IRS Form 6251 Instructions

In 1969, Congress changed the tax law to institute an alternative minimum tax (AMT) to ensure high-income earners paid their fair share of income tax. This AMT tax is calculated and reported to the Internal Revenue Service on IRS Form 6251. Today, over 50 years later, there exists a lot of confusion over AMT, and how to minimize tax liability.

This in-depth guide will walk you through IRS Form 6251, Alternative Minimum Tax-Individuals, and help you understand:

- How to complete IRS Form 6251

- Filing considerations about IRS Form 6251

- How the AMT calculation works

- How tax planning can help you avoid AMT and lower your total tax bill

Let’s start with some background information about the alternative minimum tax.

Table of contents

How to complete IRS Form 6251

In this section, we’ll work through this tax form, step by step. That way, you can better understand how to complete this form.

Fortunately, tax software makes this easier than it used to be. And for taxpayers who have to complete this tax form, your accountant may very well earn their tax preparation fees simply by taking this off your hands.

There are 3 parts to IRS Form 6251:

- Part I: Alternative Minimum Taxable Income

- Part II: Alternative Minimum Tax (AMT)

- Part III: Tax Computation Using Maximum Capital Gains Rates

Let’s start with calculating alternative minimum taxable income in Part I.

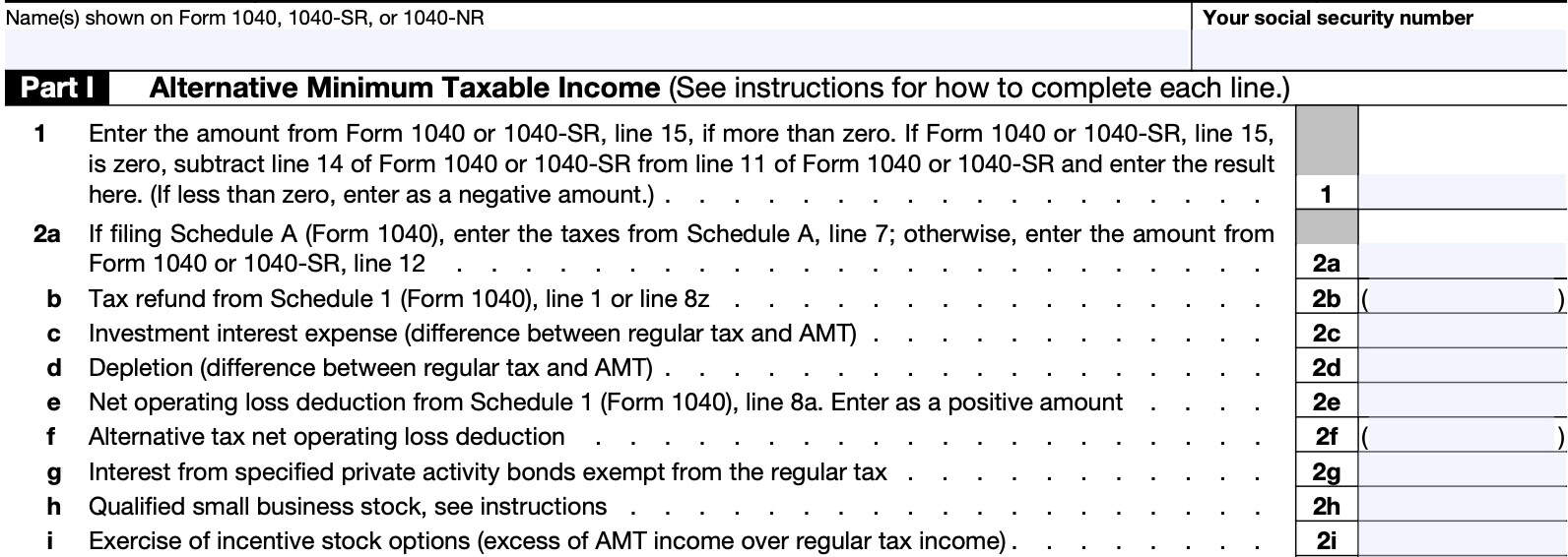

Part I: Alternative Minimum Taxable Income

In Part I, we’ll calculate your alternative minimum taxable income, or AMTI. To do this, we’ll use your taxable income from your regular tax return and add back certain adjustments or tax preference items to arrive at AMTI.

