IRS Form 1099-B Instructions

If you sold securities through financial institutions like a brokerage firm, or participated in bartering activities, you may receive IRS Form 1099-B at the end of the tax year.

In this article, we’ll go over everything you need to know about IRS Form 1099-B, including:

- How to read IRS Form 1099-B

- Reporting payments on your federal income tax return

- Frequently asked questions

Let’s start with a comprehensive breakdown of this tax form.

Table of contents

IRS Form 1099-B Instructions

In most of our articles, we walk you through how to complete the tax form. However, since Form-1099 is issued to taxpayers for informational purposes, most readers will probably want to understand the information reported on their 1099-B form, instead of how to complete it.

Before we start breaking down this tax form, it’s important to understand that there can be up to 4 copies of Forms 1099-B. Here is a break down of where all these forms end up:

- Copy A: Internal Revenue Service center

- Copy 1: State Tax Department

- Copy B: For recipient’s tax records

- Copy 2: To be filed with state tax return, if required

Let’s get into the form itself, starting with the information fields on the left side of the form.

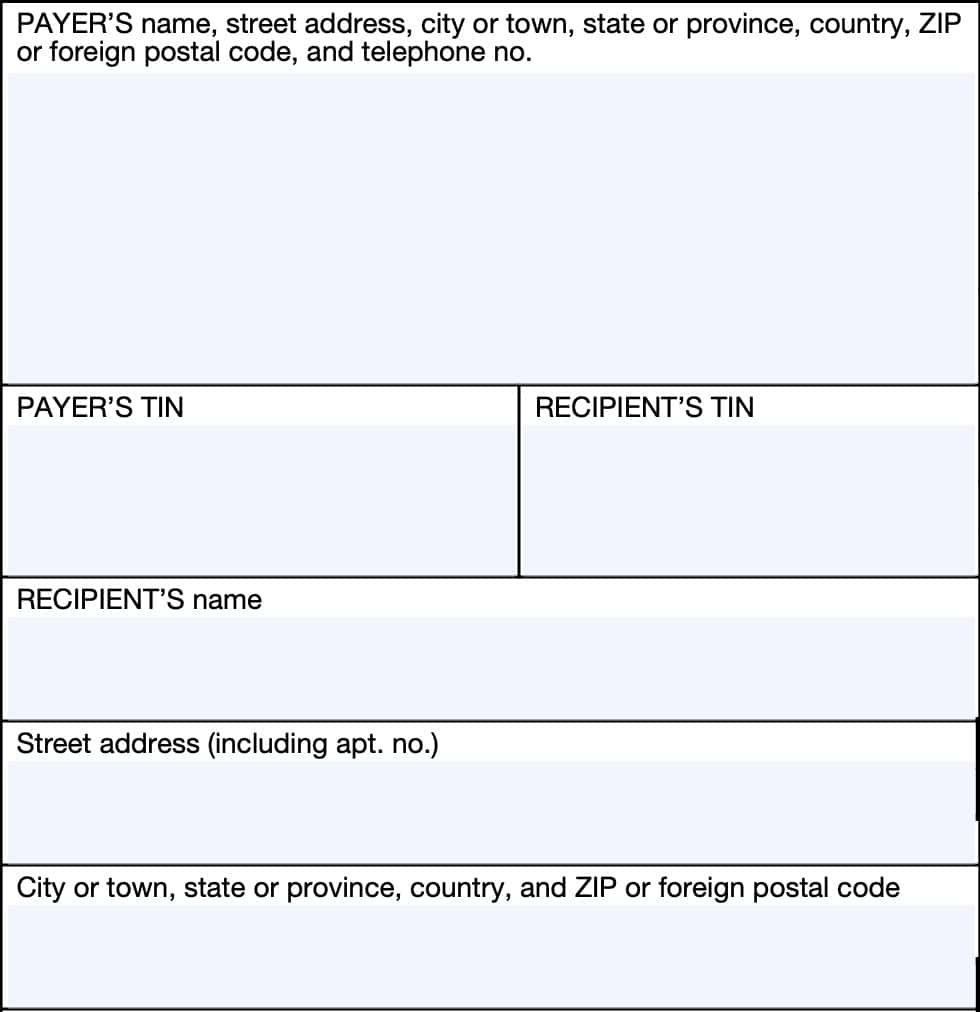

Taxpayer identification fields

Payer’s Name, Address, And Telephone Number

You should see the payer’s contact information, with complete business name, address, zip code, and telephone number in this field.

