IRS Form 8379 Instructions

Perhaps you were expecting a big tax refund when you received a notice of offset indicating that the Department of Treasury is using your federal tax refund to pay your spouse’s debt. If this is the case, you can file IRS Form 8379 to ask the Internal Revenue Service for injured spouse relief and to receive your share of a joint tax refund.

In this article, we’ll cover what you need to know about IRS Form 8379, including:

- How to complete and file IRS Form 8379

- How injured spouse allocation works

- Frequently asked questions

Let’s start with discussing going through this tax form, step by step.

Table of contents

How do I complete IRS Form 8379?

There are 4 parts to this two page tax form:

- Part I: Should you file this form?

- Part II: Information About the Joint Return for Which This Form Is Filed

- Part III: Allocation Between Spouses of Items on the Joint Return

- Part IV: Signature

Let’s go through each part, one at a time, starting with Part I.

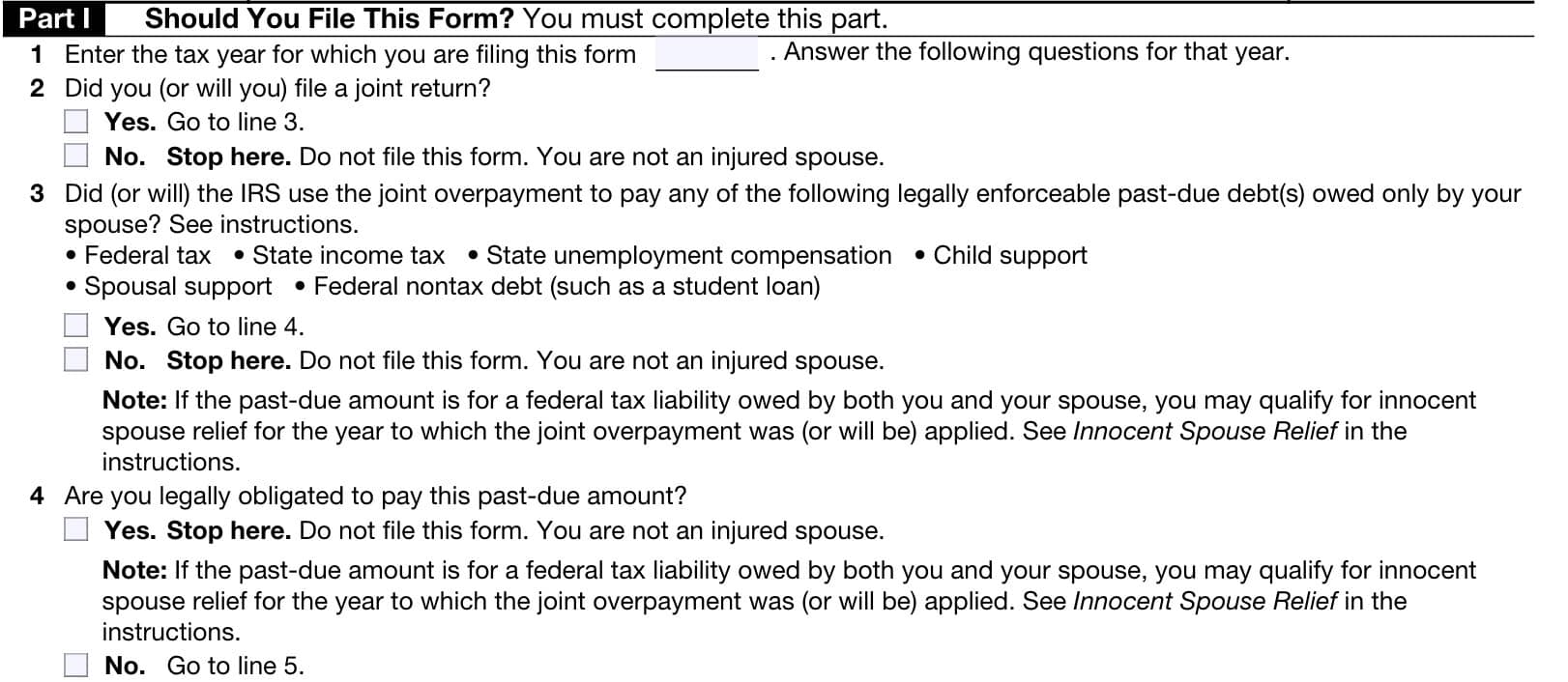

Part I: Should you file this form?