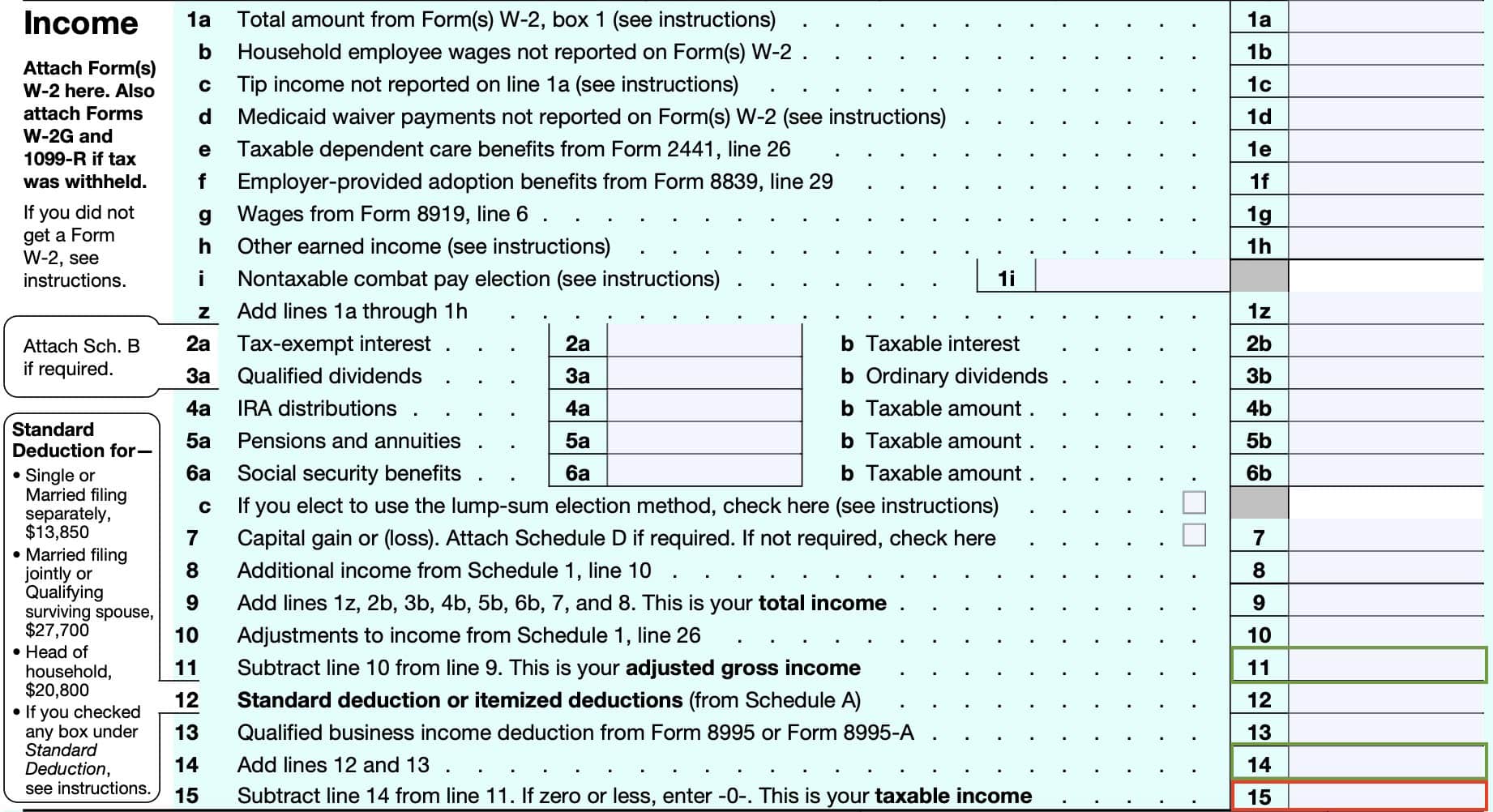

Line 1: Starting Income

Enter the amount from Line 15 of your IRS Form 1040 or IRS Form 1040-SR. This is the line marked, Taxable Income on your federal income tax return.

If your taxable income is zero, then subtract Line 14 from Line 11, which is your adjusted gross income (AGI) from your Form 1040.

Essentially, you’re subtracting the following deductions from your AGI:

- Standard deduction or itemized deductions from Schedule A

- Qualified business income deduction, as calculated on IRS Form 8995 or IRS Form 8995-A

This is the number that goes into Line 1.

After Line 1, we’ll use a a series of adjustments to help you arrive at your alternative minimum taxable income.

Not all of these apply to every taxpayer, so skip the items that do not apply.

Line 2a: Taxes

If you’re filing Schedule A (itemized deductions worksheet), you’ll enter the taxes from Line 7, except for the following any generation-skipping transfer taxes (GSTT) on income distributions.

Otherwise, enter the amount from your Form 1040, Line 12a.

Net qualified disaster loss

If you filed Schedule A just to claim an increased standard deduction on Form 1040 or 1040-SR due to a loss you suffered related to property in a federally declared disaster area, then enter zero on Line 2a and go to Line 2b.

You will include the amount of the standard deduction (before it was increased by any net qualified disaster loss) on Line 3.

Form 1040-NR filers

If you are filing Form 1040-NR, enter the amount of all taxes from Schedule A (Form 1040-NR), Line 1b, plus any foreign income taxes you are deducting on Schedule A (instead of claiming a foreign income credit on IRS Form 1116).

Don’t include any generation-skipping transfer taxes on income distributions.

Line 2b: Tax refunds

If you received a tax refund for state or local taxes paid, you’ll find that on Schedule 1 (Additional income and adjustments to income). Enter the amount from either:

- Line 1: Taxable refunds, credits, or offsets of state and local income taxes

- Line 8z: Other tax refunds attributable to any of the following:

- State or local personal property taxes or general sales taxes

- Foreign income taxes

- State, local, or foreign real property taxes

Line 2c: Investment interest expense

This line adds back any investment interest expense that you might have claimed as a deduction on either Schedule A or Schedule E.

Investment interest

You might have completed IRS Form 4952 to calculate the investment interest deduction for regular federal income tax purposes. If so, you’ll need to complete a second Form 4952 for AMT liability purposes.

In that case, you’ll follow these steps:

- Follow the Form 4952 instructions for Line 1. But also include any interest that would have been deductible if tax-exempt interest on private activity bonds were includible in gross income.

- Enter the AMT disallowed investment interest expense from the previous tax year on Line 2.

- Found on Line 7 of Form 4952

- In Part II, recalculate the following, with the appropriate adjustments:

- Gross income from property held for investment

- Net gain from the disposition of property held for investment

- Net capital gain from the disposition of property held for investment

- Investment expenses

- Complete Part III of Form 4952

On IRS Form 4952, include on Line 4a any tax-exempt interest income from private activity

bonds that you must include on Line 2g of Form 6251.

If you have any investment expenses that would have been deductible if the interest on the bonds were includible in gross income for the regular tax, you can use them to reduce the amount on Line 4a or include them on Line 5

After completing Part III on Form 4952, you’ll need to calculate the difference between Line 8 of the regular Form 4952 and the AMT Form 4952. If your AMT expense is greater, enter the difference as a negative amount.

Enter this result into Line 2c.

Investment interest expense that is not an itemized deduction

If you didn’t itemize deductions and you had investment interest expense, don’t enter an amount on Form 6251, Line 2c, unless you reported investment interest expense on Schedule E. If you did, follow the steps above for completing Form 4952.

Allocate the investment interest expense allowed on Line 8 of the AMT Form 4952 in the same way you did for the regular tax.

Enter on Line 2c, the difference between:

- Amount allowed on Schedule E for the regular tax return, and

- Amount allowed on Schedule E for AMT purposes

Line 2d: Depletion

As with Line 2c, you’ll need to recalculate the amount of depletion allowed based on:

- Taxable income from the property under Section 613(a),and

- The limit based on taxable income, with certain adjustments, under Section 613A(d)(1)

Additionally, depletion deduction for mines, wells, and other natural deposits under Section 611 is limited to the property’s adjusted basis at the end of the year, as refigured for AMT. An exception applies to independent producers or royalty owners claiming percentage depletion for oil and gas wells under Section 613A(c).

Enter the difference between the AMT amount and the regular amount. If the AMT amount is more than the regular deduction, enter this as a negative number.

Line 2e: Net operating loss deduction

Enter the number from Schedule 1, Line 8a, if applicable. This should be a positive amount.

Line 2f: Alternative tax net operating loss deduction (ATNOLD)

This is the sum of the alternative tax net operating loss (ATNOL) carrybacks and carryforwards fom previous years to the tax year. If this applies to your situation, the form instructions contain detailed guidance on this calculation.

Enter this amount as a negative number.

Line 2g: Interest from specified private activity bonds exempt from regular tax

This is interest income from “specified private activity bonds” reduced (but not lower than zero) by any deduction that would have been allowable if the interest were includible in gross income for the regular tax.

Each payer of this interest should send you a Form 1099-INT. This amount should be included in Box 9.

Specified private activity bonds

Generally, the term specified private activity bond means any private activity bond (as defined in Internal Revenue Code Section 141) the interest on which isn’t includible in gross income for the regular tax if the bond was issued after August 7, 1986. This definition generally does not include any bonds issued in 2009 or 2010.

