IRS Form 8949 Instructions

If you have sold or disposed of investments in the past year, you may need to report those transactions on your tax return by using IRS Form 8949, Sales and Other Dispositions of Capital Assets. More importantly, by filing IRS Form 8949 with your income tax return, you can reconcile the transactions as your broker or financial institution reported them to you and the Internal Revenue Service.

In this article, we’ll cover everything you need to know about IRS Form 8949. Let’s begin by walking through this tax form, step by step.

Table of contents

How do I complete IRS Form 8949?

There are two parts to this form:

Let’s start with Part I.

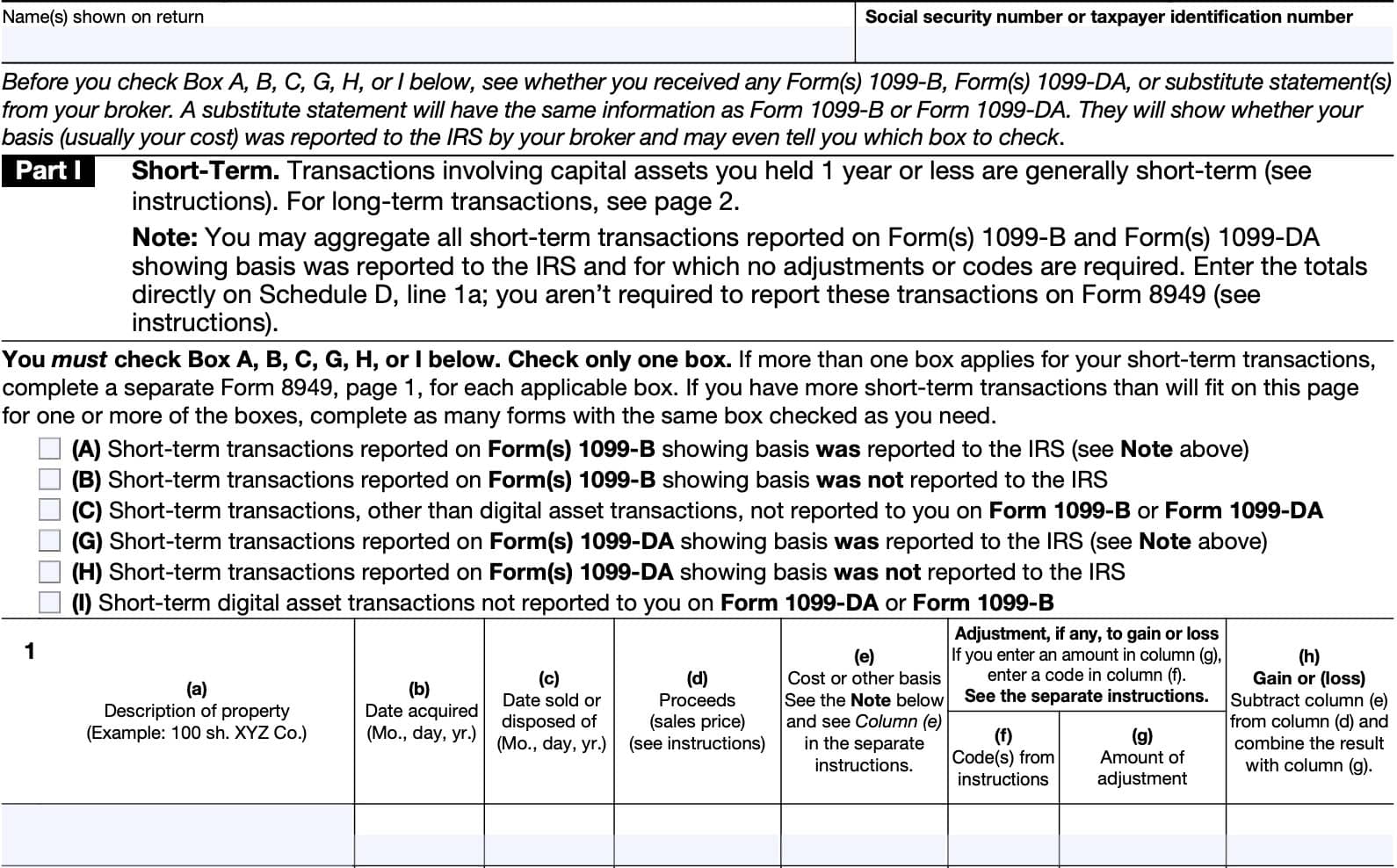

Part I: Short-term transactions

In Part I of Form 8949, you will list all short-term transactions that occurred during the tax year. Typically, short-term transactions are transactions that involve capital assets which you’ve held for one year or less.