There are 9 questions in the first part of the form. Each question will help determine whether you are an injured spouse, and walk you through relief options for your specific situation.

Line 1: Tax year for the tax return

Enter the tax year for the income tax return for which you are claiming injured spouse status.

Line 2: Is this a joint return?

If this is not a joint tax return, then the IRS does not consider you to be an injured spouse.

Line 3: Did the IRS use the joint overpayment to pay certain debts?

There are certain types of debt that are eligible for the Treasury Offset Program, administered by the U.S. Treasury Department’s Bureau of the Fiscal Service. These debts include:

- Past-due federal tax

- State taxes, such as state income tax

- State unemployment compensation debts

- Child support payments

- Spousal support to a former spouse

- Federal non-tax debt, such as student loans

If your share of a federal tax refund was garnished to pay these types of debt, then you can move forward with your injured spouse claim.

If ‘No,’ then stop here. You are not an injured spouse.

Line 4: Are you legally obligated to pay this debt?

If you answered ‘Yes,’ then you technically are not an injured spouse. An injured spouse is not legally obligated to pay their spouse’s past due debt.

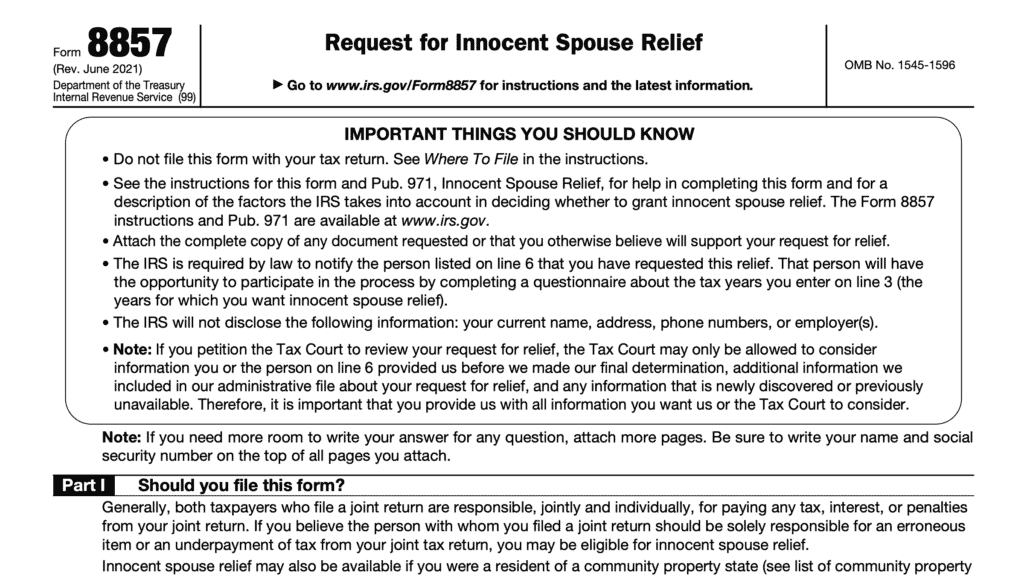

However, if you are a negatively impacted spouse and unaware of your spouse’s actions, you may qualify for innocent spouse relief, which is covered in a separate section of the Internal Revenue Code.

Innocent spouse relief

Generally, both spouses are responsible for paying the full amount of tax, interest, and penalties due related to your joint return. However, if you qualify for innocent spouse relief, you may be relieved of part or all of the joint tax liability.

