IRS Form 4562 Instructions

One of the best opportunities for small business owners to lower their tax burden is by claiming depreciation and amortization expenses on their annual tax return. The Internal Revenue Service allows people to claim deductions on IRS Form 4562, Depreciation and Amortization.

In this in-depth article, we’ll walk through how to complete this tax form, as well as some of the concepts behind this tax subject. Let’s start by walking through the form, step by step.

Table of contents

How do I complete IRS Form 4562?

There are 5 parts to this two page tax form:

- Part I: Election To Expense Property Under Section 179

- Part II: Special Depreciation Allowance and Other Depreciation

- Part III: MACRS Depreciation

- Part IV: Summary

- Part V: Listed Property

Let’s begin at the top with Part I.

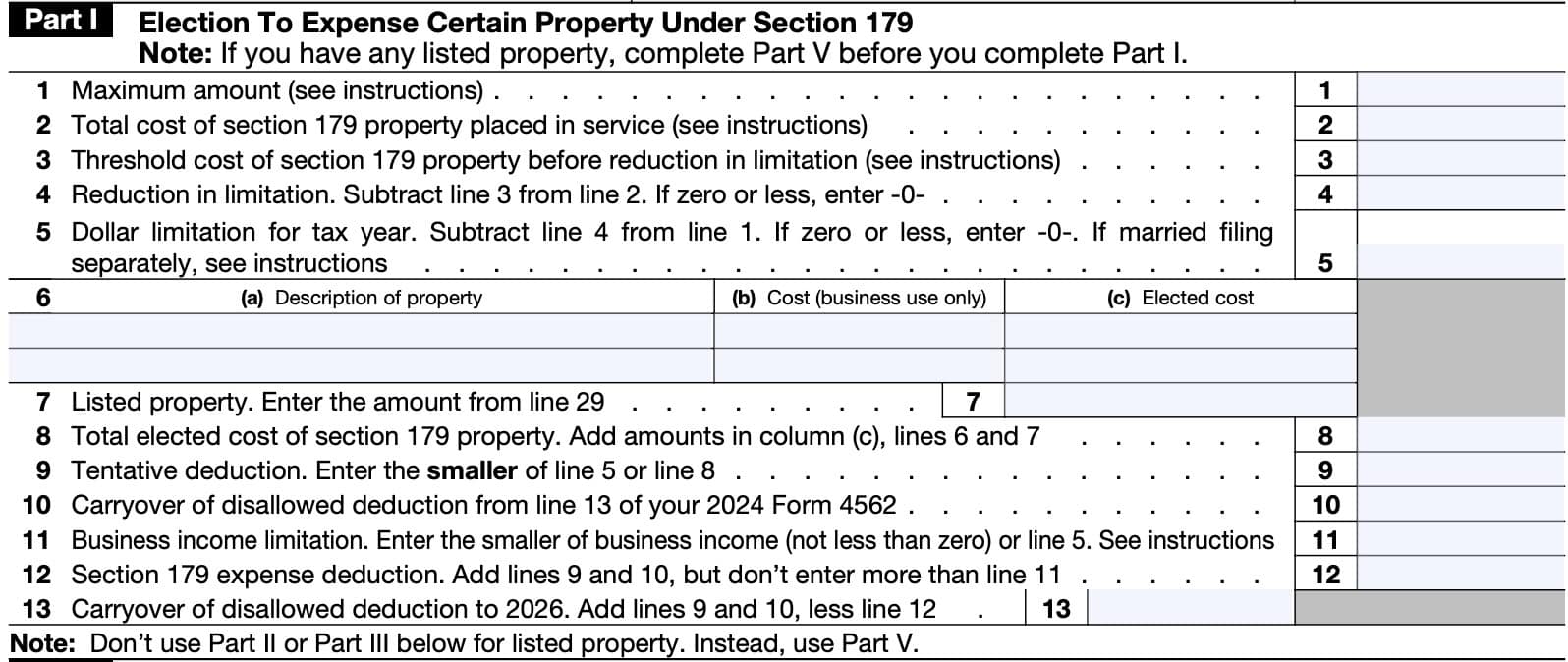

Part I: Election to expense certain property under Section 179

In Part I, we’ll calculate the amount of Section 179 depreciation you may take in the given tax year. If you are taking a deprecation deduction for listed property, you must complete Part V before starting Part I.

