5c, 5d, and 5e, the ultimate purchaser of kerosene used in noncommercial aviation (other than nonexempt, noncommercial aviation and exclusive use by a state, political subdivision of a state, or the District of Columbia) is eligible to make this claim.

Allowable uses

For Lines 5a and 5b, the taxpayer must have used the kerosene during the period of claim in commercial aviation.

If a taxpayer purchases kerosene partially for commercial aviation use and partially for noncommercial aviation use, Notice 2005-80 applies.

For Lines 5c and 5d, the kerosene must have been used during the period of claim for one of the following types of use:

- 1: On a farm for farming purposes

- 9: In foreign trade

- 10: Certain helicopter and fixed-wing aircraft

- 11: Exclusive use by a qualified blood collector organization

- 13: Exclusive use by a nonprofit educational organization

- 14: Exclusive use by a state, political subdivision of a state, or the District of Columbia

- 15: In an aircraft or vehicle owned by an aircraft museum

- 16: In military aircraft

For Line 5e, the kerosene must have been used during the period of claim for type of use 9. This claim is made in addition to the claim made on Lines 5c and 5d for type of use 9.

Depending on the tax rate of the kerosene, use Line 4a, 4e, or 4f, under Nontaxable Use of Undyed Kerosene (Other than Kerosene Used in Aviation), to make a claim for kerosene used outside the propulsion system of an aircraft.

Line 6: Sales by Registered Ultimate Vendors of Undyed Diesel Fuel

Who can claim this credit

For Line 6a, only the registered ultimate vendor may make this claim. Under Line 6b, the registered ultimate vendor may make a claim only if the buyer waives his or her right to claim. The buyer does this by providing the registered ultimate vendor with an unexpired waiver.

To make an ultimate vendor claim under Line 6, you must have registered using IRS Form 637, Application for Registration (for certain excise tax activities).

Enter your registration number, including the prefix, on the applicable line for your claim.

Allowable uses

The taxpayer must have sold the fuel during the period of claim for the exclusive use by one or more state or local governments. This includes essential government use by an Indian tribal government.

For claims on Line 6a, attach a separate statement with the name and TIN of each governmental unit to whom the diesel fuel was sold and the number of gallons sold to each.

IRS rules allow only one claim for each gallon of diesel fuel.

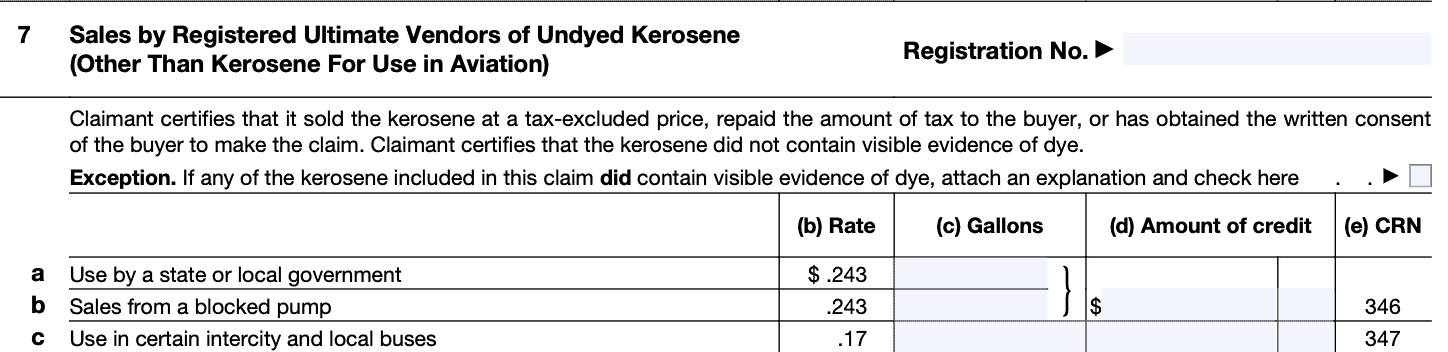

Line 7: Sales by Registered Ultimate Vendors of Kerosene (Other than Kerosene For Use in Aviation)

Who can claim this credit

For Line 7a, only the registered ultimate vendor may make this claim. For Line 7b, the claimant must have a statement that contains the following:

- Date of sale

- Name and address of the buyer

- Number of gallons of kerosene sold to the buyer

Under Line 7c, the registered ultimate vendor may make a claim only if the buyer waives his or her right to claim by providing an unexpired waiver to the vendor.