Payer’s TIN

This is the payer’s taxpayer identification number (TIN). In most situations, this will be the employer identification number (EIN).

The payer’s TIN should never be truncated.

Recipient’s TIN

As the recipient of IRS Form 1099-B, you should see your taxpayer identification number in this field. The TIN can be any of the following:

- Social Security number (SSN)

- Individual taxpayer identification number (ITIN)

- Adoption taxpayer identification number (ATIN)

- Employer identification number (EIN)

Please review this field to make sure that it is correct. However, you may see a truncated form of your TIN (such as the last four digits of your SSN), for privacy protection purposes.

Copy A, which is sent to the Internal Revenue Service, is never truncated.

Recipient’s Name And Address

You should see your legal name and address reflected in these fields. If your address is incorrect, you should notify the lender and the IRS.

You can notify the IRS of your new address by filing IRS Form 8822, Change of Address. Business owners can notify the IRS of a change in their business address by filing IRS Form 8822-B, Change of Address or Responsible Party, Business.

Account Number

This field is present in many information returns, such as IRS Form 1099-NEC or IRS Form 1099-MISC.

Your lender have established a unique account number for you, which may appear in this field. If the field is blank, you may ignore it.

However, the account number is required if the financial institution has:

- Created multiple accounts for a recipient, and

- Is filing more than Form 1099-B for that person

The account number is also required if the filer checks the FATCA filing requirement checkbox.

CUSIP number

This field shows the CUSIP (Committee on Uniform Security Identification Procedures) number or other applicable identifying number for certain securities.

FATCA filing requirement

The form issuer may check this box if they are either:

- a foreign financial institution (FFI) reporting payments to a U.S. account pursuant to an election described in Treasury Regulations Section 1.1471-4(d)(5)(i)(A), or

- A United States based payer reporting on Form 1099-B to satisfy a requirement regarding a U.S. account as described in Treasury Regulations Section 1.1471-4(d)(2)(iii)(A)

If you see this box checked, you may have filing requirements of your own. For additional information, refer to the instructions for IRS Form 8938, Statement of Specified Foreign Financial Assets.

Boxes 1 through 13

On the right-hand side of the form, we’ll see information that you may need to report on your income tax return. Before we start with Box 1a, let’s check out the field at the very top of the form.

Applicable checkbox on Form 8949

The form issuer may enter a one-letter code, intended to help you report this particular transaction on either IRS Form 8949, Sales and Other Dispositions of Capital Assets, or IRS Schedule D, Capital Gains and Losses, on your Form 1040.

Below are the one-letter codes you might see, and what each of them means.

Code A

This code indicates a short-term transaction for which the form issuer is reporting cost or other basis to the IRS.

If the issuer marked this transaction with Code A, you should report that transaction on either:

- Schedule D, Line 1a, or

- IRS Form 8949, with:

- Box A checked

- Totals carried to Schedule D, Line 1b

Code B

Code B indicates a short-term transaction for which the form issuer is not reporting cost or other basis to the IRS.

If the issuer marked this transaction with Code B, you should report that transaction on IRS Form 8949 with Box B checked. Carry the totals to Schedule D, Line 2.

Code D

This code indicates a long-term transaction for which the form issuer is reporting cost or other basis to the IRS.

If your Form 1099-B contains Code D, then you should report it on either:

- Schedule D, Line 8a, or

- IRS Form 8949, with:

- Box D checked

- Totals carried to Schedule D, Line 8b

Code E

Code E indicates a long-term transaction for which the tax form issuer is not reporting cost or other basis to the IRS.

If the issuer marked this transaction with Code E, you should report that transaction on IRS Form 8949 with Box E checked. Carry the totals to Schedule D, Line 9.

Code X

If you see Code X in this box, this means that the form issuer cannot determine the holding period.

