IRS Form 8911 Instructions

In late 2022, the federal government passed the bipartisan Inflation Reduction Act, which provided tax incentives for taxpayers who invest in certain clean energy projects. One of those incentives is called the Alternative Fuel Vehicle Refueling Property Credit. This nonrefundable tax credit allows property owners to deduct part of the installation costs of qualified equipment from their federal tax returns on IRS Form 8911.

In this article, we’ll walk through everything you need to know about IRS Form 8911, including:

- How to complete and file IRS Form 8911

- Claiming the business/investment and personal use portions of the alternative fuel vehicle refueling property credit

- Other filing considerations

Let’s start with instructions on how to complete the form.

Table of contents

How do I complete IRS Form 8911?

There are two parts to this one-page tax form, as well as a Schedule A, which taxpayers must complete for each qualifying property:

- Part I: Credit for Business/Investment Use Part of Refueling Property

- Part II: Credit for Personal Use Part of Refueling Property

Before we get into the form, we should define qualified alternative fuel vehicle refueling property and its eligibility criteria.

Qualified alternative fuel vehicle refueling property

Qualified alternative fuel vehicle refueling property is any property that the taxpayer uses for either of the following purposes:

- To store or dispense alternative fuels, other than electricity, into the fuel tank of a motor vehicle that is propelled by the fuel, but only if the storage or dispensing is at the point where fuel is delivered into the fuel tank

- To recharge an electric vehicle, but only if the recharging property is located where the vehicle is recharged

Additional requirements include:

- Having placed the refueling property into service during the tax year

- Original use of the property begins with the taxpayer

- The property is used predominantly in the United States

- For personal use property, the property must be installed at your main home or primary residence

- After 2022, property must be located in an eligible census tract.

- An eligible census tract is any population census tract that:

- Is described as a low-income community census tract in Internal Revenue Code Section 45D(e), or

- Is not an urban area as designated by the Secretary of Commerce

- An eligible census tract is any population census tract that:

Let’s go through the entire form, step by step, beginning with Schedule A.

Schedule A

Schedule A contains 3 parts:

