IRS Form 8282 Instructions

If you donated high-value property to a tax-exempt organization, you might receive IRS Form 8282 when that organization sells or disposes of that property within 3 years of your donation. If you’re a tax-exempt organization selling property, you must file IRS Form 8282 to avoid significant tax penalties.

In this article, we’ll go over IRS Form 8282, including:

- How to complete and file IRS Form 8282

- Reporting requirements

- Other frequently asked questions

Let’s start with a top-down overview of this tax form.

Table of contents

How do I complete IRS Form 8282?

In addition to the identifying information fields, there are four parts to this IRS tax form:

- Part I: Information on original donor and successor donee receiving the property

- Part II: Information on previous donees

- Part III: Information on donated property

- Part IV: Certification

Let’s start at the top, with the identifying information fields.

Identifying information

In this section, you’ll enter basic information about the charitable organization. Enter the following:

- Charitable organization’s name

- Employer identification number (EIN)

- Address, including city, state, and ZIP code

If you’ve recently changed addresses, you may need to update the IRS on your address change using IRS Form 8822-B, Change of Address or Responsible Party, Business.

Types of donees

For purposes of Form 8282, the charitable organization is also known as the donee. And if there is only one charitable organization involved, then this is fairly simple.

However, there may be instances in which you’re reporting the disposition of property that has changed hands between multiple qualified charitable organizations.

Below are different donees, and how the Internal Revenue Service defines them and their roles.

Original donee

According to the IRS, the original donee is the first tax-exempt organization to which the original donor gave the noncash donation.

For noncash donations of over $5,000, the original donee is the recipient organization required to sign Section B on IRS Form 8283, Noncash Charitable Contributions, presented by the donor for reporting noncash contributions of donated property for charitable purposes.

What to complete as original donee

If you are filing Form 8282 as the original donee, then you must complete the following fields:

- Identifying information

- Part I

- Lines 1a through 1d

- Lines 2a through 2d, if applicable

- Part III

Successor donee

A successor donee organization is any other exempt organization, other than the original donee.

What to complete as Successor donee

Successor organizations filing Form 8282 must complete the following fields:

- Identifying information

- Part I

- Lines 1a through 1d

- Lines 2a through 2d, if applicable

- Part II

- Part III

Previous donee

A previous donee is a qualified organization that previously had possession of the donated property. A previous donee could be the original donee or another successor donee.

Preceding donee

The preceding donee is the donee organization that transferred the donated item to the current organization.

There may be multiple previous donees, but only one preceding donee. The preceding donee may be the original donee or another successor donee.

Report information on the preceding donee in Part II.