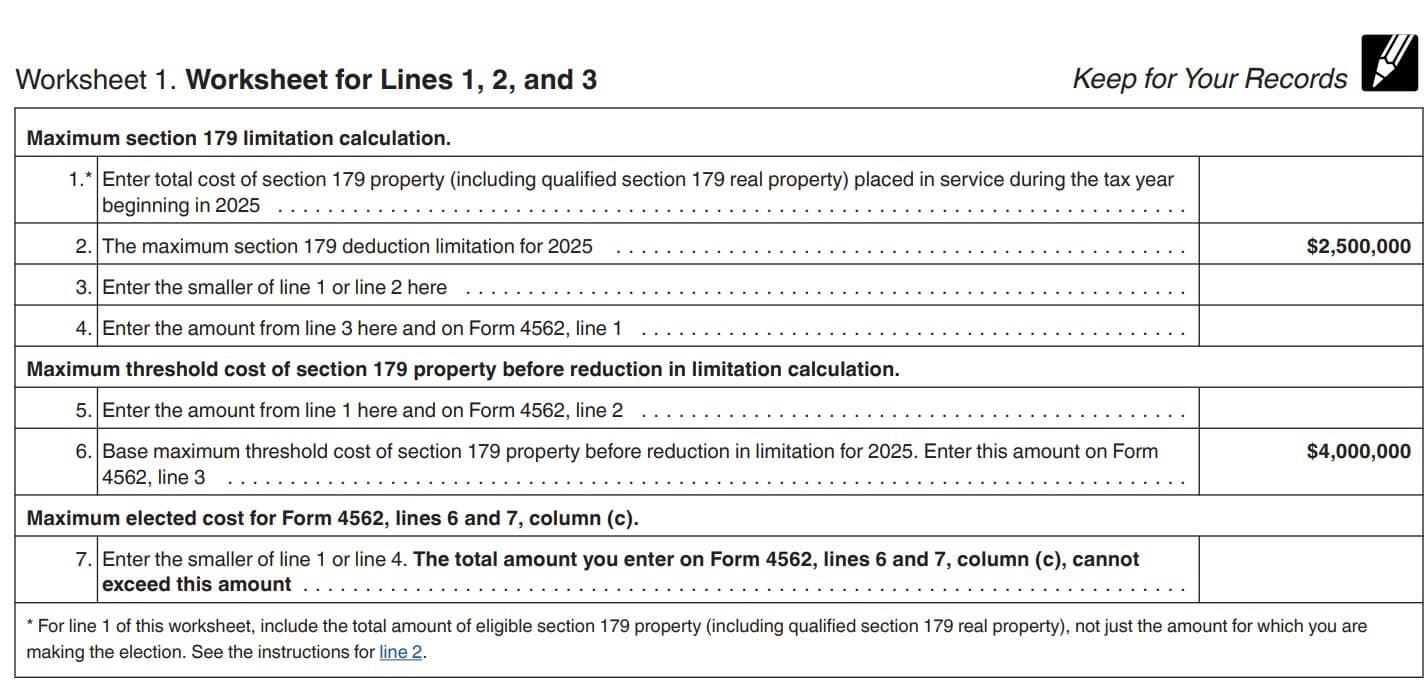

Line 1: Maximum amount

If you are expensing any Section 179 property placed into service, you may need to use the following worksheet to calculate the amounts for Lines 1, 2, and 3.

This is the maximum Section 179 expense deduction that you can take for property placed in service in a given tax year. For tax years 2025 and later, the maximum amount is $2,500,000.

According to the worksheet, you will enter the smaller of the following in Line 1:

- The total cost of Section 179 property placed into service during the tax year

- This includes all eligible business and investment property, not just property for which you are electing to expense

- $2,500,000

Recapture rule

If the Section 179 is not predominantly used (meaning used more than 50% of the time) for your trade or business at any time before the end of the property’s recovery period, the tax benefit you claimed as a Section 179 expense deduction must be reported as “other income” on your tax return. This includes qualified Section 179 disaster assistance property that ceases to be used in the applicable federally declared disaster area in any year after you claimed the Section 179 expense deduction for that property.

Line 2: Total cost of Section 179 property placed in service

This is the actual cost of all Section 179 property placed into service. This includes:

- All eligible property, including qualified real property

- Any listed property from Part V

- Property placed into service by your spouse, even if you are filing a separate tax return

- Includes qualified Section 179 real property that your spouse elected to treat as Section 179 property

Line 3: Threshold cost of Section 179 property before reduction in limitation

For expensing Section 179 property, there is a threshold amount of property that a taxpayer may put into service before limitations apply.

For 2024, this amount is $4,000,000. Enter this amount in Line 2.

For a partnership, these limitations apply to the partnership and each partner. For an S corporation, these limitations apply to the S corporation and each shareholder. In a controlled group, all component members are treated as one taxpayer.

Line 4: reduction in limitation

Subtract Line 3 from Line 2. If the result is zero or a negative number, enter ‘0.’

Line 5: Dollar limitation for tax year

If this results in zero or a negative number, enter ‘0.’ You cannot expense any Section 179 property, Skip Lines 6 through 11, enter ‘0’ on Line 12, then enter the carryover from previously disallowed deductions in Line 13.

For married taxpayers filing separately, both spouses must allocate the dollar limitation for the tax year. To do this, each spouse should multiply the total limitation by the percentage allocated to each spouse.

The default allocation for each spouse is 50%, unless you agree to elect a different allocation. The sum of percentages allocated to both spouses must equal 100%.

Line 6

In Line 6, enter the elected Section 179 cost for each item of property (except for listed property, which you should list in Column (i) of Line 26).

For each item that you list, you’ll need to enter the following information from the corresponding column:

- Column (a)-Description of property: Enter a brief description of the property you elected to expense

- Column (b)-Cost: Enter the cost of the property.

- If you acquired the property via trade-in, do not include the carryover basis. Only include the excess of the cost over the value of the property

- Column (c)-Elected cost: This is the amount that you elect to expense

If you are reporting Section 179 expense deduction from a partnership or S-corporation, enter one of the following across Columns (a) and (b):

- Partnership: From Schedule K-1 (Form 1065)

- S-Corporation: From Schedule K-1 (Form 1120-S)

Line 7: Listed property

Enter the total amount that you expensed for listed property on Line 29.

Line 8: Total elected cost of Section 179 property

Add the column (c) totals for Line 6 and Line 7. Enter the sum here.

Line 9: tentative deduction

In Line 9, enter the smaller of:

Line 10: Carryover of disallowed deduction from Previous year

If applicable, enter the amount from Line 13 of the previous year’s Form 4562. This represents the carryover of any disallowed deduction for Section 179 property that was not allowed because of the business income limitation.

If you filed IRS Form 4562 for 2024, enter the amount from Line 13 of your 2024 Form 4562.

Line 11: Business income limitation

Your Section 179 expense deduction is limited to the taxable income from actively conducting a trade or business during the year. This means that you have to have meaningful participation in managing the business or business operations.

For individuals

Enter the smaller of:

- Line 5

- Total taxable income from trade or business, without regard to the following:

- Section 179 expense

- Tax deduction for 1/2 of self-employment taxes under Section 164(f), or

- Net operating loss deduction

In calculating total taxable income, include all wages, salaries, tips, and other compensation earned as an employee. Do not reduce this amount by unreimbursed employee business expenses.

For married couples filing a joint tax return, combine the total taxable incomes for both spouses.

For partnerships

Enter the smaller of:

- Line 5

- Partnership’s total items of income and expense from any trade or business actively conducted, except for any of the following:

- Tax credits

- Tax-exempt income

- Section 179 expense deduction

- Guaranteed payments

For S-corporations

Enter the smaller of:

- Line 5

- Corporation’s total items of income and expense from any trade or business actively conducted, except for the following:

- Net operating loss deduction

- Section 179 expense deduction

- Special deductions

For Corporations other than S-corporations

Enter the smaller of:

- Line 5

- Corporation’s total items of income and expense from any trade or business actively conducted, before the following:

- Net operating loss deduction

- Section 179 expense deduction

- Special deductions

Line 12: Section 179 expense deduction

Add Line 9 and Line 10. However, do not enter any amount that exceeds the number in Line 11.

