IRS Form 8606 Instructions

If you have a nondeductible IRA or if you want to make backdoor Roth conversions, you may need to file IRS Form 8606, Nondeductible IRAs.

This article will walk through:

- How to complete and file IRS Form 8606

- Filing considerations

- Frequently asked questions

Let’s begin with a step by step review of this tax form.

Table of contents

How to complete IRS Form 8606

This section will give you a layman’s guide to filling out Form 8606. As a reminder, this is not tax advice. These are not official instructions from the Internal Revenue Service, and this does not cover every tax situation.

If you’re using tax software like TurboTax, you probably will answer some questions and the software will autopopulate the form for you. But be careful in answering these questions, because mistakes in calculating basis will carry forward each year.

There are three parts to this tax form:

- Part I: Nondeductible contributions to traditional IRAs and distributions to traditional, SIMPLE, and SEP IRAs

- Part II: Roth conversions

- Part III: Distributions From Roth, Roth SEP, or Roth SIMPLE IRAs

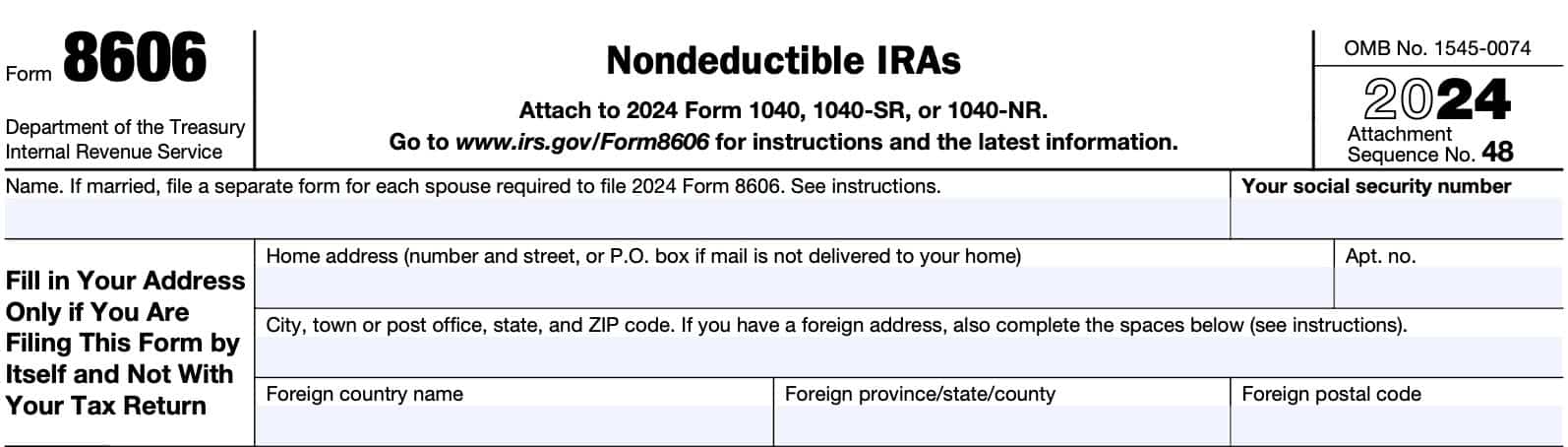

Before we start with Part I, let’s take a look at the taxpayer information fields at the top of the form.

Taxpayer Information

At the top of the form, enter your name and Social Security number. If you are married, you’ll need to complete a separate Form 8606 for each spouse separately.

Complete the address field only if you are filing Form 8606 by itself and not with your federal income tax return.