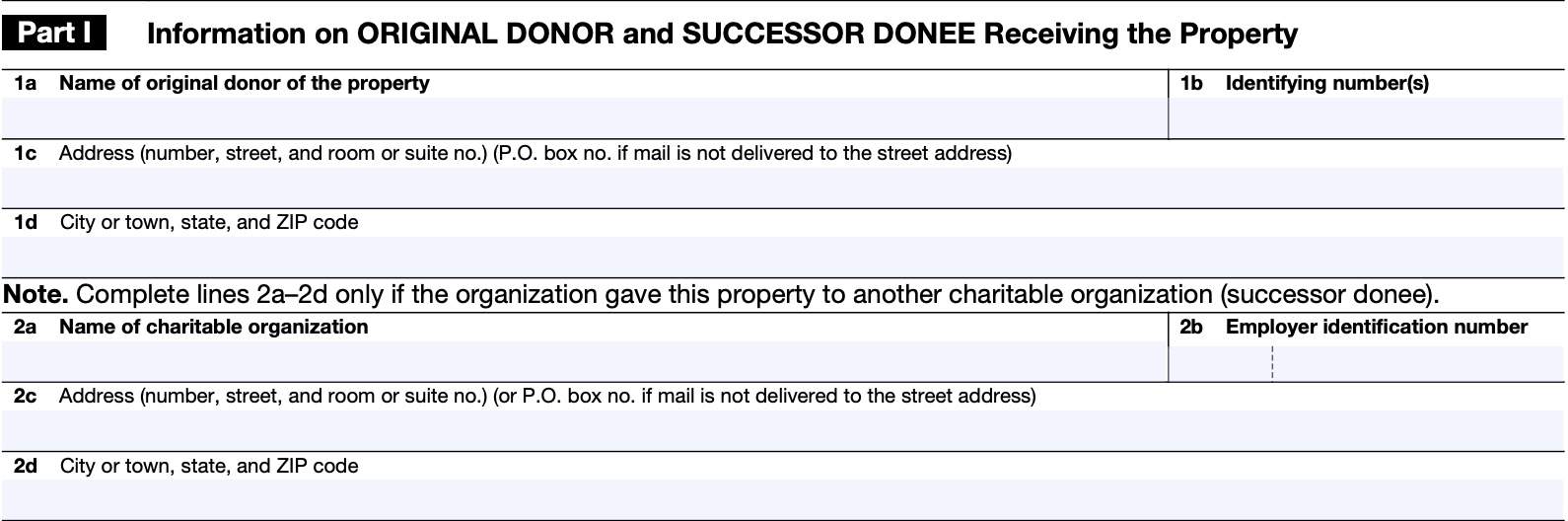

Part I: Information on original donor and successor donee receiving the property

Part I contains information on the original donor. Also, if you’re reporting that you gave this property to a successor donee, you’ll do so in Part I as well.

Let’s start with the donor’s information.

Line 1a: Name of original donor of the property

In Line 1a, enter the original donor’s name.

Line 1b: Identifying number

Enter the tax identification number as previously reported on Page 2 of Form 8283. This may be an employer identification number or the donor’s Social Security number (SSN).

Line 1c & Line 1d: Address

Enter the most recent street address you have on file for the donor. This will likely come from Form 8283, unless your organization has more updated records about the donor’s address.

If you gave the property to another charitable organization, go to Line 2a.

If you did not give the property to another charitable organization, but you need to report on one or more qualified organizations that were previous donees, then go to Part II, below.

Otherwise, go directly the Part III.

Line 2a: Name of charitable organization

Enter the name of the public charity that your organization gave the donated property to.

Line 2b: Employer identification number

Enter the successor donee’s EIN in Line 2b.

Line 2c & Line 2d: Address

Enter the complete address for the successor donee in Lines 2c and 2d.