You may qualify for relief from the joint tax liability if any of the following apply.

- There is an understatement of tax because your spouse omitted income or claimed false deductions or credits, and you didn’t know or have reason to know of the understatement.

- There is an understatement of tax and you are divorced, separated, or no longer living with your spouse.

- Given all the facts and circumstances, it wouldn’t be fair to hold you liable for the tax.

Taxpayers who believe they are eligible for innocent spouse relief should complete IRS Form 8857 instead of the injured spouse allocation form.

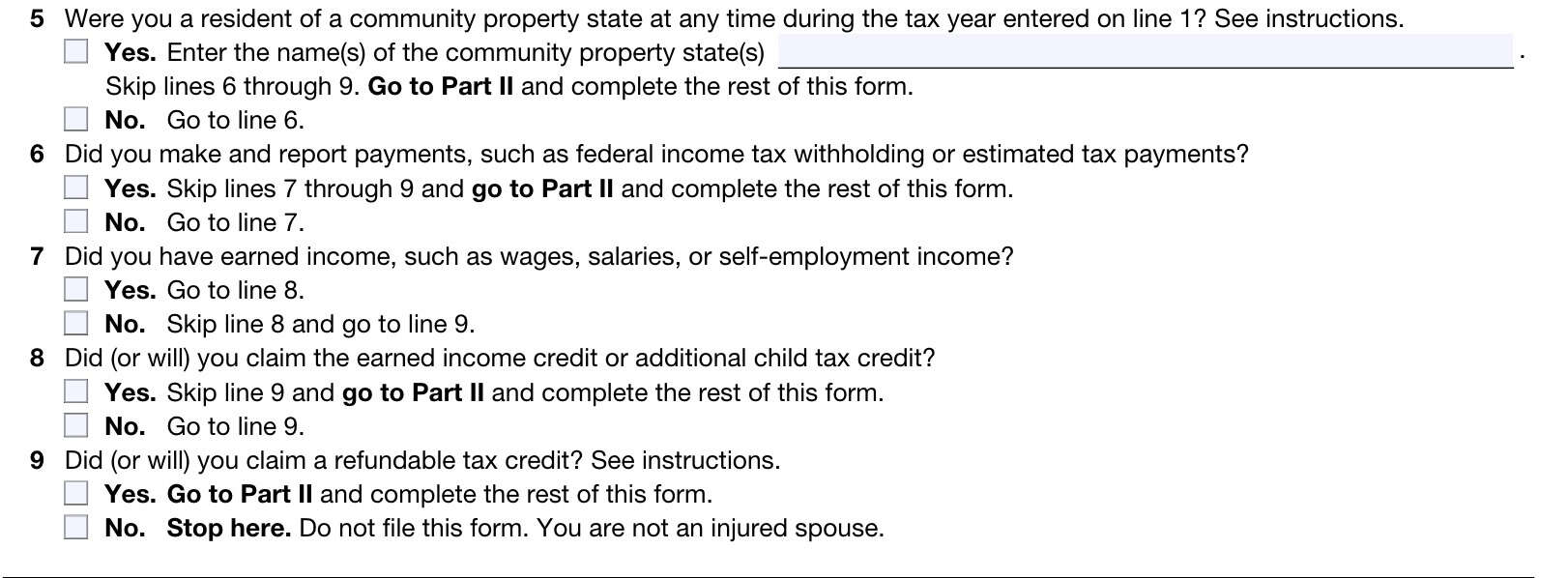

Line 5: Were you a resident of a community property state during the tax year?

Answer ‘Yes’ or ‘No.’ If ‘Yes,’ enter the state name here.

Community property states may have different rules that apply to the calculation of injured spouse relief.

IRS Publication 555 contains more information about the tax impacts of community property states. However, the IRS has created several revenue rulings, which may provide different details, depending on the state community property law where you live.