At the top of the form, enter your name and Social Security number. If you do not have a Social Security number, enter your individual taxpayer identification number (ITIN). If you’re filing on behalf of a corporation or other entity, you may need to enter an employer identification number (EIN).

Box A, Box B, Box C, Box G, Box H, or Box I?

At the top of Part I, you’ll notice boxes marked A, B, C, G, H, and I. You will need to check exactly one of these boxes, depending on the type of short-term transaction you are reporting:

- Box A: Check Box A to report transactions where the transaction and basis was reported to you and the Internal Revenue Service on Form(s) 1099-B, Proceeds from Broker and Barter Exchange Transactions.

- Box B: Check Box B to report transactions where the transaction was reported to you and the IRS, but the basis of the asset was not.

- Box C: Check Box C to report transactions where the transaction was not reported to you at all on IRS Form 1099-B

- Box G: Check Box G to report short-term transactions where the digital asset transaction was reported to you on IRS Form 1099-DA, Digital Asset Proceeds From Broker Transactions

- Box H: Check Box H to report transactions where the transaction was reported to you and the IRS, but the basis of the digital asset was not reported to the IRS.

- Box I: Check this box to report short-term digital asset transactions that were not reported to you or the IRS on either IRS Form 1099-DA or Form 1099-B.

For taxpayers who have transactions in more than one category, you will have to file a separate Form 8949 for each type of transaction.

For example, John Smith is reporting 3 short-term transactions reported to him by his broker on Form 1099-B. Two transactions have the correct basis, while the third transaction is missing its cost basis. John would report the two transactions with correct basis on one Form 8949 with Box (A) checked, and the third transaction on a separate form with Box (C) selected.

Also, for married couples filing a joint return, you may have to complete Form 8949 separately for each spouse.

Line 1

In Line 1, you should record each transaction separately, unless you can aggregate transactions or you meet one of the exception criteria, listed further in the article. Otherwise, you’ll need to complete columns (a) through (h) for each transaction.

Column (a): Description of property

In column (a), include a brief description of the property disposed of. For stocks or mutual funds, you should include the number of shares. You may use ticker symbols or symbols as long as they match the descriptions shown on your Form 1099-B, Form 1099-DA, or 1099-S (substitute statement).

When listing digital assets, you should include the full name or an abbreviated symbol of the digital asset, and the exact number of units sold or disposed of. If possible, include the sale transaction number.

Column (b): Date acquired

Enter the date that you acquired the property. For stocks, bonds, or mutual funds, this is the same as the trade date. For short sales or other real estate transactions, this would be the date that you acquired the property.

On Forms 1099-B, refer to Box 1b to determine the date of acquisition.

For inherited property, you’ll enter this in Part II, as inherited property generally is subject to preferred capital gains treatment at long-term tax rates. Enter “INHERITED” as appropriate in Column (b).

If you acquired stock over various dates, such as in a dollar cost averaging strategy, you may enter ‘VARIOUS’ in Column (b). However, you must still report short-term gains and losses in Part I, and long-term gains and losses in Part II.

Column (c): Date sold or disposed of

In Column (c), enter the date that you sold or disposed of the property. For stocks, bonds, and other securities traded on investment exchanges, this will be the trade date.

If you received a Form 1099-B, refer to Box 1c to determine the date of sale or disposition. If you received a Form 1099-DA, this information will be in Box 1e.

Column (d): Proceeds

Column (d) contains the sales price, or proceeds, of the sales transaction. How you report this depends on whether you received a Form 1099-B or Form 1099-S.

If you received a brokerage statement:

Enter the proceeds shown on the form or statement that you received. If there are selling expenses or option premiums not reflected on the statement, then you may need to adjust either the proceeds or the basis by entering ‘E’ in Column (f), then the necessary adjustment in Column (g).

If you did not receive a brokerage statement:

To report a transaction for which you did not receive a brokerage statement, then enter the net proceeds for the transaction. The net proceeds are gross proceeds minus transaction costs, such as fees, commissions, or taxes.

If you sold a call option, and it was exercised, then you will need to adjust the sales price of the sold property for any option premiums. Refer to the instructions for Schedule D for detailed instructions.