To make an ultimate vendor claim under Line 7, you must have registered using IRS Form 637, Application for Registration (for certain excise tax activities).

Enter your registration number, including the prefix, on the applicable line for your claim.

Allowable uses

Under Line 7a, the taxpayer must have sold the kerosene for use by a state or local government. For Line 7b, the sales must have occurred from a blocked pump.

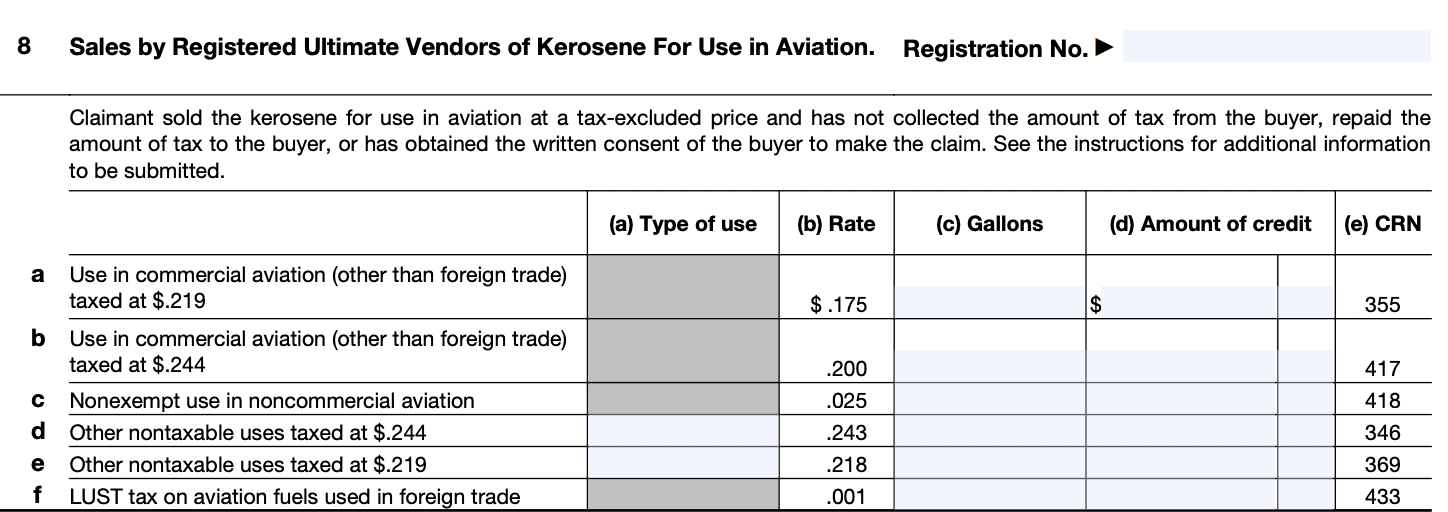

Line 8: Sales by Registered Ultimate Vendors of Kerosene For Use in Aviation

Who can claim this credit

For Lines 8a, 8b, 8d, 8e, and 8f, the registered ultimate vendor of the kerosene sold for use in commercial aviation is eligible to make this claim only if the buyer waives his or her right by providing the registered ultimate vendor with an unexpired waiver. Publication 510 has an example of this waiver in the appendix.

For Line 8c, the registered ultimate vendor of the kerosene sold for use in nonexempt, noncommercial aviation is the only person eligible to make this claim.

To make an ultimate vendor claim under Line 8, you must have registered using IRS Form 637, Application for Registration (for certain excise tax activities).

Enter your registration number, including the prefix, on the applicable line for your claim.

Allowable uses

For Lines 8a and 8b, the vendor must have sold the kerosene for use in commercial aviation during the period of claim for use in commercial aviation (other than foreign trade). Under Line 8c, the vendor must have sold the kerosene for a nonexempt use in noncommercial aviation.

