IRS Form 8862 Instructions

If you claimed certain tax credits on your income tax return, but later found out that the Internal Revenue Service disallowed them, you may have options. By filing IRS Form 8862, you may be able to provide additional information and demonstrate that you meet the requirements for that tax credit.

In this article, we’ll walk through IRS Form 8862, including:

- What types of tax credits you may claim with this form

- When you should file Form 8862 and when you should not

- How to complete Form 8862

Let’s start with a primer on what this tax form is.

Table of contents

How do I complete IRS Form 8862?

There are 5 parts to this tax form. However, you only need to complete the parts that pertain to your specific tax situation.

We’ll walk through each part, step by step.

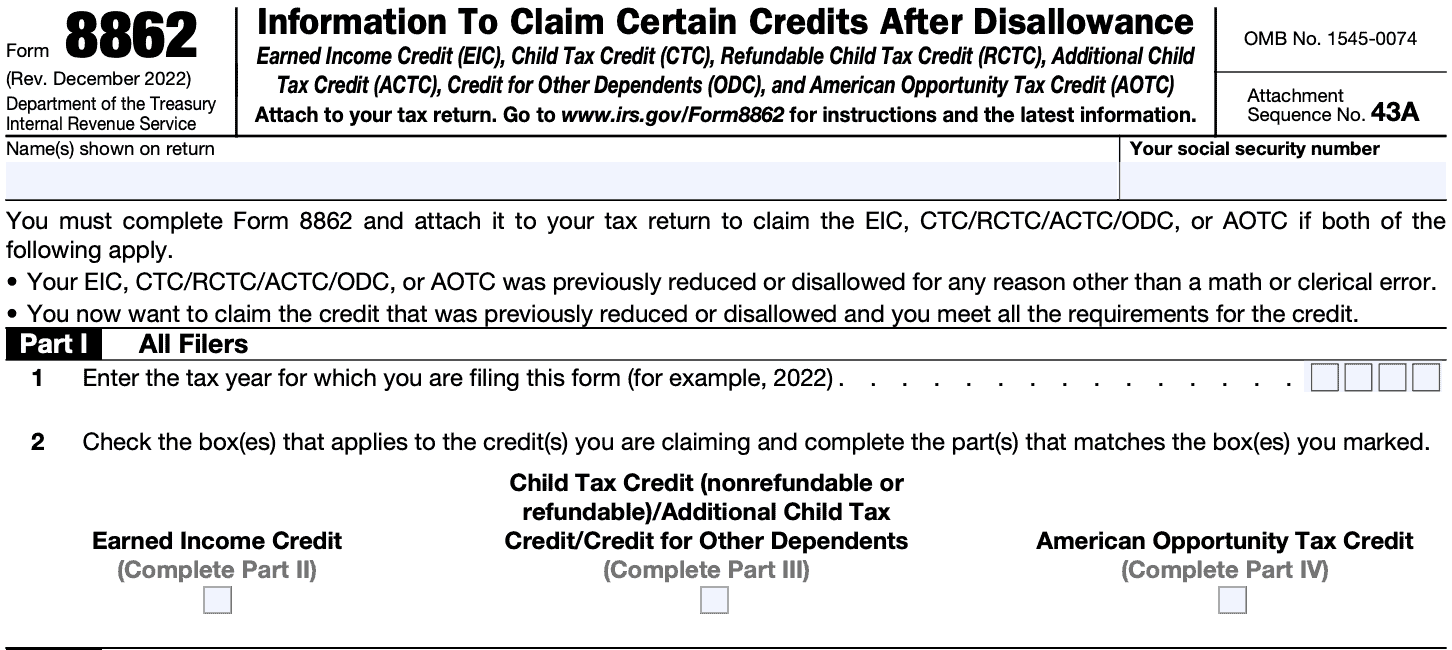

Part I: All Filers

Regardless of which credit you’re claiming, every taxpayer must complete Part I, after entering your name and SSN as shown on the rest of your tax return.

Line 1: Tax year

Enter the tax year for which you are filing this form. Do not enter the tax year in which the credit was reduced or disallowed.

For example, if filing with your 2022 tax return for a credit that was disallowed in 2021, you would enter 2022 in Line 1.

Line 2: Tax credit(s)

Check the appropriate box. If applicable, you can select more than one.

After completing Line 2, proceed to the next applicable part.