- Part I: Vehicle Refueling Property Details

- Part II: Credit Amount for Business/Investment Use Part of Refueling Property

- Part III: Credit Amount for Personal Use Part of Refueling Property

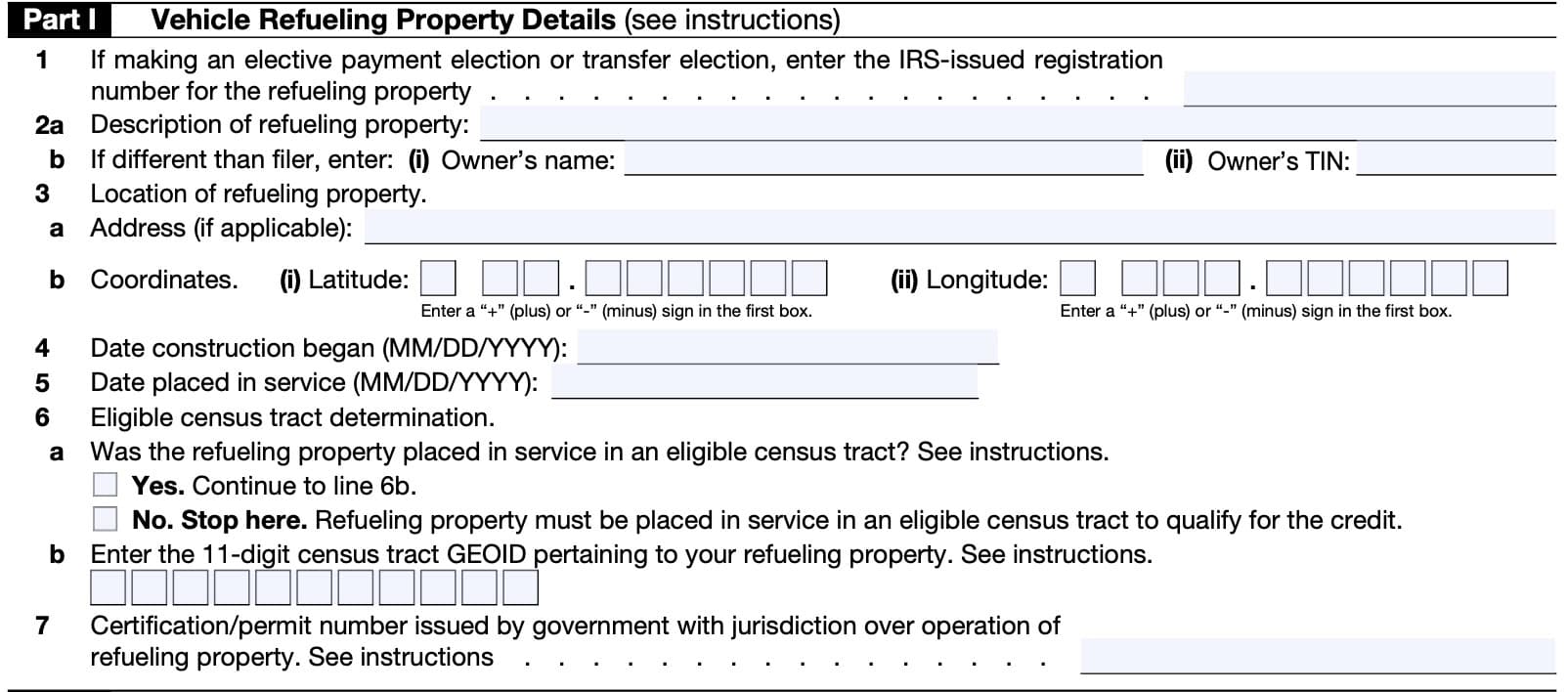

Part I: Vehicle Refueling Property Details

Line 1

If you are making an elective payment election or a transfer election, then enter the IRS-issued registration number for the refueling property.

The IRS-issued registration number can be obtained by completing a pre-filing registration for each refueling property for which you are claiming a property credit.

Line 2: Description of refueling property

In Line 2a, enter a description of the refueling property. If different from the filer’s tax information, enter the owner’s name and taxpayer identification number (TIN) in the spaces provided.

Line 3: Location of refueling property

In Line 3a, enter the address, if applicable. In Line 3b, enter the coordinates (latitude and longitude).

Line 4: Date construction began

Enter the date that construction began on the refueling property, in MM/DD/YYYY format.

Line 5: Date placed in service

Enter the placed-in-service date, in MM/DD/YYYY format.

Line 6: Eligible census tract determination

In Line 6a, was the refueling property placed in service in an eligible census tract? An eligible census tract is any population census tract that:

- Is described as a low-income community in Internal Revenue Code Section 45D(e), or

- Is not an urban area as designated by the Secretary of Commerce

If Yes, proceed to Line 6b. If No, stop. You cannot take a tax credit for this property.

In Line 6b, enter the 11-digit census tract identifier, or GEOID, that pertains to the refueling property. You can find more information on the U.S. Census website.

Line 7

Enter the certification or permit number that was issued by the government entity with jurisdiction over the property. If there is no applicable certification and/or permit number, do not fill out this line.

