Form SSA-44 Instructions

Did you receive an IRMAA determination letter? If you have recently experienced a life-changing event, you may be able to use Form SSA-44, also known as Medicare Income-Related Monthly Adjustment Amount – Life Changing Event.

The SSA-44 allows the Social Security Administration (SSA) to make the necessary corrections to lower or eliminate your IRMAA costs.

In this article, we’ll walk you step by step through:

- How the SSA-44 works

- When you might consider using the SSA-44

- Key information you can find on the SSA-44

- How to fill out the SSA-44

- What documentation you may need to send with your filled out SSA-44

- How to submit the SSA-44 for consideration

- Resources that may help you walk through the SSA-44 form

We’ll start by walking through how to complete the form, step by step. But before we do, I’ve created a low-cost, convenient course that goes through everything you’re about to read below.

If you don’t want to read all of this information, please visit my IRMAA course page to decide if it’s right for you. If not, please feel free to read this article and watch the YouTube tutorial, free of charge!

Table of contents

How to fill out the SSA-44

There are five simple steps to filling out the Social Security Form SSA-44:

- Step One: Type of Life-Changing Event

- Step Two: Reductions in Income that have Already Occurred

- Step Three: Anticipated Reductions in Modified Adjusted Gross Income Next Year

- Step Four: Documentation

- Step Five: Signature

We will break down each step of the SSA-44 so you can clearly understand what is required in this essential document.

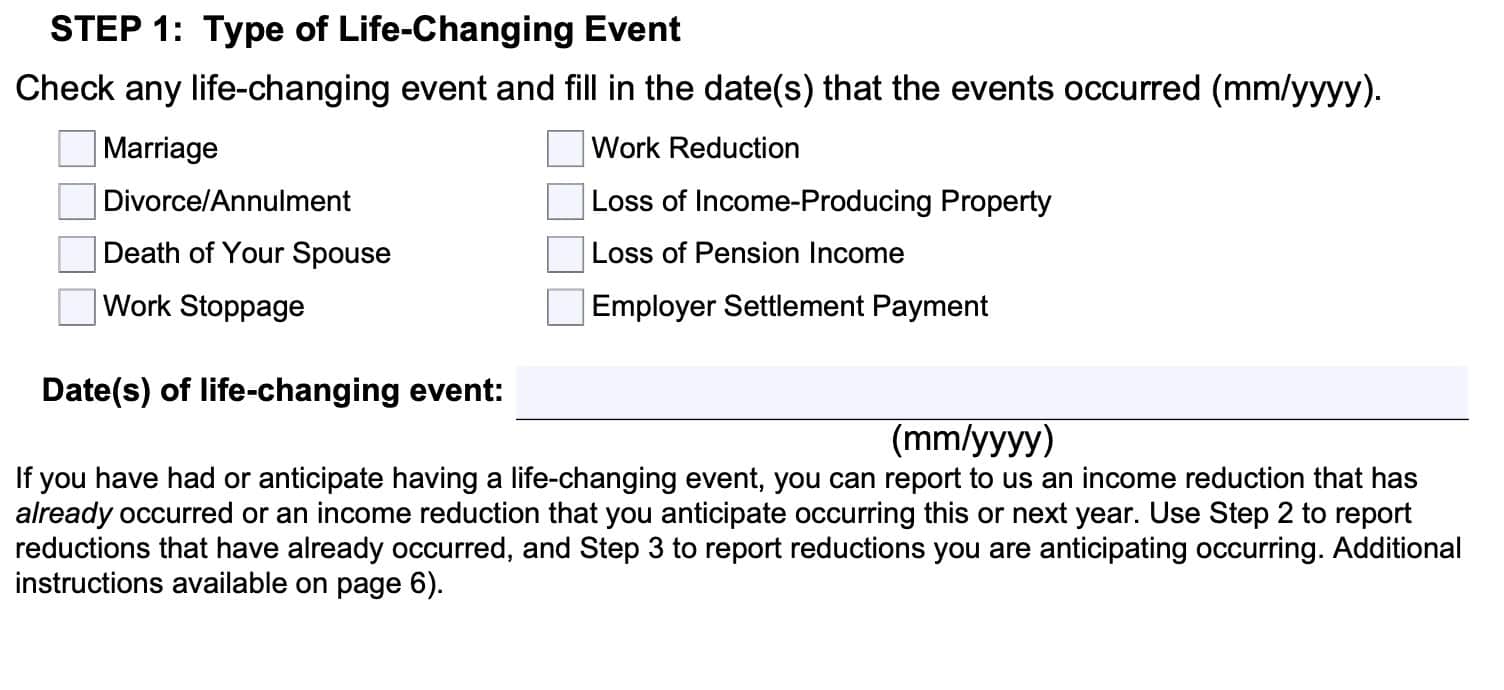

Step One: Type of Life-Changing Event

This is the type of life-changing event that happened in your life, and when that major life event occurred. If one of these events created a significant reduction in your income levels, then you can request an IRMAA reduction.

The eight types of life-changing events that SSA will consider in their IRMAA determination are:

- Marriage: You entered into a legal marriage

- Divorce/Annulment: Your legal marriage ended, and you will not file a joint return for the year.

- Death of your spouse: Your spouse died.

- Work Stoppage: You or your spouse stopped working.

- Work Reduction: You or your spouse reduced your work hours

- Loss of Income-Producing Property: You or your spouse experienced a loss of income-producing property not under your control.

- Examples include disaster, losing property due to arson, fraud or theft

- Loss of Pension Income: You or your spouse experienced some sort of disruption (cessation, termination, or reorganization) of an employer’s pension plan.

