5 Reasons Why You Don’t Need a Financial Advisor

Sometimes, when trying to figure out whether to hire a financial advisor, people will ask,

“Why do I need to hire an investment advisor to help me with this? I don’t need someone to tell me what to do with my own money!”

That’s a valid question, and one worth looking at.

Contents

The truth about financial planning

The truth is that everyone should incorporate financial planning into their lives. But not everyone needs to hire someone for financial advice or to help them make important financial decisions.

Interestingly, I’ve met many financial planning clients who are truly capable of doing every bit of the work that I used to do for them. But instead of questioning the value of our relationship, they would appreciate the fact that their finances were not something they ever needed to worry about.

They saw our financial planning fee and the time that we invest in our meetings as a very low price for the ability to spend a lot of time doing the things they want to do.

How do I know if I need to hire a financial advisor?

If you’re still researching the financial planning field, you might be trying to figure out whether it’s worth hiring a financial adviser. Certainly, there is a wide range of service offerings to choose from.

Instead of writing an article trying to convince everyone to find a qualified financial advisor, I figured I’d write an article to a different audience.

This audience is filled with people who feel like they’re well enough on their own, but are trying to figure out what they’re missing by not hiring a good financial advisor.

Ironically, those people might not be actually missing anything. They might be doing just well enough on their own. And no advisor, regardless of how good they are, will be able to add value to their client’s life if the client perceives there is no value to add.

Before we discuss reasons NOT to hire a financial advisor, it’s important to recognize the difference between mediocre advisors and great advisors. And we should outline some of the things that great advisors do.

What do great financial advisors do?

True financial professionals don’t spend entire meetings talking about the stock market. The professional advisors don’t peddle expensive life insurance policies or other financial products.

Fiduciary Standard

You’ve probably heard a lot about the fiduciary standard. Real financial advisors don’t spend a lot of time online talking about their fiduciary oath. Why?

Because they’re busy serving clients. Certainly, they take the fiduciary standard to heart. But they don’t need to go about town beating their chest about being a fiduciary financial advisor.

Because they’re naturally serving their client’s best interests. And when that happens, the client doesn’t have to worry about conflicts of interest.