Don’t include interest on the following:

- Qualified New York Liberty Bonds

- Qualified Gulf Opportunity Zone bonds

- Qualified Midwestern disaster area bonds

- Qualified Hurricane Ike disaster area bonds

Exempt-interest dividends

Exempt-interest dividends paid by a mutual fund or other regulated investment company are treated as interest income on specified private activity bonds to the extent that

- The dividends are attributable to interest on the bonds received by the company,

- minus an allocable share of the expenses paid or incurred by the company in earning the interest.

This specified private activity bond interest dividends amount will appear in your Form 1099-DIV, Box 13.

IRS Form 8814 filers

If you are filing IRS Form 8814, Parents’ Election To Report Child’s Interest and Dividends, include on this line any tax-exempt interest income from Line 1b of that form that is an AMT preference item.

Line 2h: Qualified small business stock

Applicable if you claimed the exclusion under Section 1202 for gain on qualified small business stock:

- Acquired before September 28, 2010, AND

- Held more than 5 years

If this is the case, multiply the excluded gain by 7%. This will be in IRS Form 8949, column (g). Enter this result in Line 2h as a positive number.

Line 2i: Incentive stock options

For regular tax purposes, the exercise of incentive incentive stock options (ISO) in accordance with Section 422(b) has no tax impact. Under AMT rules, it does. Generally, you must include the difference, if any, of:

- The fair market value of the stock acquired through exercise of the option (determined without regard to any lapse restriction) when your rights in the acquired stock first become transferable or when these rights are no longer subject to a substantial risk of forfeiture; AND

- The exercise price that you paid for the stock

- Including any amount you paid for the stock option that you used to acquire the stock.

If you received IRS Form 3921, Exercise of an Incentive Stock Option Under Section 422(b), you might be able to use those numbers to calculate your adjustment.

As a general rule, if you exercise an ISO and sell the underlying stock in the same year, there should be no difference between the AMT treatment and regular tax treatment of those transactions.

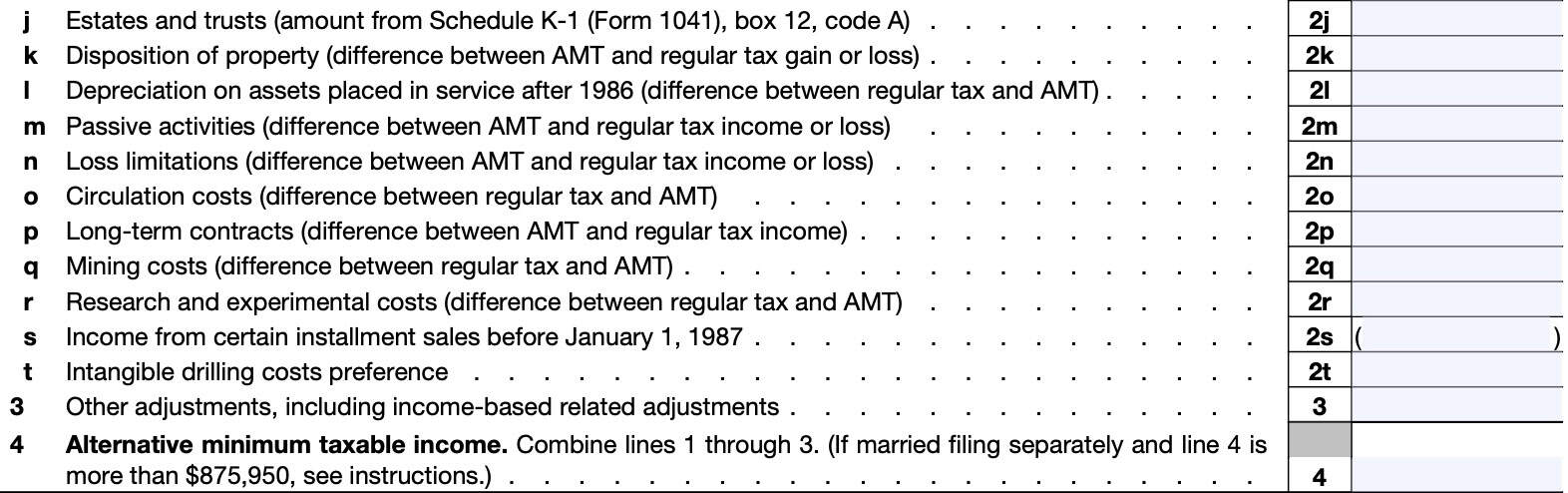

Line 2j: Estates & trusts

Include the amount from IRS Form 1041, Schedule K-1, Box 12, Code A, if applicable.

According to the Schedule K-1 instructions, Code A simply is the total of the following adjustments on a beneficiary’s K-1 statement:

- AMT adjustment attributable to qualified dividends

- AMT adjustment attributable to net short-term capital gain

- AMT adjustment attributable to net long-term capital gain

- AMT adjustment attributable to unrecaptured section 1250 gain

- AMT adjustment attributable to 28% rate gain

- Accelerated depreciation

- Depletion

- Amortization

- Exclusion items

In other words, the AMT adjustments for the beneficiaries of estates and trusts look similar to the adjustments on a U.S. individual tax return.

Line 2k: Disposition of property

This line will include the AMT adjustment for any gains or losses on the disposition of property. Use this line to report any of the following:

- Gain or loss from the sale, exchange, or conversion of property reported on IRS Form 4797, Sales of Business Property

- Casualty gain or loss to business or income-producing property that you reported on IRS Form 4684, Casualties and Thefts

- Ordinary income from the disposition of property not already accounted for, or on another line on Form 6251

- Capital gain or loss reported on either:

- IRS Form 8949 or

- Schedule D, Capital Losses & Gains

For more detailed instructions, or for examples of calculations, please refer to the form instructions.

Line 2l: Depreciation on assets placed in service after 1986

This is a very confusing line. AMT adjustments for depreciation consider some depreciation, but not all depreciation. Some must be recalculated, while some are not.

Here is a list of each:

Do not use depreciation for the following items

- Passive activities. Take this adjustment into account on Line 2m, instead

- An activity for which you aren’t at risk. Take this adjustment into account on Line 2n

- Income or loss from a partnership or an S corporation if the basis limitations apply. Take this adjustment into account on Line 2n

- A tax shelter farm activity. Take this adjustment into account on Line 3

Recalculate the following types of depreciation

- Property placed in service after 1998 that is depreciated for the regular tax using the 200% declining balance method (generally 3-, 5-, 7-, and 10-year property under the modified accelerated cost recovery system (MACRS)

- Except for certain qualified property eligible for the special depreciation allowance, as described under depreciation that is NOT refigured, below

- Section 1250 property placed in service after 1998 that isn’t depreciated for the regular tax using the straight line method; and

- Tangible property placed in service after 1986 and before 1999.