As a result, this tax document cannot help you determine whether to report a long-term capital gain or loss or short-term gain or loss.

Box 1a: Description of property

Box 1a shows a brief description of the item or service for which the form issuer is reporting tax information.

For regulated futures contracts and forward contracts: You may see ‘RFC’ or other description of the contracts shown.

Section 1256 option contracts: ‘Section 1256’ or other description

For a corporation that experienced a reportable change in control or capital structure: Box 1a may show the class of stock as one of the following:

- C: Common stock

- P: Preferred stock

- O: Other class of stock

For bartering transactions: You may see a description of the property or service provided.

Box 1b: Date acquired

This box contains date that you acquired the security or securities.

Box 1b may be blank if:

- The filer checked Box 5, or

- If you acquired the securities in various transactions on different dates

For short sales, this date reflects the date that you acquired the security delivered to close the short sale.

Box 1c: Date sold or disposed

Box 1c contains the sale date or exchange date.

For short sales, Box 1c indicates the date that the security was delivered to close the short sale.

If reporting barter exchanges, this box reflects the date that cash, property, a credit, or scrip is actually or constructively received.

For aggregate reporting in Box 8 through Box 11, no entry will be present.

Box 1d: Proceeds

This box shows the gross proceeds, reduced by any commissions or transfer taxes related to the sale of securities, for transactions involving:

- Sales of stocks

- Debt instruments

- Forward contracts

- Non-Section 1256 option contracts, or

- Securities futures contracts

Box 1d may show the proceeds from the disposition of your interest or interests in a widely held fixed investment trust.

This box might also show the aggregate amount of cash and the fair market value of any stock or other property received in a reportable change in control or capital structure arising from the corporate transfer of property to a foreign corporation.

Losses on forward contracts or non-Section 1256 option contracts will appear in parentheses.

This box will not include proceeds from regulated futures contracts or Section 1256 option contracts.

This box will not contain accrued qualified stated interest on bonds sold between payment dates (or on a payment date). Instead you should find this accrued interest on IRS Form 1099-INT, Interest Income.

How to report on your tax return

Report this amount on either IRS Form 8949 or Schedule D, as applicable.

Box 1e: Cost or other basis

Shows cost basis or other basis of securities sold.

If you acquired the securities through the exercise of a noncompensatory option granted or acquired on or after January 1, 2014, the filer has adjusted the cost basis information to reflect your option premium.

For securities that you acquired through the exercise of a noncompensatory option granted or acquired before January 1, 2014, your broker may, but does not have to, adjust the basis to reflect your option premium.

If you acquired securities through the exercise of a compensatory option, such as incentive stock options, the basis has not been adjusted to include any amount related to the option that was reported to you on a Form W-2.

If Box 5 is checked, Box 1e may be blank. IRS Publication 550, Investment Income and Expenses, may contain additional information, depending on the type of transaction.

Box 1f: Accrued market discount

Shows the amount of accrued market discount. If Box 5 is checked, this box may be left blank.

accrued market discount vs. Original issue discount

Accrued market discount is the gain in the value of a discount bond expected from holding it for any duration until its maturity. Because discount bonds are sold below face value, they usually will gradually rise in market price until they reach maturity.

Original issue discount bonds, such as zero-coupon bonds, are originally issued at a discount. Original issue discount, or OID, is reported on IRS Form 1099-OID, instead of Form 1099-B.

Report accrued market discount in Column (g), Line 1 of IRS Schedule B, Interest and Ordinary Dividends. Identify this as ‘Accrued Market Discount,’ in the available space.

Publication 550 contains more information on how accrued market discounts are calculated for debt instruments, such as bonds or certificates of deposit.

Box 1g: Wash sale loss disallowed

Shows the amount of nondeductible loss in a wash sale transaction.

Wash sales

According to IRS Publication 550, a wash sale occurs when you sell or trade stock or securities at a loss and within 30 days before or after the date of the sale you:

- Buy substantially identical stock or securities,

- Acquire substantially identical stock or securities in a fully taxable trade,

- Acquire a contract or option to buy substantially identical stock or securities, or

- Acquire substantially identical stock for your individual retirement arrangement (IRA) or Roth IRA.