- Part II: EIC

- Part III: CTC/ACTC/ODC

- Part IV: AOTC

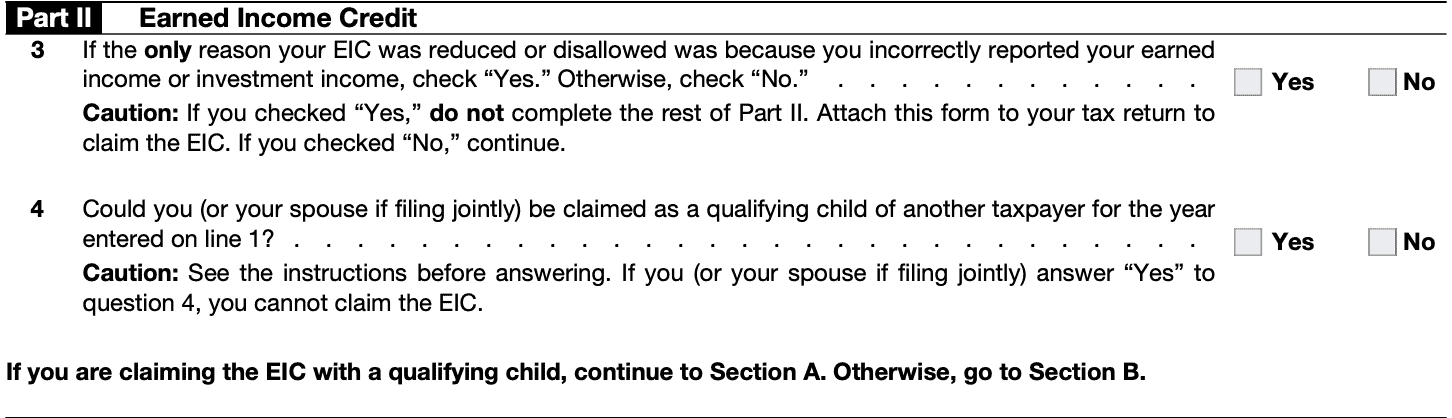

Part II: Earned Income Credit

There are 2 questions to Part II, then there are two sections.

- Section A: For taxpayers claiming the EIC with a qualifying child

- Section B: For taxpayers claiming the EIC without a qualifying child

Line 3

If the only reason your EIC was reduced or disallowed was because you incorrectly reported earned income or investment income, check “Yes.” Otherwise, check “No” and continue to Line 4.

If you checked “Yes,” you do not need to complete the rest of Part II. Simply attach your Form 8862 to your tax return to claim the EIC.

Line 4

If another taxpayer can claim either you or your spouse as a qualifying child for the tax year, then you cannot claim the EIC.

For taxpayers claiming the EITC with a qualifying child, proceed to Section A. If not, go to Section B.