- Employer Settlement Payment: You or your spouse receive a settlement from your employer/former employer because of bankruptcy.

SSA 44 Step One asks what type of life-changing event occurred and when it happened. This step also asks for the date that the event took place, because it must be in the same tax year or an earlier tax year than the one you ask SSA to consider.

Let’s imagine that the SSA calculated the 2026 IRMAA with 2024 tax information. However, you got married in 2025. In that case, you could use the 2025 information instead.

If you have already had, or are expecting a life-changing event

You can use Form SSA-44 to report anticipated future events that will lower your income, or you can report an income reduction that has already occurred.

Use Step 2 to report reductions that have already occurred, and Step 3 to report reductions that you expect in the future.

Step Two: Reductions in Income That Have Already Occurred

The second step is where you fill in the modified adjusted gross income (MAGI) for the given tax year. For most people, the 2024 tax data would have gone into the 2026 IRMAA calculation.

The SSA calculates your MAGI using two lines on your tax return:

- Adjusted Gross Income: Line 11 of Form 1040 or Form 1040-SR of your tax return

- Tax-Exempt Interest: Line 2a of Form 1040 from your tax return

- An example of tax-exempt interest would be municipal bond interest.

SSA 44 Step Two asks for your tax information and filing status for the tax year in question. You’ll simply fill in this information, as well as the tax filing status for that year.

Be sure that you only report what was already reported on your tax return. Don’t change anything here. That will be in Step 3.

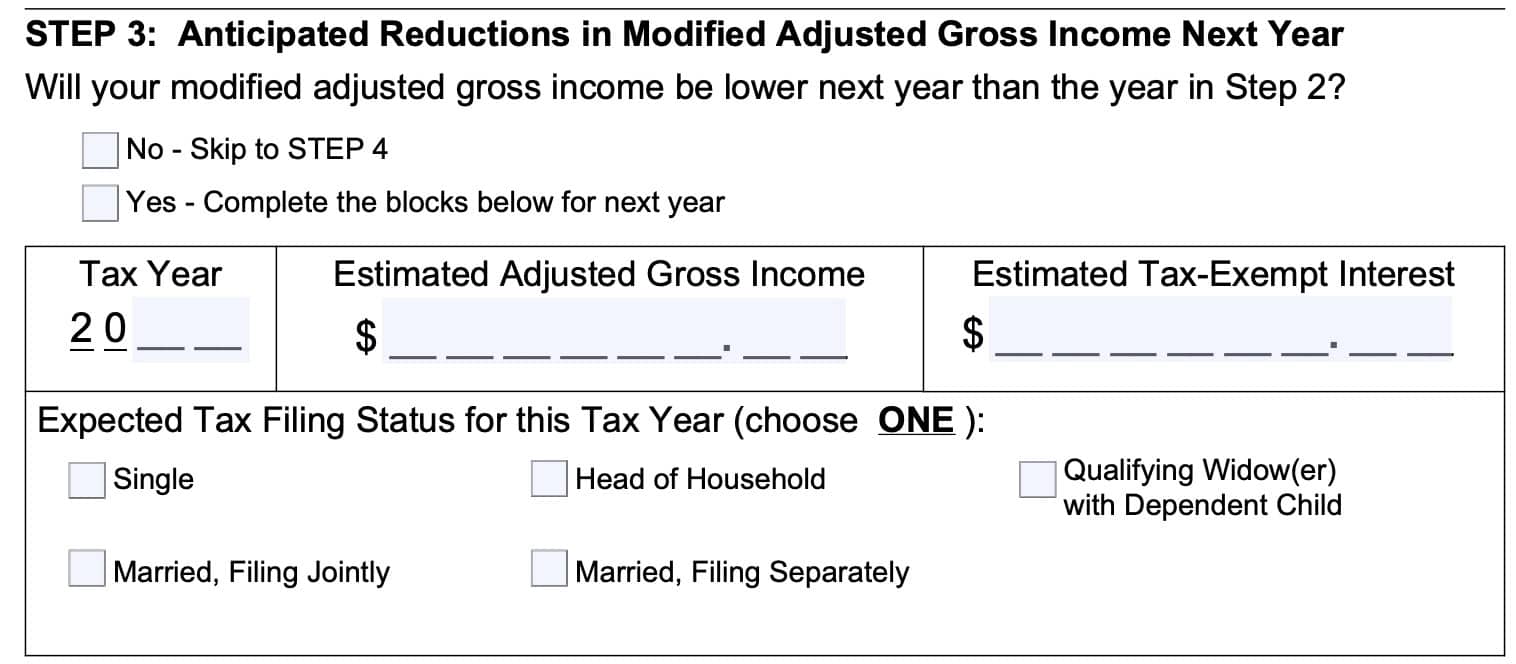

Step Three: Modified Adjusted Gross Income

This is where you estimate your household income to be based upon your life-changing event. This step has three parts:

- Will your MAGI be lower next year than the year in Step 2?

- If the answer is ‘Yes,’ then you’ll complete the rest of Step 3.

- If the answer is ‘No,’ then you’ll skip to Step 4.

- Note: It doesn’t always have to go down. For example, if you got married, but your income didn’t change, then you would answer ‘No’ and move to Step 4.

- Fill in the tax year, estimated AGI, and estimated tax-exempt interest. If you work with a financial advisor or a tax professional, then they can run a tax projection for you based upon your life-changing event. If not, then you might have to do this yourself.

- Expected tax filing status. If your tax filing status hasn’t changed, then this should be straightforward. However, if you got married or divorced, or became a widow(er), then this might be a little difficult. Below is a little background.