If you have more than one business or activity, you may allocate your allowable Section 179 expense deduction among your business. To do this, perform the following steps:

- Enter “Summary” at the Part I of the separate Form 4562 you are completing for the total amounts for all business activities. Leave the rest of the form blank

- On Line 12 of the Form 4562 of each separate business or activity, enter the amount allocated to that business or activity from the “Summary”

- No other entry is required in Part I of the separate Form 4562 for each business or activity

Line 13: Carryover of disallowed deduction

If the total of Line 9 and Line 10 is greater than Line 12, this means that part of your deduction is disallowed in the current tax year. However, you may enter the difference in Line 13 for carryover to the next year.

Add Lines 9 & 10, then subtract Line 12. Enter the result here.

Part II: Special depreciation allowance and other depreciation

Part II contains special depreciation allowances for property depreciated under certain methods. Do not use Part II for listed property.

Line 14: Special depreciation allowance for qualified property placed in service during the tax year

In Line 14, you may be able to take an additional special depreciation allowance for certain qualified property placed into service in the given tax year. This special allowance only applies for the first year that the property is in service. This allowance is after Section 179 expense deduction, but before calculating regular depreciation.

Qualified property includes the following:

- Certain items acquired after January 20, 2025

- Certain items acquired after September 27, 2017

- Certain plants bearing fruits and nuts planted or grafted after January 19, 2025

- Certain plants bearing fruits and nuts planted or grafted before January 20, 2025

- Qualified reuse and recycling property

- Qualified production property

Below is more detailed information on how to calculate the special depreciation allowance for each category of qualified property. Do not include listed property.

Certain items acquired after January 19, 2025

Certain qualified property (defined below) acquired after January 19, 2025, is eligible for a 100% special depreciation allowance.

However, you can elect to take a 40% special depreciation allowance for certain qualified property (60% for property with a long production period and certain aircraft), instead of the 100% special depreciation allowance in the first tax year ending after January 19, 2025.

Qualified property is:

- Tangible property depreciated under MACRS with a recovery period of 20 years or less;

- Computer software defined in and depreciated under IRC Section 167(f)(1);

- Water utility property (see 25-year property, later); and

- Qualified film, television, and live theatrical productions, as defined in IRC Sections 181(d) and (e). Qualified sound recording productions, as defined in section 181(f), that commence in tax years ending after July 4, 2025.

Qualified property can be either new property or certain used property.

Certain qualified property acquired after September 27, 2017 and before January 20, 2025

Certain qualified property (defined below) acquired after September 27, 2017, and placed in service

after December 31, 2023, and before January 20, 2025 (other than property with a long production period and certain aircraft), is limited to a special depreciation allowance of 60% of the depreciable basis of the property.

This includes the following:

- Tangible property depreciated under MACRS with a recovery period of 20 years or less

- Computer software depreciated under Internal Revenue Code Section 167(f)(1)

- Water utility property

- Qualified film, television, and live theatrical productions, as defined in IRC Section 181(d) and (e)

Property with a long production period and certain aircraft acquired after September 27, 2017, and placed in service before January 1, 2025, is eligible for a special depreciation allowance of 80% of the depreciable basis of the property.

The special depreciation allowance for certain qualified property (other than certain long production period property and certain aircraft) placed in service after December 31, 2024, and before January 1, 2026, is limited to 40% of the depreciable basis of the property.

Property with a long production period and certain aircraft placed in service after December 31, 2024, and before January 1, 2026, is limited to a special depreciation allowance of 60% of the depreciable basis of the property.

Certain plants bearing fruits and nuts planted or grafted After January 19, 2025

You can elect to claim a 100% special depreciation allowance for the adjusted basis of certain specified plants (defined later) bearing fruits and nuts planted or grafted after January 19, 2025.

Specified plant defined

A specified plant is:

- Any tree or vine that bears fruits or nuts, and

- Any other plant that will have more than one yield of fruits or nuts and generally has a preproductive period of more than 2 years from planting or grafting to the time it begins bearing fruits or nuts.

Any property planted or grafted outside the United States does not qualify as a specified plant.

If you elect to claim the special depreciation allowance for any specified plant, the special depreciation allowance applies only for the tax year in which the plant is planted or grafted. The plant will not be treated as qualified property eligible for the special depreciation allowance in the subsequent tax year in which it is placed in service.

To make the election, attach a statement to your timely filed return (including extensions) for the tax year in which you plant or graft the specified plant(s) indicating you are electing to apply IRC Section 168(k)(5) and identifying the specified plant(s) for which you are making the election. Once made, the election cannot be revoked without IRS consent.

For the first tax year ending after January 19, 2025, you can elect to take a 40% special depreciation allowance (instead of 100%) for certain specified plants planted or grafted after January 19, 2025.

Certain plants bearing fruits and nuts planted or grafted Before January 20, 2025

You can elect to claim a 40% special depreciation allowance for the adjusted basis of certain specified plants (defined later) bearing fruits and nuts planted or grafted after December 31, 2024, and before January 20, 2025.

Specified plant defined

A specified plant is:

- Any tree or vine that bears fruits or nuts, and

- Any other plant that will have more than one yield of fruits or nuts and generally has a preproductive period of more than 2 years from planting or grafting to the time it begins bearing fruits or nuts.

Any property planted or grafted outside the United States does not qualify as a specified plant.

If you elect to claim the special depreciation allowance for any specified plant, the special depreciation allowance applies only for the tax year in which the plant is planted or grafted. The plant will not be treated as qualified property eligible for the special depreciation allowance in the subsequent tax year in which it is placed in service.

Qualified reuse and recycling property

Certain qualified reuse and recycling property placed in service after August 31, 2008, is eligible for a 50% special depreciation allowance.

Qualified reuse and recycling property includes any machinery and equipment (not including buildings or real estate), along with any appurtenance, that is used exclusively to collect, distribute, or recycle qualified reuse and recyclable materials.

This includes software necessary to operate such equipment. See IRC Section 168(m)(3) for more information.

Qualified reuse and recycling property must also meet all of the following tests:

- The property must be depreciated under MACRS.

- The property must have a useful life of at least 5 years.

- You must have acquired the property by purchase after August 31, 2008. If a binding contract to acquire the property existed before September 1, 2008, the property does not qualify.