Revenue rulings for community property states

| If you live in the following community property state… | Then use the following IRS Revenue Ruling |

| Arizona or Wisconsin | Rev. Rul. 2004-71, available at: IRS.gov/IRB/2004-30_IRB#RR-2004-71 |

| California, Idaho, or Louisiana | Rev. Rul. 2004-72, available at: IRS.gov/IRB/2004-30_IRB#RR-2004-72 |

| Nevada, New Mexico, or Washington | Rev. Rul. 2004-73, available at: IRS.gov/IRB/2004-30_IRB#RR-2004-73 |

| Texas | Rev. Rul. 2004-74, available at: IRS.gov/IRB/2004-30_IRB#RR-2004-74 |

Line 6: Did you make or report federal income tax payments, including estimated tax payments?

If ‘Yes,’ skip Lines 7-9 and proceed to Part II.

Line 7: Did you have earned income, such as wages, salaries, or self-employment income?

If you answered, ‘No,’ skip Line 8 and go to Line 9.

Line 8: Did you claim the earned income credit or additional child tax credit?

If ‘Yes,’ skip Line 9 and go to Part II.

Line 9: Will you claim a refundable tax credit this year?

Refundable tax credits include:

- American opportunity credit, claimed on IRS Form 8863, Education Credits

- For tax years 2009 and later

- Credit for federal tax paid on fuels

- Refundable prior year alternative minimum tax

- Premium tax credit

- 2014 and later years

If you answer ‘No,’ then you are not considered an injured spouse. If ‘Yes,’ then let’s go to Part II.

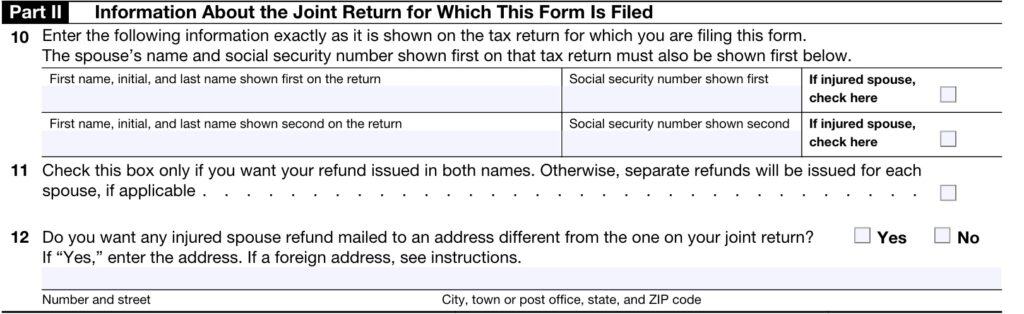

Part II: Information about the joint return

Part II requests information about the joint return in question.

Line 10: Taxpayer information

Line 10 should contain the complete name and Social Security number for both spouses, according to the jointly filed tax return. The injured spouse will check the appropriate box next to his or her name.

Line 11: Refund box

Check this box only if you want the the injured spouse’s share of a tax refund issued in both spouse’s names. Otherwise, leave it blank.

Line 12: Different address

If you want your refund mailed to the address on your tax return, check ‘No.’ If you want a different address, check ‘Yes’ and fill in the new address.

If this is a permanent change of address, you should file IRS Form 8822, Change of Address, to accompany your Form 8379. If this is a temporary change of address, you don’t need to complete Form 8822, but there may be a delay in the processing of your form.