Marriage/Divorce

According to the IRS, your filing status is based upon your marital status as of December 31 of the year on your tax return.

Marriage: If you got married before December 31, then you can file as married (either jointly or separately). If you get married on January 1 of the next year, then you would file as single (unless you are filing jointly with a deceased spouse for the year in question).

Divorce: If your divorce decree is finalized before the end of the year, then you would file as Single. If your divorce becomes effective on January 1 or later, then you would file as married (either separately or jointly).

Deceased Spouse: If your spouse died, then you can file a joint tax return for the year in which they died. After that, you’ll either file as single (if you didn’t remarry), married (if you did remarry), or qualifying widow(er) (if you have a dependent child).

If you are able to file as a qualifying widow(er), that privilege exists for the two tax years after the death of a spouse.

The Internal Revenue Service has a page where you can determine your filing status, which takes about 5-10 minutes to walk through. Check it out in this Youtube video.

SSA 44 Step Three asks for your expected MAGI for the year following the year of your life-changing event.

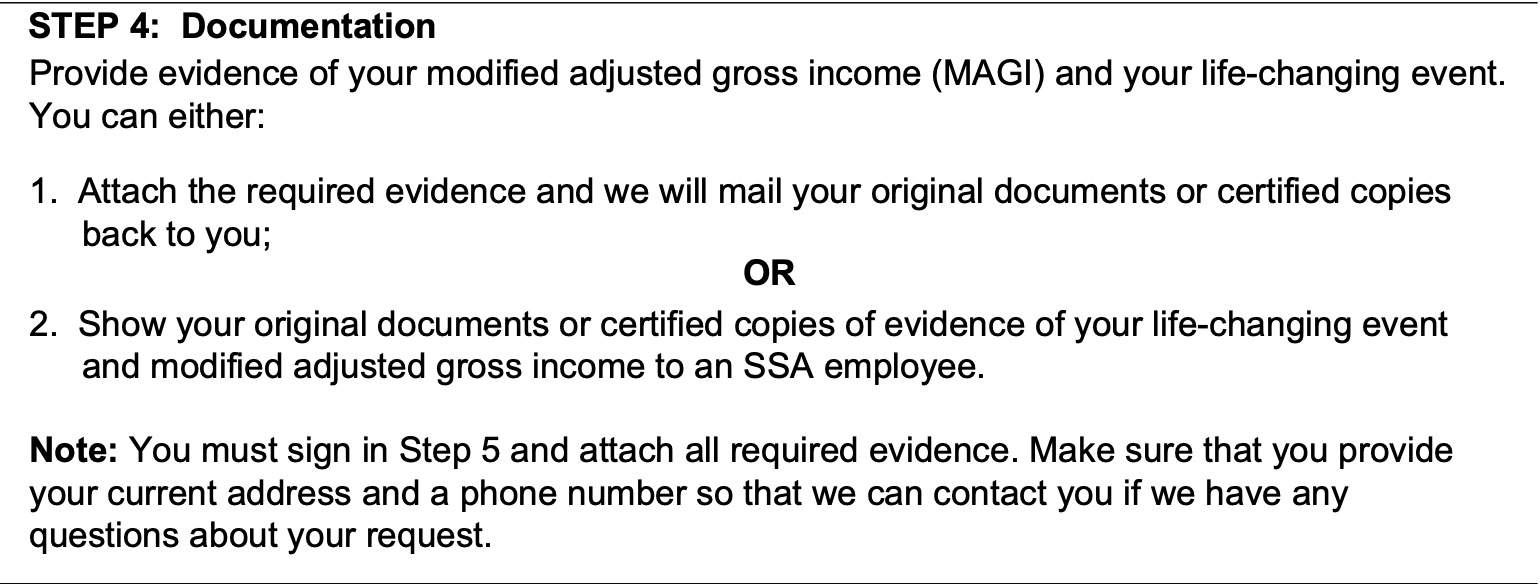

Step Four: Documentation

In this step, you’ll collect the required documents (or certified copies of those documents), depending on your life-changing event. You can find this list on page 8 of the SSA-44.

Hint: If you only have one copy of the document, such as death certificates, you may want to get a copy so you can keep the original.

In the case of a work stoppage or reduction of income, you simply need to sign a statement (under penalty of perjury) that you’ve partially or completely stopped working, or that you took a job with less compensation.

While the SSA returns all submitted documents, you should keep a copy for your own records.

SSA 44 Step Four asks for supporting documentation.