- If the transitional election was made under Section 203(a)(1)(B) of the Tax Reform Act of 1986, this rule applies to property placed in service after July 31, 1986.

Other depreciation that is NOT refigured

- Residential rental property placed in service after 1998

- Nonresidential real property with a class life of 27.5 years or more placed in service after 1998 that is depreciated for the regular tax using the straight line method

- Other section 1250 property placed in service after 1998 that is depreciated for the regular tax using the straight line method

- Property (other than section 1250 property) placed in service after 1998 that is depreciated for the regular tax using either

- 150% declining balance method, or

- Straight line method

- Property for which you elected to use the alternative depreciation system(ADS) of IRC Section 168(g) for the regular tax

- Qualified property that is or was eligible for a special depreciation allowance if the depreciable basis of the property is the same for the AMT and the regular tax

- Any part of the cost of any property for which you elected to take a Section 179 expense deduction. The reduction to the depreciable basis of Section 179 property by the amount of the Section 179 expense deduction is the same for the regular tax and the AMT

- Motion picture films, videotapes, or sound recordings

- Property depreciated under the unit-of-production method or any other method not expressed in a term of years

- Indian reservation property that meets the requirements of Section 168(j)

- A natural gas gathering line placed in service after April 11, 2005

How to refigure depreciation for AMT purposes

Recalculating depreciation for AMT purposes largely depends on when the property was placed into service.

Property placed in service before 1999

Recalculate depreciation for AMT using the alternative depreciation system, or ADS, using the same convention as for the regular tax system. Use the following table for method and recovery period

| IF the property is | THEN use the |

| Section 1250 property | Straight line method over 40 years |

| Tangible property (other than Section 1250 property) depreciated using straight line method for calculating regular tax liability | Straight line method over the property’s AMT class life |

| Any other tangible property | 150% declining balance method, changing to straight line method in the first year that SL method gives a larger deduction, over the property’s AMT class life |

Property placed in service after 1998

For property placed into service after 1998, use the same convention and recovery period used for regular tax.

For Section 1250 property, use the straight line method.

For all other property, use the 150% declining balance method. Change to straight line method in the first year that SL method gives a larger deduction.

Please refer to the instructions for more details on how to determine AMT class life.

Line 2m: Passive activities

You may need to recalculate passive activity gains and losses for AMT by accounting for all adjustments and preferences, as well as any AMT prior year unallowed losses that apply to that passive activity.

You’ll enter the difference between AMT-allowed and regular gain/loss as calculated on:

- IRS Schedule C, Profit or Loss From Business

- IRS Schedule E, Supplemental Income and Loss

- IRS Schedule F, Profit or Loss from Farming

- IRS Form 4835, Farm Rental Income and Expenses

If any of the following situations apply, enter the AMT amount as a negative number:

- AMT loss exceeds the regular tax loss

- AMT gain is less than the regular tax gain

- You have an AMT loss and a regular tax gain

Publicly traded partnership

If you had a loss from a PTP, refigure the loss using any AMT adjustments and preferences and any AMT unallowed loss from prior years.

Line 2n: Loss limitations

You’ll need to refigure gains and losses from the following by accounting for all AMT adjustments and preferences that apply:

- Activities for which you aren’t at risk, and

- Basis limitations applicable to partnerships and S corporations

To avoid duplication, any AMT adjustment or tax preference item taken into account on this line shouldn’t be taken into account in figuring the amount to enter on any other adjustment or tax preference item line of this form.

Line 2o: Circulation costs

Circulation costs are the expenses to establish, maintain, or increase circulation of a newspaper, magazine, or other periodical.

These are normally fully deductible in the year they were paid or incurred. For AMT purposes, the taxpayer must capitalize and amortize these costs over 3 years.

Enter the difference in Line 2o, even if it’s a negative number.

If you had a loss on property, but the circulation costs were not fully amortized, then your AMT deduction is the smaller of:

- The allowable loss for the costs, had they remained capitalized, OR

- Remaining costs to be amortized for AMT purposes

Line 2p: Long-term contracts

For AMT purposes, most taxpayers must use the percentage-of-completion method described in Section 460(b) to determine income from a long-term contract. However, this rule doesn’t apply to home construction contracts.

For contracts excepted from the percentage-of-completion method by Section 460(e)(1), you’ll use simplified procedures for allocating costs in Section 460(b)(3) to determine percentage of completion.

Taxpayers required to use percentage-of-completion method may owe interest or be entitled to a refund of interest for the tax year the contract is completed. See IRS Form 8697, Interest Computation Under the Look-Back Method for Completed Long-Term Contracts, for additional details.

Line 2q: Mining costs

Mining exploration and development costs deducted in full for the regular tax in the tax year they were paid or incurred must be capitalized and amortized over 10 years for AMT calculations.

Enter the difference between the regular tax deduction and the AMT amortization.

However, you do not need to do this for costs where you elected the optional 10-year write-off.

Line 2r: Research and development costs

In a similar manner to mining costs, taxpayers must amortize research and development costs over a 10-year period. Enter the difference between the regular tax deduction and AMT-allowed deduction.

Line 2s: Income from certain installment sales before January 1, 1987

Enter the amount of installment sale income reported for regular tax purposes as a negative amount on Line 2s.

Line 2t: Intangible drilling costs preference

This is also a preference item that warrants an adjustment for AMT purposes.

If this applies to your situation, the form instructions contain additional information about how to calculate excess intangible drilling costs (IDCs).

Line 3: Other adjustments

You’ll enter other income-related adjustments that might apply to your situation. This could include:

- Depreciation figured using pre-1987 rules on equipment placed into service after 1987

- Pollution control facilities

- Tax shelter farm activities

- Charitable contributions of certain property

- Business interest limitation

- Biofuel producer credit and biodiesel and renewable diesel fuels credit

- Mortgage interest deducted on Schedule A on a non-primary residence, such as a vacation home

- Net qualified disaster loss

It’s important to note that adjustments to one item might warrant a recalculation to another item.

Possible affected items

Examples of items that could be affected by adjustments elsewhere include:

- Section 179 expense deduction (Form 4562, Line 12)

- Expenses for business or rental use of your home

- Conservation expenses (Schedule F, Form 1040, Line 12)

- Taxable IRA distributions, if prior year IRA deductions were different for AMT and regular tax purposes (Form 1040, Line 4b)

- Self-employed health insurance deduction (Schedule 1, Line 17)

- Self-employed SEP, SIMPLE, and qualified plans deduction (Schedule 1, Line 16)

- IRA deduction (Schedule 1, Line 20)

Line 4: AMT Income

Combine Lines 1 through 3, then enter the total in Line 4.

If your tax filing status is married filing separately

If your filing status is married filing separately, and Line 4 is more than $875,950, then you must include an additional amount.