According to tax laws, you cannot deduct capital losses generated by wash sales on your income tax return for federal tax purposes.

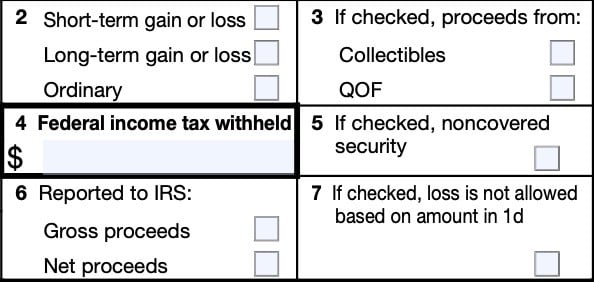

Box 2

The short-term and long-term boxes pertain to short-term gain or loss and long-term gain or loss on the sale of stocks or other securities.

If there is a check in the “Ordinary” box, special rules may apply, depending on the type of security reported.

Box 3

If checked, proceeds are from a transaction involving collectibles or from a Qualified Opportunity Fund (QOF).

Long-term gains from the sale of collectibles are subject to a different tax rate than other securities.

Taxpayers may defer capital gains from the sale of qualified opportunity funds, based on certain conditions.

Box 4: Federal income tax withheld

You should see backup withholding amounts reported in Box 4. If you have not given your TIN to the payer, you may be subject to backup withholding rules on payments made on IRS Form 1099-B.

In this case, you may need to complete IRS Form W-9 Request for Taxpayer Identification Number and Certification. This will allow the payer to report the correct TIN to the Internal Revenue Service.

Foreign recipients may need to complete IRS Form W-8 instead.

You should include this amount on your Form 1040 or Form 1040-SR as tax withheld when filing your income tax return.

Box 5

If Box 5 is checked, this indicates that the securities sold were noncovered securities. The following boxes may be blank as a result:

- Box 1b: Date acquired

- Box 1e: Cost or other basis

- Box 1f: Accrued market discount

- Box 1g: Wash sale loss disallowed

- Box 2: Type of gain

Noncovered securities

Noncovered securities are securities that are not subject to added reporting by your broker on any Form 1099-B you may receive.

Generally, a noncovered security means one of the following:

- Stock purchased before 2011

- Stock in most mutual funds purchased before 2012

- Stock purchased in or transferred to a dividend reinvestment plan before 2012

- Debt instruments acquired before 2014

- Stock options granted or acquired before 2014, or

- Securities futures contracts executed before 2014

Box 6

Box 6 indicates whether the proceeds in Box 1d were gross proceeds or net proceeds.

If the exercise of a noncompensatory option resulted in a sale of a security, a checked “Net proceeds” box indicates whether the amount in Box 1d was adjusted for option premium.

Box 7

If there is a check in Box 7, you cannot take a loss on your tax return based on gross proceeds from a reportable change in control or capital structure reported in Box 1d.

The broker should advise you of any losses on a separate statement.

Box 8: Profit or (loss) realized in 2024 on closed contracts

Boxes 8 through 11 report on the following types of transactions:

- Regulated futures contracts

- Foreign currency contracts, and

- Section 1256 option contracts

If you see Boxes 8 through 11 completed, you should not expect any other fields completed, except for Box 1a and Box 4, if applicable.

Box 8 shows the profit or (loss) realized on any closed contract during the current tax year. This includes regulated futures, foreign currency, or Section 1256 option contracts closed during the current tax year.

Box 9: Unrealized profit or (loss) on open contracts-previous tax year

Shows any year-end adjustment to the profit or (loss) shown in Box 8 due to open contracts as of the end of the previous tax year.

Box 10: Unrealized profit or (loss) on open contracts-current tax year

Box 10 shows the unrealized profit or (loss) on open contracts held in your account as of the end of the current tax year. These are considered closed contracts as of the end of the year.

This will become an adjustment reported as unrealized profit or (loss) on open contracts at the end of the following tax year.