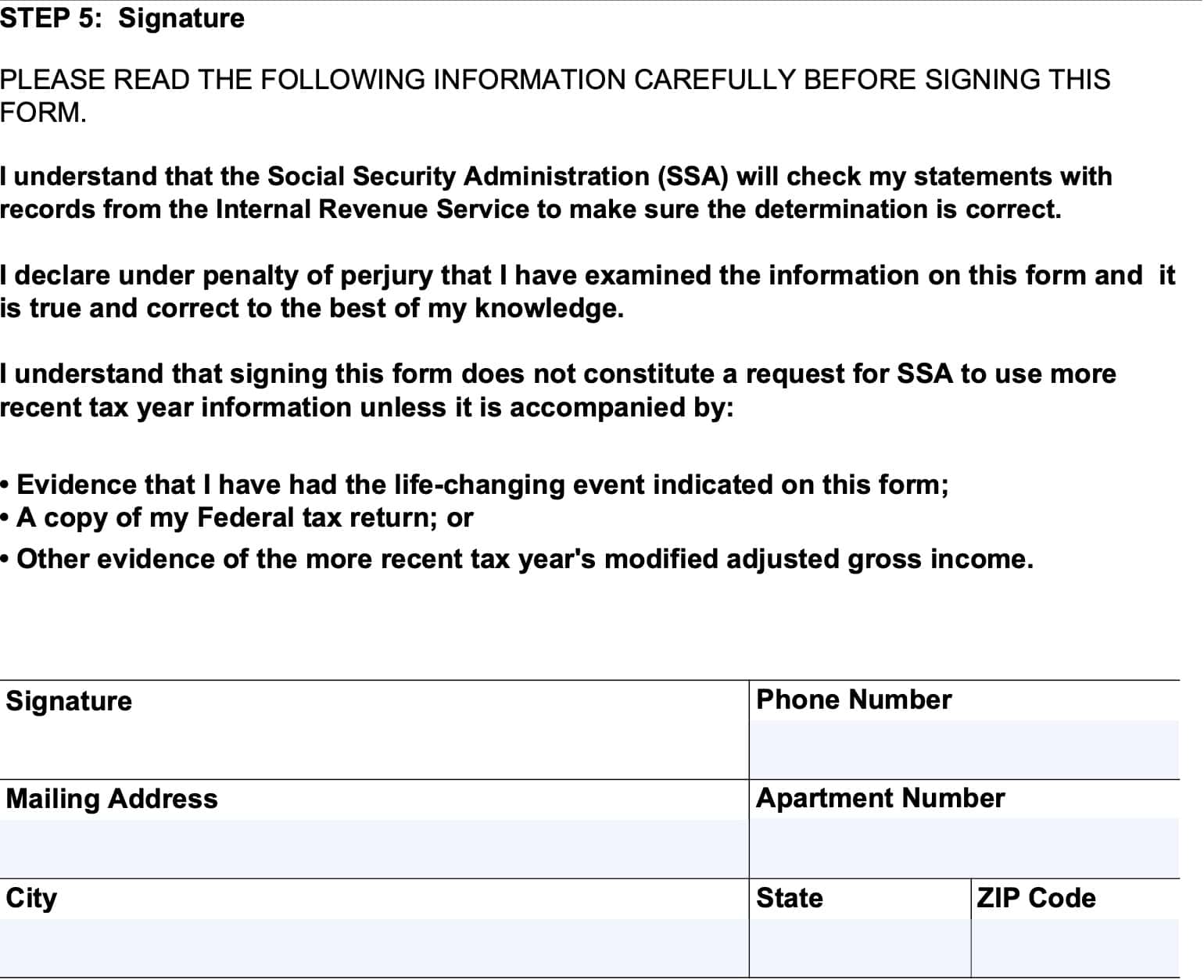

Step Five: Signature

You’ll sign the document under penalty of perjury. In other words, if you attempt to defraud the government, you can face penalties. So this form should only be completed if you’re sincere.

You’ll also want to provide a copy of your tax return, which will help speed up the determination process.

SSA 44 Step Five asks for your signature (sworn under oath). Also, in the contact information fields, enter your mailing address and phone number.

Please note: If there are two spouses on Medicare, you’ll probably each receive an IRMAA determination letter. If that’s the case, then you’ll need to do this for each spouse.

How Form SSA-44 works

IRMAA (also known as Income-Related Monthly Adjustment Amount) is an increase in Medicare premiums based on income level. In other words, the United States government uses your tax returns to determine whether you should pay more for Medicare than the standard premium. If IRMAA applies, you pay an additional surcharge for both Medicare Part B and Part D.

If your income tax returns reflect a higher modified adjusted gross income (MAGI), you’ll receive a letter known as an “Initial Determination Notice.” The Social Security Administration usually sends these notices in advance of the following year.

For example, 2026’s IRMAA letters were sent towards the end of 2025. However, those determinations were mostly based upon 2024 tax returns.

The reason for this is simply because 2025 hadn’t even finished. Because of this process, IRMAA determinations are (at best) based upon tax information that is two years old.

And a lot could have changed in your life between 2024 and 2026 that might have lowered your income. For example, many people retire and their income naturally goes down in retirement.

In recognition of this, the SSA defines significant life changes that may have impacted your income as ‘life-changing events.’