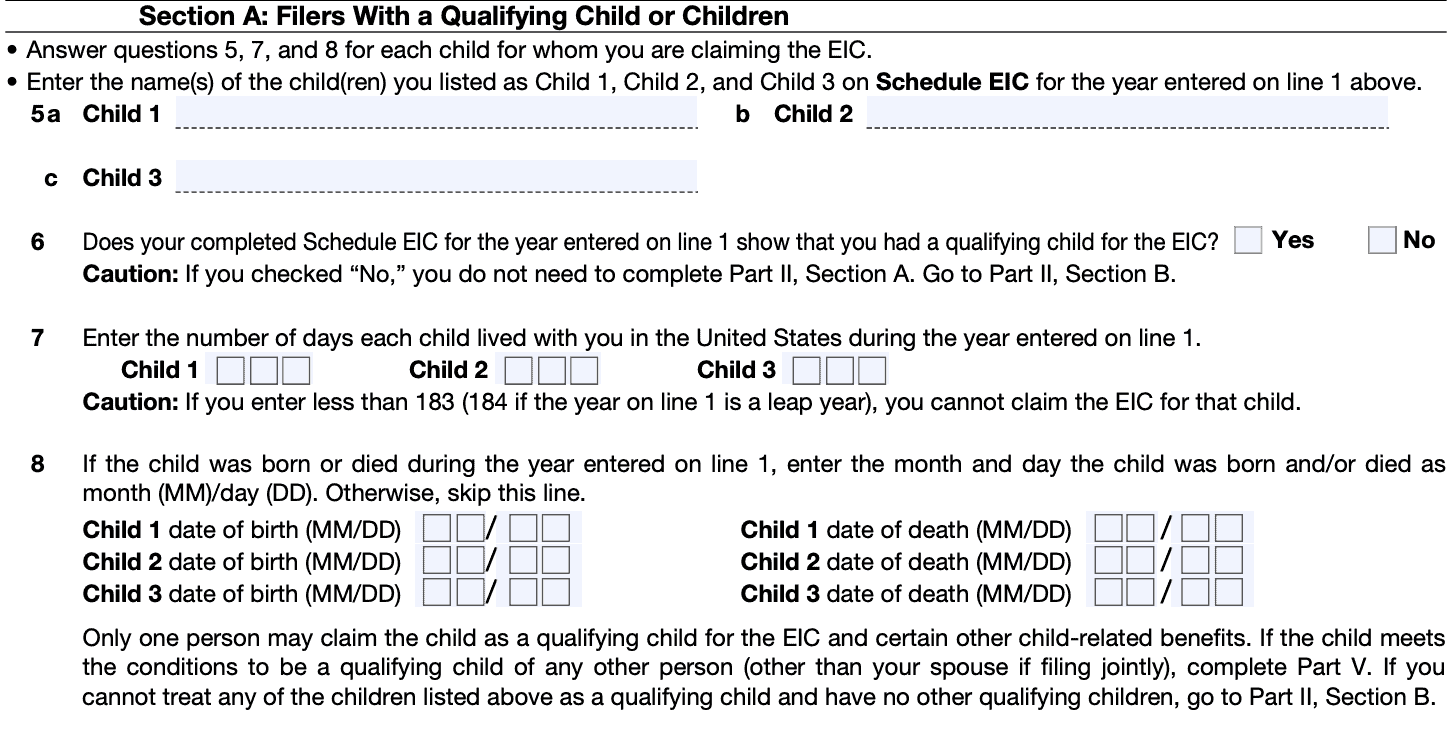

Line 5: Name of Child(ren)

Enter the names of the children that you listed on Schedule EIC for the given tax year.

Line 6: Qualifying child?

If your completed Schedule EIC shows that you have a qualifying child, then continue to Line 7. If not, go directly to Section B.

Line 7: Number of days each child lived with you in the United States

Enter the number of days each child lived with you in the United States

Line 8

If a child was born or died during the year, enter the date of birth or date of death in the line. Otherwise, proceed to one of the following:

- Part V: If the child meets the conditions to be a qualifying child for any other person

- Section B: If you cannot treat any of the listed children as a qualifying child and you have no other qualifying children

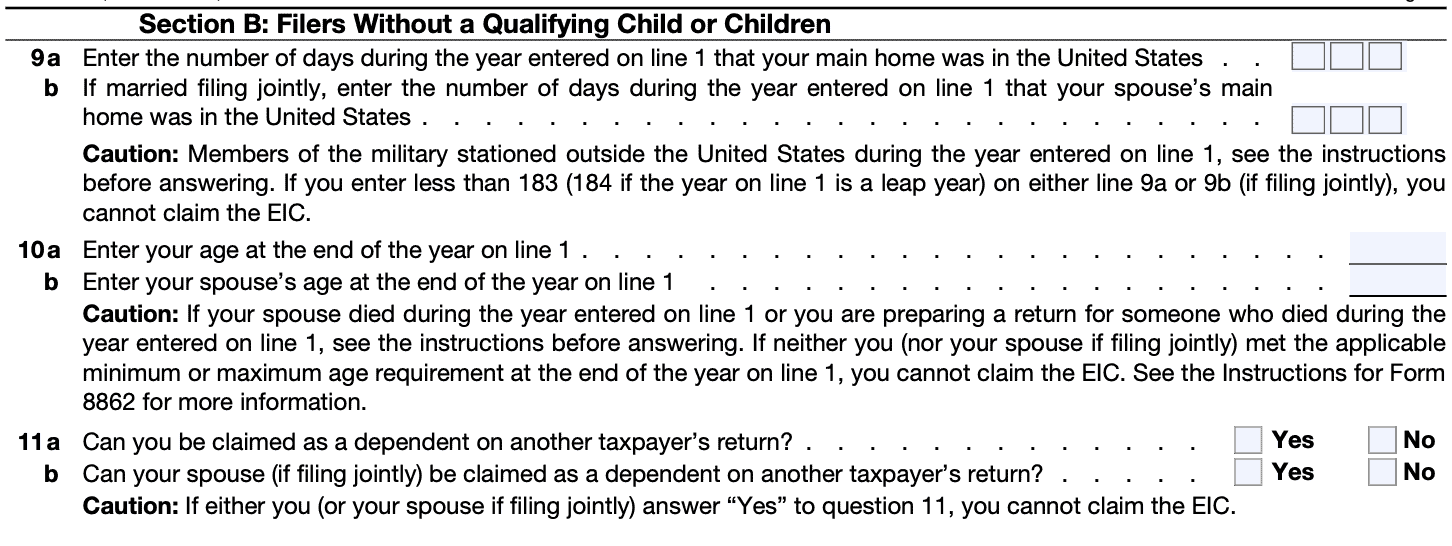

If you do not have a qualifying child, you must complete Section B.