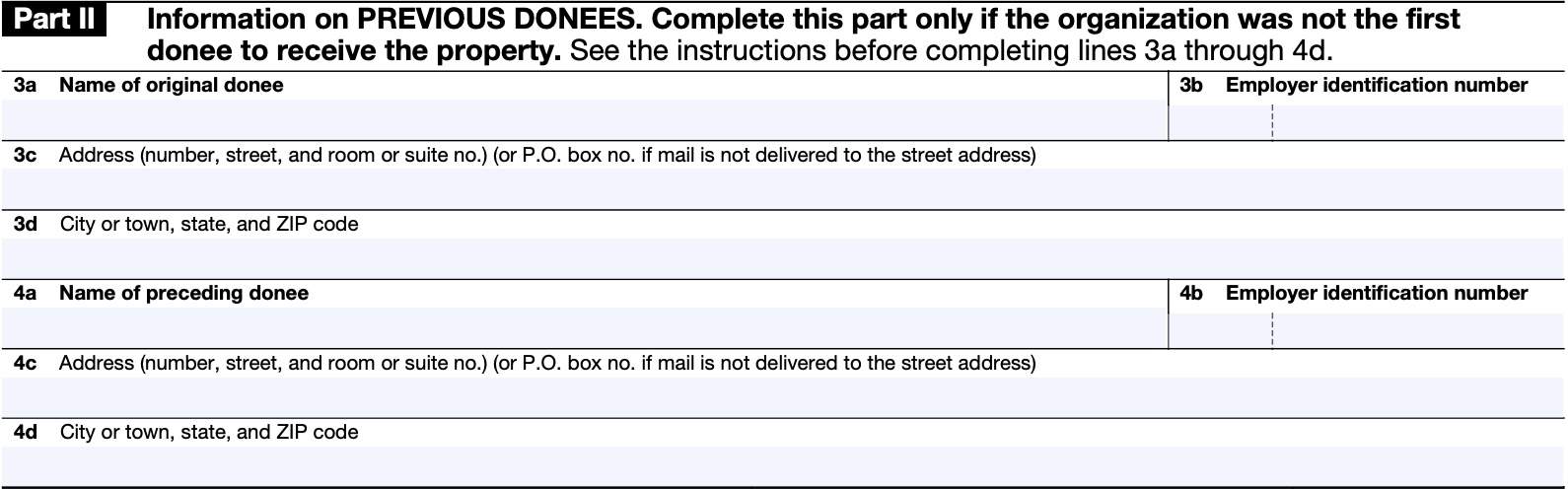

Part II: Information on previous donees

Exempt organizations only need to complete Part II if they are not the original donee. Original donees may skip Part II and proceed to Part III, below.

If you are the second donee, then you will complete Lines 3a through 3d for the original donee. If you are the third or later successor donee, then you will need to complete the following:

- Lines 3a through 3d: Original donee

- Lines 4a through 4d: Preceding donee

You do not have to report on any successor donees between the original donee and the preceding donee.

When completing Lines 3a through 3d, or Lines 4a through 4d, use the same guidance as for Lines 2a thorough 2d, above.