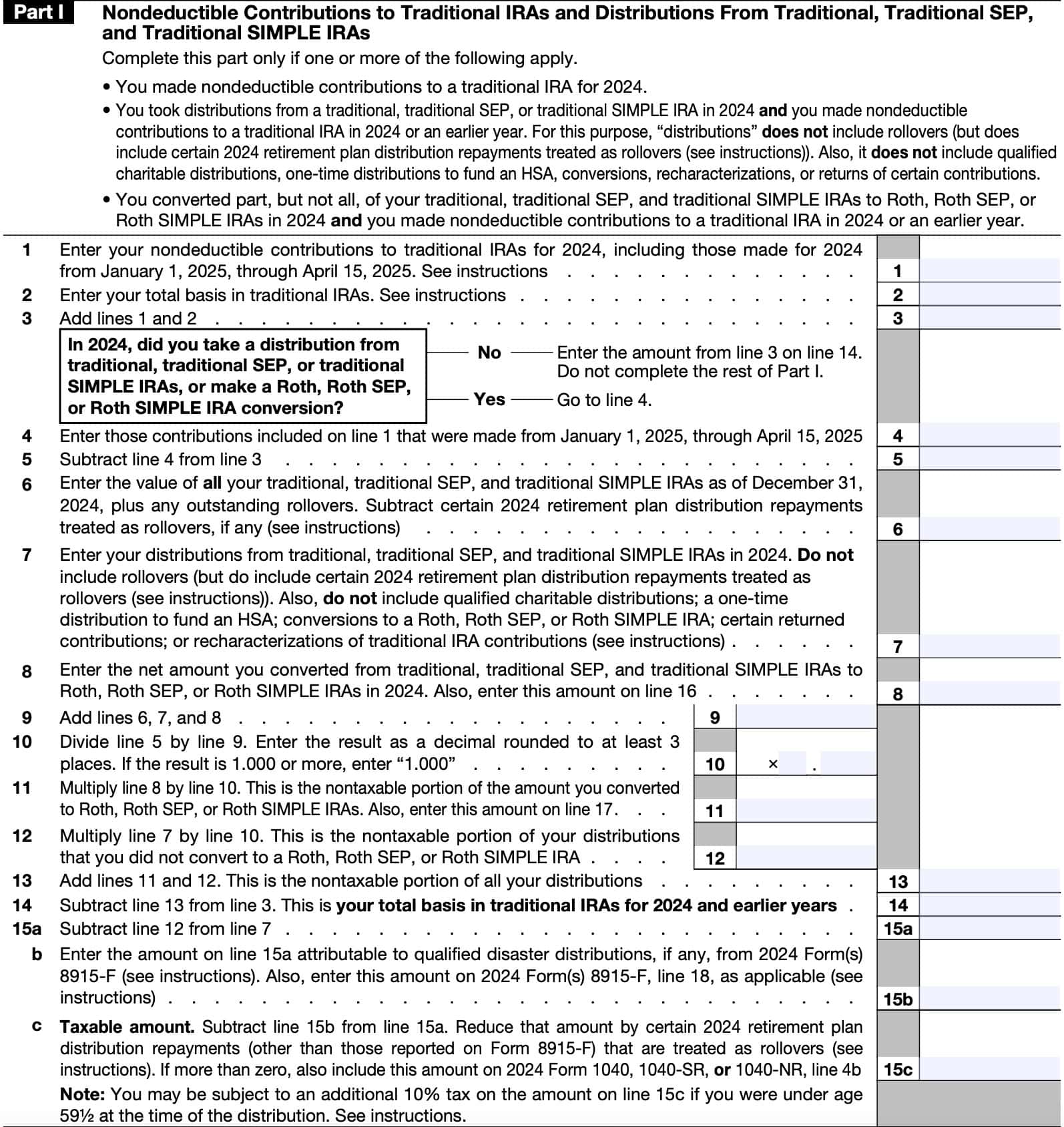

Part I: Nondeductible Contributions To Traditional IRAs And Distributions To Traditional, SIMPLE, And SEP IRAs

You only fill out Part I of Form 8606 if one of the following apply:

- You made nondeductible IRA contributions in the current tax year

- You took distributions from a traditional, SIMPLE, or SEP IRA in the current tax year AND you made nondeductible IRA contributions in the current year or an earlier year

- You converted part (but not all) of your traditional, SEP, or SIMPLE IRA assets in the current tax year AND you made nondeductible IRA contributions in the current tax year or an earlier year

If this applies to you, then here’s what you should include for each line.

Line 1: Nondeductible Traditional IRA Contributions

You’ll include all nondeductible traditional IRA contributions for the tax year here. The tax year includes up to the filing deadline.

So for the 2024 tax year, you could include any nondeductible IRA contribution made from January 1, 2025 through the 2024 tax filing deadline, which is April 15, 2025.

But if you made a contribution in January through April of 2025 for tax year 2025, do not include that number here. You’ll save it for the tax filing season in 2026.

IRA deduction worksheet

If you used the IRA deduction worksheet located in the Schedule 1 instructions, or from IRS Publication 590-A, you should refer to the instructions for additional guidance. You can watch this video below for a step by step walkthrough of the IRS deduction worksheet.

Line 2: Basis In Traditional IRAs

This is basis that will transfer from previous tax years. If this is your first year filing Form 8606, then this number will probably be zero.

However, even if this is your first filing year, you may still have basis if:

- You had a return of excess traditional IRA contributions

- You had a transfer of part or all of a traditional, SIMPLE, or SEP IRA incident to divorce or separation

- You had a rollover of a nontaxable amount from a qualified retirement plan to your traditional, SIMPLE, or SEP IRA that you did not previously report.

If you’re carrying forward basis from a previous tax year, you’ll use the carryforward number from that year’s tax return.

Use the chart below to determine which line to carry forward from your prior year form:Use the chart below to determine which line to carry forward from your prior year form:

| If your most recent Form 8606 was… | Then use this line from your Form 8606 |

| After 2000 | Line 14 |

| After 1992, but before 2001 | Line 12 |

| After 1988, but before 1993 | Line 14 |

| 1988 | The total of the amounts on Lines 7 and 16 of that Form 8606. |

| 1987 | The total of the amounts on Lines 4 and 113 of that Form 8606. |

For example, if your most recent Form 8606 was in 2020, then you would carry forward the number located in Line 14 of that year’s Form 8606. This is the case for all tax returns on or after tax year 2001.

Line 3

Add Lines 1 and 2.

If you did not take a distribution from a traditional, SIMPLE, or SEP IRA, or do a Roth conversion, then the instructions tell you to skip down to Line 14.