Line 9

In Line 9a, enter the number of days that you main home was in the United States

Line 9b: If you’re married filing a joint return, enter the number of days your spouse’s main home was in the United States.

For servicemembers: If you are on extended active duty outside the United States, the IRS considers your main home to be in the United States during that time.

Extended active duty is military duty ordered for an indefinite period or for a period of more than 90 days. Once ordered to extended active duty, your assignment is considered so, even if you do not serve 90 days or more.

Line 10

Enter your age at the end of the tax year in Line 10a. If married, enter your spouse’s age at the end of the year in Line 10b.

If your spouse died during the year, or you’re preparing a return for someone who died during the year, see the form instructions for additional guidance. Taxpayers who cannot meet the applicable age requirements cannot claim the EIC.

Line 11: Can you (or your spouse) be claimed as a dependent on another taxpayer’s return?

Select ‘Yes’ to either one that applies. If either you or your spouse can be claimed, then you cannot claim the EIC.

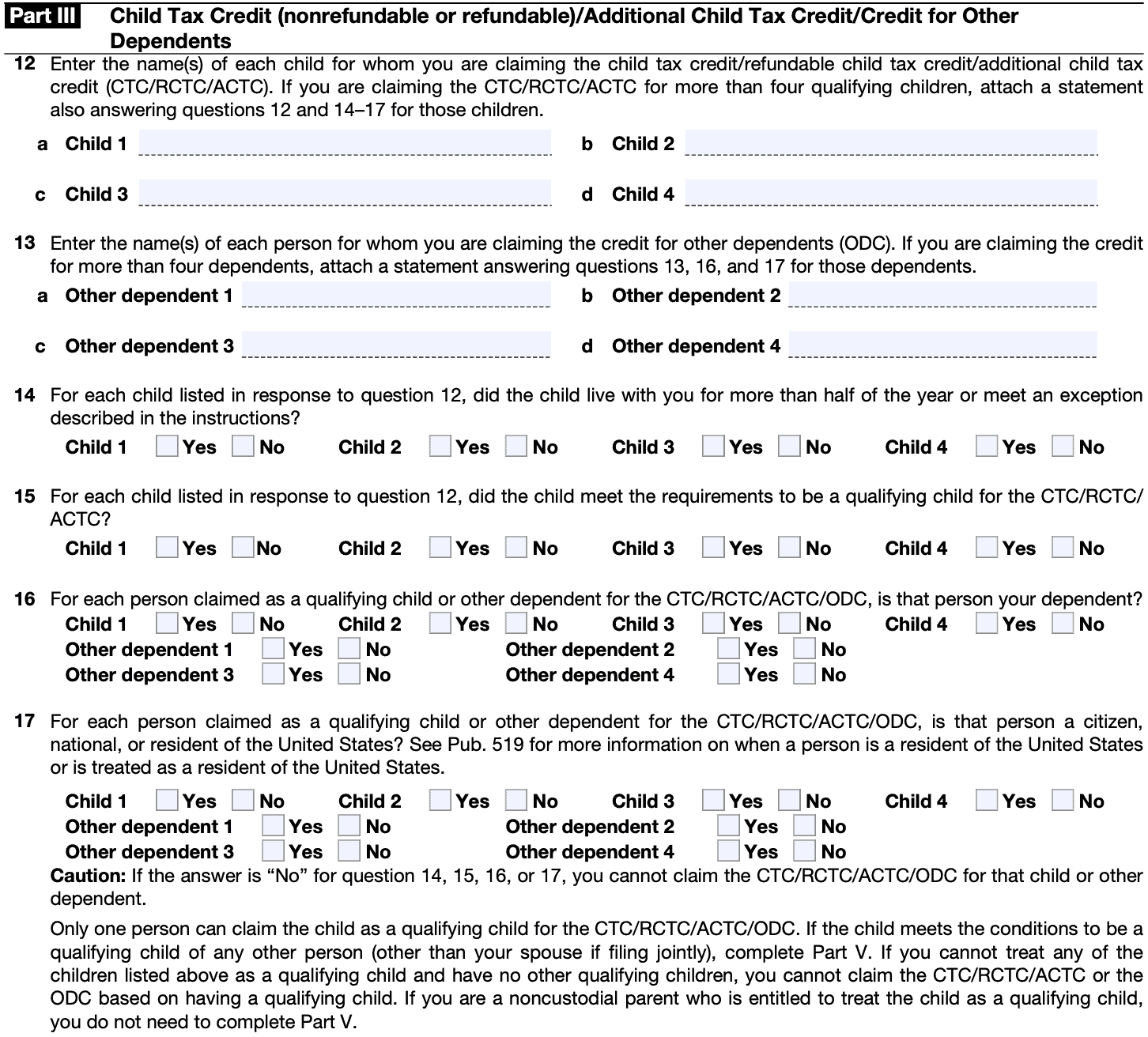

Part III: Child Tax Credit/Additional Child Tax Credit/Credit for Other Dependents

Complete Part III if applying for the CTC, RCTC, ACTC, or ODC

Line 12: Name of child(ren)

Enter the names of the children for which you are claiming one of the following:

- CTC

- RCTC

- ACTC

If claiming a credit for more than 4 qualifying children, attach supporting documentation that answers questions 12 and 14-17 for those individuals.

Line 13: Name of dependents

Enter the names of the dependents for which you are claiming the credit for other dependents.

If claiming a credit for more than 4 qualifying children, attach supporting documentation that answers questions 13, 16, and 17 for those individuals.

Line 14: Did the child live with you for more than half of the year or meet an exception outlined in the instructions?

Exceptions exist for kidnapped children and children of divorced or separated parents. Generally, if a child did not live with you for more than half the year or meet an exception, then you cannot claim the tax credit.

Line 15: Did the child meet the requirements to be a qualifying child for the CTC/RCTC/ACTC?

Select the answer that applies to each individual.

Generally, a qualifying child is one who meets the following criteria:

- Is your son, daughter, stepchild, foster child, brother, sister, stepbrother, stepsister, half brother, half sister, or a descendant of any of them (for example, your grandchild, niece, or nephew)

- Was under age 18 at the end of the year

- Did not provide over half of his or her own support for the year

- Lived with you for more than half of the year

- Is claimed as a dependent on your return

- Does not file a joint return for the year

- Can file a return if solely to claim a refund of withheld income tax or estimated tax paid

- Was a U.S. citizen, a U.S. national, or a U.S. resident alien

Line 16: Is the claimed person YOUR dependent?

Select the answer that applies to each individual. You may not claim a credit on behalf of an individual who is not your dependent.

Line 17: Citizenship status

If the claimed person was either a resident, national, or citizen, select “Yes.” Otherwise, select “No.” IRS Publication 519, U.S. Tax Guide for Aliens, contains more information about citizenship status.