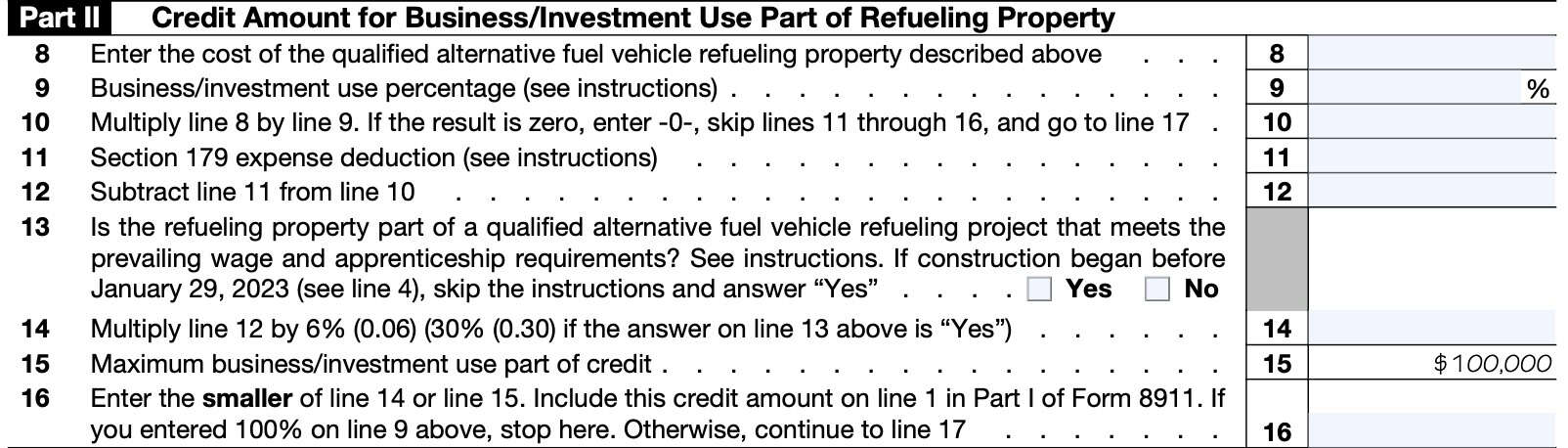

Part II: Credit Amount for Business/Investment Use Part of Refueling Property

Line 8: Cost of qualified alternative fuel vehicle refueling property

Enter the total installation cost of the qualified property described in Part I of Schedule A.

Line 9: Business/investment use percentage

Enter the percentage of business use or investment use. Enter 100% if the property is used solely for business/investment purposes.

If the refueling property is used for both business/ investment purposes and personal purposes, determine the percentage of business/investment use.

If during the tax year you convert refueling property used solely for personal purposes to business/investment use (or vice versa), figure the percentage of business/ investment use only for the number of months you use the property in your business or for the production of income.

Multiply that percentage by the number of months you use the property in your business or for the production of income and divide the result by 12.

Line 10

Multiply Line 8 by Line 9 and enter the result. If the result is zero, then skip Lines 11 through 16, and go to Part III of Schedule A.

Line 11: Section 179 expense deduction

Enter any IRC Section 179 expense deduction you took for the depreciable property from Part I of IRS Form 4562, Depreciation and Amortization.

Line 12

Subtract Line 11 from Line 10. Enter the result here.

Line 13: Prevailing wage and apprenticeship requirements

If construction of a project began before January 29, 2023, skip the instructions and answer Yes. Otherwise, review the instructions outlined below to determine whether to answer Yes or No.

Prevailing wage requirements

The taxpayer will ensure that any laborers and mechanics employed by the taxpayer or any contractor or subcontractor in the construction of any qualified alternative fuel vehicle refueling property that is part of the project are paid wages at rates not less than the prevailing rates for construction, alteration, or repair.

Apprenticeship requirements

Regarding the construction of any qualified alternative fuel vehicle refueling property that is part of the project, apprenticeship requirements are as follows.

- The taxpayer must ensure that, depending on when construction began, 10% to 15% of the total labor hours performed in the construction, alteration, or repair of the qualified project are performed by qualified apprentices from a registered apprenticeship program.

- The taxpayer must ensure that the applicable ratio of apprentices to journey-workers established by the registered apprenticeship program is met for apprentices working on the qualified project each day.

- Any taxpayer (or contractor or subcontractor) that employs four or more individuals in the construction, alteration, or repair of the qualified project must also hire at least one qualified apprentice

Line 14

If Line 13 is Yes, multiply Line 12 by 30%. Otherwise, multiply Line 12 by a credit rate of 6% and enter the total here.

Line 15: Maximum business/investment use part of credit

The default is $100,000 per property.

Line 16

Enter the smaller of Line 14 or Line 15. Also, include this credit amount on Line 1 in Part I of IRS Form 8911. If you entered 100% on Line 9, then stop here. Otherwise, go to Line 17, below.

Part III: Credit Amount for Personal Use Part of Refueling Property

Line 17: Was the refueling property installed on property used as your main home?