If Line 4 is greater than $1,142,550, then add another $66,650. Otherwise, include 25% of the excess AMT amounts above $875,950.

For example, if the Line 4 amount is $895,950, then enter $900,950 instead. The additional $5,000 is 25% of the $20,000 difference ($895,950 minus $875,950).

Let’s proceed to Part II, where we’ll calculate the actual AMT tax liability.

Part II: Alternative Minimum Tax (AMT)

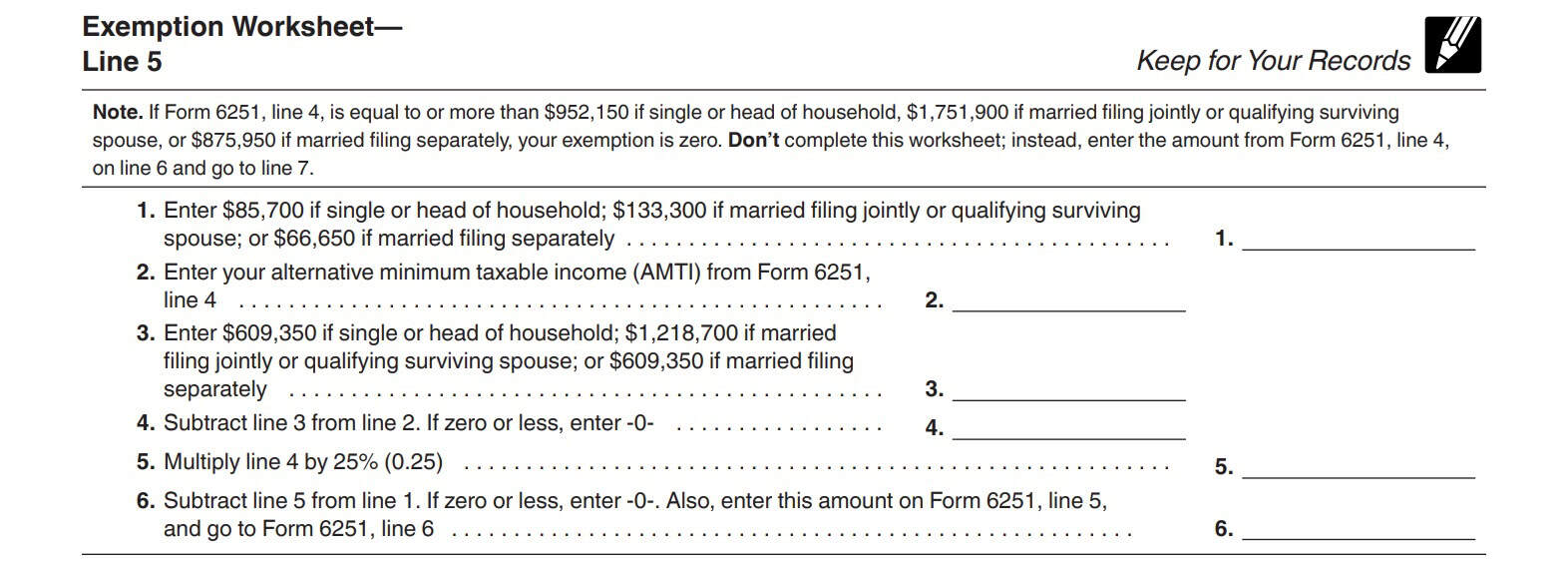

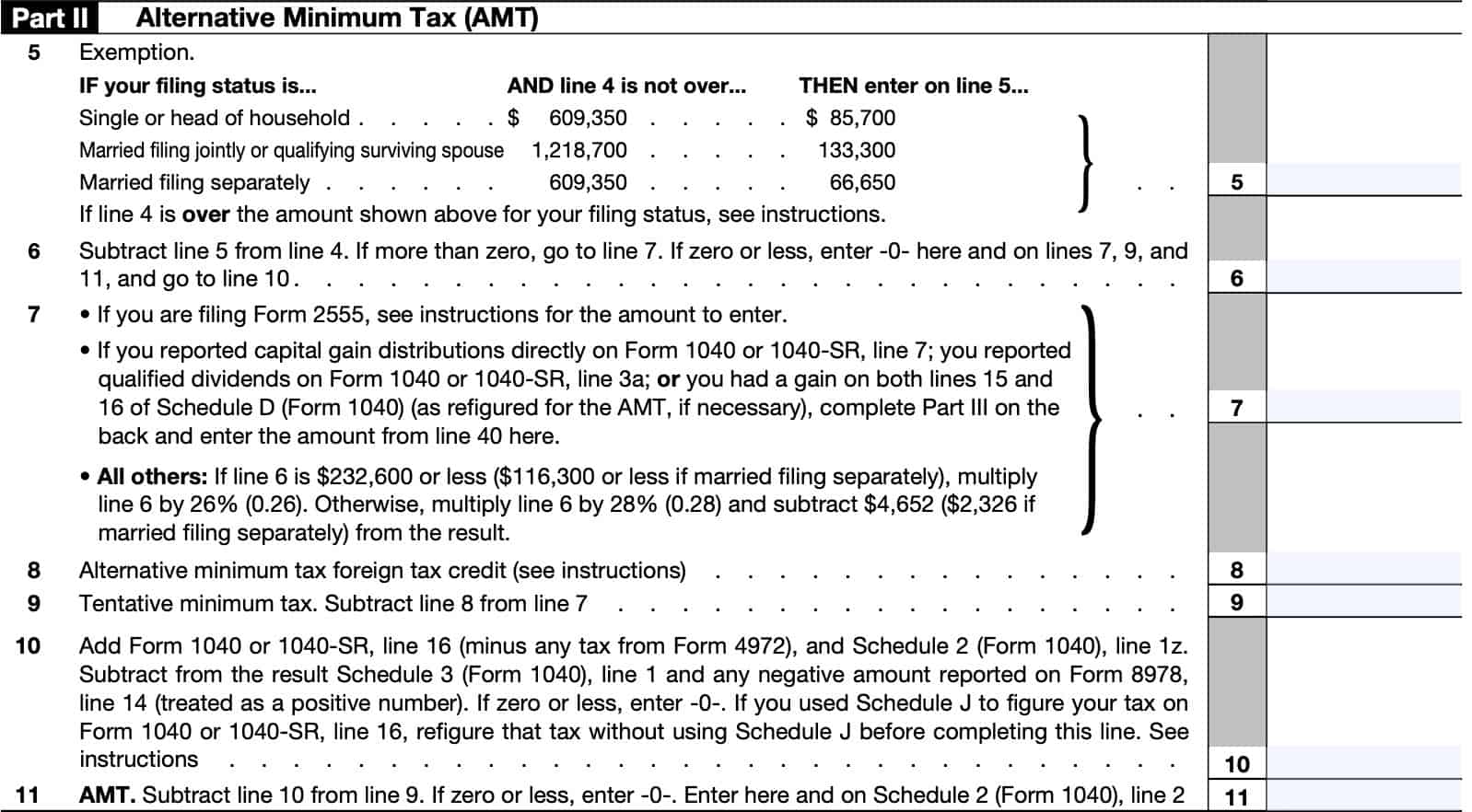

Line 5: Exemption amount

Your AMT exemption amount depends on your filing status and the amount of income you have. See the table below.

| Filing status | Line 4 is not over: | Enter this amount on Line 5 |

| Single or head of household | $609,350 | $85,700 |

| Married filing jointly or qualifying widow(er) | $1,218,700 | $133,300 |

| Married filing separately | $609,350 | $66,650 |

If Line 4 is over the respective amount for your filing status, you’ll need to complete an exemption amount worksheet. See below.