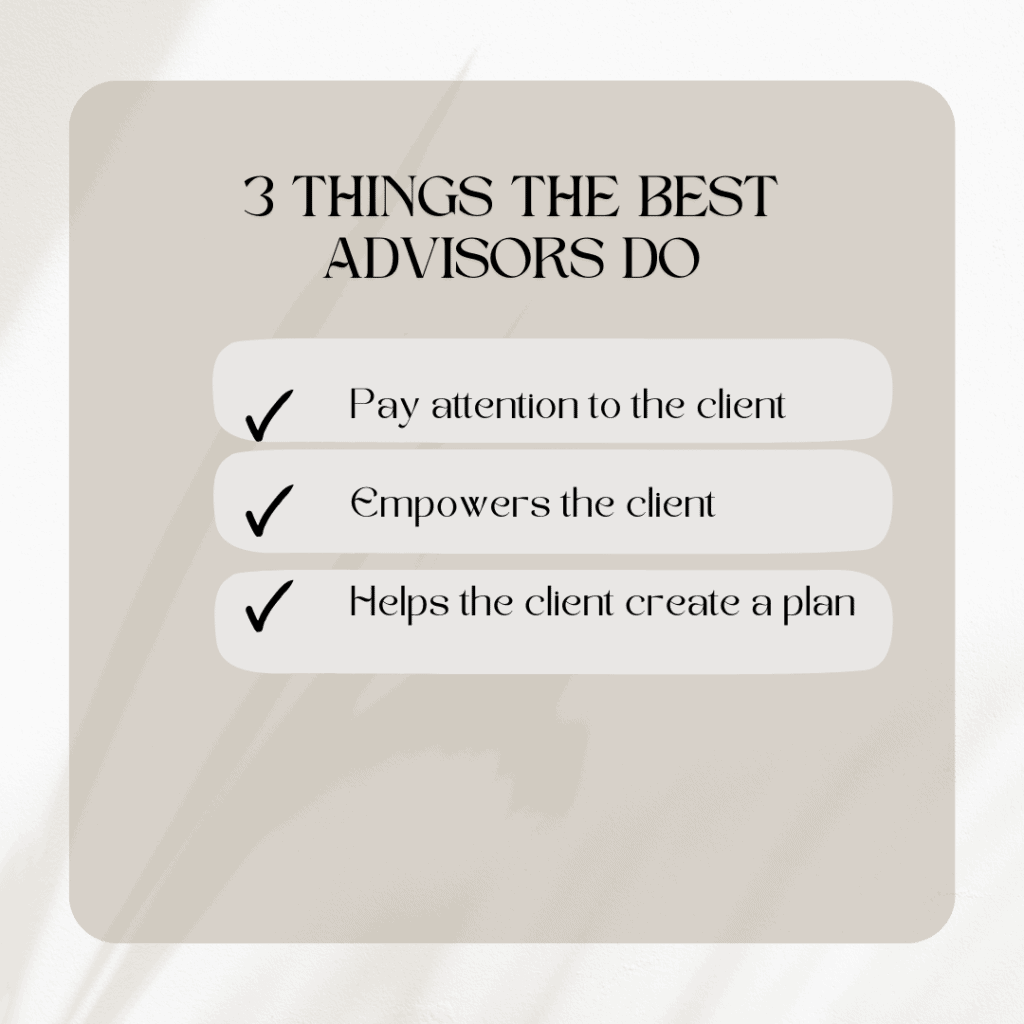

What the best financial advisors do

The best advisors do what all clients appreciate. They make their financial services about the client’s needs.

The right financial advisor:

- Pays attention to the client’s immediate financial needs

- Helps the client feel in control over major financial decisions

- Has a comprehensive plan to address all areas of the client’s financial situation.

In order to successfully do this, a financial advisor needs to have comprehensive knowledge of all areas in the world of personal finance. And the most comprehensive certification in this area is the Certified Financial Planner designation.

What is a Certified Financial Planner?

A lot of financial advisors say that they have education and broad areas of expertise in the financial planning field. A Certified Financial Planner (CFP) is someone who has actually demonstrated both. In order to become a CFP, an advisor must have a formal education in the following areas of study:

- Financial planning principles

- Risk & insurance planning

- Retirement planning

- Tax planning

- Investment planning & wealth management

- Estate planning

Not only does a CFP have to demonstrate their financial planning knowledge and expertise, but they have to continue to undergo financial education. The CFP Board requires a CFP to complete 30 hours of education every two years.

Now we understand what great advisors do. But there is more than one way that financial advisors help their clients. Before deciding that you don’t need an advisor at all, let’s take a look at how they work.

How financial advisors work

There are several different business models in the advisory world. But they can be broken down into 3 different categories.

Commission-based advisors

These are advisors who help individual investors select from a range of mutual funds or insurance products. In turn, their compensation consists of a commission from the sale of these products.

There are many advisors who decry the commission-based advisory model. And certainly, there are a lot of financial consultants who do bad things. These bad actors give the entire industry a bad name.

But there are several facts worth mentioning:

1. The commission-based advisory world is the best-known way for a new advisor to get started.

Many financial advisors are career-changers. Retired military, former teachers, executives, etc. Financial advisors can literally come from any other career.

And up until about 10 years ago, there was virtually no real way for these advisors to learn how to operate an independent financial advisory practice. Even as recently as 25 years ago, there really wasn’t a business model that didn’t use commissions as part of the advisor’s compensation.

With the advent of XY Planning Network, the Alliance of Comprehensive Planners, and Military Financial Advisors Association, there are more resources available for aspiring fee-only planners. But most people will still get their training through the broker-dealer world.

2. Commissions virtually run the insurance industry.

It’s virtually impossible to buy an insurance policy without paying a commission. Unless you buy the policy directly from the insurance carrier. Then, they simply keep the commission that would have gone to an insurance agent.

And a fee-only advisor cannot, by definition, be the person who helps you implement the recommended insurance policy.

There are a lot of people looking into how to make commission-free term life insurance policies. But the way life insurance is bought and sold has compelled many advisors to get an insurance license just so their clients don’t have to shop around on their own.

Fee-based (or fee and commission) advisors

These are advisors who charge a financial planning fee and charge a commission for certain investment or insurance products.

Many of these advisors fall into one of two camps:

1. I only charge a commission for the term life insurance policies my clients buy.

As mentioned previously, there literally isn’t a way for an advisor to directly have their client buy a life insurance policy without having a license and collecting a commission.

I’ve known many advisors who do a great job. They charge a reasonable fee. And they only collect a commission when their client buys a reasonable, term life insurance policy. Their commission is less than 5% of their overall income, but they cannot call themselves ‘fee-only.’

2. I charge a fee to build a comprehensive financial plan. Then I collect a commission for each product I sell to you under the plan.

This is allowed. And sometimes it might be the right thing, especially for someone with relatively simple investment accounts.