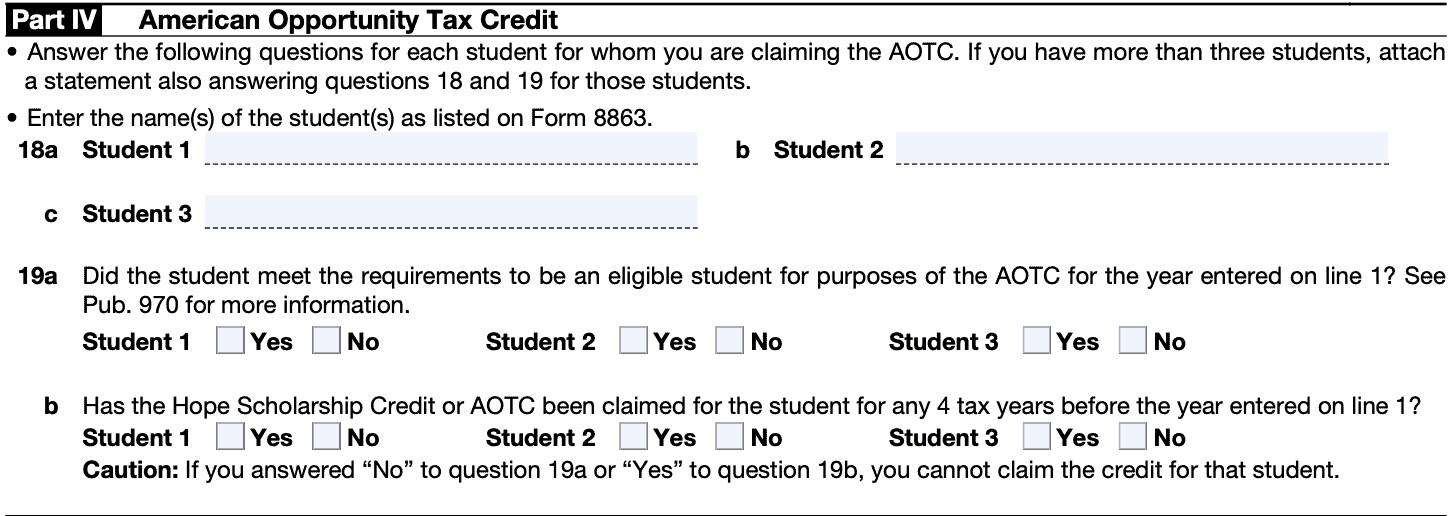

Part IV: American Opportunity Tax Credit

Answer Questions 18 and 19 for each student for whom you are claiming the AOTC. If you have more than 3 students, attach a supporting statement with answers to Questions 18 and 19 for those individuals.

Line 18: Student name

An eligible student meets the following criteria:

Enter the person’s name in the applicable line.

Line 19: Did student meet the requirements?

Below are the requirements to qualify for the AOTC:

- The student did not have expenses that were used to figure an AOTC in any 4 earlier tax years.

- Includes any tax year(s) in which the Hope scholarship credit was claimed for the same student.

- The student had not completed the first 4 years of post-secondary education before the year on Line 1.

- Generally, freshman, sophomore, junior, and senior years of college

- For at least one academic period beginning in the year on Line 1, the student was enrolled at least half-time in a program leading to a degree, certificate, or other recognized educational credential.

- Can be the first 3 months of the following year if the qualified expenses were paid in the previous year

- The student has not been convicted of any federal or state felony for possessing or distributing a controlled substance as of the end of the year on Line 1.

Check IRS Publication 970, Tax Benefits for Education, if you are not sure of the AOTC criteria.

If you answered either “No” to Question 19a or “Yes” to Question 19b, then you cannot claim the AOTC for that student.