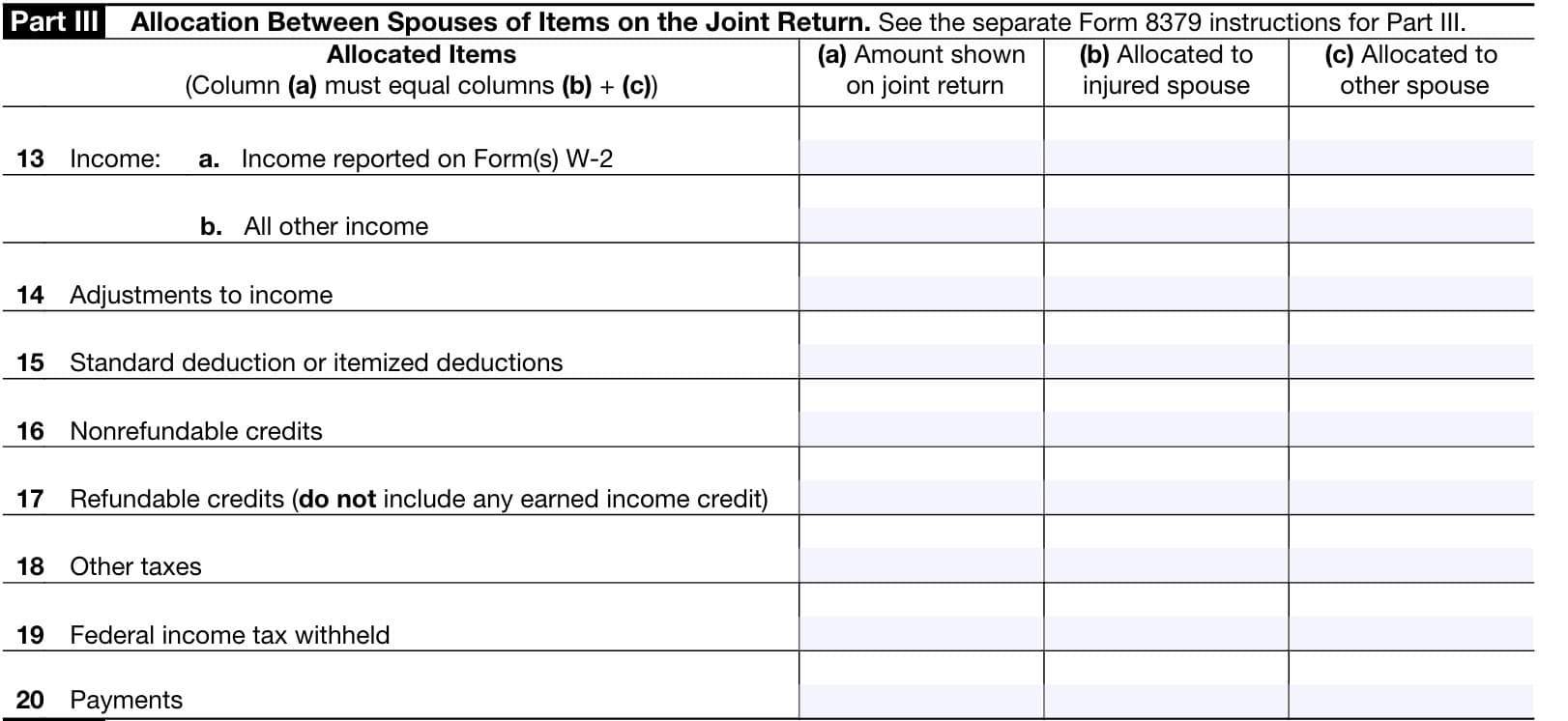

Part III: Allocation between spouses

If you’re working with a tax professional, you may want that person to complete Part III on your behalf. If you are completing this by yourself, you’ll need to separate each of these line items for each spouse.

In essence, you’re treating this as if you and your spouse are filing separate income tax returns. From there, the IRS will determine your injured spouse allocation.

How Columns (a) through (c) work

In Column (a) for each line, you’ll need to report the number as it appears on your tax return.

In Column (b), you’ll report your share (injured spouse’s share). Column (c), should contain the other spouse’s share of the refund.

As indicated on the form, both columns (b) and (c) must add up to column (a).

Line 13a: Income

On Line 13a, include any wage income that you included on your tax return. You should find this on Line 1 of IRS Form 1040.