Line 4: Contributions Made In The Current Calendar Year

For Line 4, you will back out the contributions for the current year. For example, a 2024 tax return would back out contributions made from January 1 to April 15, 2025.

If you made deductible AND nondeductible IRA contributions in both years, you can decide which contributions were deductible, and which were nondeductible, regardless of tax year.

But for purposes of figuring the nondeductible distributions, contributions made in the later year do not count.

Line 5

Subtract Line 4 from Line 3, then enter the total here.

Line 6: Total Value Of ALL Traditional, SIMPLE, And SEP IRAs Plus Outstanding Rollovers

This is the total of your IRAs at calendar year-end. You’ll usually get a year-end statement account from your financial institution around the end of January of the following tax year.

Outstanding Rollovers

Usually, outstanding rollovers are subject to a 60-day rollover rule. For purposes of reporting on Form 8606, an outstanding rollover is a rollover made after November 1 of the given tax year, but within the 60-day rollover rule.

If a rollover falls outside the 60-day rule, the taxpayer can certify (in writing) why they missed the deadline to the IRA custodian or financial institution. This will allow the institution to properly report the transaction to the Internal Revenue Service. IRS Revenue Procedure 2020-46 gives more guidance on written certifications.

Exceptions to the 60-day rollover rule

Neither of the following are subject to the 60-day rollover rule:

- Direct rollovers: Rollovers between accounts within one financial institution

- Trustee-to-trustee transfers: Rollovers between accounts at separate financial institutions

Forrest’s Tax Tip: When possible, you should use a direct rollover or a trustee to trustee transfer to avoid any possibility of running afoul of the 60-day rule.

Line 7: Distributions From Traditional, SIMPLE, And SEP IRAs

This includes distributions in the given tax year only. For tax year 2024, this would include only distributions made in 2024.

However, you should not include the following items in the Line 7 amount:

- Roth conversions

- Recharacterizations of traditional contributions to Roth contributions

- Rollovers into a qualified plan

- A one-time distribution to fund an HSA

- Distributions that are treated as a return of contribution

- Qualified charitable distributions

- Certain qualified disaster distributions

- Distributions incident to divorce

Line 8: Net Roth Conversions

If you did Roth conversions from a traditional, SIMPLE, or SEP IRA, you’ll enter the net Roth conversion amount here.

This will be the same number you enter on Line 16.

Line 9

Add the following items, then enter the total in Line 9:

Line 10

Divide Line 5 by Line 9. Input the answer as a decimal using 3 decimal places. This represents the ratio of basis to total IRA assets.

For example, if Line 5 was $5,000 and Line 9 was $10,000, then Line 10 would be .500.

This ratio will help you calculate the nontaxable portion of any distributions or Roth conversions on Line 11.

Line 11

Multiply Line 8 by Line 10, then enter the answer here.

For example, if Line 10 was .500 and Line 8 was $2,000, then Line 11 would be $1,000.

This represents the nontaxable portion of your Roth IRA conversions. This number will also go into Line 17.

Line 12

This is the nontaxable portion of your total IRA distributions (not including Roth conversions).

Line 13

Add Lines 11 & 12.

This represents the combined nontaxable distributions from your IRAs, both distributions and Roth conversions.

Line 14: Total basis in traditional IRAs for all tax years

Subtract Line 13 from Line 3.

This represents your total basis in traditional IRA accounts for the reported tax year and earlier tax years.

Line 15

This consists of 3 sections: Line 15a, Line 15b, and Line 15c.

Line 15a

Subtract Line 12, the nontaxable of total IRA distributions but not Roth conversions, from Line 7, total IRA distributions, not including Roth conversions.

Line 15b

The amount from Line 12 attributable to qualified disasters.

Note: If you do not have IRS Form 8915-D or IRS Form 8915-F, you probably will leave this blank.

Line 15c

Subtract Line 15b from Line 15a. This is the taxable part of your IRA distribution.

You will use the number on Line 15c (if it is not zero), on Line 4b of your Form 1040 (taxable IRA distributions).

Early Withdrawal Penalties

If you are under the age of 59½ at the time of distribution, you may be subject to a 10% early withdrawal penalty. Also, if you withdrew from a SIMPLE IRA within the first 2 years of having the account, you may be subject to a 25% early withdrawal penalty.

To calculate early withdrawal penalties, you may need to file IRS Form 5329, Additional Taxes. From there, you would report any additional taxes on Schedule 2 of your Form 1040 when filing your tax return.

