IRS Form 1138 Instructions

Corporations that expect to incur a net operating loss can file IRS Form 1138 to request a tax extension for paying their prior year tax. By doing this, a corporation may avoid having to amend their prior year return to take the carryback of the operating loss later on.

In this article, we’ll walk through everything you need to know about IRS Form 1138, including:

- How to complete IRS Form 1138

- Filing considerations

- Frequently asked questions

Let’s begin with a step by step overview of this extension form.

Table of contents

How do I complete IRS Form 1138?

This one-page tax form is relatively straightforward. Let’s start with the taxpayer information at the top.

Taxpayer information

At the top of IRS Form 1138, enter the following taxpayer information.

Corporation name

Enter the name of the corporation here. This should reflect the name on your corporation’s most recent federal tax return or in your business documents.

Employer identification number

Enter the nine-digit employer identification number, or EIN, associated with your business. If you do not have an EIN, you may need to file Form SS-4 to apply for an employer identification number.

Corporation address

Enter your corporation’s address here. Include the suite, room, or other unit number after the street address. If you’ve changed your corporation’s address since the last income tax return was filed, you may need to file IRS Form 8822-B, Change of Address or Responsible Party – Business.

Post office address

If the post office does not deliver mail to the street address and the corporation has a P.O. box, show the post office box number instead.

Third party recipients

If the corporation receives its mail in care of a third party, such as an accountant or attorney, enter on the street address line “C/O” followed by the third party’s name and street address or P.O. box.

For example, attorney John Smith receives mail on behalf of his client, the Acme Corporation. Although Acme Corporation’s address is in a different location, John Smith’s address is: 1000 Main St, Any Town, TX 12345.

You would enter the Acme Corporation’s address as:

C/O John Smith,

1000 Main St

Any Town, TX 12345

Foreign addresses

If the corporation’s address is outside the United States or its possessions or territories, fill in the line for “City or town, state, and ZIP code” in the following order:

City

Province or state

Country

Follow the foreign country’s practice for entering the postal code, if any. Do not abbreviate the country name.

Lines 1 through 6

Let’s go through each line of Form 1138, step by step.

Line 1: Ending date of the tax year of the expected net operating loss (NOL)

In Line 1, enter the ending date for the taxable year in which you expect the net operating loss.

Line 2: Amount of expected NOL

In Line 2, enter the amount of the expected net operating loss that you reasonably expect based on the tax year.

According to the form instructions, you must consider all of the facts relating to the corporation’s operations when coming up with an estimated NOL. Include these items when estimating the amount of the expected NOL:

- The number and dollar amounts of the corporation’s government contracts that have been canceled

- Profit and loss statements, and

- Other factors that may specifically apply to the corporation’s operations.

Internal Revenue Code Section 172 may contain additional information to help determine the amount of the expected NOL.

NOL limitations

Limitations apply to:

- The amount of taxable income of a new loss corporation for any tax year ending after an ownership change that may be offset by any pre-change NOLs, and

- Use of preacquisition losses of one corporation to offset recognized built-in gains of another corporation (See IRC Section 384)

You will have the opportunity to add any necessary information in Line 5, which should support your estimates here.

Line 3

In Line 3, you’ll enter the expected reduction of a previously determined tax that is directly attributable to the expected net operating loss carryback. This should apply for specific tax years before the year of the NOL.

Previously determined tax

Previously determined tax is generally:

- The amount shown on the tax return, plus any amounts assessed as deficiencies before Form 1138 is filed; minus

- Any abatements, credits, or refunds allowed or made before filing Form 1138

According to IRC Section 1314(a):

- The increase or decrease in business income tax previously determined should come solely from the correct treatment of the item which was the subject of any tax error made

- This computation should be made for any other taxable year affected by either:

- An NOL deduction, or

- A capital loss carryback or carryover

- The calculated amount due, as well as any wrongfully collected income taxes or interest for each taxable year shall be that year’s adjustment amount.

You will need to attach a schedule showing how the reduction was figured. Refer to your corporate income tax return’s instructions for more details on calculating the NOL deduction and recomputing your tax liability.

Line 4: Ending date of the tax year immediately preceding the tax year of the expected NOL

In Line 4, enter the ending date of the immediately preceding tax year for the year in which you expect the NOL, or the prior tax year.