Line 6

Subtract Line 5 from Line 4, then enter the result.

If more than zero, go to Line 7.

If zero or less, enter ‘0’ on the following:

Go to Line 10.

Line 7

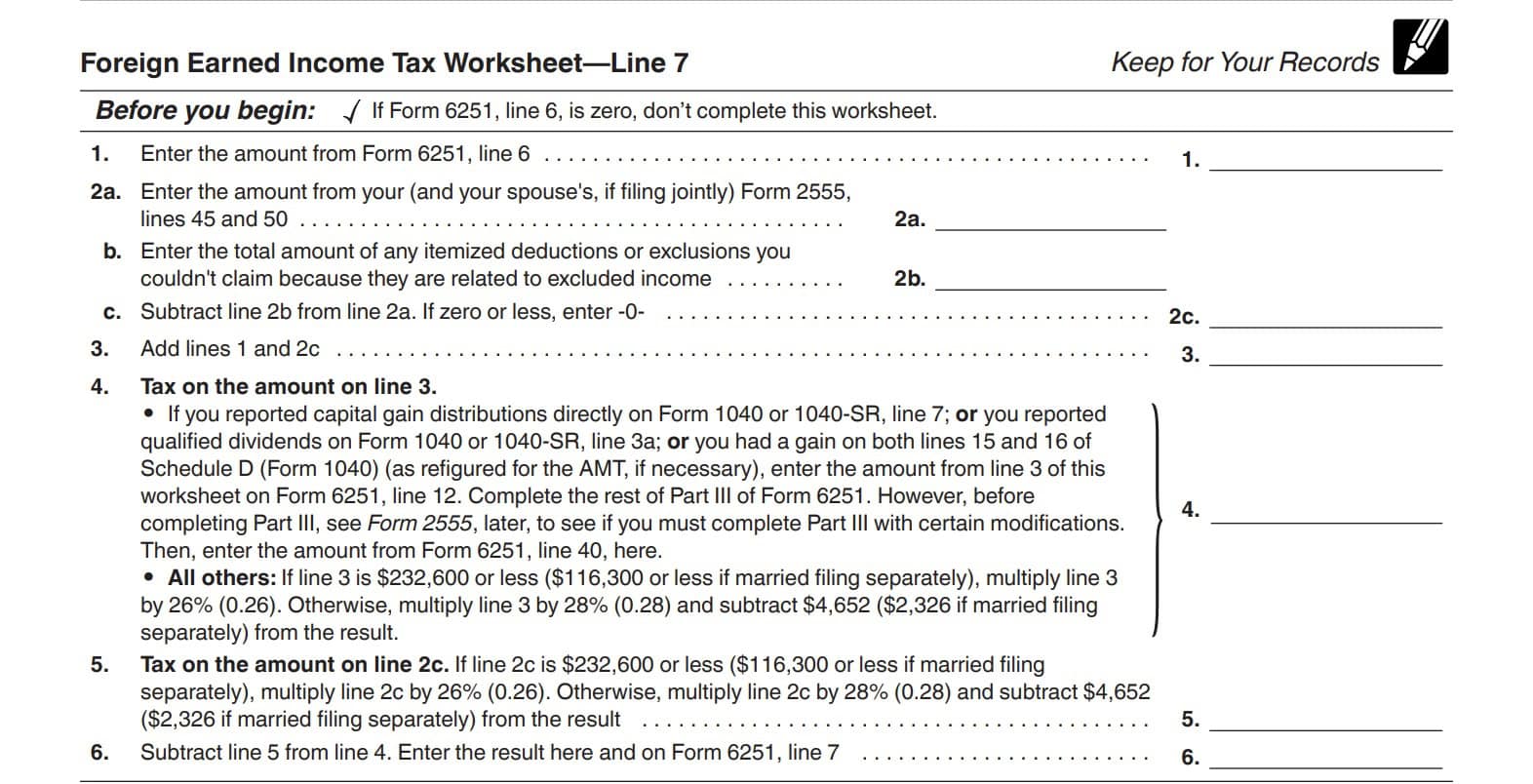

If you are filing Form 2555 because you have foreign earned income, you’ll need to complete a Foreign Earned Income worksheet (see below).

If you reported capital gain distributions

If you reported capital gain distributions on Form 1040, Line 7, qualified dividends on Line 3a, or had a gain on both Lines 15 and 16 of Schedule D, then you’ll need to:

All other taxpayers

If Line 6 is $232,600 or less ($116,300 if married filing separately), multiply Line 6 by the AMT tax rate of 26%.

For AMT amounts above this threshold:

- Multiply Line 6 by 28%

- Subtract $4,652 from the result

- $2,326 for taxpayers with tax filing status of married filing separate returns

Line 8: Alternative minimum tax foreign tax credit

If foreign tax credits apply to you, you may need to refer to the instructions to determine your foreign tax credit under AMT.

Line 9: Tentative minimum tax

Subtract Line 8 from Line 7. The result is your tentative minimum tax.

Line 10

This primarily applies to people who filed IRS Form 8978, Partner’s Additional Reporting Year Tax, or farmers and fishermen who filed Schedule J on their Form 1040.

If either applies, you’ll need to calculate your adjustment as outlined below.

IRS Form 8978 filers

Decrease the amount you report on Form 6251, line 10, by any negative amount reported on Form 8978, Line 14 (treated as a positive number).

Schedule J filers

If you file Schedule J to figure your tax on Form 1040, 1040-SR, or 1040-NR, Line 16, you must refigure that tax (including any tax from Form 8814) without using Schedule J before completing this line.

This is only for Form 6251; don’t change the amount on Form 1040, 1040-SR, or 1040-NR, Line 16.

Line 11

Subtract Line 10 from Line 9. Enter the amount here and on Schedule 2, Additional Taxes. This is your alternative minimum tax.