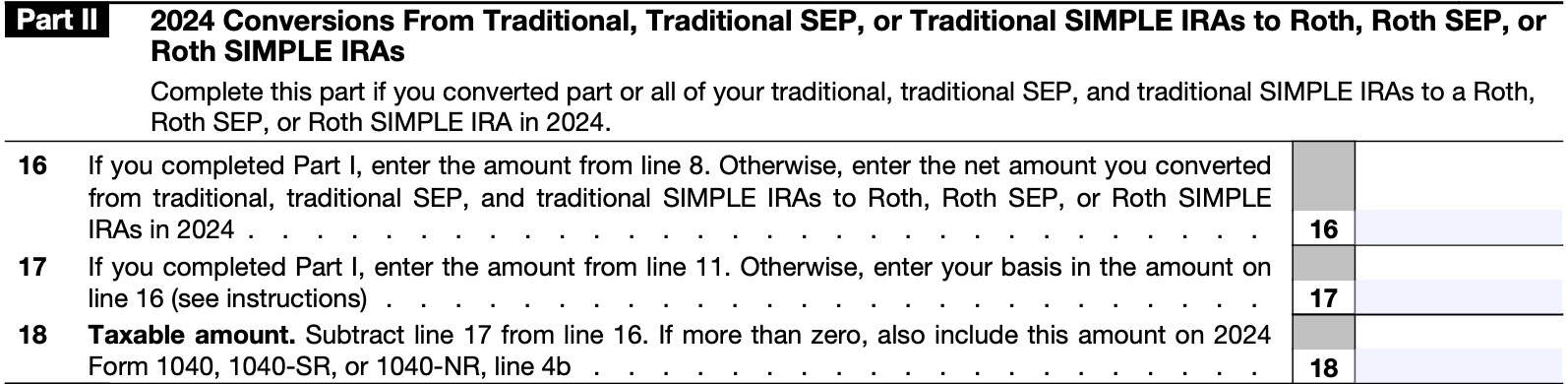

Part II: Roth Conversions

You’ll only fill out Part II if you did Roth conversions during the tax year. If you did not do Roth conversions, then skip to Part III.

Line 16

Carry over the Roth conversion amount from Line 8.

Line 17

Carry over the nontaxable Roth conversion amount from Line 11.

If you did not complete Line 11, then enter the total basis amount from Line 2, plus the contributions you made for the tax year that were made before the conversion.

Line 18: Taxable Amount

Subtract Line 17 from Line 16.

If this number is zero or less, do not include on Form 1040, Line 4b (taxable IRA distributions). You will include this number on Form 1040, Line 4a (IRA distributions).