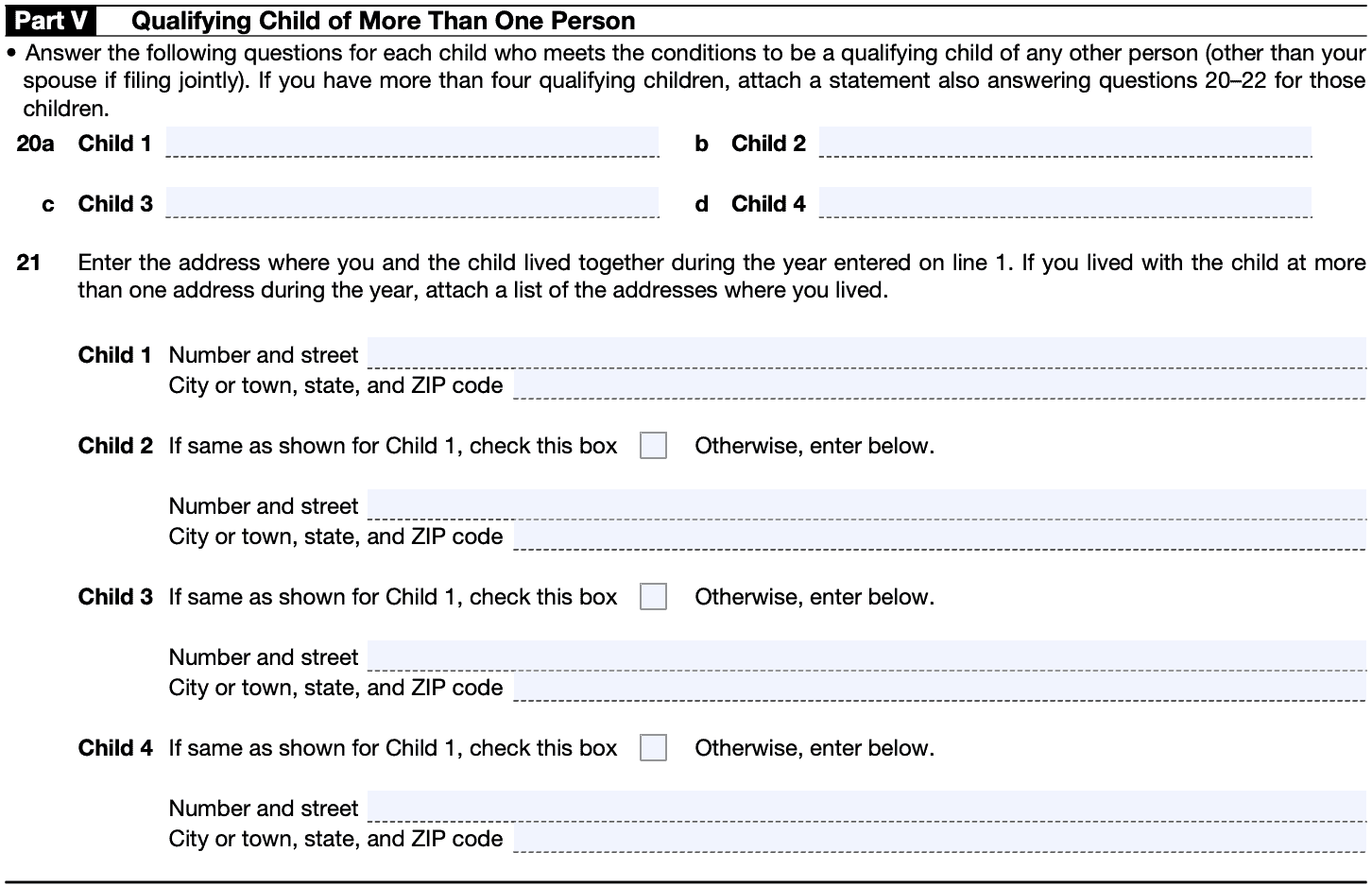

Part V: Qualifying Child of More than One Person

Answer Part V for any child who could be considered a qualifying child for any other taxpayer. If you have more than 4 qualifying children, attach a supporting statement with the answers to Lines 20-22.

IRS Publication 501 contains additional information in cases where multiple taxpayers can claim a qualifying child for tax credit purposes.

Line 20: Name of qualifying child

Enter the child’s name in each line.

Line 21: Address child lived

Enter the address where you and your child lived during the tax year. If you and the child lived at multiple addresses, attach a list of the addresses where you lived.

Enter the number, street, city/town, state, and zip code for each address.

Line 22

If any other person lived with a named child for more than half the tax year, enter “Yes.” Then enter the relationship of each person to the child on the appropriate line.

If no one else (other than your spouse and dependents you claim on your income tax return) lived with the child, enter “No.”

When completed, attach IRS Form 8862 to your income tax return for the year listed in Line 1.

Video walkthrough

Watch this instructional video to learn more about claiming a previously disallowed tax credit by filing IRS Form 8862.

Frequently asked questions

IRS Form 8862, Information to Claim Certain Credits After Disallowance, is the federal form that a taxpayer may use to claim certain tax credits that were previously disallowed.

Taxpayers may use Form 8862 to claim one or more of the following tax credits: earned income credit (EIC), child tax credit (CTC), refundable child tax credit (RCTC), additional child tax credit (ACTC), credit for other dependents (ODC), and the American Opportunity Tax Credit (AOTC).

To use this form and claim the appropriate tax credit, a taxpayer must meet the tax credit requirements, and the IRS must have previously reduced or disallowed the tax credit due to a reason other than a math error or clerical mistake.