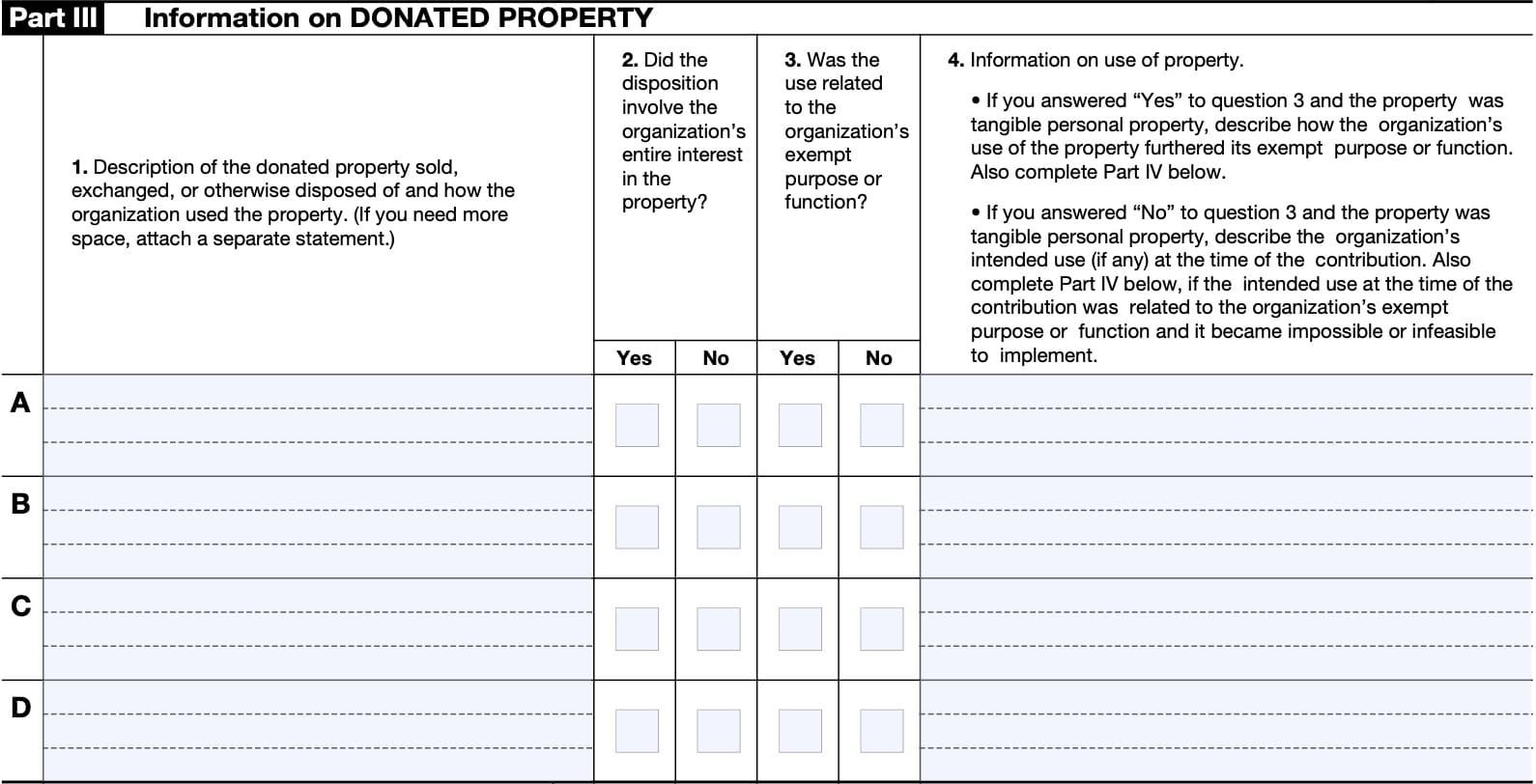

Part III: Information on donated property

In Part III, you can provide information on the donated property. This part contains space for up to 4 separate donations, but you can attach additional forms as required.

Let’s go through what you will enter in each section. To simplify matters, we will refer to each part as Lines, even though “Lines” 1-4 look more like columns.

Line 1: Description of the donated property sold, exchanged, or otherwise disposed of, and how the organization used the property

Enter a description of the donated property. You must provide, in detail, a description of the donated property that was disposed of.

This includes any property sales, exchanges, or other disposition of donated property within 3 years of receipt of the original contribution.

If describing a motor vehicle, include the vehicle identification number, or VIN. For describing an airplane, include the aircraft identification number. For boats, include the hull identification number.

These identification numbers should match those reported on the original IRS Form 1098-C, Contributions of Motor Vehicles, Boats, and Airplanes.

Also, explain how the organization used the donated property during the period of time time that the organization owned it. If you need additional space, you may attach a statement, and include it with your completed Form 8282.

Line 2: Did the disposition involve the organization’s entire interest in the property?

Check ‘Yes’ if the organization disposed of their entire ownership state in the property. Otherwise, select ‘No.’

Line 3: Was the use related to the organization’s exempt purpose or function?

Check “Yes” if the organization’s use of the charitable deduction property was related to its exempt purpose or function.

Check “No” if the organization sold, exchanged, or otherwise disposed of the property without using it.

Line 4: Information on use of property

The information in this field depends on whether you answered ‘Yes’ or ‘No’ to the question in Line 3.

If you answered Yes

If you answered ‘Yes,’ and the property was tangible personal property, then you must describe how the organization’s use of the property furthered its tax-exempt purpose or function. You must also complete Part IV, below.

If you answered No

If you answered ‘No,’ and the property was tangible personal property, then you must describe how the organization intended to use the property.

You must also complete Part IV, below, if the intended use at the time of contribution was related to the exempt organization’s purpose, but it became impossible or not feasible to implement.