Key information you can find on SSA-44

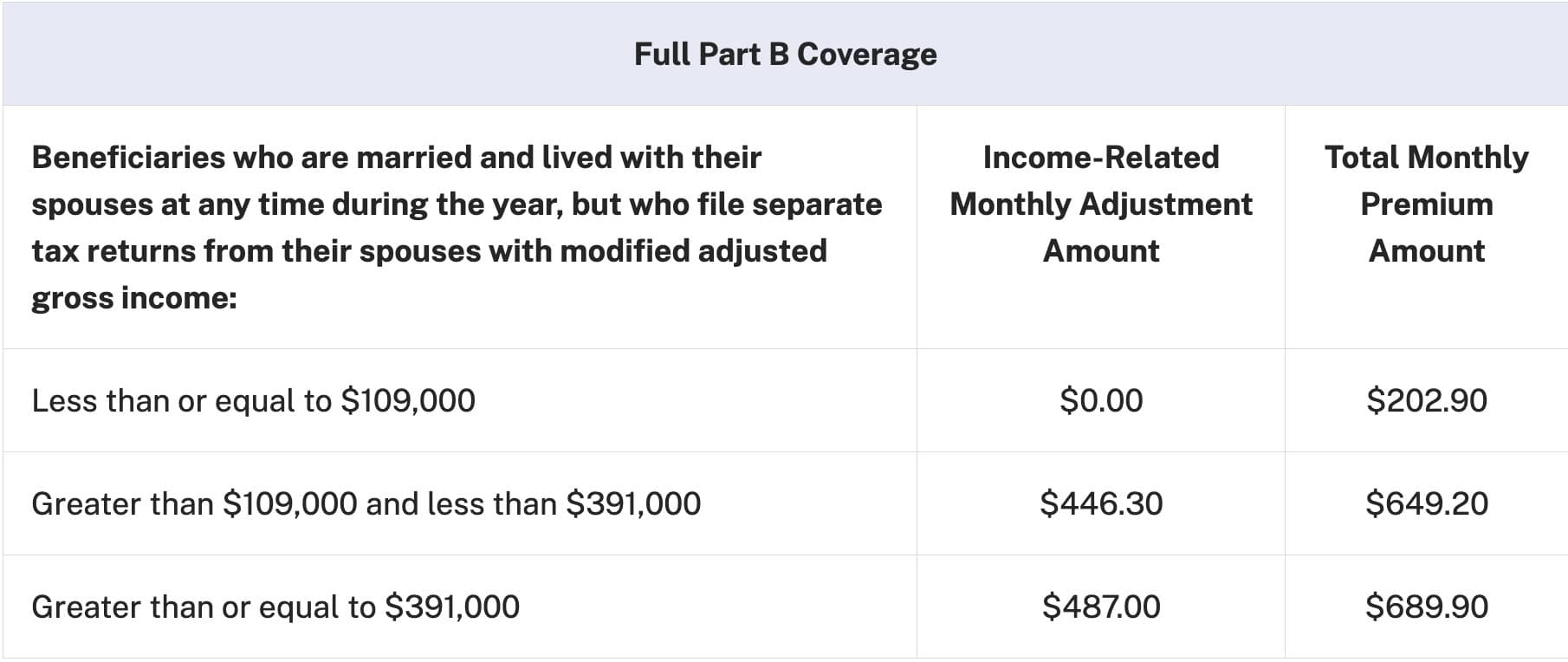

Virtually everything you need to successfully complete the SSA-44 is found on the SSA-44 itself The rates below are 2026 IRMAA rates, based upon information from the Centers for Medicare and Medicaid Services government website).

However, it’s worth pointing out some of the useful things you can find on the form:

Part B premium tables

You can see the IRMAA Part B monthly premiums in the following chart:

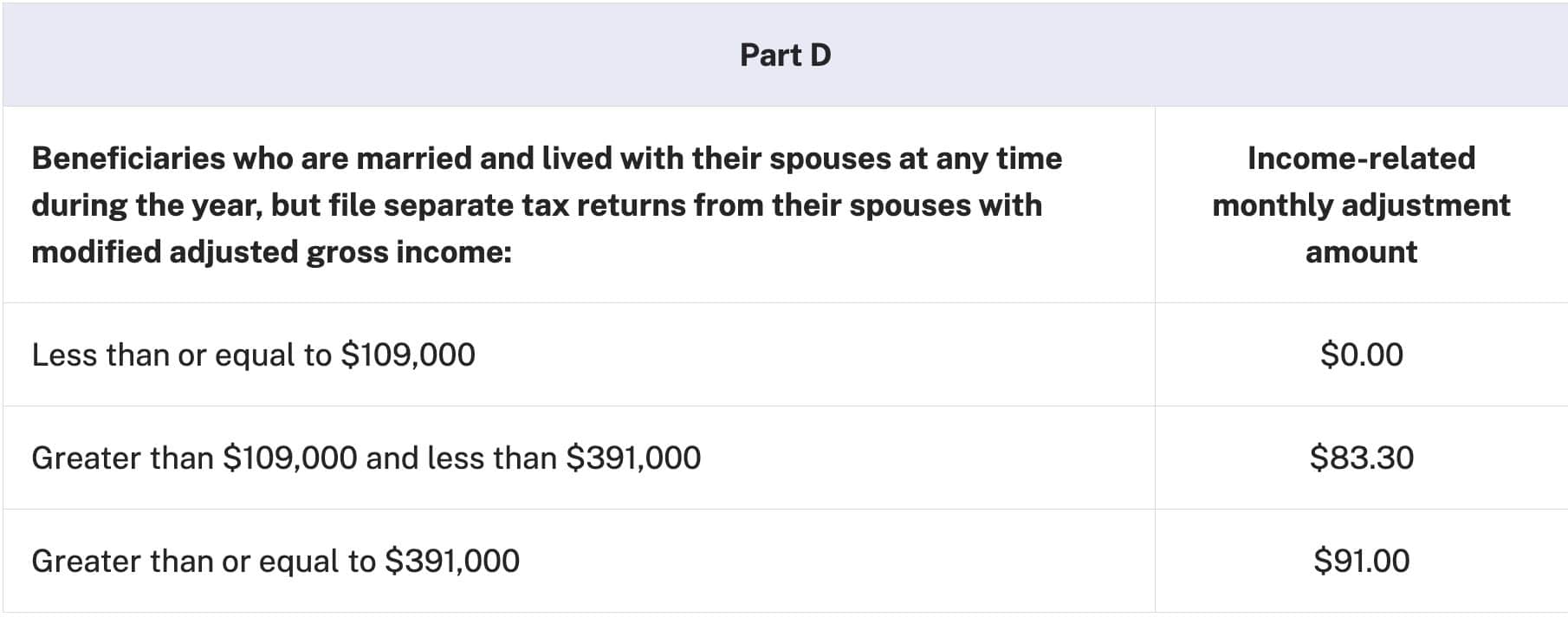

Below is a separate table for married taxpayers filing separate returns.