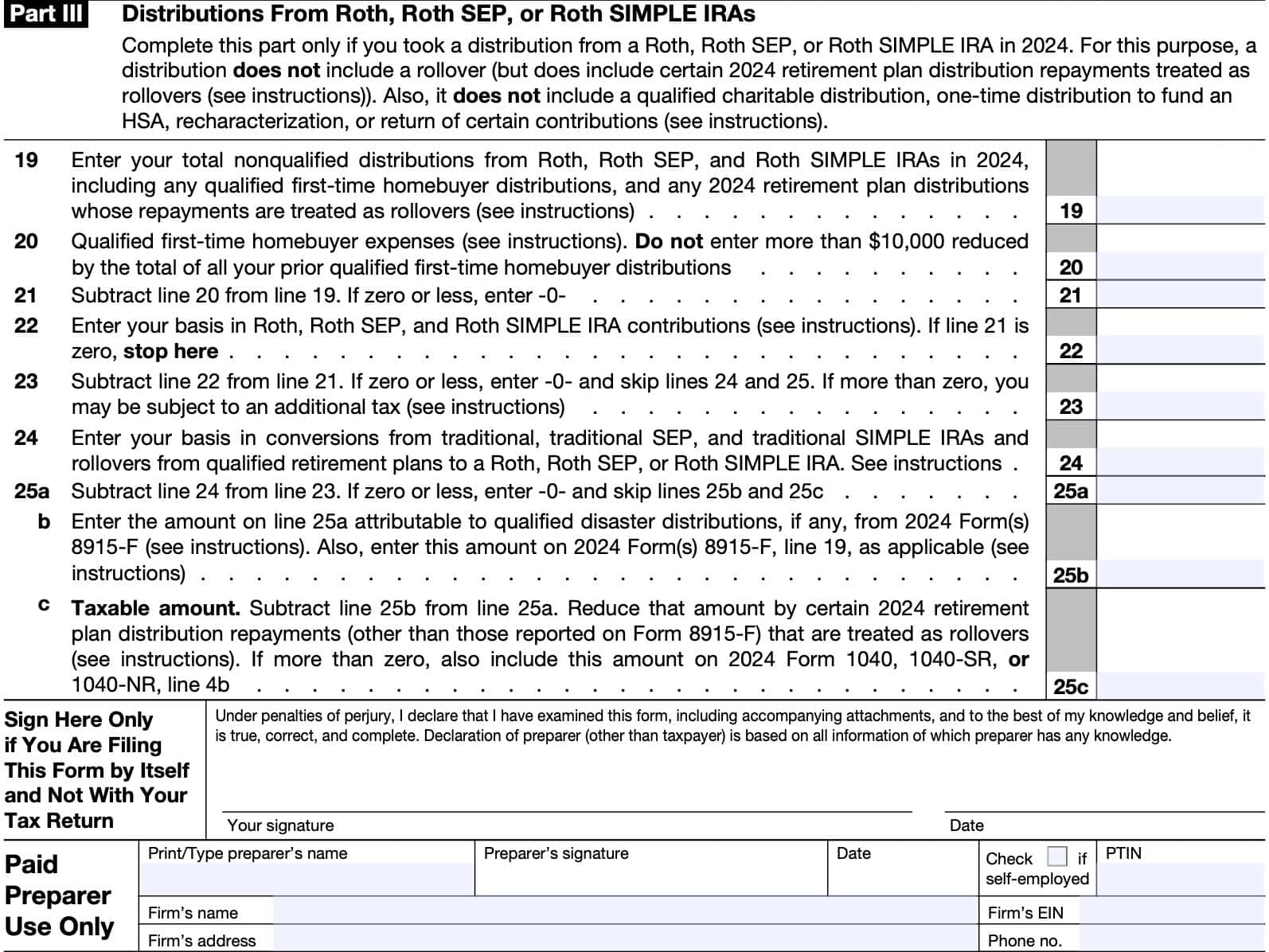

Part III: Roth IRA Distributions

In Part III, we’ll focus on distributions from Roth IRA accounts.

Line 19: Nonqualified Roth IRA Distributions

Include all nonqualified Roth IRA distributions, including qualified first-time homebuyer distributions and qualified natural disaster distributions.

But do not include any of the following:

- Outstanding rollovers

- Recharacterizations

- Distributions that are a return of contributions

- Distributions made on or after age 59½, as long as you made a contribution in any year at least 5 years prior.

- For tax year 2024, this includes contributions for any tax year from 1998 to 2019.

- One-time distribution to fund an HSA

- Qualified charitable distributions (QCDs)

- Distributions made upon death or due to disability for any Roth IRA where a contribution was made at least 5 years prior.

- Qualified distributions from Form 8915-F that were repaid in 2024, on or before the repayment deadline

- Distributions incident to divorce

If you meet the criteria, those qualified distributions will not appear on your Form 8606. So, for most retirees who worry about reporting their Roth IRA withdrawals, you don’t need to worry.

Line 20: Qualified First-Time Homebuyer Expenses

Since the lifetime limit is $10,000, this separate block forces the calculation. Any withdrawals for expenses exceeding this amount may be subject to penalty.

Line 21

Subtract Line 20 from Line 19. If this number is zero or less, you’ll enter 0.

Line 22: Roth IRA Basis

If you’ve never taken a Roth distribution, you’ll simply enter all contributions through the tax year in question.

This also includes adjustments for transfers incident to divorce. Finally, for military death gratuity or SGLI recipients, the proceeds that were rolled into a Roth account are calculated as part of the basis in your Roth account.

If you did take a distribution, you’ll need to calculate the basis using the Basis in Regular Roth IRA Contributions Worksheet for Line 22, in the form instructions. To learn more, watch this video below.

Line 23

Subtract Line 22 from Line 21.

If the basis (Line 22) is more than the distribution (Line 21), this number will be zero, and you can skip to the signature block.

If the basis is less than the distribution, then at least some of your distribution might be taxable.

Line 24

Enter basis from Roth conversions from traditional, SEP, and SIMPLE IRAs, as well as rollovers from qualified retirement plans to a Roth IRA.

If You’ve Never Done A Roth Conversion

This number will be zero.

If You Took A Roth Distribution Before The Tax Year

If you previously took a Roth distribution in excess of your basis in regular Roth IRA contributions in 2011 or later, then your basis is the excess of that year’s Line 24 amount over that year’s Line 23 amount.

For example, if you took a Roth distribution in 2023, then your basis would be the excess of Line 24 from your 2023 Form 8606 over the Line 23 amount from that form.

If your most recent distribution was from a tax year prior to 2011, then you should refer to the form instructions for additional guidance.

If You Did Roth Conversions, But Never Took A Roth Distribution

You’ll include the total of your Roth conversions here. The IRS instructions contain year-by-year instructions on which lines to import conversion amounts from.

This number will be adjusted by any adjustment in basis for conversions or rollovers incident to a divorce.

Line 25

This consists of 3 sections: Line 25a, Line 25b, and Line 25c.

Line 25a

Subtract Line 24 (basis from Roth conversions) from Line 23 (total distributions minus basis from Roth contributions).

Line 25b

Enter the amount from Line 25a attributable to qualified disasters.

Note: If you do not have Form 8915-D or Form 8915-F, you probably will leave this blank.

Line 25c: Taxable Amount

Subtract Line 25b from Line 25a. This is the taxable part of your Roth IRA distribution.

Essentially, Line 25c should be zero, even if you are younger than 59½ if you are withdrawing less than the amount of your total contributions (counted towards basis), and conversions (also counted towards basis). Any additional amounts are considered earnings, and may be taxable if not part of a qualified withdrawal.

Let’s take a closer look at some filing considerations for Form 8606.

Filing considerations

Many taxpayers erroneously believe that since Roth IRA contributions grow tax-deferred, and qualified distributions are tax-free, they’ll never need to report anything. But IRS Form 8606 covers so much more than that.

Below are some filing considerations about IRS Form 8606, starting with what this form actually does.

What Is IRS Form 8606?