For Lines 8d and 8e, the taxpayer must have sold the kerosene for use in noncommercial aviation during the period of claim for one of the following types of use:

- 1: On a farm for farming purposes

- 9: In foreign trade

- 10: Certain helicopter and fixed-wing aircraft

- 11: Exclusive use by a qualified blood collector organization

- 13: Exclusive use by a nonprofit educational organization

- 14: Exclusive use by a state, political subdivision of a state, or the District of Columbia

- 15: In an aircraft or vehicle owned by an aircraft museum

- 16: In military aircraft

In Line 8f, the kerosene must have been sold in foreign trade.

Line 9: Reserved for Future Use

The IRS has kept this line reserved for future use.

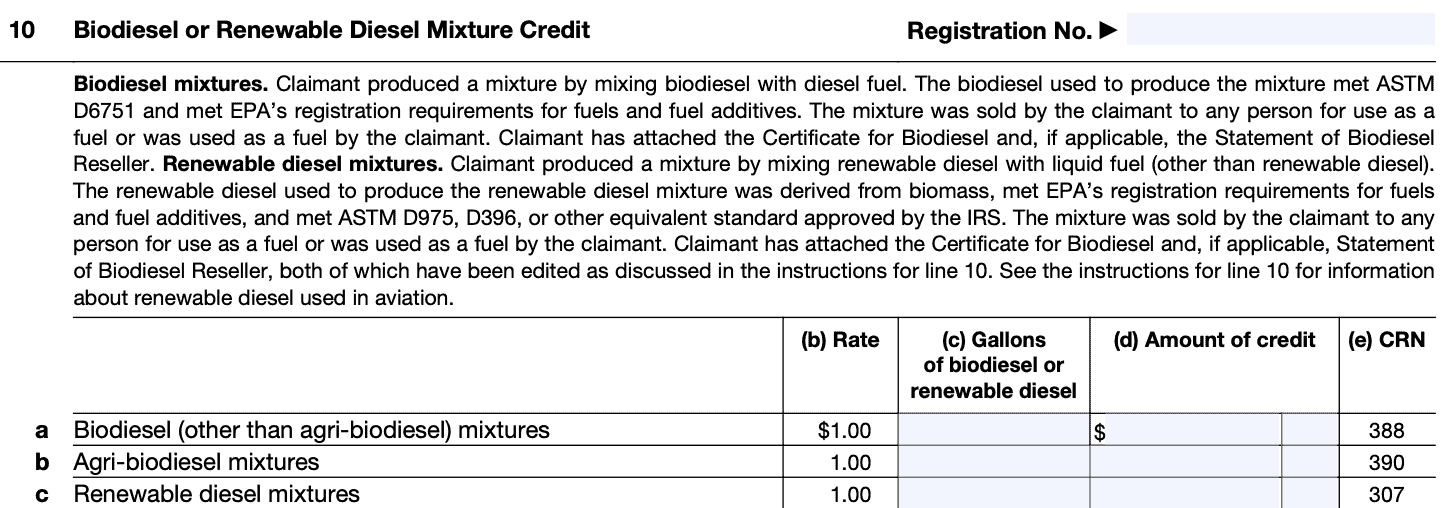

Line 10: Biodiesel or Renewable Diesel Mixture Credit

Who can claim this credit

The person that produced and sold or used the mixture in their trade or business is the only person eligible to make this claim. The biodiesel mixture credit is based on the gallons of biodiesel or renewable diesel in the fuel mixture.

Additionally, the biodiesel or renewable diesel must meet certain ASTM and EPA requirements as outlined in the form instructions.

Allowable uses

The Certificate for Biodiesel and, if applicable, Statement of Biodiesel Reseller must be attached to the first claim filed that is supported by the certificate or statement. If this isn’t possible, the claimant must attach a separate statement, containing the following:

- Certificate identification number.

- Total gallons of biodiesel or renewable diesel on certificate.

- Total gallons claimed on Schedule 3 (from IRS Form 8849).

- Total gallons claimed on Form 720, Schedule C, line 12.