In Columns (b) and (c), enter the amount of wage income reported to each spouse on IRS Form W-2.

Line 13b: All other income

In Column (a), include all other income reported on your tax return. You’ll need to identify the type and amount of income.

You’ll find these on Lines 1b through 9 of your Form 1040 or Form 1040-SR. You should also see these income items on Schedule 1, lines 1 through 10.

For Columns (b) and (c), you’ll need to allocate all income shown on your tax return. Allocate any joint income, such as interest income earned on your joint bank account and reported on IRS Form 1099-INT, as you wish.

Line 14: Adjustments to income

Include the adjustments to income from your tax return. You should find these on Line 10 of your Form 1040, or on Lines 11 through 26 of Schedule 1.

In Columns (b) and (c), allocate each adjustment to the spouse who would have claimed it if a separate return had been filed.

For example, allocate the IRA deduction to the spouse who owns the IRA and allocate the student loan interest deduction to the spouse who is legally obligated to make the interest payments.

If there are any adjustments that don’t belong exclusively to one spouse, you may allocate them as you determine.

Line 15: Deductions

Enter the total deduction amount in column (a). You’ll find this in Line 12(c) of your 1040.

If you took the standard deduction

In columns (b) and (c), you’ll enter 1/2 of the total deduction in each column.

Basic Standard Deduction Amounts

For 2025, the basic standard deduction amount for a married couple filing a joint tax return was $31,500. For 2026, this amount is $32,200.

If someone can claim you as a dependent

If someone could claim you or your spouse as a dependent, your basic standard deduction is the amount on line 4c of the Standard Deduction Worksheet for Dependents. You can find this worksheet in the Form 1040 or Form 1040-SR instructions.

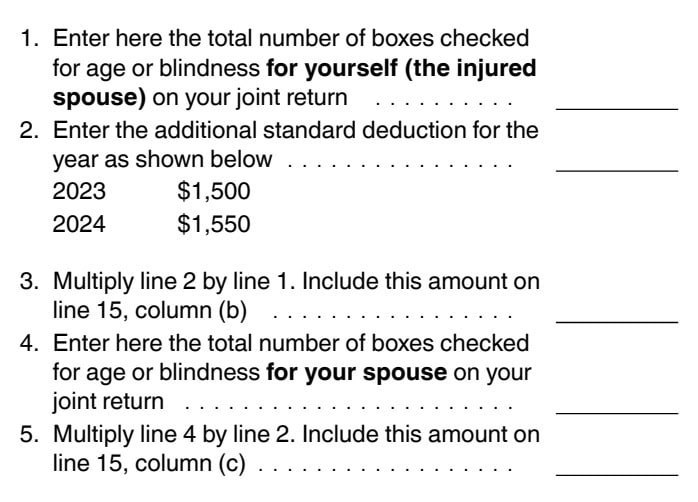

If you checked any boxes for age or blindness on your tax return

If you checked any boxes for age or blindness on your joint return, use the following worksheet to allocate the additional standard deduction. The additional standard deduction is the difference between the total standard deduction and the basic standard deduction.

If you itemized deductions

If you itemized tax deductions on Schedule A, you’ll need to allocate each deduction (such as medical expenses) to the spouse entitled to that deduction.

Line 16: Nonrefundable credits

You’ll find these on Line 19 of your tax return and in Part I of Schedule 3.

For columns (b) and (c) you’ll allocate any credits attributable to a dependent to the spouse who would have claimed that credit in a separate return. These credits may include:

- Child tax credit or credit for other dependents, as calculated on Schedule 8812

- Child and dependent care credit, calculated on IRS Form 2441

- Education credits, as determined on IRS Form 8863

Do not include earned income credit here, as the IRS will determine each spouse’s allocation.

Line 17: Refundable credits (not including earned income credit)

You’ll find these on Line 28-30 of your tax return and in Part II of Schedule 3.