IRS Form 8606 is a tax form that helps an IRA owner keep track of and report tax basis in IRA accounts to the Internal Revenue Service.

Despite its limiting title, IRS Form 8606 actually serves multiple purposes:

- Reporting nondeductible IRA contributions

- Reporting distributions from traditional IRAs, SEP IRAs, or SIMPLE IRAs if there is basis in these accounts

- Reporting Roth conversions

Let’s take a look at each one, a little more closely.

Reporting Nondeductible IRA Contributions

Of course, if you’re making nondeductible contributions to a traditional IRA (individual retirement account), you’ll report them here. Reporting nondeductible contributions allows you to report (and keep) track of the basis inside your traditional IRAs.

Keeping track of basis of traditional IRAs isn’t that important while you’re still accumulating retirement savings. However, if you have after-tax dollars and pre-tax dollars in your IRAs, then qualified withdrawals are subject to the Roth conversion pro rata rule.

And in your retirement years, knowing the basis of your IRA accounts will allow you to better determine the tax treatment of your withdrawals. This way, you know exactly how much tax-free money you have access to.

And if you’re doing executing a backdoor Roth strategy every year, you’ll be reporting your nondeductible contributions as part of your backdoor Roth conversion strategy.

Facilitating Backdoor Roth IRA Conversions

If you’re not familiar with the concept of a backdoor Roth IRA conversion, the premise is simple.

When most people start their careers, their gross income is low enough so they can contribute directly to their Roth IRAs. As their careers progress, their income gradually (or suddenly) increases.

At some point, the taxpayer may exceed the income limits for being able to make a direct Roth IRA contribution. Hence, the backdoor Roth conversion.

Instead of contributing directly to a Roth IRA, many taxpayers will make a nondeductible IRA contribution. From there, they’ll make a Roth conversion from their traditional IRA account. Since they’ve already paid tax on the contribution, the Roth conversion is a tax-free transaction.

Nondeductible IRA contributions are reported on Part 1 on IRS Form 8606.

Reporting Distributions From Traditional IRAs, SEP IRAs, Or SIMPLE IRAs If There Is Basis In These Accounts.

Normally, distributions from an IRA in any given tax year are reported on IRS Form 1099-R Distributions From Pensions, Annuities, Retirement or Profit-Sharing Plans, IRAs, Insurance Contracts, etc. And if the distribution is reported only on the 1099-R, and is not a designated Roth distribution, then the assumption is that 100% of the distribution came from the pretax amounts.

Calculating basis in an IRA

But if you made a non-deductible IRA contribution into a traditional account, then you’ve established tax basis in that account, simply known as basis. Generally speaking, basis is the cost of an investment.

For example, let’s imagine you have an IRA with $5,000 in pre-tax money. You make a $5,000 nondeductible traditional IRA contribution. You now have an IRA account worth $10,000, $5,000 of which is your IRA basis.

When reported properly, qualified withdrawals from the portion of the distribution that’s allocated to basis will be excluded from taxable income.

Form 8606 will help ensure that you aren’t subject to double taxation on the same IRA contribution by helping you keep track of the taxable part of the distribution. Distributions from accounts with after-tax amounts are reported on Part 1 of Form 8606.

Reporting Roth Conversions

If you’re implementing your Roth conversion strategy, then you’ll be reporting Roth conversions on Form 8606 as well. Form 8606 helps track the cost basis of all IRA balances, including non-deductible contributions.

Again, the intention is to avoid paying income taxes twice on the same investment in your own IRA. Roth conversions from a traditional, SIMPLE, or SEP IRA are reported on Part 2 of Form 8606.

Nonqualified Roth IRA distributions are reported in Part 3 of Form 8606. This includes a one-time distribution for a first-time homebuyer.

Part 3 is used to determine whether a tax penalty might apply to a non-qualified Roth IRA distribution. If so, Part 3 will indicate this.

Who Must File Form 8606?

According to the IRS, a taxpayer must file Form 8606 if they:

- Made any nondeductible IRA contribution.

- This includes repayment of a qualified natural disaster or reservist distribution.

- Received distributions from a traditional, SIMPLE, or SEP IRA, and the basis is greater than zero.

- This doesn’t include rollovers, qualified charitable distributions (QCDs), a one-time distribution to fund a health savings account (HSA), conversion, recharacterization, or the return of certain contributions.

- There was a transfer of part or all of an IRA as part of the divorce agreement, and that transfer changed the basis in the account.

- There was a distribution from a Roth IRA.

- There was a distribution from an inherited IRA that had basis, or there was a distribution from an inherited Roth IRA that wasn’t a qualified distribution.

If you’ve filed Form 8606 on your federal income tax return in prior years, you’re probably going to be filing Form 8606 going forward.

Video walkthrough

In this video, we go over how to complete IRS Form 8606, step by step.

Are you tired of dreading tax season?

If you’re like most people, you push through the stress of filing, only to be hit with a bigger bill than expected—then put it all behind you until the same cycle repeats next year.

But what if you could change the game?