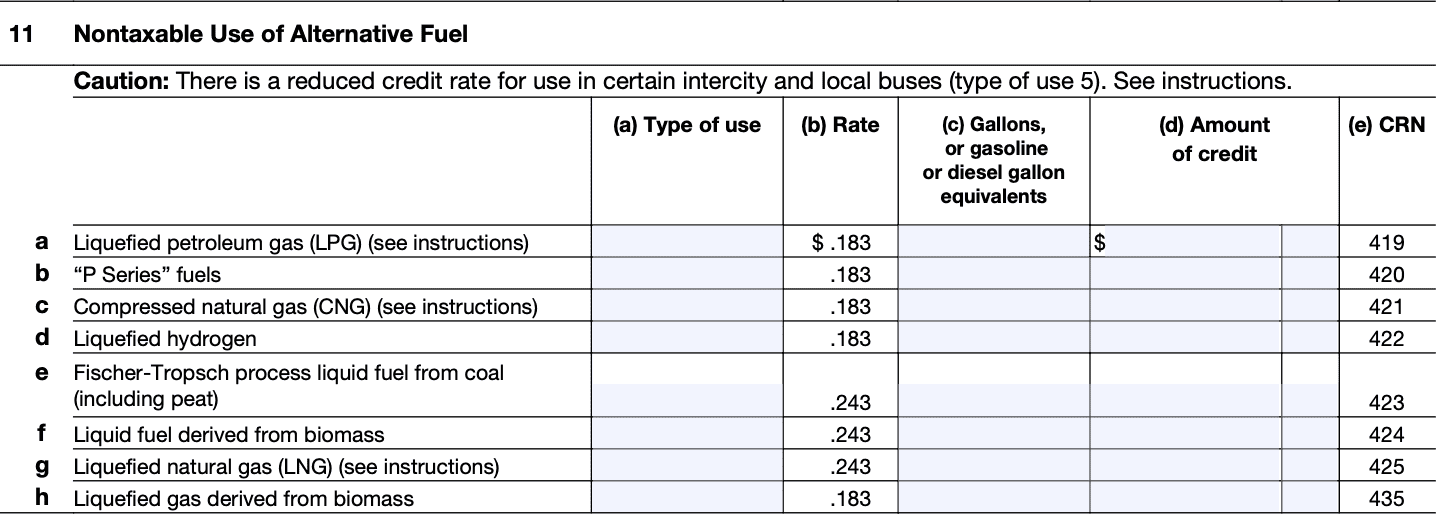

Line 11: Nontaxable Use of Alternative Fuel

Who can claim this credit

The ultimate purchaser of the taxed alternative fuel is the only person eligible to make this claim under Line 11.

Allowable uses

The alternative fuel must have been used during the period of claim for one of the following types of use:

- 1: On a farm for farming purposes

- 2: Off-highway business use (for business use other than in a highway vehicle registered or required to be registered for highway use)

- 4: In a boat engaged in commercial fishing

- 5: In certain intercity and local buses

- 6: In a qualified local bus

- 7: In a bus transporting students and school employees (school buses)

- 11: Exclusive use by a qualified blood collector organization

- 13: Exclusive use by a nonprofit educational organization

- 14: Exclusive use by a state, political subdivision of a state, or the District of Columbia