When should I file IRS Form 8862?

According to the form instructions, a taxpayer must file and attach Form 8862 to their federal tax return for a tax credit that was previously reduced or disallowed for any reason other than a math or clerical error under the following circumstances:

- Earned income tax credit was disallowed in a taxable year after 1996

- Any of the following were disallowed in a previous tax year after 2015:

- CTC: Child Tax Credit

- RCTC: Refundable Child Tax Credit

- ACTC: Additional Child Tax Credit

- ODC: Credit for Other Dependents

- AOTC: American Opportunity Tax Credit

However, there are certain exceptions to this as well.

When should I NOT file IRS Form 8862?

There are two types of situations in which a taxpayer should not file form 8862:

- Situations that qualify for the tax credit without having to file

- Situations in which the taxpayer remains ineligible for the tax credit

Qualify without having to refile

You do not need to file Form 8862 to qualify for the tax credit if one of the following applies:

- If, after your tax credit was reduced or disallowed in an earlier year,

- You filed Form 8862 or other documents, after which the IRS allowed your credit, and

- Your credit has not been reduced or disallowed again in subsequent years for any reasons other than a math or clerical error.

- You are claiming the EIC without a qualifying child and the only reason your EIC claim was reduced or disallowed in the prior year was because it was determined that a child listed on Schedule EIC was not your qualifying child.

Ineligible to file

If one of the following applies to your tax situation, filing Form 8862 will not help you:

- If you are within 2 years after the most recent tax year for which there was a final determination that your taxpayer’s claim was due to reckless or intentional disregard of the rules, or

- If you are within 10 years after the most recent tax year for which there was a final determination that your tax credit claim was due to fraud.