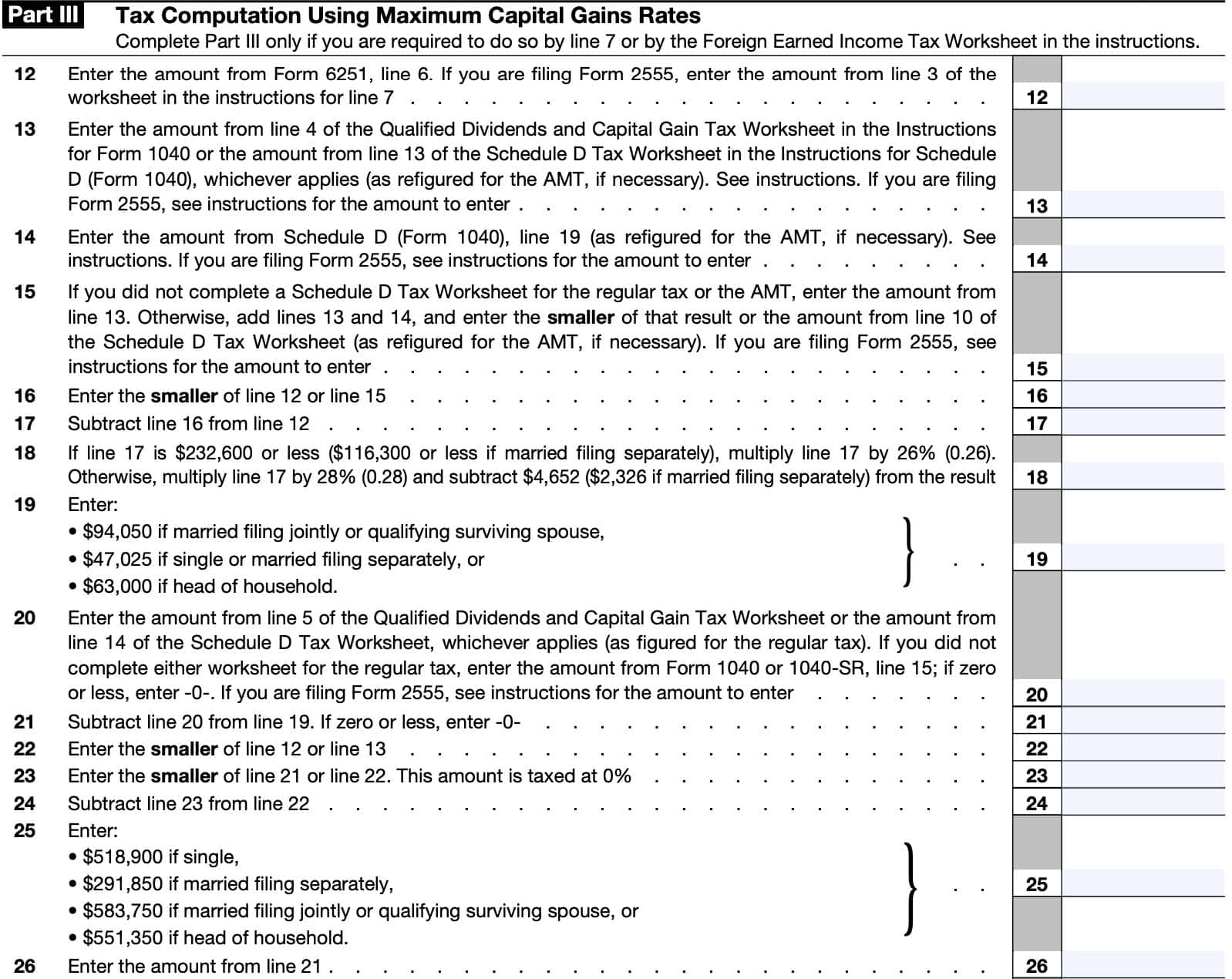

Part III: Tax Computation Using Maximum Capital Gains Rates

Not all taxpayers must complete Part III. Only complete Part III if one of the following applies:

- You followed the instructions for Line 7, and they directed you to complete Part III,

- The Foreign Earned Income Tax Worksheet directs you to do so

Line 12: Enter amount from Line 6

Enter the amount from Line 6, above, unless you’re filing Form 2555. In this case, then enter the amount from Line 3 of the foreign earned income worksheet located in the instructions for Line 7.

Line 13

Follow the instructions for Lines 13 through 15 if any of the following apply:

- The gain or loss from any transaction reported on Form 8949 or Schedule D is different for AMT and regular tax purposes because of a different basis due to:

- Depreciation adjustments

- ISO adjustments

- Different AMT loss carryover from the previous tax year

- You didn’t complete either the Qualified Dividends and Capital Gain Tax Worksheet or the Schedule D Tax Worksheet because Form 1040, 1040-SR, or Form 1040-NR, Line 15, is zero

- You received a Schedule K-1 that shows an amount in Box 12 with code B, C, D, E, or F.

If any of these apply, follow the respective instructions outlined below.

In Line 13, enter the capital gains distributions amount from:

- Line 4 of the Qualified Dividends and Capital Gain Tax Worksheet in the Form 1040 instructions, or

- Line 13 of the Schedule D Tax Worksheet

Line 14

Enter unrecaptured Section 1250 depreciation amount from Schedule D, Line 19.

Line 15

If you did not complete Schedule D, enter the amount from Line 13.

If you did complete Schedule D, add Lines 13 and 14, then enter the smaller of:

- That result, OR

- Line 10 from Schedule D

Line 16

Enter the smaller of Line 12 or Line 15 here.

Line 17

Subtract Line 16 from Line 12. Enter the result here.

Line 18: AMT Tax Brackets

If Line 17 is $232,600 or less ($116,300 for married couples filing separately), multiply Line 17 by 26%.

Otherwise, multiply by 28%, and subtract $4,652 (or $2,326 if married filing separate returns)

Line 19

Enter:

- $94,050 if married filing jointly or qualifying surviving spouse

- $47,025 if single or married filing separately

- $63,000 if head of household

If filing IRS Form 1040-NR, enter $47,025 ($94,050 if your filing status is qualifying surviving spouse).

Line 20

Enter the one that applies:

- Line 5 of the Qualified Dividends and Capital Gain Tax Worksheet

- Line 14 of the Schedule D Tax Worksheet

- Form 1040, Line 15 (taxable income)

Form 2555 filers

If you are filing Form 2555, the amount you enter on Line 20 will take into account your regular tax capital gain excess, if any. Don’t refigure this amount using the amount of your AMT capital gain excess.

If you are filing Form 2555 and you didn’t complete either the Qualified Dividends and Capital Gain Tax Worksheet or the Schedule D Tax Worksheet for the regular tax, enter the amount from line 3 of the Foreign Earned Income Tax Worksheet in the Form 1040 instructions.

Line 21

Subtract Line 20 from Line 19. If result is negative, enter ‘0.’