Column (e): Cost or other basis

The cost basis of any property that you purchase is usually the cost. This includes the purchase price as well as any transaction costs, such as fees or commissions.

You may not be able to use the actual cost in the following situations:

- Inheriting property

- Receiving property as a gift

- Receipt of property in a tax-free exchange, involuntary conversion, or in connection with a wash sale

The basis for inherited property is generally the property’s fair market value on the date of death. For property that you received as a gift, the cost basis is usually the donor’s cost basis.

For more detailed information on how to determine the cost basis of an asset, please refer to the IRS instructions.

Column (f): Adjustment code from IRS Form instructions

To explain adjustments to gains or losses in column (g), you must enter one or more adjustment codes, as outlined in the form instructions. If more than one code applies, enter all applicable codes in alphabetical order, but do not separate them by a space or comma.

Below is a list of specific situations and their corresponding code:

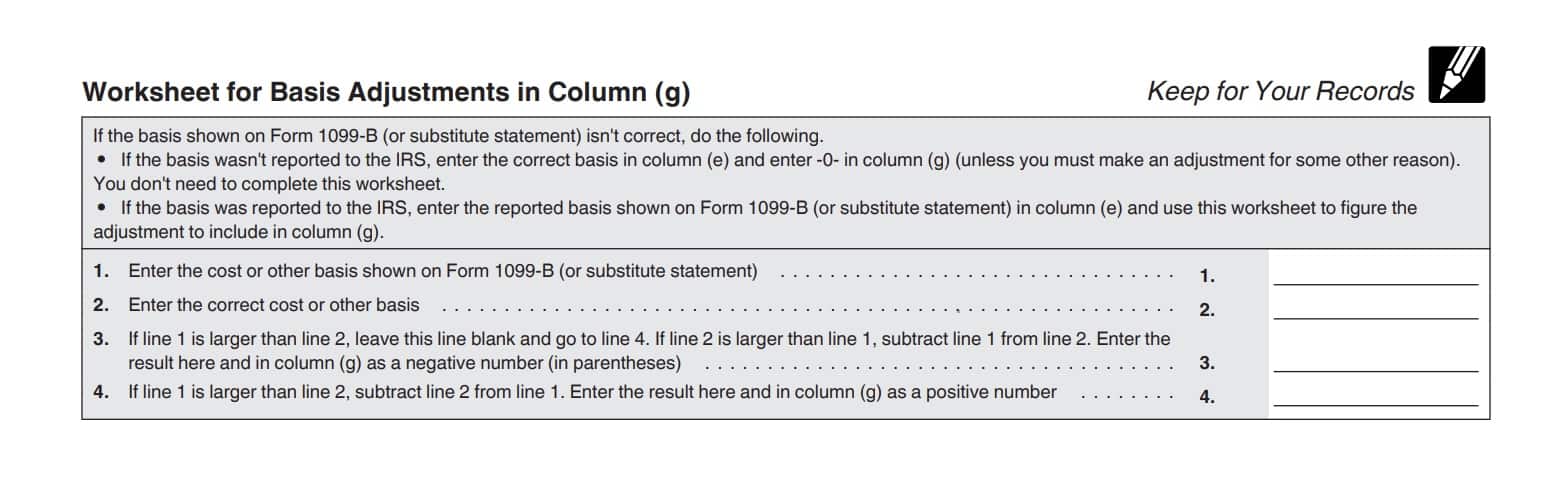

If you received Form 1099-B or a substitute, and the basis in Box 1e is incorrect

Enter code B in column (f) and do one of the following:

If this transaction is reported on a Part I with box B checked, or on Part II with box E checked, enter the correct basis in column (e), then enter ‘0’ in column (g).

If you reported this transaction on a Part I with box A checked, or on Part II with box D checked, enter the basis shown on Form 1099-B or its substitute in column (e). Enter an adjustment in column (g). To learn how to make this adjustment, you’ll need to see the worksheet for basis adjustments in column (g), below.

If you received a Form 1099-B or a substitute, and the type of gain (or loss) in box 2 is incorrect

Enter code T in column (f) then report the transaction on the correct part of Form 8949. Enter ‘0’ in column (g) if there are no adjustments required.

If you received a Form 1099-B or a substitute as a nominee for the property’s actual owner

Enter code N in column (f) then report the transaction on Form 8949 as if you were the actual owner. However, you should also enter any gains as a negative adjustment (using parentheses), or any losses as a positive adjustment in column (g).