Tax planning puts you in control. It’s about being proactive, not reactive—taking small, smart steps throughout the year to reduce your tax burden, increase your savings, and keep more of your hard-earned money working for you.

Here’s what effective tax planning helps you do:

✅ Avoid the surprise of a high tax bill

✅ Understand how your income and decisions affect your taxes

✅ Strategically lower your tax liability over time

Ready to make smarter tax moves?

👉 Join my free weekly tax planning newsletter and get one actionable tip every week to help you reduce your taxes legally and effectively.

Start taking control—your future self will thank you.

Frequently asked questions

IRS Form 8606 is filed annually by a taxpayer as part of their federal income tax return for the prior year. If you’re not required to file a tax return, you would file IRS Form 8606 with the same IRS Service Center where you would normally file your tax return.

If you’re not required to file a Form 1040, you might still need to file IRS Form 8606. For example, you may need to file IRS Form 8606 to report nontaxable amounts on qualified IRA distributions.

You may be reporting incorrect information on your tax return and eventually pay more in federal income tax than you would otherwise have to. Additionally, taxpayers who do not file IRS Form 8606 may face a $50 unless they can demonstrate reasonable cause.

For Roth conversions, you can expect to receive a Form 1099-R from the financial institution reporting on the account where your conversion came from. Normally, the Roth conversions is coded with distribution code 2 in Block 7 of Form 1099-R.

Where can I find a copy of IRS Form 8606?

You can find a copy of this tax form on the IRS website. For your convenience, we’ve enclosed the latest version of Form 8606 below.

If I have made charitable contributions then how do I report it ? It was from my IRA directly to institution . I am 74 years old

It sounds like your charitable contribution was made as a qualified charitable distribution, or QCD.

Below is the guidance on reporting QCDs on your tax return, from the IRS website. It appears that you might not have to use IRS Form 8606 if you had zero basis in your IRA when you made the QCD. In other words, if your entire IRA balance consisted of pre-tax contributions and earnings, then you might be able to report your QCD directly on the Form 1040. However, I would double-check with your tax professional to ensure this is accurate in your situation.

To report a qualified charitable distribution on your Form 1040 tax return, you generally report the full amount of the charitable distribution on the line for IRA distributions. On the line for the taxable amount, enter zero if the full amount was a qualified charitable distribution. Enter “QCD” next to this line. See the Form 1040 instructions for additional information.

You must also file Form 8606, Nondeductible IRAs, if:

you made the qualified charitable distribution from a traditional IRA in which you had basis and received a distribution from the IRA during the same year, other than the qualified charitable distribution; or

the qualified charitable distribution was made from a Roth IRA.

What is a “basis” and how do I figure this out? I only need to fill out Part II. I’m going to do a Trad IRA conversion to Roth IRA.

Here is the basis definition, directly from the IRS Form 8606 instructions: Your basis in traditional, SEP, and SIMPLE IRAs is the total of all your nondeductible contributions and nontaxable amounts included in rollovers made to these IRAs minus the total of all your nontaxable distributions, adjusted if necessary.

In other words, basis is the amount of your contributions that you’ve already paid income tax on, so it’s not taxable. The rest of your IRA balance, including deductible contributions, pre-tax rollovers, and earnings, do not count towards your basis, since you haven’t paid taxes on them yet.

When you do your Roth conversions, you’ll avoid paying taxes on the portion of your conversion that is attributable to basis, but you’ll have to pay taxes on the portion that isn’t part of your basis.

how do i send this to the IRS if I am trying to attach it to my fed tax return?

If you’re filing electronically, your tax preparation software should allow your completed Form 8606 to accompany the rest of your Form 1040, as with other forms and schedules. If you’re filing by paper, then you can print all copies and mail them to the IRS together.

On form 8606:

Lets say you had a traditional IRA with $2000 in it and you convert it to a Roth. You had $1000 withheld for federal taxes( I believe this $1000 is a distribution) and the other $1000 went into a Roth IRA(converted to Roth).

On line 11 of form 8606 you have $100 of the Roth IRA that is nontaxable and on line 12 of form 8606

you have $100 of the distribution that is nontaxable.

On line 16 you enter $2000 from line 8. On line 17 you enter $100 from line 11.

Line 18 is $1900 which is entered on line 4b of 1040 per directions. I assume $2000 goes on line 4a

of form1040.

How do you account for the other $100 that is nontaxable?

Do you ignore the directions and put $1800 on line 4b of 1040?

Do you account for the other nontaxable $100 somewhere else?

Thanks for any help.

Harry Schulz

I’m not sure that I can answer this without actually seeing your Form 8606. Here are some questions that I have:

1. If you’re completing Part I, is that because you made IRA contributions in the same year that you did a Roth conversion? If you started the tax year with a $2,000 balance, and converted the entire amount, why wouldn’t you simply complete Part II? In that case, you would simply report:

Line 16: $1,000 Roth conversion

Line 17: $100 basis

Line 18: $900 taxable amount

You would then report the entire $2,000 distribution on your Form 1040, Line 4a, and $1,900 on Line 4b. The reason for this is because Form 8606 is only capturing the Roth conversion amount, while your Form 1040 captures the entire transaction.