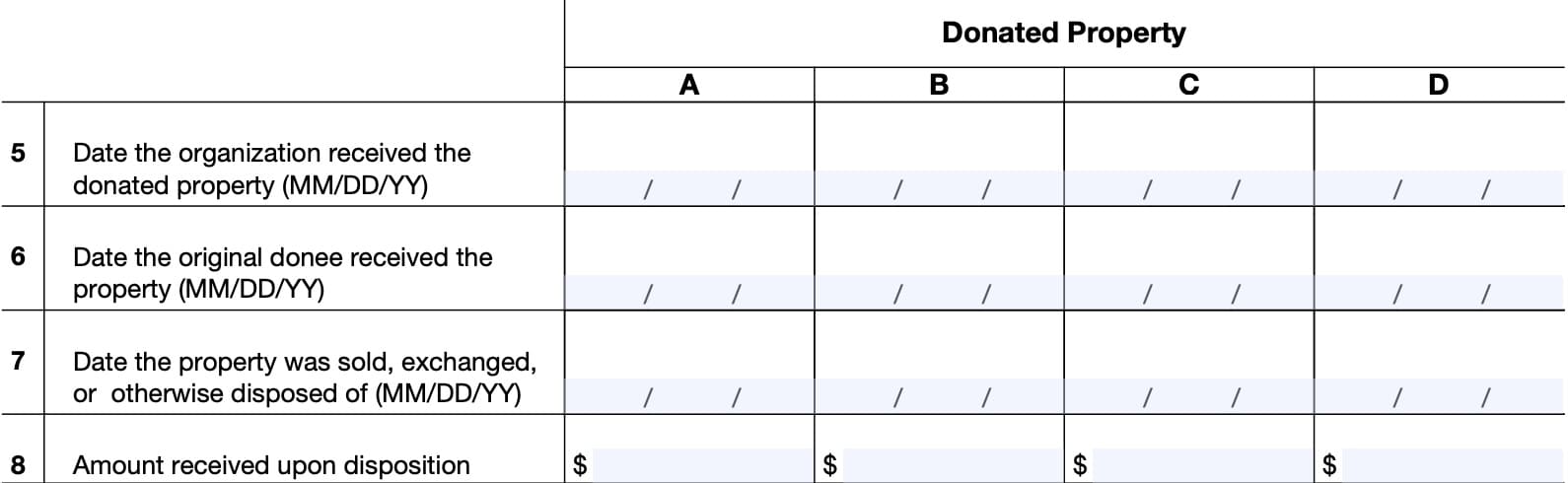

Line 5: Date the organization received the donated property

For each item, enter the date of receipt of the described property.

Use the following format: MM/DD/YYY.

Line 6: Date the original donee received the property

Enter the date that the original donee received the property. As a reminder, if the receipt of the property is more than 3 years prior to the date of disposition, cited in Line 7, you do not need to include it on IRS Form 8282.

Use the following format: MM/DD/YYY.

Line 7: Date the property was sold, exchanged, or otherwise disposed of

Enter the date of disposition or sale of the property.

Use the following format: MM/DD/YYY.

Line 8: Amount received upon disposition

Enter the total amount that you received for the property.