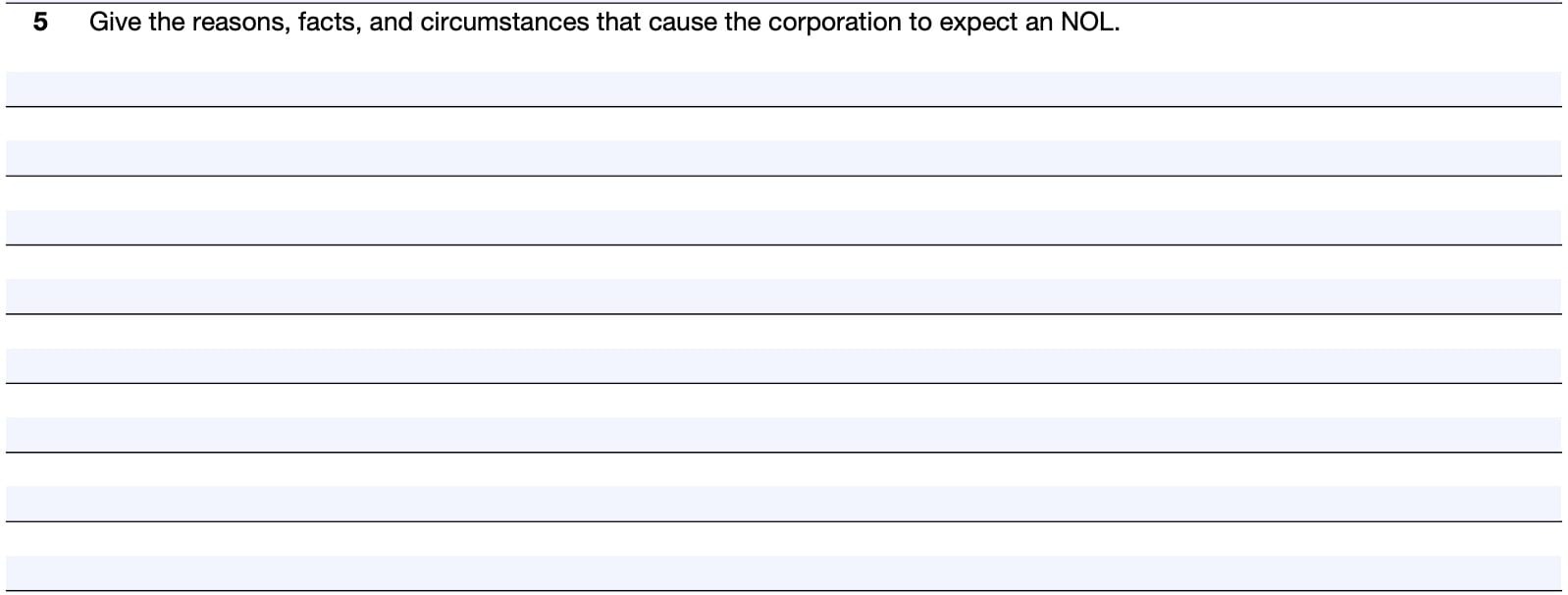

Line 5

In Line 5, you’ll enter the facts and circumstances that have caused the corporation to expect an NOL. These facts should support the anticipated net operating loss that you entered in Line 2.

Line 6: Amount for which payment is to be extended

In Line 6, we’ll calculate the amount of tax for which we are requesting additional time to pay. This line is broken down in to 3 parts.

Line 6a: Total tax shown on the tax return, plus deficiencies, interest, or penalties

For the previous year as shown on Line 4, enter on Line 6a the total of:

- The total tax shown on the return, plus

- Any amount assessed as one of the following prior to the filing of this IRS Form 1138:

- Tax deficiency

- Interest on outstanding tax

- Late payment penalty

Line 6b: Taxes paid plus refunds, credits, and abatements

In Line 6b, enter the total of the following:

- Amount of tax paid or required to be paid before the date you file this form (see below)

- Amount of tax refunds, credits, and abatements made before the date you filed this extension request

Tax paid or required to be paid before filing Form 1138

This amount includes the following:

- Any amount assessed as a tax deficiency if you file this form more than 21 calendar days after an IRS notice and demand for payment

- More than 10 business days in cases where the payment amount is $100,000 or greater

- Any interest or late payment penalty associated with this tax deficiency

However, do not include any tax amounts for which the corporation has received an extension of time to pay under IRC Section 6161. This might include the following tax extension requests:

- IRS Form 1127, Application for Extension of Time for Payment of Tax Due to Undue Hardship

- Not an automatic extension of time for payment of taxes, but based upon tax information provided to the IRS based upon the circumstances of the hardship

- IRS Form 4768, Application of Extension to File a Return for Estate & Generation-Skipping Transfer (GST) Tax

- Provides an automatic tax-filing extension as well as an extension to pay U.S. estate or GST tax

Line 6c: Amount of tax for which time for payment is extended

Subtract Line 6b from Line 6a, then enter the result. However, do not enter an amount that exceeds the amount reported on Line 3, above.