- The property must be placed in service after August 31, 2008.

- The original use of the property must begin with you after August 31, 2008.

- For self-constructed property, special rules apply. under IRC Section 168(m)(2)(C)

Qualified reuse and recycling property does not include rolling stock or other equipment used to transport reuse and recyclable materials or any property to which Section 168(g) or (k) applies.

Qualified production property

For certain qualified production property (as defined in IRC Section 168(n)(2)) placed in service after July 4, 2025, and before January 1, 2031, you can elect to claim a 100% special depreciation allowance.

Exceptions

Qualified property does not include:

- Listed property used 50% or less in a qualified business use (as defined in the instructions for Lines 26 and 27);

- Any property required to be depreciated under the Alternative Depreciation System (ADS)

- Not property for which you elected to use ADS

- Property placed in service, or planted or grafted, as applicable, and disposed of in the same tax year;

- Property converted from business or income-producing use to personal use in the same tax year it is acquired;

- Property described in section 168(k)(9)(A) or 168(k)(9)(B); or

- Property for which you elected not to claim any special depreciation allowance

Line 15: Property Subject to Section 168(f)(1) Election

In Line 15, enter the depreciation for property that you depreciate under the unit-of-production method, or another method not based on years.

You will need to attach a separate sheet that includes:

- A description of the property

- The depreciation method that you used, which excludes the property from MACRS or ACRS

- Depreciable basis

Line 16: Other depreciation

In Line 16, enter the total depreciation you’re claiming for the following types of property, except for listed property and property subject to Section 168(f)(1) election. This might include the following:

- ACRS property (pre-1987 rules).

- ACRS stands for accelerated cost recovery system. IRS Publication 534, Depreciating Property Placed Into Service Before 1987, contains more details

- Property placed into service before 1981

- Certain public utility property that doesn’t meet certain normalization requirements

- Certain property acquired from related persons

- Property acquried in certain nonrecognition transactions

- Certain audio recordings, movies, and vides

- Property depreciated under the income forecast method

- Limited to motion picture films, video tapes, sound recordings, copyrights, books, and patents

If any of these apply, it’s a good idea to refer to the Line 16 instructions for more detail.

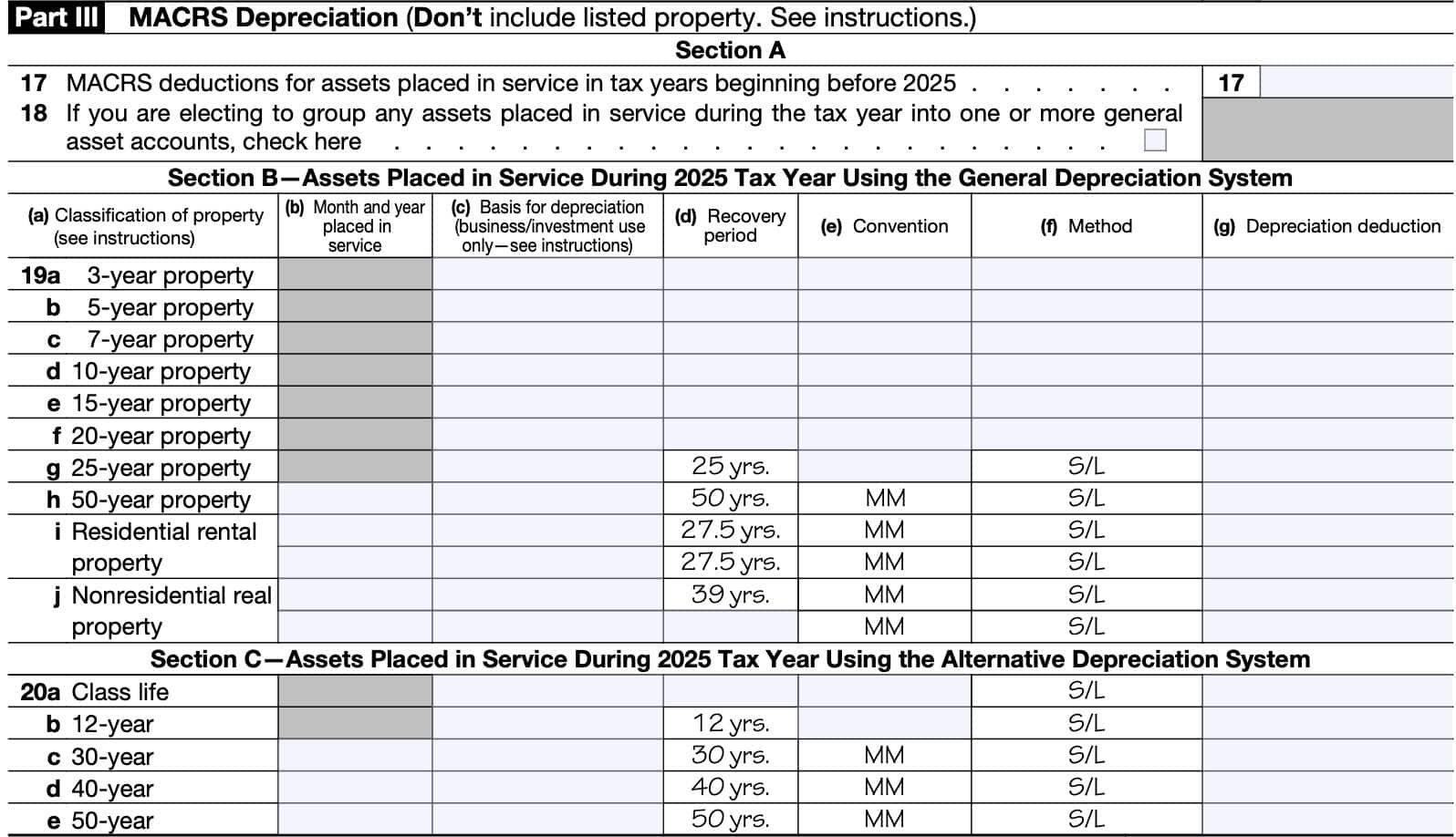

Part III: MACRS depreciation

In Part III, you’ll calculate the depreciation allowance for property under MACRS. MACRS stands for Modified Accelerated Cost Recovery System, and is generally used to depreciate tangible property placed into service after 1986. Property depreciated under the MACRS method is often referred to as a MACRS asset.