To do the opposite, charging high fees while declaring yourself a fee-only, holistic financial planner, can be even more dangerous. But let’s look at the fee-only advisory model.

Fee-only advisors

According to the CFP Board, an advisor can only call themselves fee-only if they do not affiliate with any company that charges a commission.

Most fee-only advisors operate under one of three business models:

Hourly rate model

This might be what most people think of when they want to hire a financial planner. The most common group of advisors who charge an hourly model is the Garrett Planning Network.

This is great in situations when the clients’ needs are relatively simple. But it’s a hard way for an advisor to make a living, because most hourly advisors have to continue marketing themselves.

Almost like a broker or insurance agent looking for their next sale. So many Garrett planners offer to manage their clients’ assets.

Charge a percentage of assets under management

The majority of fee-only financial planners charge their clients a fee as calculated by a percentage of their assets under management.

For example, let’s imagine your wealth manager is managing $1 million in your retirement accounts, and their fee is 1% per year. Your fee would be $10,000 per year.

Most advisors are able to justify their fee not because they do such a great job at investment management, but because they provide holistic financial planning. In other words, they expect their client to come to them with any problem that has to do with money.

And a client’s wealth does represent their complexity. To a point.

A 1% fee might be reasonable for clients whose accounts are $1 million or less. Or $2 million. But probably not $10 million.

At some point, the primary difference is executing trades. And it’s certainly not worth paying twice the money.

That’s why most advisors have a sliding scale on their AUM fees. You can always ask for this schedule, or look it up on their disclosure form (known as a Form ADV). This brings us to the last type of advisor.

Charge a flat fee

This is one of the more recent compensation models, and it can be done in several ways.

Charge a flat fee for a comprehensive plan.

This is something that most hourly planners do. They’ll estimate the number of hours it might take to build a comprehensive financial plan, and make that their fee.

Nothing wrong with this, but then it’s up to you to implement it. Or hire them to do so. And it’s hard to tell the difference between the fee-only advisor doing this or the broker dealer who’s using this as a lead to sell you products.

Charge a monthly ‘retainer’ fee.

This is what most XY Planning Network planners do. Nothing wrong with this model, either.

But many people who subscribe to this model wake up one day, looking to cut expenses. They look at their monthly retainer fee and decide to ‘cut their expense.’

But if they’ve only gone through a portion of the financial planning, or they haven’t implemented all the recommendations, then the client might be doing themselves more harm than good.

Charge a flat annual fee.

Many planners are starting to use this model. It allows a client to see exactly what they’re paying for their expected service. And they agree to the fee.

Or they don’t. But it’s transparent, and the client gets to make an informed decision either way.

How to tell the difference:

Ask them. Any advisor has to honestly answer any questions about their compensation.

Fee-only planners will proudly declare that they only charge a fee. They serve their fiduciary duty by not hiding any of their compensation behind commissions.

People who receive commissions will tell you that they do receive commissions. The real advisors will tell you under what conditions they receive a commission (like to implement an insurance policy). And if the majority of their compensation is fees, they’ll tell you that too.

But if you feel awkward talking about that, then you can ask, “Who regulates you?”

If they sell insurance

Insurance agents are regulated by their state’s insurance commissioner’s office.

If they sell investment products

A broker-dealer representative is regulated by FINRA, the Financial Industry Regulatory Authority.

If they do not sell products

They are regulated by their state’s board of financial regulation (not the same as the insurance agents), or by the SEC.

If they charge a combination of commission & fees

Then they are regulated by each of the offices they would fall under. For example, a fee-based advisor with an insurance license would be subject to regulation by their state’s investment advisory office and insurance regulator.

But let’s take a look at situations where you might not need a financial planner at all. Here are 5 possible reasons.

Reason #1: You have a strong passion and interest for managing your own finances.

Some people LOVE doing things themselves. Everyone has that neighbor who could hire a lawn service. But that neighbor spends so much time on their lawn and their landscaping that it’s hard to imagine a company doing a better job.

That neighbor who keeps track of everything on a calendar:

- When to mulch

- When to spread fertilizer

- When to spread pesticide

- When to change the watering cycle between seasons

Then there’s the rest of us. Most people are so focused on everything else that’s going on in our lives, that it feels like we’re barely treading water.

There’s the financial equivalent to that, albeit less obvious to the neighbors. There’s the person who has a spreadsheet for everything.

This would include their spending, their savings goals, the amount of money they need for retirement, etc.

And with free consumer-oriented software like Mint, you don’t even need to be a spreadsheet genius to do this. You just need to have the time and energy to stay on top of things. Consistently.