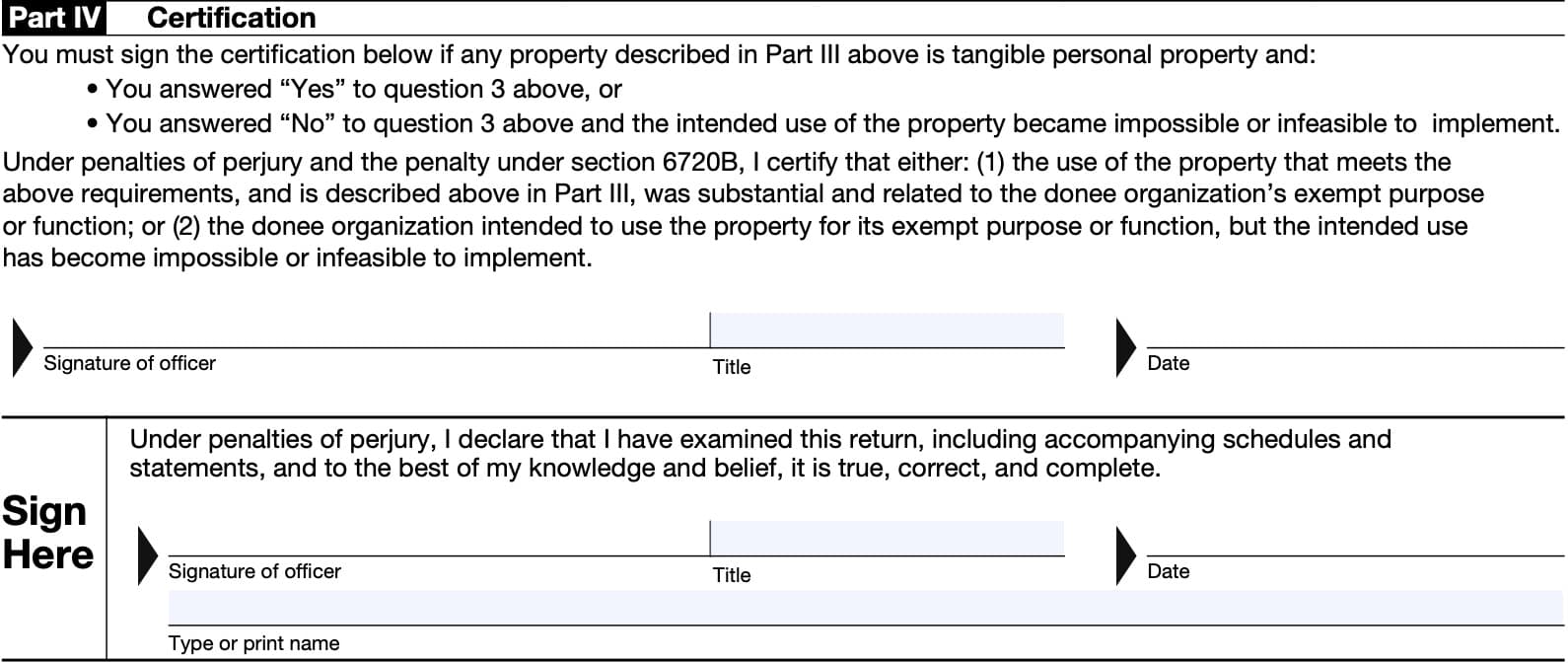

Part IV: Certification

You must complete Part IV if any of the property is tangible personal property, and either of the following happened:

- You answered ‘Yes’ to Question 3, above, or

- You answered ‘No’ to Question 3, and the intended use of the property became impossible or infeasible to implement

By signing this certification, you are certifying that either:

- Use of the property meets IRS requirements, and was substantial and related to the organization’s purpose or function, or

- The donee organization intended to use the property for its exempt purpose or function, but that the intended use became impossible or infeasible to implement.

This is subject to penalties of perjury and punishment under Internal Revenue Code Section 6720B. This section, which covers contributions of property for charitable purposes but not made in good faith or with reasonable cause, carries a penalty of a $10,000 fine.

Tangible personal property

The Internal Revenue Manual defines tangible personal property as “anything other than real property or intangible personal property which includes items such as patents, copyrights, stocks, and the goodwill value of a business.”

Underneath the certification, sign and date the completed Form 8282, and enter the name and title of the responsible officer signing the form. The same officer may sign Part IV and the bottom of the completed form.

Video walkthrough

Watch this informational video to walk through IRS Form 8282, step by step!

Frequently asked questions

Tax-exempt organizations must file IRS Form 8282 to report the disposition charitable deduction property if the disposition of the property took place within 3 years of the contribution. Exceptions exist for property valued at under $500 or if the property was consumed or distributed for charitable purposes.

Under normal circumstances, charitable organizations that dispose of charitable deduction property within 3 years of the donation must file IRS Form 8282 within 125 days of the disposition of the property.

Charitable organizations filing Form 8282 may send the completed form to: Department of the Treasury, IRS Service Center, Ogden, UT 84201-0027. They must provide a full copy of Form 8282 to the to the original donor, as well.

Donors and donor organizations who receive Form 8282 for donated property should keep the form in their tax records. However, there is no additional reporting requirement for this information return.

According to the tax code, the penalty for failure to file Form 8282 is $50 per occurrence.

Where can I find IRS Form 8282?

As with most tax forms, you may find IRS Form 8282 on the IRS website. We have enclosed the most recent copy of the form here, in this article.