After the adjustment, the amount in column (h) should equal zero. However, if you received capital gains distributions as a nominee, you may need to report them on IRS Schedule D.

If you sold or exchanged your main home at a gain, must report the sale or exchange in Part II, and you can exclude some or all of the gain

Enter code H in column (f) then report the sale or exchange as if you were not taking the Section 121 exclusion. Then, enter the amount of the excluded gain as a negative number in column (g).

For example, you bought your primary residence in 2015 for $100,000. In 2025, you sold your primary home in 2025 for $450,000 (after adjustments), realizing a $350,000 capital gain. As a single homeowner, you meet the criteria to exclude up to $250,000 of capital gain from your taxable income. You would report capital gains from the sale of your primary residence as follows:

- Column (d): $450,000

- Column (e): $100,000

- Column (f): T

- Column (g): ($250,000)

- Column (h): $100,000

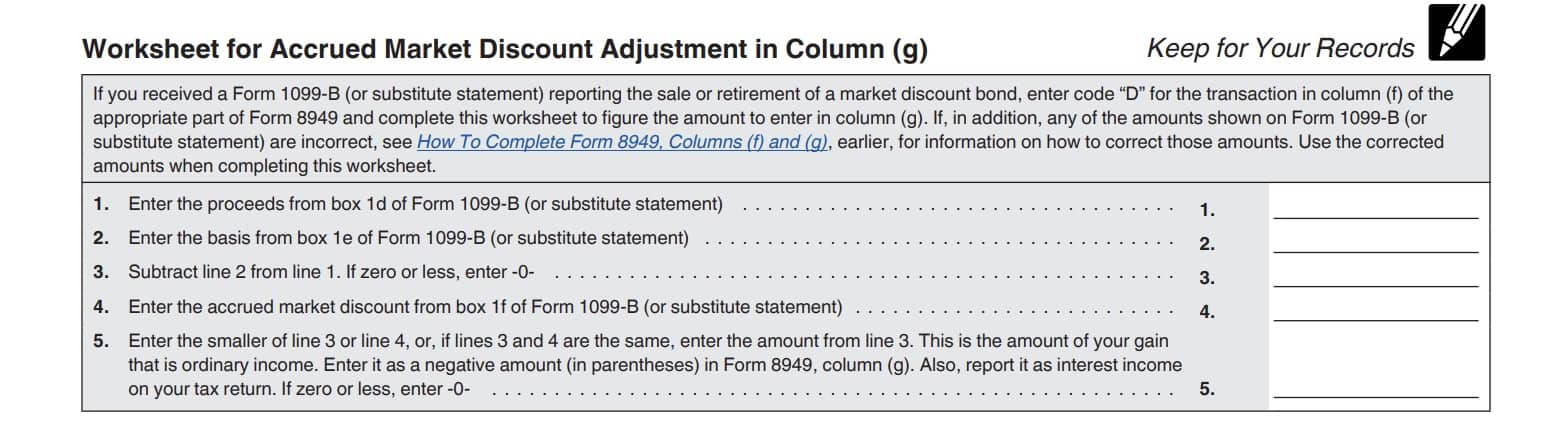

If you received a Form 1099-B or a substitute that shows accrued market discount in Box 1f

Enter code D in column (f) then use the worksheet for accrued market discount adjustment in Column (g), with the following exceptions:

- If you received a partial payment of principal on a bond, do not use the worksheet. Enter the smaller of the following in column (g):

- Accrued market discount

- Your proceeds

- If you choose to include market discount in income, enter ‘0’ in column (g). then follow the instructions for code B, above.

If you sold or exchanged QSB stock and can exclude part of the gain

Enter code Q in column (f) then report the sale or exchange as if you were not taking the exclusion, then enter the amount of the exclusion as a negative number in column (g). If this transaction is reported as an installment sale, you may need to refer to the Schedule D instructions for more detail.

If you can exclude part or all of the gain under rules outlined in Schedule D instructions for DC Zone assets or qualified community assets

Enter code X in column (f) then report the sale or exchange as if you were not taking the exclusion, then enter the amount of the exclusion as a negative number in column (g).

If you elect to postpone all or part of your gain under rules outlined in Schedule D instructions

Enter code R in column (f) then report the sale or exchange of a capital asset as if you were not taking the exclusion, then enter the amount of the postponed gain as a negative number in column (g).

If you have a nondeductible loss from a wash sale

Enter code W in column (f) then report the amount of the nondeductible loss as a positive number in column (g). See the Schedule D instructions or IRS Publication 550 for more details about wash sales.