In either of these cases, you cannot take the credit(s).

Refundable tax credits vs. nonrefundable tax credits

Before we go over this tax form, we should set aside some time to discuss the difference between refundable credits and nonrefundable credits.

What is a refundable tax credit?

A refundable tax credit can reduce your income tax liability below zero. In other words, a refundable credit can result in a tax refund during a taxable year in which you pay zero income tax.

What is a nonrefundable tax credit?

Conversely, a nonrefundable tax credit can reduce the amount of tax you pay to zero, but will not result in a negative tax liability.

IRS Form 8862 Tax credit overview

Most of these tax credits are refundable credits, under the right circumstances. Otherwise, the tax credit might be nonrefundable. We’ll go through each in minor detail.

Earned Income Credit (EIC)

The earned income credit, also known as the earned income tax credit (EITC), is a refundable tax credit. Specifically, the EIC helps people who work, but earn a low to moderate income.

To qualify for the EIC, a taxpayer must:

- Have a valid Social Security number

- If filing a joint return, both spouses must have an SSN, as well as any child listed on Schedule EIC

- Not have a filing status of Married Filing Separately (MFS)

- Be a U.S. citizen or resident alien the entire calendar year

- May be a nonresident alien married to a US citizen

- Not file IRS Form 2555 to claim the foreign earned income exclusion

- Not have investment income over $10,000

- Have earned income

- Not be a qualifying child

- Or have a spouse who is a qualifying child

- Have a qualifying child who meets the following tests:

- Age test

- Relationship test

- Residency test

- Joint return test

- Is not a qualifying child of another person

If you do not have a qualifying child, you must:

- Be at least age 25 but younger than 65 at the end of the tax year

- Not qualify as another taxpayer’s dependent

- Live in the United States for more than 1/2 of the tax year

The IRS website contains an EIC assessment tool, known as the EIC assistant. You can use this tool to determine whether you qualify for this tax credit.

Child Tax Credit (CTC) & Additional Child Tax Credit (ACTC)

The child tax credit is a partially refundable tax credit for families with qualifying children who meet certain income requirements. The credit is $2,000 per child, of which $1,400 is refundable .

The refundable portion of the CTC is also known as the additional child tax credit.

To be a qualifying child for the tax year, your dependent generally must:

- Be under age 18 at the end of the year

- Be your son, daughter, stepchild, eligible foster child, brother, sister, stepbrother, stepsister, half-brother, half-sister, or a descendant of one of these (for example, a grandchild, niece or nephew)

- Provide no more than half of their own financial support during the year

- Have lived with you for more than half the year

- Be properly claimed as your dependent on your tax return

- Not file a joint return with their spouse for the tax year or file it only to claim a refund of withheld income tax or estimated tax paid

- Have been a U.S. citizen, U.S. national or U.S. resident alien

The IRS has an interactive tool to help taxpayers determine whether they qualify for the child tax credit or the credit for other dependents (ODC).

Credit for Other Dependents (ODC)

The ODC is a non-refundable tax credit available for taxpayers who might not qualify for the child tax credit. The maximum available credit is $500 per qualified dependent. A qualified dependent:

- Can be any age, including those who are age 18 or older.

- Must have Social Security numbers or individual taxpayer identification numbers.

- Can be dependent parents or other qualifying relatives supported by the taxpayer.

- Can be dependents living with the taxpayer who aren’t related to the taxpayer.

American Opportunity Tax Credit (AOTC)

The AOTC is a partially refundable tax credit. Qualified taxpayers may receive a maximum annual credit of $2,500 per eligible student. Up to 40% of this tax credit is refundable. This means that if you owe zero tax, you could receive a refund of up to $1,000 per eligible student.

Where can I find IRS Form 8862?

You may download a copy of this and other federal tax forms on the IRS website, or select the file below.

Related tax articles

If you’re interested in other free fillable tax forms from the IRS, check out our free fillable forms archives! With links to in-depth instructional articles and video tutorials for every tax form, the archives is the place for people who want to understand a tax form for themselves.

This tax form is one of the fillable tax forms provided by the Internal Revenue Service, to help taxpayers reduce their tax preparation costs. To see more forms like this, visit our free fillable tax forms page, where you’ll also find articles like this.

Unlike the IRS, our articles contain step by step instructions for each tax form, as well as video walkthroughs. You can also check out all of our videos by subscribing to our YouTube channel!