MACRS depreciation includes both the General Depreciation System (GDS) and the Alternative Depreciation System (ADS).

IRS Publication 946, How to Depreciate Property, contains exceptions and additional details.

Line 17: MACRS deductions for assets paced in service before current tax year

In Line 17, you’ll enter the current year tax deductions for MACRS assets placed into service in a previous tax year. You can calculate these deductions by using the same methods outlined in Line 19.

Line 18

Check this box if you wish to group assets into one or more general asset accounts. Assets in a general asset account are depreciated as if they were a single asset.

Each general asset account can only contain assets that:

- You placed into service during the same tax year

- You depreciate using the same

- Depreciation method

- Recovery period

- Convention

- Are not considered personal use and business use items

To see all applicable rules for general asset accounts, please see the Line 18 instructions.

Line 19: Assets placed in service during the tax year using the general depreciation system

Use Line 19 for new assets that:

- You placed into service during the tax year

- You depreciate under the general depreciation system

- Are not listed property

Follow the specific instructions for each classification of property, as outlined below. Refer to IRS Publication 946 if you do not know the classification of a particular property.

Line 19 is broken down into the following:

- Line 19a: 3-year property

- Line 19b: 5-year property

- Line 19c: 7-year property

- Line 19d: 10-year property

- Line 19e: 15-year property

- Line 19f: 20-year property

- Line 19g: 25-year property

- Line 19h: 50-year property

- Line 19i: Residential rental property

- Line 19j: Nonresidential rental property

Enter the following information for each classification of property, as applicable:

Column (b): Month & year placed in service

For real property placed into service during the tax year, enter the month and year that you placed the property into service. For personal use property that you converted into business property, treat the property as if it were placed into service on the conversion date.

Column (c): Basis for depreciation

To calculate your basis for depreciation, you’ll need to multiply the cost or other basis of the property by the percentage of business or investment use.

From there, subtract any credits or deductions otherwise allocable to the property. This may include, but is not limited to:

- Section 179 expense deduction

- Deduction under Section 179D for certain energy efficient commercial building property

- Deduction for removal of barriers to the disabled and the elderly

- Disabled access credit

- Enhanced oil recovery credit

- Credit for alternative fuel vehicle refueling property

- Credit for employer-provided childcare facilities and services

- Any special depreciation allowance included on Line 14

- Any basis adjustment for investment credit property.

- See IRC Section 50(c).

- Any basis adjustment for advanced manufacturing investment credit property.

Column (d): Recovery period

Unless otherwise indicated in the form, the recovery period for each type of property corresponds to the classification of property.

| Classification | Recovery period |

| 3-year property | 3 years |

| 5-year property | 5 years |

| 7-year property | 7 years |

| 10-year property | 10 years |

| 15-year property | 15 years |

| 20-year property | 20 years |

| 50-year property | 50 years |

Column (e): Convention

There are three types of allowable conventions, depending on the type of property and when you placed it into service.

Half-year convention

The half-year convention applies to all property reported on Lines 19a through 19g, unless the mid-quarter convention applies.

The half-year convention does not apply to:

- Residential real property

- Nonresidential real property

- Railroad gradings & tunnel bores

To apply the half-year convention, enter ‘HY‘ in column (e).

Mid-quarter convention

If the total depreciable bases of MACRS property placed into service in the last 3 months of the tax year exceeds 40% of the total depreciable bases for MACRS property placed into service for the entire tax year, use the mid-quarter convention.

When determining whether the mid-quarter convention applies, do not use the following:

- Property that is being depreciated under a method other than MACRS.

- Any residential rental property, nonresidential real property, or railroad gradings and tunnel bores.

- Property that is placed in service and disposed of within the same tax year.

Annotate mid-quarter convention by entering ‘MQ‘ in column (e).

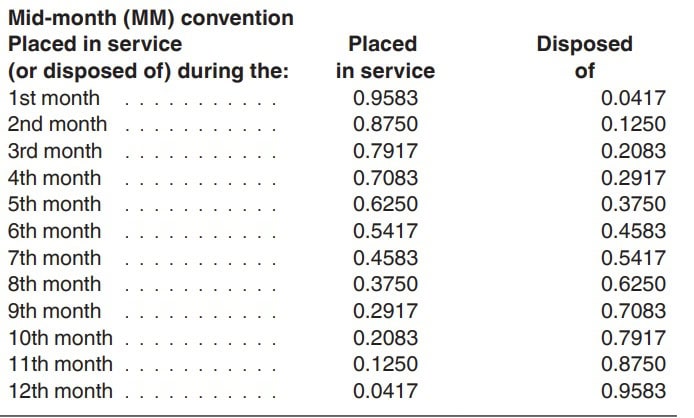

Mid-month convention

This only applies to residential rental property, nonresidential real property, railroad gradings, and tunnel bores. Use ‘MM’ in column (e) to annotate use of the mid-month convention.

Column (f): Method

Where applicable, you may use the straight line method for all property within a specific classification placed into service during the tax year. This is an irrevocable election. To use straight-line, annotate ‘S/L‘ in column (f) for the specific line.

In certain instances, you may also use one of the following methods:

- 200% declining balance: Annotated by entering 200 DB in column (f)

- 150% declining balance: Annotated by entering 150 DB in column (f)

The IRS instructions contain additional information about the proper use of declining balance methods.

Column (g): Depreciation deduction

Enter the dollar amount of the total depreciation deduction for each classification of property. You may need to use tables located in the IRS form instructions or IRS Publication 946 to perform these calculations.

Line 20: Assets Placed In Service During The Tax Year Using The alternative Depreciation System

For Line 20, you’ll calculate depreciation for assets placed into service during the tax year and depreciated under ADS. Do not include automobiles or other listed property.

You must use ADS to depreciate the following types of property:

- Tangible property used predominantly outside the United States

- Tax-exempt use property

- Tax-exempt bond financed property

- Imported property covered by a Presidential executive order

- Property used predominantly in a farming business and placed in service during any tax year in which you made an election under Section 263A(d)(3) to not have the uniform capitalization rules of Section 263A apply.