This is the amount for which the IRS will grant an extension of time to pay.

Signature

Sign and date the bottom of the form. There are a couple of notes for consideration.

Penalties of perjury apply

This statement indicates that if you knowingly misrepresent the company’s expected NOL in order to defer payment of income tax, then the Internal Revenue Service may hold you accountable for civil or criminal penalties.

Signature of officer

The officer’s signature implies that the person is authorized to represent the company with respect to this filing.

Filing IRS Form 1138

There are some additional considerations to filing IRS Form 1138 that you should understand.

Purpose of IRS Form 1138

A corporation can file IRS Form 1138 if the corporation:

- Expects to incur an NOL in the current tax year, and

- Can carry back the NOL to its preceding tax year

By filing Form 1138, the corporation can extend the period of time for payment of tax for that prior tax year. This includes an extension of time for payment of a tax deficiency.

However, the tax liability that you can postpone by filing Form 1138 cannot exceed the expected tax overpayment from the NOL carryback.

Only tax payments that are required to be paid after the filing of Form 1138 are eligible for extension. Do not file this form if all required payments have been paid or were required to have been paid.

Previous filings

If the corporation previously filed Form 1138 and later finds information that will change the amount of the expected NOL, the corporation can file a revised Form 1138.

Should the new information result in an increase of the NOL, the corporation can postpone the payment of a larger amount of tax as long as the larger amount has not yet been paid or is not yet required to be paid.

If the amount of the NOL decreases because of the new information, the corporation must pay the tax to the extent that the amount of tax postponed on the original filing exceeds the amount of tax postponed on the revised filing.

When to file IRS Form 1138

File Form 1138 after the start of the tax year of the expected NOL but before you must pay the tax from the preceding tax year.

Period of extension

In general, the extension for paying the tax expires at the end of the month in which the return for the tax year of the expected NOL is required to be filed (including extensions).

The corporation can further extend the time for payment by filing IRS Form 1139, Corporation Application for Tentative Refund, before the period of extension ends.

The period will be further extended until the date the IRS informs the corporation that it has allowed or disallowed the application in whole or in part.

Termination of extension

The IRS can terminate the extension if it believes that any part of the form contains erroneous or unreasonable information.

The IRS also can terminate the extension if it believes it may not be able to collect the tax.

Interest

The federal government charges interest on postponed amounts from the payment original due date. The interest is figured at the underpayment rate specified in IRC Section 6621.

How to file IRS Form 1138

As a general rule, file IRS Form 1138 with the Internal Revenue Service Center where the corporation files its income tax return.

A corporation can file Form 1138 as a separate extension form or with IRS Form 7004, Application for Automatic Extension of Time To File Certain Business Income Tax, Information, and Other Returns.

Filing with IRS Form 7004

If you file IRS Form 1138 and IRS Form 7004 together, the Form 1138 will reduce or eliminate the amount of tax due when you file Form 7004.

If Form 1138 is filed with Form 7004, then file Form 1138 with the Internal Revenue Service Center at the applicable address where the corporation files Form 7004.

Video walkthrough

Watch this instructional video to learn more about using Form 1138 to request an extension to pay taxes when expecting an NOL carryback.

Frequently asked questions

A corporation that expects a net operating loss (NOL) in the current year may file IRS Form 1138 to extend the period of time for payment of taxes due from the immediately preceding tax year. This avoids having to file an amended return to apply the NOL to the prior year taxes.

No. You may either file IRS Form 1138 with IRS Form 7004 to request an extension to file your tax return or as a standalone extension form.

No. Individual taxpayers may not file IRS Form 1138, even if they incur a net operating loss on Schedule C. IRS Publication 536, Net Operating Losses (NOLs) for Individuals, Estates, and Trusts, contains guidance on how to treat NOLs on a federal individual income tax return.

Where can I find IRS Form 1138?

You can find IRS forms (as PDF files) on the Internal Revenue Service website. For your convenience, we’ve enclosed the most recent version of IRS Form 1138 in this article.