If Yes, continue to Line 18. Otherwise, stop here. You cannot take a credit for refueling property installed for personal purposes if installed on property not used as your primary residence.

Line 18

Subtract Line 10 from Line 8, above.

Line 19

Multiply Line 18 by 30%. Enter the total here.

Line 20: Maximum personal use part of credit

$1,000 is the default value here.

Line 21

Enter the smaller of Line 19 or Line 20. Also, include this credit amount on Line 4 in Part II of IRS Form 8911.

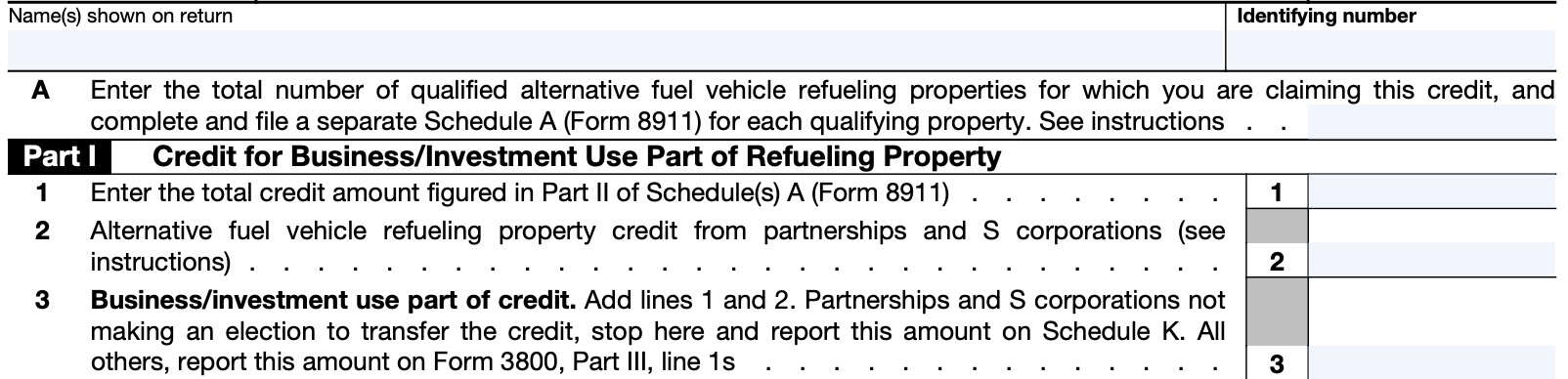

Part I: credit for business/investment use part of refueling property

Just before Part I, you’ll see the name and identifying number fields at the top of Form 8911. Please review these fields to ensure that your tax software has filled them in properly. Below that, you’ll see Line A, which should correspond to the number of refueling properties. Each property should have its own Schedule A.

Line 1: Total credit amount figured in Part II of Schedule A

Enter the total credit of qualified alternative fuel vehicle refueling property placed in service during the tax year.

Line 2: Alternative fuel vehicle refueling property tax credit from partnerships and S corporations

Enter the total alternative fuel vehicle refueling property credits from:

- Partnership: Schedule K-1 (Form 1065), Box 15, Code P, and

- S corporation: Schedule K-1 (Form 1120-S), Box 13, Code P

Line 3

Add Line 7 and Line 8. This represents the business/investment use of the credit.

For partnerships and S-corporations, stop here and report this amount on Schedule K. All other taxpayers should report this amount on IRS Form 3800, General Business Tax Credits, Part III, Line 1s.