Reason #2: You have the time and energy to stay on top of your financial planning needs.

Funny thing about that lawn-oriented neighbor. They have the same 24 hours in a day as everyone else. But they MAKE the time to spend on their lawn.

That neighbor’s enthusiasm means that no matter what happens, their lawn is a priority in their life.

I like digging in the dirt (not really, but let’s pretend that I do). I like keeping a nice lawn. But every weekend? I’ve got a teenage son who’s perfectly capable of pushing a lawn mower.

Plus, we live about 30 minutes from the beach. On a nice day, we’d rather take the family there. Oh, and we have Boy Scouts, swim meets, and everything else that fills in our time.

Bottom line is this: Regardless of whatever else is going on in your life either financial planning floats to the top of your to-do list, or it doesn’t.

If financial planning is something you carve time out of your busy scheduled to do, then you might not need a financial advisor now.

But when you feel things starting to slip, and those financial tasks start getting pushed further and further out, then you might want to look at hiring someone.

Reason #3: You love managing your own investments and doing your own investment research.

Either you love this or you don’t. While this seems very similar to #1, it is slightly different. You can love balancing your credit card statement every month and dread the thought of managing investments.

Perhaps you’re great at socking away money, but don’t know what to do with it. The point is, you can manage your day-to-day finances to the penny and still find value in a relationship with a good investment adviser.

But, if you find yourself comparison shopping for the lowest-cost index funds, or you take your teenage son to the annual Bogleheads conference to share your passion for investing, you might not need a financial advisor. In fact, you might have fundamental differences in investment strategy which would actually be counter-productive to a good advisor-client relationship.

An advisor-client relationship works best when:

- The advisor is very clear in their investment philosophy, and

- The client understands, and agrees with the investment philosophy

If you think that you’ll spend more time questioning why the advisor picked XYZ fund instead of ABC fund, then you probably don’t need an advisor. Moreover, that advisor doesn’t need you as a client second-guessing their job.

Especially if you don’t mind doing ALL the work yourself.

Reason #4: You like paperwork.

It’s easy to overlook all the paperwork and reading that’s involved in managing your own finances.

For example, when you’re discussing the intricacies of a back door Roth IRA conversion, or evaluating the things you can do to tighten up your estate plan, you can read a million articles.

But to actually do ANY of these things usually requires delving into the tedious details. Paperwork. Phone calls. Sitting on hold, waiting for someone from the insurance/investment company to pick up.

Thinking of all the different estate planning aspects of your life. Then hiring an attorney to actually write out your estate planning documents. All of these are things that take time, and admittedly for most people, slip through the cracks.

If you never miss a deadline and can remain on point with all the minutiae, then you might not need a financial advisor to help you keep on task.

Reason #5: If something happens to you, all the important people in your life are fully prepared to do things EXACTLY the way you would.

One time, I went to a prospective client’s house. To his credit, he meticulously maintained his finances in every way outlined above. While I probably could have helped with a couple of tax strategies, the advice I would’ve given him really wouldn’t have had much impact on his net worth.

When it came to his estate plan, he told me that he had that covered too. Then he proceeded to pull out a thick white binder and told me that if he got hit by a bus, all his wife would have to do is ‘break glass,’ and follow the instructions.

While he might not have needed a financial advisor, the mortified look on his wife’s face told me all I needed to know. She’ll need an advisor one day, and she’ll probably be on her own to find the right one. Because she’s currently married to the only one her husband will ever have.

Conversely, I had a client who very efficiently and effectively managed his family’s finances his entire life. When he developed terminal cancer, he hired me to help ensure that when he was gone, someone was looking out for his wife’s best interests.

My client recognized that while she was grieving, his wife might need someone to help her manage all the things that he used to do on his own. He might not have needed a financial advisor either, but he was a little more in tune with his wife’s uncertainties than the first guy.

Just because you’re sure that you’ve got all the bases covered, you can’t assume that your loved ones feel the same way. Perhaps they don’t have the confidence you have.

Perhaps they don’t have the same interest you do. Maybe they want to hire someone to take care of all the details so they can enjoy the things they love.

But, if everyone in your family is comfortable in knowing that they only need to ‘break glass’ and follow the instructions, then perhaps you don’t need to hire a financial advisor.

Conclusion

Not everyone needs to work with a financial advisor to achieve their financial goals. While financial planning is very important, it’s perfectly possible for people to do this themselves.

All it takes is the time, energy, education, passion, diligence and dedication to do a lot of the work yourself.