If you received a Form 1099-B and the amount of nondeductible wash sale loss is incorrect, post the correct amount of the nondeductible loss as a positive number in column (g). If the amount of the loss is less than the amount shown on the statement, attach a separate statement explaining the difference.

Enter ‘0’ in column (g) if no part of the loss is a nondeductible loss from a wash sale.

If you have a nondeductible loss other than a loss indicated by code W

Enter code L in column (f) then report the amount of the nondeductible loss as a positive number in column (g).

If you received a Form 1099-B or substitute for a transaction and there are selling expenses or option premiums not reflected on the form, or a statement by an adjustment to the proceeds or basis shown

Enter code E in column (f) then enter in column (d) the proceeds shown on the form or statement.

Enter in column (e) any cost or other basis shown on the statement.

In column (g), enter any selling expenses or option premiums paid as a negative number. Enter any option premiums that you received as a positive number.

If you had a loss from the sale, exchange or worthlessness of small business stock (under IRC Section 1244), and the total loss is more than the maximum amount that can be treated as an ordinary loss

Enter code S in column (f) then refer to the Small Business stock section of the Schedule D instructions.

If you disposed of collectibles

Enter code C in column (f) then enter ‘0’ in column (g). Report the disposition as you would any sale or exchange.

If you report multiple transactions on a single row as outlined under one of the exceptions

Enter code M in column (f) then refer to the exceptions section of the form instructions. Enter ‘0’ in column (g) unless another code requires that you make another adjustment.

If you have an adjustment not otherwise explained

Enter code O in column (f) then enter the appropriate amount in column (g).

If you are electing to postpone part or all of your overall gain under Schedule D instructions for QOFs

Enter code Z in column (f) then see the form instructions on reporting an election to defer tax liability on eligible gains invested in a QOF.

If you are reporting your gain from a QOF that you previously deferred

Enter code Y in column (f) then refer to the form instructions on reporting a gain previously deferred in a QOF.

If no other statements apply

Leave column (f) blank.

Column (g): Amount of adjustment

In this column, enter any required adjustments to gain or loss. Enter negative adjustments in parentheses.

If you entered more than one code in column (f), enter the net adjustment in this column.

Column (h): Gain or loss

Calculate the gain or loss for each row.

First, subtract the cost basis figure in column (e) from the proceeds in column (d). From there, add or subtract any adjustments from column (g).

Enter the result in column (h) as the resultant gain or loss. Enter negative numbers in parentheses.

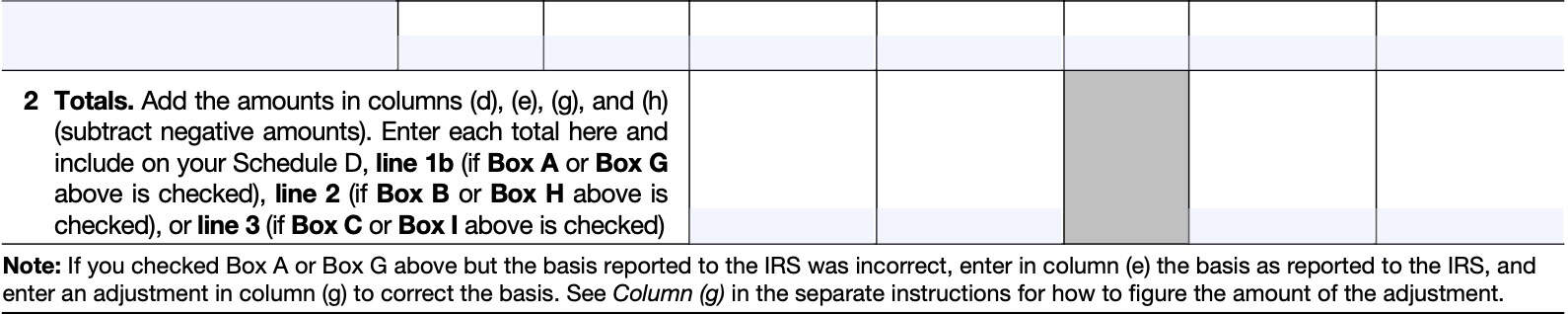

Line 2

In Line 2, you will enter the totals from the amounts in columns (d), (e), (g), and (h), above. Enter each total here and include these numbers on Schedule D as follows:

- If Box A or Box G is checked, enter total in Line 1b on Schedule D

- If Box B or Box H is checked, enter total in Line 2 on Schedule D

- If Box C or Box I is checked, enter total in Line 3 on Schedule D

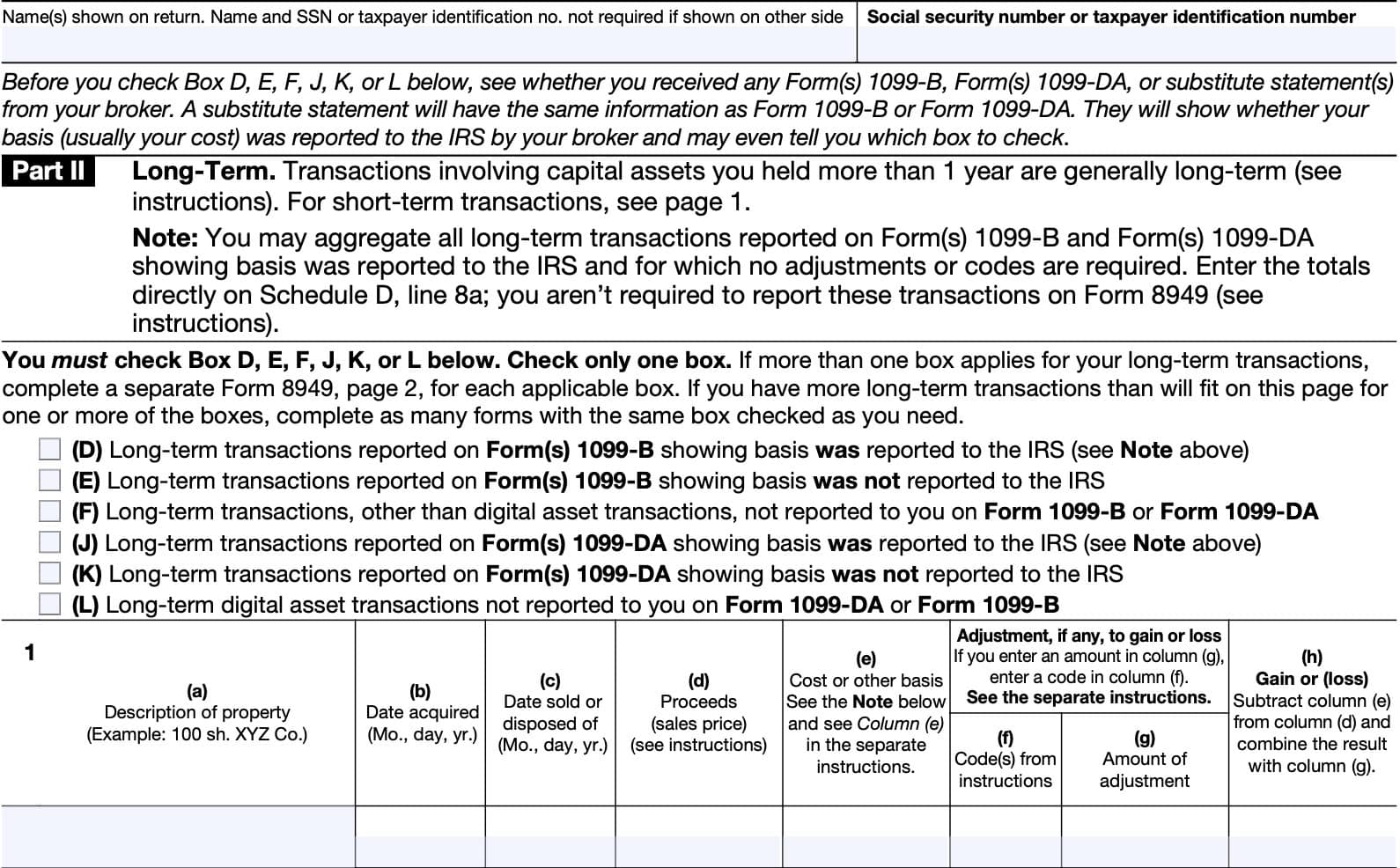

Part II: Long-term transactions

Box D, Box E, Box F, Box J, Box K, or Box L?

At the top of Part II of Form 8949, you’ll notice boxes marked D, E, F, J, K, and L for reporting long-term transactions, similar to Part I.

You will need to check exactly one of these boxes for the type of long-term transaction you are reporting:

- Box D: Check Box D to report transactions where the transaction and basis was reported to you and the Internal Revenue Service on Form(s) 1099-B.