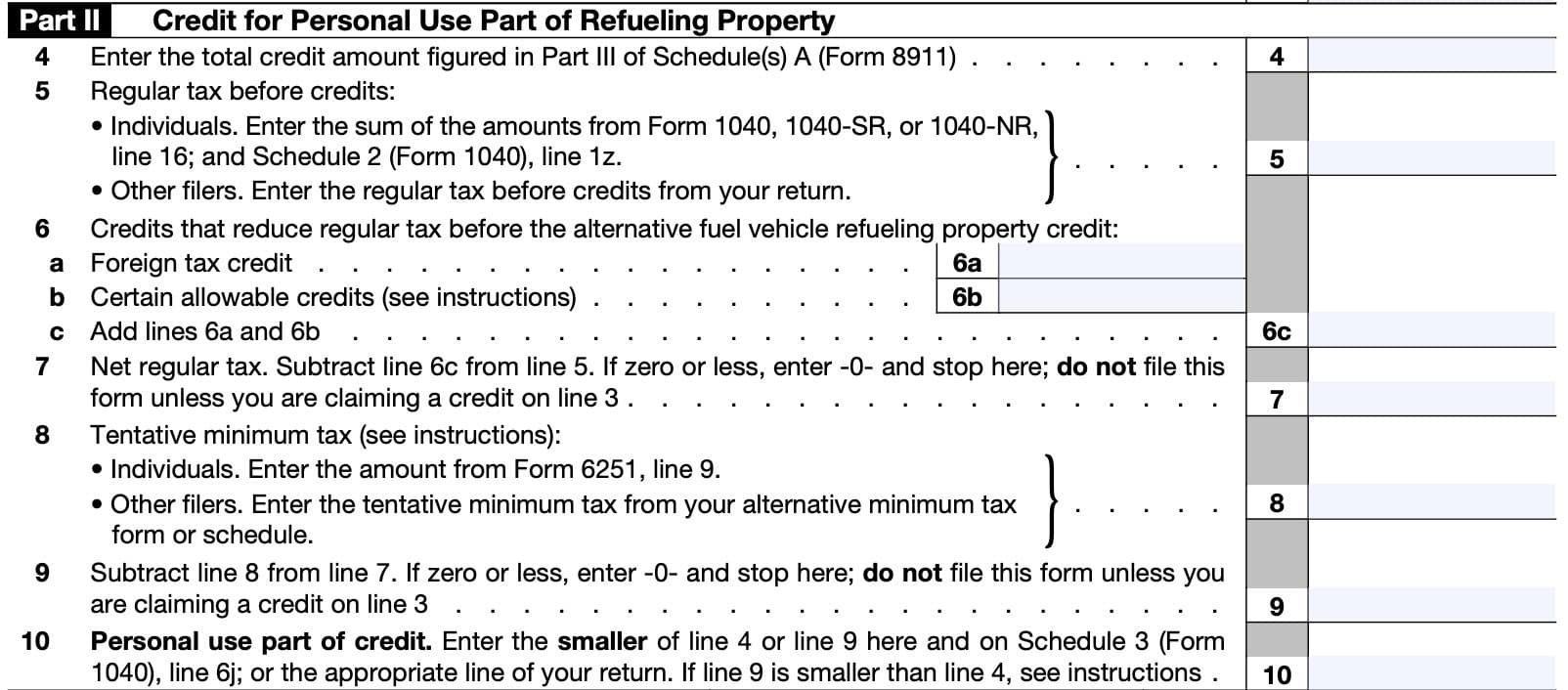

Part II: Credit for Personal Use Part of refueling property

In Part III, we’ll calculate the personal credit for qualified fueling equipment placed into service during the tax year.

Line 4

Enter the amount of qualified residential fueling equipment costs for equipment placed into service during the year, from Part III of Schedule A.

If the result is zero or less, stop here. Do not file this form unless claiming a tax credit under Part II.

Line 5: Regular tax before credits

For individuals, enter the sum of:

- IRS Form 1040, Form 1040-SR, or Form 1040-NR, Line 16

- Schedule 2, Line 1z

Other tax filers should enter the regular tax before credits are applied, from your income tax return.

Line 6: Credits that reduce regular tax before the alternative fuel vehicle refueling property credit

Enter the following types of credit, in the respective lines

Line 6a: Foreign tax credit

You can find this on IRS Form 1116, Foreign Tax Credit.