For columns (b) and (c) allocate any credits attributable to a dependent of the spouse who would have claimed that credit in a separate return. Allocate business credits based upon each spouse’s interest in that business. Allocate other tax credits as you see fit.

Do not include earned income credit here, as the IRS will determine each spouse’s allocation.

Line 18: Other taxes

You can find these in Schedule 2 of your original tax return.

In Columns (b) and (c), allocate self-employment tax to the spouse who earned the self-employment income.

Excess advance premium tax credit

Allocate the excess advance premium tax credit repayment in any way you determine.

Net investment income tax

Allocate the net investment income tax, calculated on IRS Form 8960, consistently with the allocation used for net investment income on Line 13b.

Line 19: Federal income tax withheld

This will be found on Line 25d of your original tax return.

In Columns (b) and (c), enter federal income tax withholding for each spouse’s income as shown on any of the following:

- IRS Form W-2, Wage and Tax Statement

- IRS Form W-2G, Certain Gambling Winnings

- IRS Form 1099 series tax forms

Also include any excess Social Security or Tier 1 Railroad Retirement (RRTA) tax, or Additional Medicare Tax withholding from IRS Form 8959, Line 24, attributable to each spouse.

Line 20: Payments

You’ll find additional payments on Line 26 of your tax return.

In Columns (b) and (c), you can allocate joint estimated tax payments in any way you choose as long as both you and your spouse agree.

If you can’t agree on how to allocate tax payments, the estimated tax payments will be allocated according to each spouse’s separate tax liability as a percentage of the overall tax bill.

For example, John & Mary Smith have made $10,000 in total payments. They have concluded that the tax bill should be broken down as follows:

- John: 60%

- Mary: 40%

Unless they agree on a different allocation, $6,000 should be credited to John’s column, while Mary’s column should reflect $4,000.

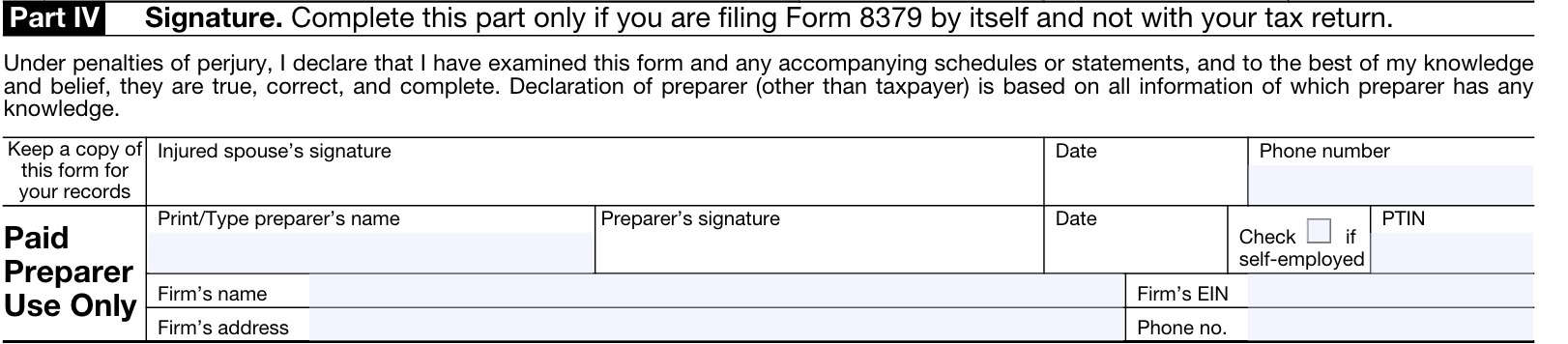

Part IV: Signature

Part IV is simply the signature section. Only the injured spouse needs to sign this form. If you’re working with a paid tax preparer, that tax professional will input their information as well.

If you are filing IRS Form 8379 as part of your income tax return, then you do not need to complete Part IV.

Avoiding common mistakes

Below are some common mistakes taxpayers make when filing IRS Form 8379 and how to avoid them.