- Box E: Check Box E to report transactions where the transaction was reported to you and the IRS, but the basis of the asset was not.

- Box F: Check Box F to report transactions where the transaction was not reported to you at all on Form 1099-B

- Box J: Check Box J to report long-term transactions where the digital asset transaction was reported to you on IRS Form 1099-DA

- Box K: Check Box K to report transactions where the transaction was reported to you and the IRS, but the basis of the digital asset was not reported to the IRS.

- Box L: Check this box to report long-term digital asset transactions that were not reported to you or the IRS on either IRS Form 1099-DA or Form 1099-B.

Line 1

For Part II, you will follow identical instructions as in Line 1 for each transaction meeting the criteria for long-term gains (or losses) treatment.

Long term capital gains

You should treat the following types of transactions as long-term capital gains:

- Sale of stocks or other capital assets held for more than 1 year

- Often referred to as one year, one day rule

- Holding period for long term treatment on the sale of race horses is 2 years

- Digital assets held for more than 1 year

- Sale of inherited property, regardless of holding period

- Capital gain distributions from mutual funds.

- Always report capital gain distributions as long term regardless of how long you’ve held the mutual fund itself

- Reported on IRS Schedule D

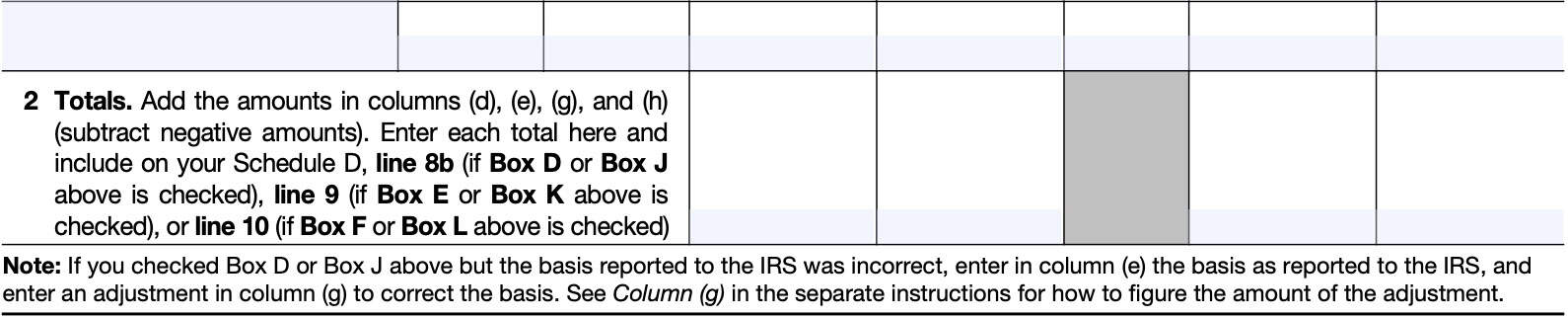

Line 2

In Line 2, you will enter the totals from the amounts in columns (d), (e), (g), and (h), above. Enter each total here and include these numbers on Schedule D as follows:

- If Box D or Box J is checked, enter total in Line 8b on Schedule D

- If Box E or Box K is checked, enter total in Line 9 on Schedule D

- If Box F or Box L is checked, enter total in Line 10 on Schedule D

Video walkthrough

Watch this instructional video to learn more about reporting capital asset sales and exchange transactions on IRS Form 8949.

Frequently asked questions

Taxpayers use Form 8949 to report sales and exchanges of capital assets. Form 8949 allows you and the IRS to reconcile amounts reported to you and the IRS on brokerage statements such as Forms 1099-B or 1099-S (substitute statements).

Long term capital gains have a holding period of more than one year between acquiring and sale of an asset. Conversely, short term gains and losses have a holding period of one year or less. Long term capital gains are treated more favorably than short term gains, which are treated as ordinary income.

You may still need to report the transactions on Form 8949, depending on your situation. You should check to see if there is an appropriate code for column (f) to explain any adjustments you enter into column (g).

A qualified opportunity fund, or QOF, is an economically distressed community certified by the Internal Revenue Service. Investments in qualified opportunity funds may be eligible for preferential tax treatment to create economic development opportunities in communities that might not otherwise receive capital investments.

Where can I find IRS Form 8949?

You may find copies of Form 8949 on the IRS website. For your convenience, we’ve included the most current version in this article in PDF format.