- Any nonresidential real property, residential rental property, or qualified improvement property held by an electing real property trade or business

- As defined in IRC Section 163(j)(7)(B)

- Any property that has a recovery period of 10 years or more under Section 168(c) that is held by an electing farming business

- As defined in IRC Section 163(j)(7)(C)

Part IV: Summary

In Part IV, you’ll total the depreciation amounts from:

Once totaled, you’ll enter the expense deduction on the appropriate line of your income tax return.

Line 21: Listed property

Enter the amount from Line 28, below.

Line 22: Total

Add the amounts from the following lines:

- Line 12 (except for partnerships and S corporations)

- Line 14

- Line 15

- Line 16

- Line 17

- Line 19: Column (g)

- Line 20: Column (g)

- Line 21

Enter the total here and on the appropriate line of your federal income tax return.

For partnerships & S corporations: Do not include Section 179 amounts on this line. Section 179 expense deductions are passed through separately to partners and shareholders on Schedule K-1.

Line 23: Portion of the basis attributable to Section 263A costs

If you are subject to uniform capitalization rules, enter the increase in basis from costs that you must capitalize. Refer to Treasury Regulations Section 1.263A-1 for more details.

Part V: Listed property

In Part V, you’ll calculate the depreciation expense for listed property. However, there are a few notes for guidance.

For taxpayers claiming the standard mileage rate, actual vehicle expenses (including depreciation) or depreciation on other listed property, you must provide the information listed in Part V. This is true regardless of the year that you place the property in service.

If you file IRS Form 2106 to claim employee business expenses, then use that form instead of Part V. Also, if you file Schedule C on your Form 1040, you may report vehicle information in Part IV of Schedule C if the following apply:

- You are claiming the standard mileage rate or actual vehicle expenses excluding depreciation,

- You are not otherwise required to file Form 4562

There are 3 sections to Part V:

- Section A: Depreciation and Other Information (Lines 25 through 29)

- Section B: Information on Use of Vehicles (Lines 30 through 36)

- Section C: Questions for Employers Who Provide Vehicles for Use by Employees (Lines 37 through 41)

If you are using the standard mileage rate or deducting lease expense, you only need to complete Line 24, columns (a) through (c) for Section A, Section B, and Section C, if applicable.

Line 24

For Line 24a, check whether you have evidence to support your claim of business or investment use for the asset you are claiming a deduction for.

In Line 24b, check ‘Yes’ if this is written evidence.

Line 25: Special depreciation allowance for qualified listed property

You may be able to deduct the special depreciation allowance for certain qualified listed property that you placed into service during the tax year. This includes certain property that you acquired after September 27, 2017, and placed into service before January 1, 2027.

See the IRS form instructions for additional detail on calculating this special depreciation allowance.

Enter the total in column (h).

Line 26: Property used more than 50% in a qualified business use

For Line 26, you’ll calculate the depreciation for property used more than 50% for qualified business use. For property used less than 50% for qualified business use, go to Line 27.

For each item, you’ll need to list the following information:

Column (a): Type of property

This includes the following assets, in order:

- Automobiles or other vehicles

- Other listed property

For automobiles, list the makes and models of each vehicle. For others, give a general description. If you have more than 5 vehicles used exclusively for business/investment purposes, you may group them by tax year. Otherwise, list each vehicle separately.

Column (b): Date placed in service

Enter the date that you placed the asset in service. If converting from personal use, treat the property as a business asset on the date of conversion.

Column (c): Business or investment use percentage

Enter the percentage of business or investment use.

For vehicles, you can determine this by dividing the number of miles driven for business purposes by the total number of miles the vehicle is driven for all purposes.

For other listed property, allocate use based upon the most appropriate unit of time that the property is actually used, not just available for use.

If you would like more information, refer to the form instructions.

Column (d): Cost or other basis

Enter the property’s actual cost or other basis, including sales tax. For vehicles, reduce your basis by any qualified electric vehicle credit that you previously claimed, or any alternative motor vehicle credit allowed.

If converting from personal use, the basis is the smaller of:

- The property’s adjusted basis

- Fair market value (FMV) on the date of conversion

Column (e): Basis for depreciation

Multiply column (c) by column (d). From this result, subtract the following:

- Section 179 expense deduction

- Special appreciation allowance

- Credits for employer-provided childcare facilities and services

- 50% of any investment credit taken for property placed into service before 1986

- For vehicles and other listed property placed in service after 1985, reduce the depreciable basis by the entire investment credit.

Column (f): Recovery period

For property placed in service after 1986 and used more than 50% in a qualified business use, follow the instructions for Line 19, column (d).

For property placed in service after 1986 and used less than 50% in a qualified business use, follow the straight line method over its ADS recovery period. The ADS recovery period is 5 years for automobiles and computers.

Column (g): Method/convention

Enter the method and convention used, following the guidance outlined for Line 19, columns (e) and (f).

Column (h): Depreciation deduction

For vehicles, see the limits for passenger automobiles in the IRS form instructions. You may need to use limitation tables outlined in the form instructions based upon the following:

- Type of vehicle

- Number of years in service

- Date placed in service

For property used more than 50% in a qualified business use and placed in service after 1986, figure column (h) by following the instructions for Line 19, column (g). If placed in service before 1987, multiply column (e) by the applicable percentage given in Publication 534 for ACRS property.

If the recovery period for an automobile ended before your tax year beginning in 2022, enter your unrecovered basis, if any, in column (h).

Column (i): Elected Section 179 cost

Enter the amount you elected to expense under Section 179. For vehicles, refer to the form instructions for restrictions that may apply.

Line 27: Property used Less than 50% in a qualified business use

For Line 27, follow the instructions for Line 26. However, calculate the depreciation deduction in Column (h) by multiplying column (e) by column (f), instead of following the instructions for Line 19.

Line 28

Add all column (h) amounts from Lines 25 through 27. Enter on here, and on Line 21.

Line 29

Add the amounts in column (i) from Line 26. Enter here and on Line 7.

Line 30

Lines 30 through 36 are used for calculating vehicle use. You must complete this for each vehicle that you are claiming a depreciation expense for.

If you provided vehicles to your employees, answer the questions in Section C (starting with Line 37) before answering Line 30. Employers do not need to complete Lines 30 through 36 for vehicles:

- Used by employees who are not more than 5% owners or related persons, and

- For which you answered ‘Yes’ to any question on Lines 37 through 41

In Line 30, enter the total business or investment miles driven during the year. Do not include commuting miles.