- 15: In an aircraft or vehicle owned by an aircraft museum

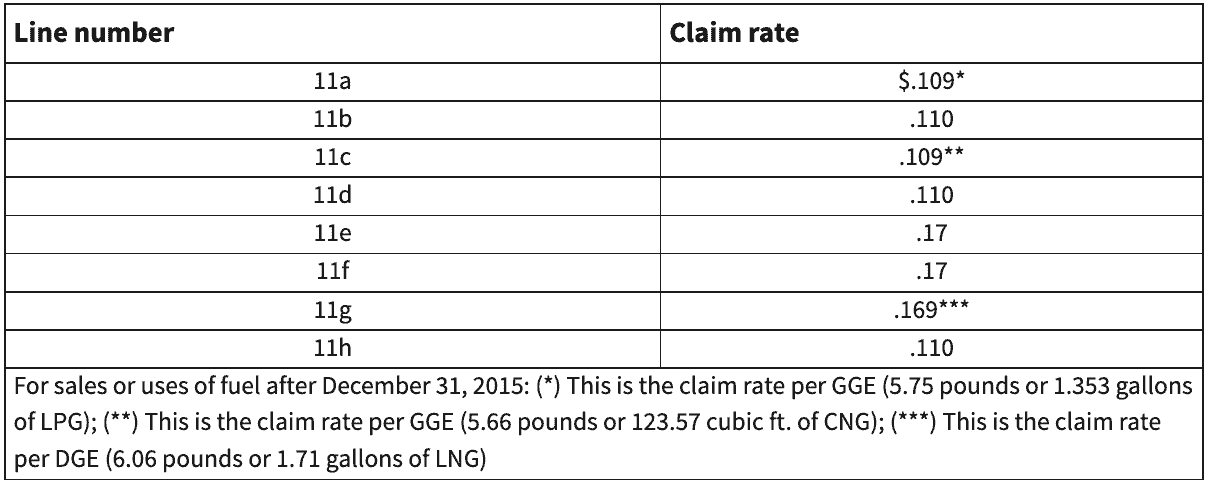

For type of use 5, write ‘Bus’ to the left of column (a), and use the appropriate claim rate outlined below.

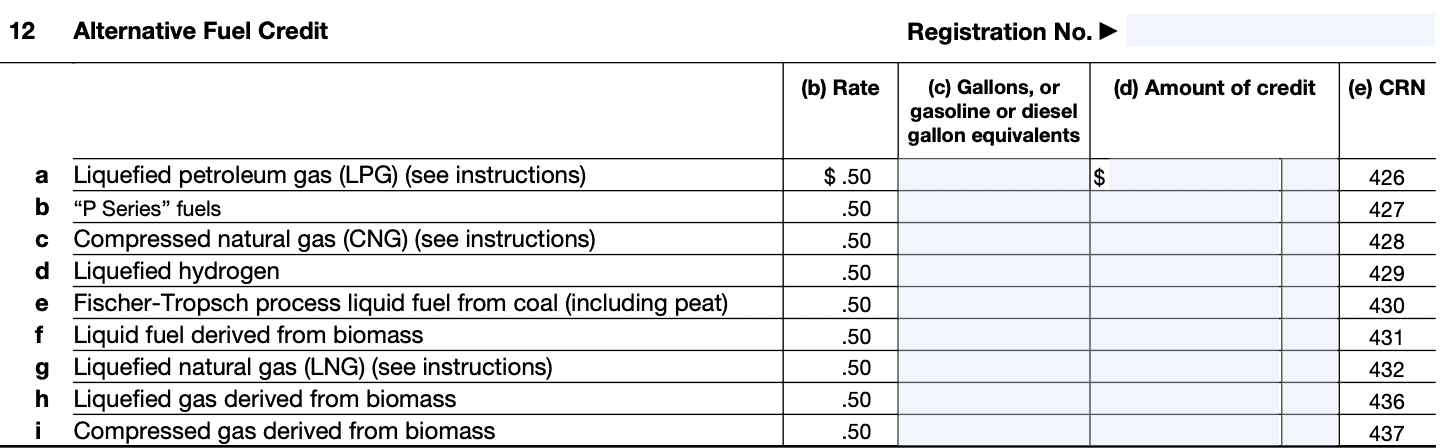

Line 12: Alternative Fuel Credit

Who can claim this credit

Taxpayers cannot claim the alternative fuel mixture credit on this form, only the alternative fuel credit. A taxpayer seeking to claim the alternative fuel mixture credit must file IRS Form 8849, Claim for Refund of Excise Taxes.

Only the following registered alternative fuelers are eligible to make a claim:

- One who sold alternative fuel at retail and delivered it into the fuel supply tank of a motor vehicle or motorboat

- One who sold an alternative fuel, delivered it in bulk for taxable use in a motor vehicle or motorboat, and received the required statement from the buyer

- One who used an alternative fuel (not sold at retail or in bulk as previously described) in a motor vehicle or motorboat

- One who sold an alternative fuel for use as a fuel in aviation

Allowable uses

Any alternative fuel credit must first be taken on IRS Form 720, Schedule C, to reduce your taxable fuel liability reported on Form 720.