Filing separately from tax return

Taxpayers do not need to file IRS Form 8379 with their income tax return. However, if you file Form 8379 separately, don’t include a copy of your original joint return. Do include copies of the following for each spouse:

- Forms W-2 and W-2G

- 1099 forms showing income tax withheld

Not properly marking your return

If you file Form 8379 with your joint return or amended joint return, enter “Injured Spouse” in the upper left corner of page 1 of your joint return.

Not properly allocating tax items to each spouse

Items of income, expenses, credits, and deductions must be allocated to the spouse who would have entered the item on his or her separate return.

Filing for the wrong kind of debt

Make sure your spouse’s debts are subject to offset.

For example, the following legally enforceable debts may be eligible:

- Federal tax

- State income tax

- Child support

- State unemployment compensation debts

- Student loan debt

For more information on tax refund offsets, check out our guide!

Video walkthrough

Watch this instructional video to learn more about Form 8379 and injured spouse allocation.

Are you tired of dreading tax season?

If you’re like most people, you push through the stress of filing, only to be hit with a bigger bill than expected—then put it all behind you until the same cycle repeats next year.

But what if you could change the game?

Tax planning puts you in control. It’s about being proactive, not reactive—taking small, smart steps throughout the year to reduce your tax burden, increase your savings, and keep more of your hard-earned money working for you.

Here’s what effective tax planning helps you do:

✅ Avoid the surprise of a high tax bill

✅ Understand how your income and decisions affect your taxes

✅ Strategically lower your tax liability over time

Ready to make smarter tax moves?

👉 Join my free weekly tax planning newsletter and get one actionable tip every week to help you reduce your taxes legally and effectively.

Start taking control—your future self will thank you.

Frequently asked questions

If you filed a joint income tax return, and you are not responsible for your spouse’s debt, then the IRS considers you to be an injured spouse. As an injured spouse, you can request your portion of the refund back from the IRS, by using IRS Form 8379.

IRS Form 8379, Injured Spouse Allocation, helps the IRS understand how much of a joint couple’s tax liability should be used to pay one spouse’s past-due debt. The other spouse, or the injured spouse, may file Form 8379 to claim the refund amount that is owed to him or her.

You may file IRS Form 8379 either with your original tax return or separately. If filing after you’ve submitted your tax return, you may submit the completed form to the Internal Revenue Service Center where you turned in your tax return. If filing with an amended return or after electronically submitting your tax return, you may submit the form to the IRS center where you live.

No. A taxpayer must use IRS Form 8857 to request innocent spouse relief.

The IRS grants innocent spouse relief to one spouse to prevent that spouse from having to pay additional income tax due to tax return errors caused by the other spouse. Injured spouse allocation allows a spouse to claim money taken from his or her tax refund to pay the other spouse’s debt.

Where can I get a copy of IRS Form 8379?

You can obtain a free download from the IRS website or by clicking the file below.

Related tax forms

This tax form is one of the fillable tax forms provided by the Internal Revenue Service, to help taxpayers reduce their tax preparation costs. To see more forms like this, visit our free fillable tax forms page, where you’ll also find articles like this.

Unlike the IRS, our articles contain step by step instructions for each tax form, as well as video walkthroughs. You can also check out all of our videos by subscribing to our YouTube channel!

Where do I put on the 1040 SR form the $12,000 deduction promised as part of “The One Big Beautiful Bill deduction” ?

f;jksn@yahoo.com

First, you’ll need to complete Schedule 1-A, Additional Deductions (see links below). Use Part V to calculate the Enhanced Deduction for Seniors, based on MAGI limitations, then report the total of all additional OBBBA deductions on Line 13b of your Form 1040 or Form 1040-SR.

IRS Schedule 1-A, Additional Deductions

Article: https://www.teachmepersonalfinance.com/irs-schedule-1-a-instructions

Video: https://youtu.be/1iwv1RsvP58