Line 31

Enter the total number of commuting miles driven during the year.

Line 32

Enter the total number of miles that you drove for personal use during the year.

Line 33

Add Lines 30 through 32. This should represent the total miles driven.

Line 34: Was the vehicle available for personal use during off-duty hours?

Answer Yes or No.

Line 35: Was the vehicle primarily used by a 5% owner or related person?

Answer Yes or No.

Line 36: is another vehicle available for personal use?

Answer Yes or No.

Line 37

In Section C, answer Yes or No to each question.

Do you maintain a written policy statement prohibiting the personal use of vehicles by your employees? This includes commuting.

The policy statement must meet the following conditions:

- The employer owns or leases the vehicle and provides it to one or more employees for use in the employer’s trade or business.

- When the vehicle is not used in the employer’s trade or business, it is kept on the employer’s business premises, unless it is temporarily located elsewhere (for example, for maintenance or because of a mechanical failure).

- No employee using the vehicle lives at the employer’s business premises.

- No employee may use the vehicle for personal purposes, other than de minimis personal use (for example, a stop for lunch between two business deliveries).

- Except for de minimis use, the employer reasonably believes that no employee uses the vehicle for any personal purpose.

Line 38

Do you maintain a written policy statement prohibiting the personal use of vehicles by your employees, except for commuting?

The policy statement must meet the following conditions:

- The employer owns or leases the vehicle and provides it to one or more employees for use in the employer’s trade or business, and it is used in the employer’s trade or business.

- For bona fide noncompensatory business reasons, the employer requires the employee to commute to and/or from work in the vehicle.

- The employer establishes a written policy under which the employee may not use the vehicle for personal purposes, other than commuting or de minimis personal use (for example, a stop for a personal errand between a business delivery and the employee’s home).

- Except for de minimis use, the employer reasonably believes that the employee does not use the vehicle for any personal purpose other than commuting.

- The employer accounts for the commuting use by including an appropriate amount in the employee’s gross income.

However, this policy statement is not available if the employee is an officer, director, or 1% or more owner.

Line 39

Do you treat all use of vehicles by employees as personal use? Answer ‘Yes’ or ‘No.’

Line 40

Do you provide more than 5 vehicles for employees, other than related persons or 5% owners? If so, you do not need to complete the questions in Section B (Lines 30 through 36, above).

Line 41

Do you meet the requirements concerning qualified automobile demonstration use? To meet these requirements, you must maintain a written policy statement that:

- Prohibits its use by individuals other than full-time automobile salespersons

- Prohibits its use for personal vacation trips

- Prohibits storage of personal possessions in the automobile and

- Limits the total mileage outside the salesperson’s normal working hours

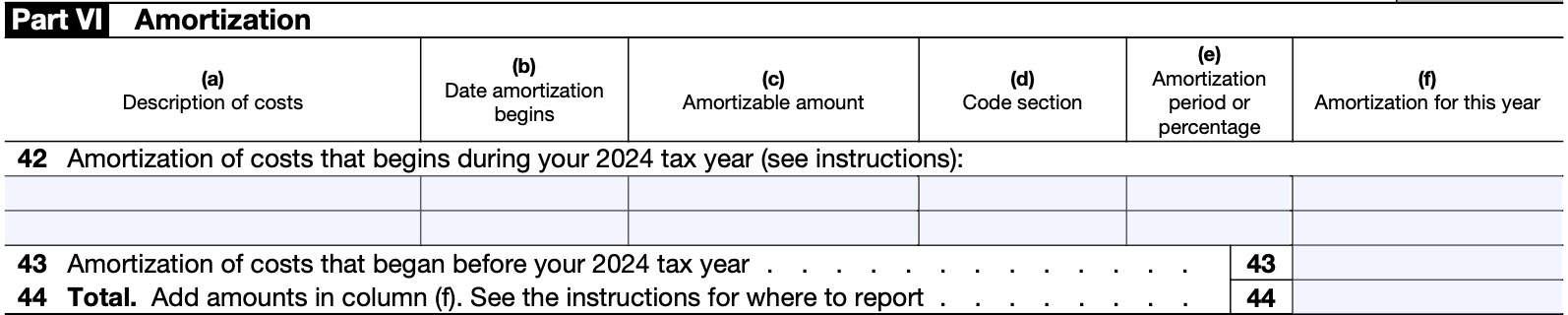

Part VI: Amortization

In Part VI, we’ll calculate amortization costs. You may amortize the following:

- Geological and geographical expenditures

- Pollution control facilities

- Bond premiums

- Research and experimental expenditures

- Lease acquisition costs

- Qualified forestation and reforestation costs

- Certain tax preferences under IRC Section 59(e)

- Certain Section 197 intangible assets, such as goodwill

- Startup and organizational costs for your business

- Creative property costs

If one or more of these applies to your situation, you should refer to the form instructions for more specific details.

Line 42: Amortization of costs beginning during the tax year

For each item, you’ll need to enter:

- Column (a): Description of the costs that you are amortizing

- Column (b): Date the amortization begins

- Column (c): Amortizable amount

- Column (d): Internal Revenue Code section

- Column (e): Amortization period or amortization percentage

- Column (f): Amortization for the year

Line 43: Amortization of costs beginning before the tax year

For Line 43, enter the total amortization costs in column (f) for costs that began before the given tax year.

However, if you are reporting non-R&D expenses that began before the tax year and there is no other reason to file Form 4562, you do not need to file this form. Simply enter the amortization amount directly on the ‘other deductions’ or ‘other expenses’ line of your federal tax return.

Line 44: total amortization

Add Lines 42 and 43. For more details, refer to IRS Publication 535, Business Expenses.

Classification of property

Depreciable property can be depreciated over a specific period of time, depending on what type of property it is. IRS publication 946 contains extensive guidance for determining the classification for most types of depreciable property.

Below are depreciation classifications for some of the most common property business owners place into service.

3-Year Property

3-year property includes the following:

- A race horse that is more than 2 years old at the time it is placed into service

- Any horse, other than a race horse, that is more than 12 years old at the time it is placed in service

- Any qualified rent-to-own property (as defined in IRC Section 168(i)(14)).