Box 11: Aggregate profit or (loss) on contracts

Boxes 8, 9, and 10 are all used to figure the aggregate profit or (loss) on regulated futures, foreign currency, or Section 1256 option contracts for the year, reported in Box 11.

Include this amount on your IRS Form 6781, Gains and Losses From Section 1256 Contracts and Straddles.

Box 12

If Box 12 is checked, the filer has reported the basis in Box 1e to the Internal Revenue Service. Either the short-term gain or long-term gain box in Box 2 will also be checked.

If Box 12 is checked on Form(s) 1099-B and NO adjustment is required, you may be able to report your transaction directly on Schedule D of your income tax return.

If the “Ordinary” box in Box 2 is checked, an adjustment may be required.

Box 13: Bartering

Box 13 shows the following that you may have received from barter exchange transactions:

- Cash received

- Fair market value (FMV) of property or services you received

- FMV of trade credits or scrip credited to your account by a barter exchange

Depending on the nature of the bartering activity, you may have to report profits and losses on either Schedule C, Profit or Loss from Business, or Schedule E, Supplemental Income, when filing your tax return.

IRS Publication 525, Taxable and Nontaxable Income, contains additional information on how to report losses and gains from bartering activities.

State tax information

Boxes 14 through 16 contain tax information for state tax purposes. If you live in a state without income tax, you may not see any information in Boxes 14 through 16.

However, these boxes may contain relevant tax information for up to 2 different states.

Box 14: State name

If applicable, Box 14 will contain the complete name for the state for which your state income tax was withheld.

Box 15: State Identification Number

If your financial institution has a specific state tax identification number, that TIN will appear in Box 15.

Box 16: State Income Tax Withheld

Box 16 contains the state income tax withheld by the state listed in Box 14.

Filing IRS Form 1099-B

For tax entities who must file this tax form with the Internal Revenue Service, the IRS requires certain paper versions of information returns to be accompanied by IRS Form 1096, Annual Summary and Transmittal of U.S. Information Returns.

Check out our step-by step instructional guide for more information on how to submit your information return with IRS Form 1096.

Video walkthrough

Learn more about tax information reported to you on Form 1099-B by watching this instructional video.

Do you use TurboTax?

If you use TurboTax, and you’re completing this tax form for the first time, you might be ready to try TurboTax Federal Premium instead of the free or deluxe versions. TurboTax Federal Premium comes in two offerings, DIY or Live Assisted.

Do it yourself

To learn more about using TurboTax Federal Premium’s DIY option, click here.

Live Assisted

If you feel more comfortable having a tax expert guide you for the first time through this new form (or any other new forms), get started here.

Ready to hand the reins over to someone else completely? Go here to learn more about TurboTax’s Live Assisted Full Service offering!

Frequently asked questions

Brokerage firms and barter exchanges file IRS Form 1099-B to report cash, stock, or property received in exchange for stocks, commodities, debt instruments, regulated futures contracts, foreign currency contracts, securities future contracts, or stock options.

Brokers and barter exchanges must provide Form 1099-B to each recipient by February 15th of the year following the year in which brokerage or bartering activities took place.

You should contact the brokerage firm or barter exchange for your Form 1099-B. If you do not receive a response, you may contact the IRS for assistance by calling 800-829-1040.

Where can I find IRS Form 1099-B?

You can find a copy of the IRS 1099-B form on the IRS website. For your convenience, we’ve enclosed the latest version of this tax form here, in the article.

Related tax articles

This tax form is one of the fillable tax forms provided by the Internal Revenue Service, to help taxpayers reduce their tax preparation costs. To see more forms like this, visit our free fillable tax forms page, where you’ll also find articles like this.

Unlike the IRS, our articles contain step by step instructions for each tax form, as well as video walkthroughs. You can also check out all of our videos by subscribing to our YouTube channel!

Thank you for your videos. I have questions. Do you mind calling me? I’ll leave my email for your reply & send my number from there if you don’t mind.

What questions do you have? For free, I can answer questions on this post, which would be for the benefit of everyone.

If you’d rather discuss your questions one on one, this page contains additional information about how I work with clients. From there, you can select a time to schedule a call to discuss your questions in more depth: https://www.teachmepersonalfinance.com/work-with-me/