Any excess alternative fuel credit may be taken on:

- Form 720, Schedule C;

- IRS Form 4136; or

- Schedule 3 (Form 8849)

Line 13: Registered Credit Card Issuers

Who can claim this credit

The registered credit card issuer is the only person eligible to make this claim if the credit card issuer:

- Is registered by the IRS;

- Has either:

- Not collected the amount of tax from the ultimate purchaser or

- Obtained the written consent of the ultimate purchaser to make the claim;

- Does one of the following:

- Certifies that it has repaid or agreed to repay the amount of tax to the ultimate vendor,

- Obtains the written consent of the ultimate vendor to make the claim, or

- Otherwise makes arrangements which directly or indirectly provide the ultimate vendor with reimbursement of the tax; and

- Has in its possession an unexpired certificate from the ultimate purchaser and has no reason to believe any of the information in the certificate is false.

If any of these conditions is not met, the credit card issuer must collect the tax from the ultimate purchaser. Only the ultimate purchaser can make the claim.

Allowable sales

The diesel fuel, kerosene, or kerosene for use in aviation must have been purchased:

- With a credit card issued to the ultimate purchaser during the period of claim

- For the exclusive use by a state or local government

- This includes essential government use by an Indian tribal government

Line 14: Nontaxable Use of a Diesel-Water Fuel Emulsion

Who can claim this credit

The ultimate purchaser of the diesel-water fuel emulsion is the only person eligible to make this claim.

Allowable uses

For Line 14a, the diesel-water fuel emulsion must have been used during the period of claim for one of the following types of use:

- 1: On a farm for farming purposes

- 2: Off-highway business use (for business use other than in a highway vehicle registered or required to be registered for highway use)

- 5: In certain intercity and local buses

- 6: In a qualified local bus

- 7: In a bus transporting students and school employees (school buses)

- 8: For diesel fuel and kerosene (not used in aviation) used as other than a fuel in the propulsion engine of a train or diesel-powered highway vehicle (not including off-highway business use)

- 11: Exclusive use by a qualified blood collector organization

- 13: Exclusive use by a nonprofit educational organization

- 14: Exclusive use by a state, political subdivision of a state, or the District of Columbia

- 15: In an aircraft or vehicle owned by an aircraft museum

For Line 14b, the diesel-water fuel emulsion must have been exported during the period of claim.

If using ‘Type of Use’ 5, do the following:

- Write “Bus” in the space to the left of column (a)

- Enter the correct claim rate in column (b). The claim rate for type of use 5 is $.124 per gallon.

Line 15: Diesel-Water Fuel Emulsion Blending

Who can claim this credit

The person that produced (the blender) and sold or used the diesel-water fuel emulsion is the only person eligible to make this claim.

Allowable uses

The blender must attach a statement to the claim certifying that:

- The diesel-water fuel emulsion contains at least 14% water,

- The emulsion additive is registered by a U.S. manufacturer with the EPA under Section 211 of the Clean Air Act,

- Undyed diesel fuel taxed at $.244 was used to produce the diesel-water fuel emulsion, and

- The diesel-water fuel emulsion was used or sold for use in the blender’s trade or business

Line 16: Exported Dyed Fuels and Exported Gasoline Blendstocks

Who can claim this credit

Only the person that exported dyed diesel fuel or dyed kerosene during the period of claim can make this claim.

Line 17: Total Income Tax Credit Claimed

For Line 17, add the totals of column (d) for Lines 1 through 16. Enter the sum on Line 17 and on the appropriate line as follows:

- Line 12, Schedule 3 (IRS Form 1040)

- Line 20b, Schedule J (IRS Form 1120)

- Line 23c, IRS Form 1120-S

- Line 16b, Schedule G (IRS Form 1041)