Line 6b: Certain allowable credits

Enter the total of any credits or adjustments on:

- IRS Form 1040, 1040-SR, or 1040-NR, Line 19: Child tax credit or credit for other dependents from Schedule 8812

- Schedule 3, Line 2: Credit for child and dependent care expenses from IRS Form 2441

- Schedule 3, Line 3: Education credits from Form 8863

- Schedule 3, Line 4: Retirement savings contributions credit from IRS Form 8880

- Schedule 3, Line 5: Residential energy credits from IRS Form 5695 (Part I and Part II)

- Schedule 3, Line 7: Other nonrefundable federal tax credits

You must reduce this amount by the following, reported on Schedule 3:

- Line 6a: General Business Credit

- Line 6b: Credit for Prior-Year Minimum Tax

- Line 6k: Credit to Holders of Tax Credit Bonds

Line 6c

Add Lines 6a and 6b together. Enter the total here.

Line 7: Net regular tax

Subtract Line 6c from Line 5. If the result is zero or less, then enter ‘0’ and stop. Do not file this form unless you are claiming a tax credit on Line 3.

Line 8: Tentative minimum tax

You may not owe alternative minimum tax (AMT), but you must still calculate the tentative minimum tax to figure your tax credit.

For individuals, complete IRS Form 6251, Alternative Minimum Tax, and enter the amount from Line 9.

For other filers, enter the tentative minimum tax from your AMT form or schedule.

Line 9

Subtract Line 8 from Line 7. If the result is zero or less, stop completing this form. Do not file unless you are claiming a credit on Line 3.

Line 10: Personal use part of credit

Enter the smaller of:

- Line 4

- Line 9

Also enter this number on Schedule 3, Line 6j (Form 1040), or the appropriate line of your tax return.

If Line 9 is smaller than Line 4, there is a portion of this tax credit that you may not use. Unfortunately, this credit is lost, as you cannot carry unused credits for personal use forwards or backwards into another tax year.

Video walkthrough

Watch this instructional video to learn more about how to claim this federal tax credit on your income tax returns.

Are you tired of dreading tax season?

If you’re like most people, you push through the stress of filing, only to be hit with a bigger bill than expected—then put it all behind you until the same cycle repeats next year.

But what if you could change the game?

Tax planning puts you in control. It’s about being proactive, not reactive—taking small, smart steps throughout the year to reduce your tax burden, increase your savings, and keep more of your hard-earned money working for you.

Here’s what effective tax planning helps you do:

✅ Avoid the surprise of a high tax bill

✅ Understand how your income and decisions affect your taxes

✅ Strategically lower your tax liability over time

Ready to make smarter tax moves?

👉 Join my free weekly tax planning newsletter and get one actionable tip every week to help you reduce your taxes legally and effectively.

Start taking control—your future self will thank you.

Frequently asked questions

The recently passed Inflation Reduction Act extended this tax credit to 2032. However, this was superceded by the One Big Beautiful Bill Act, which states that taxpayers cannot take this credit for any property placed into service after June 30, 2026.

For tax years 2022 and earlier, maximum tax credit amount is $1,000 per location, if you had a qualifying charging station at each location and you changed your main home during the tax year. For 2023 and later, the base credit is $1,000 per piece of property placed into service during the tax year.

This bipartisan infrastructure law raised the maximum credit for business and investment use property from $30,000 to $100,000. For personal use property, taxpayers may take the credit on more than one piece of property during a tax year, even if at the same location.

Charging equipment, such as electric vehicle chargers, EV charging stations, or charging stations for electric motor vehicles, can be considered eligible property for the alternative fuel vehicle refueling property credit as long as all credit requirements are met.

The Internal Revenue Service guidelines cite the following census tract requirements: Census tracts for eligible projects must be designated as low-income by 26 U.S. Code Section 45D(e), or not declared an urban area by the Secretary of Commerce.

Where can I get IRS Form 8911?

You may download this tax form and Schedule A from the IRS website as PDF files. For your convenience, we’ve included the latest version of both in this article, below.

Related tax forms

This tax form is one of the fillable tax forms provided by the Internal Revenue Service, to help taxpayers reduce their tax preparation costs. To see more forms like this, visit our free fillable tax forms page, where you’ll also find articles like this.

Unlike the IRS, our articles contain step by step instructions for each tax form, as well as video walkthroughs. You can also check out all of our videos by subscribing to our YouTube channel!