5-Year Property

5-year property includes the following:

- Automobiles

- Light general purpose trucks

- Typewriters, calculators, copiers, and duplicating equipment

- Any semi-conductor manufacturing equipment

- Any qualified technological equipment

- Any Section 1245 property used in connection with research and experimentation

- Certain energy property specified in IRC Section 168(e)(3)(B)(vi)

- Appliances, carpets, furniture, etc., used in a rental real estate activity

- Any new machinery or equipment used in a farming business and placed in service after 2017, in tax years ending after 2017

- The original use of the property must begin with you after 2017

- Does not include grain bins cotton ginning assets, fences, or other land improvements

7-Year Property

7-year property includes the following:

- Office furniture and equipment

- Railroad track.

- Any motorsports entertainment complex (as defined in IRC Section 168(i)(15)).

- Any natural gas gathering line (as defined in IRC Section 168(i)(17)) placed in service after April 11, 2005,

- The original use of which begins with you after April 11, 2005

- Is not under self-construction or subject to a binding contract in existence before April 12, 2005.

- No AMT adjustment is required

- Any used agricultural machinery and equipment placed in service after 2017, grain bins, cotton ginning assets, or fences used in a farming business

- No other land improvements

- Any property that does not have a class life and is not otherwise classified

Important note: 7 years is the default depreciation schedule for any property that does not have a class life and is not otherwise classified.

10-Year property

10-year property includes the following:

- Vessels, barges, tugs, and similar water transportation equipment

- Any single purpose agricultural or horticultural structure (see IRC Section 168(i)(13)).

- Any tree or vine bearing fruits or nuts

- Any qualified smart electric meter property

- Any qualified smart electric grid system property

15-year property

15-year property includes the following:

- Any municipal wastewater treatment plant

- Any telephone distribution plant and comparable equipment used for 2-way exchange of voice and data communications

- Any Section 1250 property that is a retail motor fuels outlet (whether or not food or other convenience items are sold there).

- Initial clearing and grading land improvements for gas utility property

- Certain electric transmission property specified in IRC Section 168(e)(3)(E)(v) placed in service after April 11, 2005

- Original use of which begins with you after April 11, 2005

- Is not under self-construction or subject to a binding contract in existence before April 12, 2005

- Qualified improvement property, as defined in IRC Section 168(e)(6), placed in service by you after December 31, 2017

20-year property

20-year property includes the following:

- Farm buildings

- Does not include single purpose agricultural or horticultural structures

- Municipal sewers not classified as 25-year property

- Initial clearing and grading land improvements for electric utility transmission and distribution plants

25-year property

25-year property includes the following:

- Property that is an integral part of the gathering, treatment, or commercial distribution of water that, without regard to this classification, would be 20-year property; and

- Municipal sewers

50-year property

50-year property includes any improvements necessary to construct or improve a roadbed or right-of-way for railroad track that qualifies as a railroad grading or tunnel bore under IRC Section 168(e)(4).

Residential real property

Any building where at least 80% of total rents comes from dwelling units.

Nonresidential real property

Nonresidential real property is any real property that is:

- Not residential rental property

- Not property with a class life of less than 27.5 years

Video walkthrough

Watch this in-depth video to learn how to calculate your depreciation and amortization deductions using Form 4562.

Are you tired of dreading tax season?

If you’re like most people, you push through the stress of filing, only to be hit with a bigger bill than expected—then put it all behind you until the same cycle repeats next year.

But what if you could change the game?

Tax planning puts you in control. It’s about being proactive, not reactive—taking small, smart steps throughout the year to reduce your tax burden, increase your savings, and keep more of your hard-earned money working for you.

Here’s what effective tax planning helps you do:

✅ Avoid the surprise of a high tax bill

✅ Understand how your income and decisions affect your taxes

✅ Strategically lower your tax liability over time

Ready to make smarter tax moves?

👉 Join my free weekly tax planning newsletter and get one actionable tip every week to help you reduce your taxes legally and effectively.

Start taking control—your future self will thank you.

Frequently asked questions

Listed property is property that taxpayers may frequently use in personal use or for business purposes. Listed property generally includes passenger vehicles or other automobiles that lend themselves to personal use, or property often used for recreational use, such as communications and recording equipment.

The Modified Accelerated Cost Recovery System, known as MACRS, allows taxpayers to depreciate and deduct a larger portion of their asset’s cost earlier in its life than the straight-line depreciation method. MACRS is required for most business asset depreciation unless another expense or depreciation method is allowed.

Qualified business use property generally is property used in any way for your trade or business. Qualified business use does not include investment use, lease of property to a 5% owner or related person, compensation for services performed as 5% owner or related person, or use as compensation for any person unless an amount is included in that person’s income for the use of the property.

How do I Find IRS form 4562?

You may find a copy of Form 4562 on the IRS website. For your convenience, we’ve enclosed the latest version in this article.

Related tax articles

This tax form is one of the fillable tax forms provided by the Internal Revenue Service, to help taxpayers reduce their tax preparation costs. To see more forms like this, visit our free fillable tax forms page, where you’ll also find articles like this.

Unlike the IRS, our articles contain step by step instructions for each tax form, as well as video walkthroughs. You can also check out all of our videos by subscribing to our YouTube channel!

You tube lead me your article. I love your article. It well explain about IRS instruction that I didn’t understand. I appreciated you.

I can’t find a definition anywhere of “Section 179 property”. How do I know whether something is Section 179 property? I have to know that to fill out the form.

According to the Internal Revenue Code, you can elect to recover all or part of the cost of certain qualifying property, up to a limit, by deducting it in the year you place the property in service. This is the Section 179 deduction. You can elect the Section 179 deduction instead of recovering the cost by taking depreciation deductions.

You can find more information about Section 179 in IRS Publication 946, Chapter 2: https://www.irs.gov/publications/p946

Where is the second-year and later depreciation of listed property reported? (not a new placement) All line 26? Should I adjust the basis for depreciation column E by depreciation claimed in previous years? Thank you Forrest!

You can still list second-year (and subsequent year) property in Line 26 as applicable. You don’t need to adjust the basis, since you’ll be recording the other key parts of the depreciation formula (such as year placed in service, original basis, and current year deduction) in the other columns.