You would then report your taxes paid in the payments section on your Form 1040. Either in Line 25(b), if the taxes were reported on your Form 1099-R (as it seems in your example), or elsewhere, if you paid the taxes with outside money (estimated tax payments or other withholdings).

If you made contributions during the tax year, then you’d have to complete Part I. For that, I’d have to take a closer look at your tax return to make a determination.

To continue my question about 8606:

I am completing Part 1 because I did a Roth conversion and had taxes withheld. I believe you answered my question. To restate my question:

I had $2000 in a traditional IRA $1000.00 was withheld for federal taxes and $1000 went into a Roth.

Line 8 is $1000 ( amount that went into Roth), The basis is $200(for both taxes and Roth) so:

line 11 is $100

line 12 is $100.

Line 13 is $200.

Line 16 is $1000

Line 17 is $100

Line 18 is $900

From what you said I think:

1040 Line 4a is $2000

1040 Line 4b is $1800

What confused me is that form 8606 line 18 shows the taxable amount that is included in 4b from the Roth conversion. The 8606 form and instructions does not tell you with the taxable amount from a distribution.

Thanks

Ha

I still wonder why you completed Part I if you did not make a traditional IRA contribution. According to the form, you should only complete Part I if one or more of the following apply:

• You made nondeductible contributions to a traditional IRA for 2023.

• You took distributions from a traditional, traditional SEP, or traditional SIMPLE IRA in 2023 and you made nondeductible

contributions to a traditional IRA in 2023 or an earlier year. For this purpose, a distribution does not include a rollover

(other than certain qualified disaster distribution repayments from 2023 Form(s) 8915-F), qualified charitable distribution,

one-time distribution to fund an HSA, conversion, recharacterization, or return of certain contributions.

• You converted part, but not all, of your traditional, traditional SEP, and traditional SIMPLE IRAs to Roth, Roth SEP, or

Roth SIMPLE IRAs in 2023 and you made nondeductible contributions to a traditional IRA in 2023 or an earlier year.

From what I understand, if you didn’t make any contributions, then the first item doesn’t apply. The form specifies that a Roth conversion is not the same as a distribution, so the second item doesn’t apply. If you converted all of your IRA to a Roth account, then the third item doesn’t apply.

Is there something that I missed?

The reason I filled out part 1 of form 8606:

I converted a traditional IRA to a Roth and had federal taxes withheld and I had made non-deductable contributions in previous years. I think the tax withheld is a distribution so filling out Part 1 is required.

Also, I did not convert all of the IRA and had made non-deductable contributions in previous years so filling out Part 1 is again required.

Thanks for the help

Harry

Forrest,

Just wanted to confirm my understanding of form 8606.

I did a rollover conversion from a Traditional IRA to a Roth IRA in December, 2024.

I also made a payment for estimated taxes on this rollover.

In looking at the 1040 instructions it says to look at form 8606.

I was going to report the same amount on line 4A and 4B.

Do I still also have to file form 8606.

None of the IRA funds that were roll overed were Nondeductible funds.

If yes would I only use Part II of the form.

Since there is no basis it will result in the same amount to be put on line 4A and 4B.

Appreciate your reply to this.

Regards

Daniel,

You do have to file IRS Form 8606. You’ll complete Part I, but there will be a lot of zeroes in it, regarding basis. You should put the same amount on Lines 4a and 4b of your Form 1040. Be sure to include the taxes paid amount as part of the Line 4a and 4b amount (and to report it in the Payments section, which some people forget).

Forrest,

Thank you for getting back to me.

Based on your earlier response I do have to file form 8606.

In looking at the instructions for Part 1 it those not look like any of those reasons apply to me for filling out Part 1.

I did a rollover of funds from a Traditional IRA to a Roth IRA, but I have not made any nondeductible contributions to a Traditional IRA in 2024 or in a earlier year.

In the instructions it says that both should apply in order to have to fill out Part I.

It looks to me that I only have to fill out Part II.

As a example, lets say I roll overed $20,000 and this is the net amount.

Line 16 would be $20,000

Line 17 would be $0.00

Line 18 would be $20,000.

This $20,000 would be entered on line 4A and 4B of form 1040.

Would this be correct or am I missing something?

I do not see where Part 1 would apply in my case.

If Part I needs to be filled out can you explain what line items I would need to fill.

Also, I made a estimated payment for taxes on this at the time of the rollover,

I plan to report this estimated payment on line 25 c of Form 1040 as other forms of tax payment.

Please advise if this would be the correct reporting on this.

Appreciate your help on this.

Regards

I think everything you said is on point. You shouldn’t have to complete Part I if you’ve never made nondeductible contributions. You have no basis.

The amounts you report in Part II and on your Form 1040 look correct as well.

The one item I’d look into is the estimated payment for Line 25c. You might consider entering it on Line 26, instead, unless you had taxes withheld directly on your Form 1099-R (then it would be Line 25b). I don’t think this matters too much, as long as the tax payment is correct.

Otherwise, I think everything else is in order.

Forrest,

Thank you for the information on this.

Best Regards