Related tax articles

This tax form is one of the fillable tax forms provided by the Internal Revenue Service, to help taxpayers reduce their tax preparation costs. To see more forms like this, visit our free fillable tax forms page, where you’ll also find articles like this.

Unlike the IRS, our articles contain step by step instructions for each tax form, as well as video walkthroughs. You can also check out all of our videos by subscribing to our YouTube channel!

This helped me a lot to understand so tomorrow during my appointment with the accountant I can be sure about what she’s entering in the form.

is there a way or requirement to report the sale of gifted stock? (not from inheritance but outright gift from relative)

Sure. Generally, the basis of your gifted stock is the same basis as it was for the person who gifted it to you. Inheriting stock involves a ‘step-up’ in basis, where the cost basis is the stock price on the date that the previous owner passed away. Gifted stock generally does not have the step up in basis.

You would still use IRS Form 8949 and/or Schedule D to report the sale of gifted securities.

In 2024, my son played crypto trader, and while buying and selling crypto, ended at a serious loss of around $100k. He makes about $93k a year. The crypto exchange doing his many, many transactions has not sent a form 1099-B. What is the best he can do to on the crypto reporting, which overall for 2024 was $100k.

That depends on the records that your son kept. If he kept accurate records, he can still report the losses (cost basis minus proceeds, minus selling costs). He can deduct up to $3,000 to offset ordinary income. If his capital losses exceed $3,000, then the losses generally will be carried forward to future tax years, where they will either offset capital gains, or $3,000/year of ordinary income.

Do you have to list each individual transaction from the 1099? The one I received has roughly 8 pages of long term transactions. Do I need to list each individually on Form 8949, or can I simply list the totals as “XYZ Financial Transactions” (brokerage firm), date: various and the total the summary 1099 provided shows for each column?

There are certain instances where you don’t have to list individual transactions. For example, the form instructions state:

If you don’t need to make any adjustments to the basis or type of gain (or loss) reported to you on Form 1099-B (or substitute statement) or to your gain (or loss) for any transactions for which basis has been reported to the IRS (normally reported on Form 8949 with box D checked), you don’t have to include those transactions on Form 8949. Instead, you can report summary information for those transactions directly on Schedule D.

Similarly, there are also a couple of exceptions to the rule where you have to list transactions:

There are exceptions to the rule that you must report each of your transactions on a separate row of Part I or II. Any taxpayer who qualifies can use Exception 1 or Exception 2 below.

Exception 1: Form 8949 isn’t required for certain transactions. You may be able to aggregate those transactions and report them directly on either line 1a (for short-term transactions) or line 8a (for long term transactions) of Schedule D. This option applies only to transactions (other than sales of collectibles) for which:

• You received a Form 1099-B (or substitute statement) that shows basis was reported to the IRS and doesn’t show any adjustments in box 1f or 1g;

• The Ordinary box in box 2 isn’t checked;

• You don’t need to make any adjustments to the basis or type of gain (or loss) reported on Form 1099-B (or substitute statement), or to your gain (or loss); and

• You aren’t electing to defer income due to an investment in a QOF and aren’t terminating deferral from an investment in a QOF

Exception 2: Instead of reporting each of your transactions on a separate row of Part I or II, you can report them on an attached statement containing all the same information as Parts I and II and in a similar format (that is, description of property, dates of acquisition and disposition, proceeds, basis, adjustment and code(s), and gain (or loss)). Use as many attached statements as you need. Enter the combined totals from all your attached statements on Parts I and II with the appropriate box checked.

Can you please provide an example to fill out form 8949 if long term sold was stock in December ’24 with a capital gain and purchased shares of a QOF in January ’25? How do you report you taxes for year ’24?

Are you talking about selling QOF in 2024, then reporting the deferred gain? Or are you talking about selling regular stock in 2024, then using the proceeds to purchase shares in a QOF?

Troublesome Form 8949. I received Form 1099-S from a lawyer. What box do I check for a house I sold last year as Long-term In Part II? There aren’t any boxes for Form 1099-S. Only 1099-B and 1099-DA.

You would use Box F.

I donated publicly traded stock to a DAF charity, and received a letter detailing the transaction, but not a 1099 form. I plan to report the donation on form 8283, but do I also need to report the donation on form 8949?

You do not need to report the donation on Form 8949, only Form 8283. If you had sold the stock, then donated the proceeds (eroding the benefits of donating stock), then you would need to complete Form 8949.