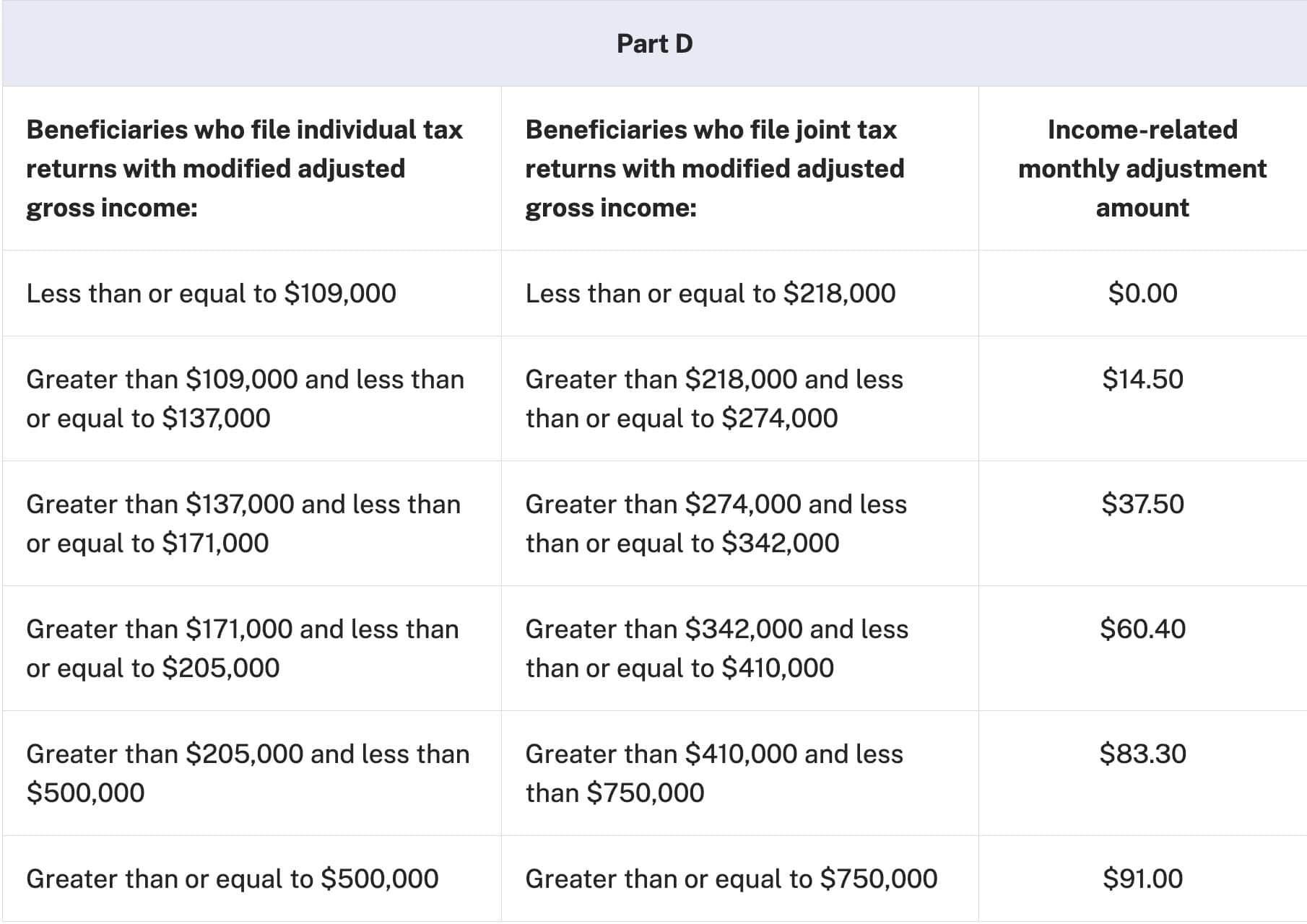

Part D premium tables

And here are the surcharges for Medicare Part D:

From here, you can figure out not only what SSA is billing you, but what you should be paying based upon your life-changing event.

For example, if your 2024 MAGI was $120,000 and you filed a tax return as a single taxpayer, then you would fall under the first IRMAA tier.

This means that you would be expected to pay an additional $74.00 in Part B premiums per month. Your Part D premiums would go up by $13.70 per month.

Let’s say you got married in 2025, but your income wasn’t expected to increase. This is a change in your tax filing status. That means you could be reconsidered as if you were married, filing jointly (which you probably would end up doing when you file your 2025 tax return).

In that case, your $120,000 MAGI would be under the IRMAA threshold and you would not pay any additional premiums.

In other words, you can use this table to have a pretty good estimate of where you’ll end up before you start filling out the paperwork.

Video walkthrough

When you might consider using SSA-44

If a life-changing event has impacted your income, then you would use the SSA-44 to request a reconsideration of the new facts for a new IRMAA determination.

Submitting an SSA-44 is not an appeal—it’s actually much simpler than the appeals process. An SSA-44 asks the SSA to consider new income-related facts as if they were part of the initial determination.

Frequently asked questions about SSA-44

Unfortunately, the Social Security Administration cannot accept electronic versions of this form. You must bring your completed SSA-44 to your local Social Security office for consideration.

Yes. If the Social Security Administration processes your request for consideration, then your new Part B and Part D premiums will be retroactively applied to the beginning of the year. If IRMAA payments were deducted from Social Security benefits, then you should receive an additional payment.

No. You can complete this form yourself, or with the assistance of an SSA representative. There is no reason you should feel compelled to pay someone to complete this form for you.