- Proper line on other returns as appropriate

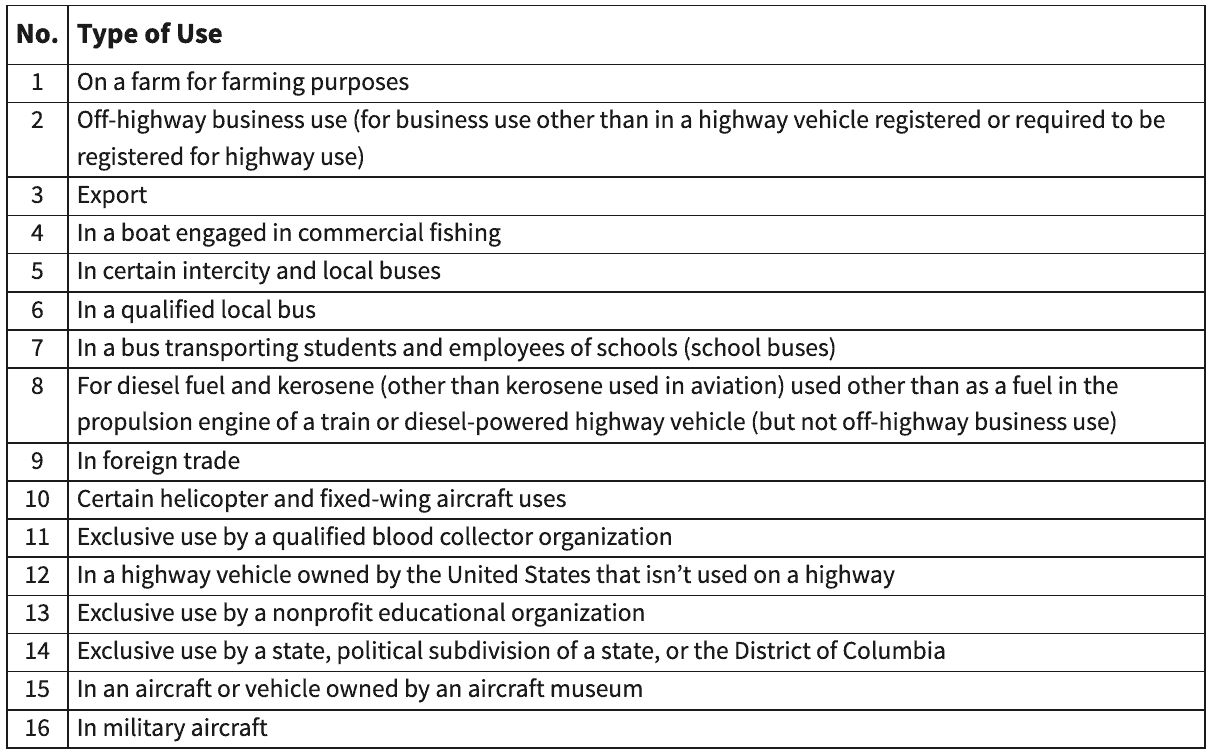

What is considered qualified nontaxable fuel use?

In the fuel industry, fuel and other petroleum products can be purchased, stored, resold, or transferred many times before becoming consumed. In most cases, the ultimate fuel user is the only entity that can claim a tax credit against their tax bill.

Below is a chart that depicts the qualifying purpose, and a corresponding code that the taxpayer must use on Form 4136.

For example, a horse farmer using fuel on a farm for farming purposes would enter 1 in the Type of use column when filing Form 4136.

Video walkthrough

Watch this instructional video to learn more about claiming the credit for federal taxes paid on fuels using IRS Form 4136.

Frequently asked questions

IRS Form 4136, Credit for Federal Tax Paid on Fuels, enables certain taxpayers to claim a fuel credit, depending on the type of fuels used, and the type of business use the credit is claimed for.

No. You may claim a refund for excise taxes on IRS Form 8849, or claim credits on your quarterly excise tax return using IRS Form 720. However, you cannot use Form 4136 to claim amounts previously claimed on either Form 8849 or Form 720.

Where can I find a copy of IRS Form 4136?

You may download a PDF copy of this form from the IRS website. For your convenience, we’ve enclosed the most recent version of the form below.

Related tax articles

This tax form is one of the fillable tax forms provided by the Internal Revenue Service, to help taxpayers reduce their tax preparation costs. To see more forms like this, visit our free fillable tax forms page, where you’ll also find articles like this.

Unlike the IRS, our articles contain step by step instructions for each tax form, as well as video walkthroughs. You can also check out all of our videos by subscribing to our YouTube channel!