You can call your local Social Security office for instructions on how to submit the SSA-44 and supporting documentation. To find the closest local office to you, go to the Social Security Office Locator and type in your zip code.

Where can I find a copy of SSA-44?

You can go to the SSA website to save a copy of this form for your records or to complete. You may also obtain a copy from your local SSA office.

For your convenience, we’ve attached the latest version of this form to the bottom of this article.

Related articles

Do you need assistance completing Form SSA 44?

I’ve helped hundreds of people complete and submit their Form SSA-44 to reduce or eliminate their IRMAA surcharges. If you would like to work with me one-on-one, I offer a service where you can schedule a remote appointment to go over your form, step by step.

Please feel free to schedule your appointment here!

Excellent walk-through, having done this three times, it is hard to find good info on this subject.

A couple of things I would add:

1. Step Two applies to the year you had or have the life-changing event, so it can be the current year. Step Three then becomes the next year (future). If you are using the current year for Step Two, you will be estimating your MAGI for both Step Two and Step Three.

This may be an improvement over the prior need to file SSA-44 two years in a row. Recently filed this for 2023 and 2024. Received the reduction back to Jan. 2023. We’ll see if the November 2023 letter has the IRMAA calculation correct from this SSA-44, or if it still looks back to 2022 when income was higher.

2. If you are retiring, get a statement on letterhead from your HR office of your retired status before you leave work and file it away in case you need it for your LCE in a future year.

3. If you are married, make sure to bring a copy of your marriage certificate to the SSA office. They will need proof that the LCE of one or the other spouse should be applied.

Thanks again, and one typo in Step Two: the SSA-44 form screenshot must be from an older version because if references AGI being on Line 7 of the 1040 and you have that in the text also. AGI is on Line 11 for 1040s from 2020 on (so far; it keeps moving around).

I’m wondering why my notice from Social Security Administration with an income between $183,000.01 and $499,999.99 shows part B IRMAA charges of $384.30 while the form SSA-44 has that extra charge as $362.60. Also the charge for part D on the notice is $74.20 and on SSA-44 has the charge as $70.00. I’m filing single as my wife passed 3+ years ago which should make no difference now. The website information is said to be accurate so please explain the difference.

Richard,

Thank you for your question. There’s a simple explanation for this. As of today, the SSA has not updated the Form SSA-44 to reflect the new IRMAA charges. The form version on the SSA website is from 12/2022. The SSA should be releasing a new version of the form relatively soon, which should reflect the updated rates. Once that’s posted, I’ll update this article accordingly.

However, the rates in your notice are correct, according to the Medicare website: https://www.cms.gov/newsroom/fact-sheets/2024-medicare-parts-b-premiums-and-deductibles

My wife inherited 9 shares of no par value common stock from her mother. The company merged with another and the new merged company forced the sale back to them. Hence the sale was out of our control as we had no plans to sell. Received notice that IRMAA was going to raise our Medicare premiums from $174 to $559 per month. Does a force stock sale qualify as a life changing i.e. Loss of property as the shares provide annual income? Should I ask for a new determination based on the forced sale? Have you ever had this before?

Theoretically, it may be possible, but I see a couple of hurdles that you’d have to jump through.

1. This has to be loss of income-generating property. If you can demonstrate that your future income will be significantly lower because of this, then you might have a chance.

But it’s still a long shot, because there are several statements in the SSA operating procedures (known as POMS) that don’t directly address your situation, but don’t really help you, either.

2. From the SSA POMS HI 01120.035 Life Changing Event (LCE) – Loss of Income-Producing Property (https://secure.ssa.gov/poms.nsf/lnx/0601120035):

The loss of income-producing property must not be caused by the beneficiary’s direction. The loss must be caused by circumstances beyond the beneficiary’s control. A loss due to donation, gift, sale or transfer of income-producing property is not considered a loss beyond the beneficiary’s control and does not qualify for a new initial determination using a more recent tax year. Ordinary risk of loss taken at the time of investment in income-producing property is considered at the beneficiary’s direction. Examples of circumstances beyond a beneficiary’s control are losses caused by:

Natural disasters (such as flood, hurricane, tornado, fire, earthquake, volcano eruption)

Disease (affecting crops, livestock or other animals)

Arson

Buy-out of the property by a government under Eminent Domain

Theft (including the taking of money or property by blackmail, burglary, embezzlement, extortion, larceny, robbery, fraud, investment fraud or other criminal activity)

NOTE: Loss of dividend income does not qualify as a loss of income from income producing property unless the loss is due to criminal theft. See HI 01120.005D.

3. POMS HI 0112.005D (https://secure.ssa.gov/poms.nsf/lnx/0601120005#d) states:

Some examples of one-time income that cause an increase and are non-qualifying events (NQEs) include:

Capital gains from the sale of property

Lottery winnings;

Casino winnings;

Conversion of an IRA; or

Cashing bonds.

So the problem that you’re facing is that there doesn’t appear to be clear guidance (publicly available) that supports your case. Which will make it more difficult for someone to process a new determination to your satisfaction. But your best bet may be to try and convince someone that your situation is more like the eminent domain situation, rather than a voluntary sale.

I wish you the best of luck!

Crazy you can’t fax or email a copy in!

Hey Forrest – Thanks for doing this work. Here is my situation:

We are retired (67/68 years old). Our income is fixed at about $150,000.00 annually. Last year (2023) we pulled $190,000.00 out of an IRA to pay off our home. That nearly doubled the “Income” represented on our tax return for the year. Of course, we were presented with an IRMAA increase for 2025. I’ve already completed our 2024 taxes (early) because I actually know our income from all sources (less than $150K). If we don’t meet any of the defined “Life Changing Events” but we can show that our income level is less than required for the IRMAA increase, do you know of any way that we can appeal that decision? Thanks again for any guidance you can provide.

Steve,

Thank you for writing. Unfortunately, I don’t really see a way forward for you, in reducing your IRMAA for the 2025 tax year. However, if your 2024 MAGI is under the threshold as you indicated, then it should come off in the 2026 tax year.

Since SSA-44 isn’t an appeal (it’s a request for a new initial determination based upon SSA-defined life changing events), you could formally appeal this to the SSA. But I feel that you might spend more money and time than you would receive in return.

II experienced a FEMA Declared Natural Disaster to my home on 12/25/22 due to a blizzard, which caused frozen pipers and extensive damage to my home. While Insurance covered a good deal of cost, I took out a large lump sum, $150K, $30K withheld for taxes, from my Traditional IRA/401K to cover out of pocket costs I experienced. I took this lump sum out in 2023. I received a IRMAA letter from SSA in November 2024. Ordinarily, my only retirement income is based on Pension and SSA, so I pay the basic Medicare Premium. This IRMAA I’m being assessed is over $700.00 a month higher for Parts B &D. I cannot afford this hit each month. But for the Natural Disaster damage to my home, I would not have made this withdrawal. I do not understand how to complete SSA Form 44. I submitted Tax Returns for 2020 through 2023, insurance documents, correspondence, canceled checks, invoices from contractors, etc. In Step 2 of SSA Form 44 I put what was my adjusted gross income for the year 2022. I left Step 3 blank, and signed the form. I put all the evidence and a letter to SSA on a CD, as well as a note attached to Form SSA-44 indicating I was not sure how to complete this form, and asked SSA complete it if I id something incorrect. A week later, SSA mails all this back to me with a new SSA-44 to complete, and no instructions what I am supposed to do. I presume I did not complete the form accurately, but I don’t understand how I can do so without having yet done my taxes for the IRMAA Premium year of 2025 based on income from the year 2024. I understood the SSA-44 to indicate you can base your reduction on an earlier year, if you don’t expect any changes for the year 2024, which I do not, except for COLAS. How does one complete SSA-44 under the circumstances of a lump sum withdrawal from Traditional IRA/401K necessitated by extensive damage to a home from a Natural Disaster. I must plead ignorance here. I do not understand SSA-44, nor how to complete it in my case. I would sincerely appreciate any input you have to offer. Thank you.

Pamela,

I hope this will help better understand your IRMAA situation. Your 2025 IRMAA is based upon your 2023 income. Form SSA-44 is used to help the SSA understand whether you experienced 1 of 7 life-changing events (LCEs) that the SSA recognizes as the basis for a new initial determination of your IRMAA (i.e. a new determination based upon information from one of the LCEs that the SSA would not have had).

The 8 LCEs that the SSA recognizes are:

1. Marriage

2. Divorce or annulment

3. Death of spouse

4. Work stoppage (i.e. retirement or involuntary stoppage due to disability)

5. Work reduction

6. Loss of income-producing property (involuntary)

7. Loss of pension

8. Employer settlement payment

These are the only situations that the SSA will reconsider your situation for. I do not think your IRA/401k withdrawal would qualify, but if one of these other events happened during 2023, you could complete Form SSA 44 and still qualify for relief. If not, then I don’t think that filing Form SSA-44 will help you.

Even if you’re not able to reduce or eliminate IRMAA in 2025, it should go down the following year when it’s recalculated based upon your 2024 tax return.

The one question that I have is whether the $700 per month is accurate.

I would strongly recommend scheduling an appointment at your local SSA office to make sure you understand all of your options.

My SSA-44 answer to step #2 is 2023 the same year as my life changing event and the sale of my investment property. But what year should I put to show that this was a one time sale that resulted in the increased income thus negating my retirement income which was social security only? I paid capital gains. Should I put 2022 for step 2 and 2024 for step 3?

You could use 2023 for Step 2 and 2024 for Step 4.

Just an observation: if your life-changing event was the voluntary sale of an investment property, I don’t believe that the SSA will approve this. The SSA considers the loss of income-producing property to be:

“You or your spouse experienced a loss of income-producing property that was not at your direction (e.g. not due to the sale or transfer of the property). This includes:

-Loss of real property in a Presidentially or Gubernatorially-declared disaster area,

-Destruction of livestock or crops due to natural disaster or disease,

-Loss of property due to arson, or

-Loss of investment property due to fraud or theft.

I retired in November 2024 and uploaded on-line in my SSAGov account the SSA44 form for work stoppage as life changing event. I uploaded the form 11 days ago which was successfully done – how long typically will it take to get a response back?

In my experience, it’s taken about 6-8 weeks to expect a response. Whenever you receive the successful determination, it should be retroactively applied to the beginning of the year, and any IRMAA that was taken out should be restored.

I already have Part A and need to use CMS-40B to sign up for Part B. Should I submit an SA-44 with the CMS-40B, or wait until I get the IRMAA letter to submit the SA-44?

You should probably wait to get the IRMAA letter before submitting the SSA-44.

I retired fully in 01/2022. Did not ever work while receiving social security. Can filing the SSA-44 help lower my Part B premium and retro pay back on the 5+ years?

If your Part B is already at the base level, then no. The SSA-44 is only to reduce or prevent the IRMAA surcharge that happens for higher-income taxpayers. And it won’t help you claw back benefits retroactively over the past 5 years.