Line 22

Enter the smaller of Line 12 or Line 13.

Line 23

Enter the smaller of Line 21 or Line 22. This amount is taxed at 0%.

Line 24

Subtract Line 23 from Line 22. Enter the result in Line 24.

Line 25

Enter the number that applies, based on your tax filing status:

| Filing Status | Number |

| Single | $518,900 |

| Married filing separately | $291,850 |

| Married filing jointly or qualifying widow(er) | $583,750 |

| Head of household | $551,350 |

Line 26

Enter the amount from Line 21 here.

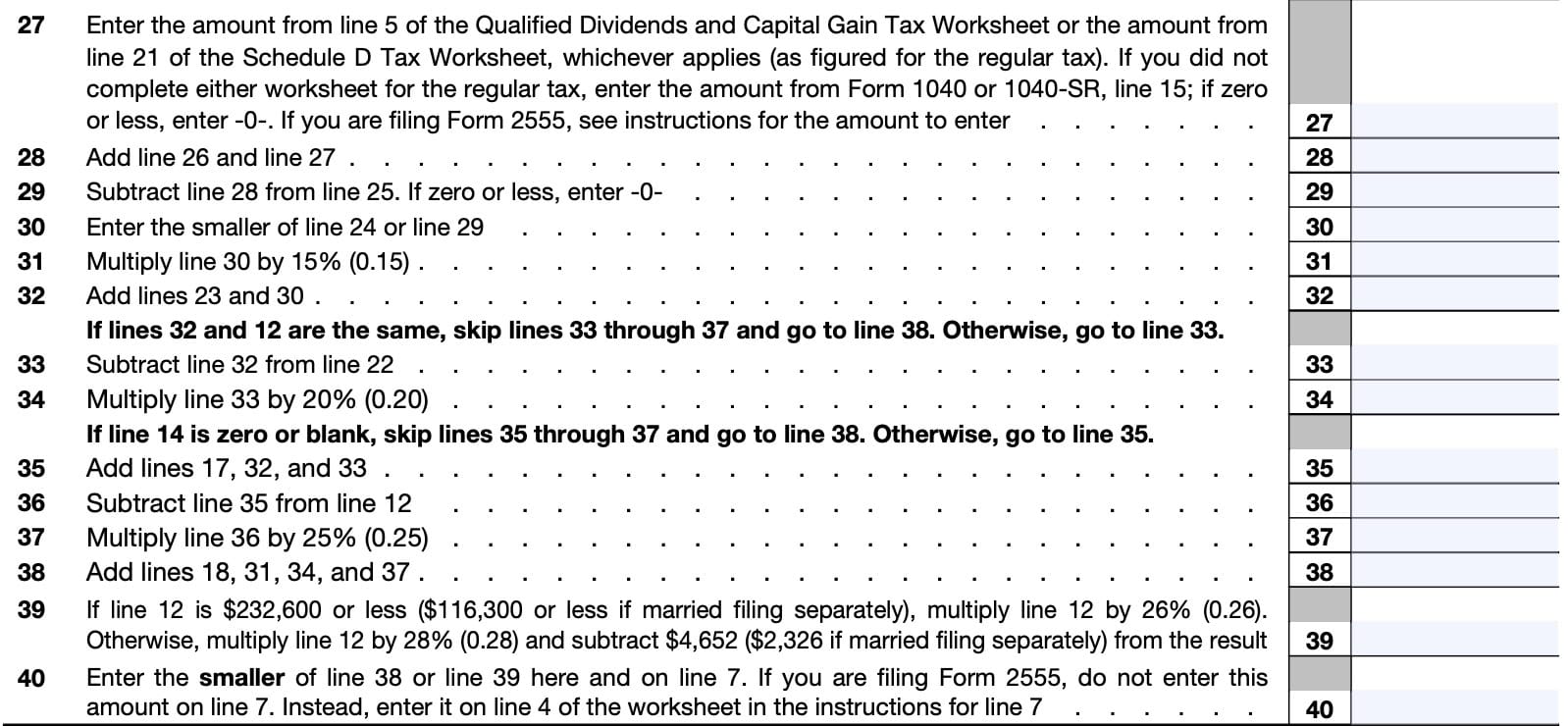

Line 27

Enter one of the following, whichever applies:

- Amount from Line 5 of the Qualified Dividends and Capital Gain Tax Worksheet

- Amount from Line 21 from Schedule D

- Form 1040, Line 15 (taxable income)

Line 28

Add Line 26 and Line 27, then enter the result here.

Line 29

Subtract Line 28 from Line 25. If zero or less, enter ‘0.’

Line 30

Enter the smaller of:

- Line 24

- Line 29

Line 31

Multiply the Line 30 amount by 15%, then enter the total here.

Line 32

If Line 32 and Line 12 are identical, go directly to Line 38. If they are not identical, go to Line 33.

Line 33

Subtract Line 32 from Line 22, then enter the result here.

Line 34

Multiply Line 33 by 20%, then enter the result.

If Line 14 is zero or blank, skip Lines 35 through 37 and go to Line 38. Otherwise, go to Line 35.

Line 35

Add the following lines:

Enter the result here.

Line 36

Subtract Line 35 from Line 12. Enter the result here.

Line 37

Multiply Line 36 by 25%, then enter the result.

Line 38

Add the following:

Enter the total here.

Line 39: AMT percentages

If Line 17 is $232,600 or less ($116,300 for married couples filing separately), multiply Line 17 by 26%.

Otherwise, multiply Line 17 by 28%, then subtract $4,652 (or $2,326 if married filing separate returns).

Line 40

Enter the smaller of either Line 38 or Line 39 here and on Line 7

Form 2555 filers

If filing Form 2555, do not enter this amount on Line 7. Instead, enter this amount on Line 4 of the worksheet in the instructions for Line 7.

Filing considerations

Below are some filing considerations for taxpayers who may need to use Form 6251 to calculate their tax liability.

How do I file Form 6251?

Taxpayers who must file IRS Form 6251 will generally complete it with their personal income tax return. However, they do not need to attach the form to their tax return unless one of the following is true:

- IRS Form 6251, Line 7 is greater than Line 10

- You claim any general business credit, and either Line 6 or Line 25 of IRS Form 3800 is more than zero

- You claim one of the following:

- Qualified electric vehicle credit (using IRS Form 8834)

- Personal use part of the alternative fuel vehicle refueling property credit on IRS Form 8911

- Credit for prior year minimum tax (IRS Form 8801)

- The total of Lines 2c through 3 is negative, and Line 7 would be greater than Line 10 if you did not account for Lines 2c through 3.

How do I determine whether I’m subject to AMT?

The IRS Form 1040 instructions help taxpayers determine whether AMT applies to them. According to the form instructions, taxpayers may use one of two methods to do this:

- Schedule 2, Line 1 Instructions

- IRS Form 6251

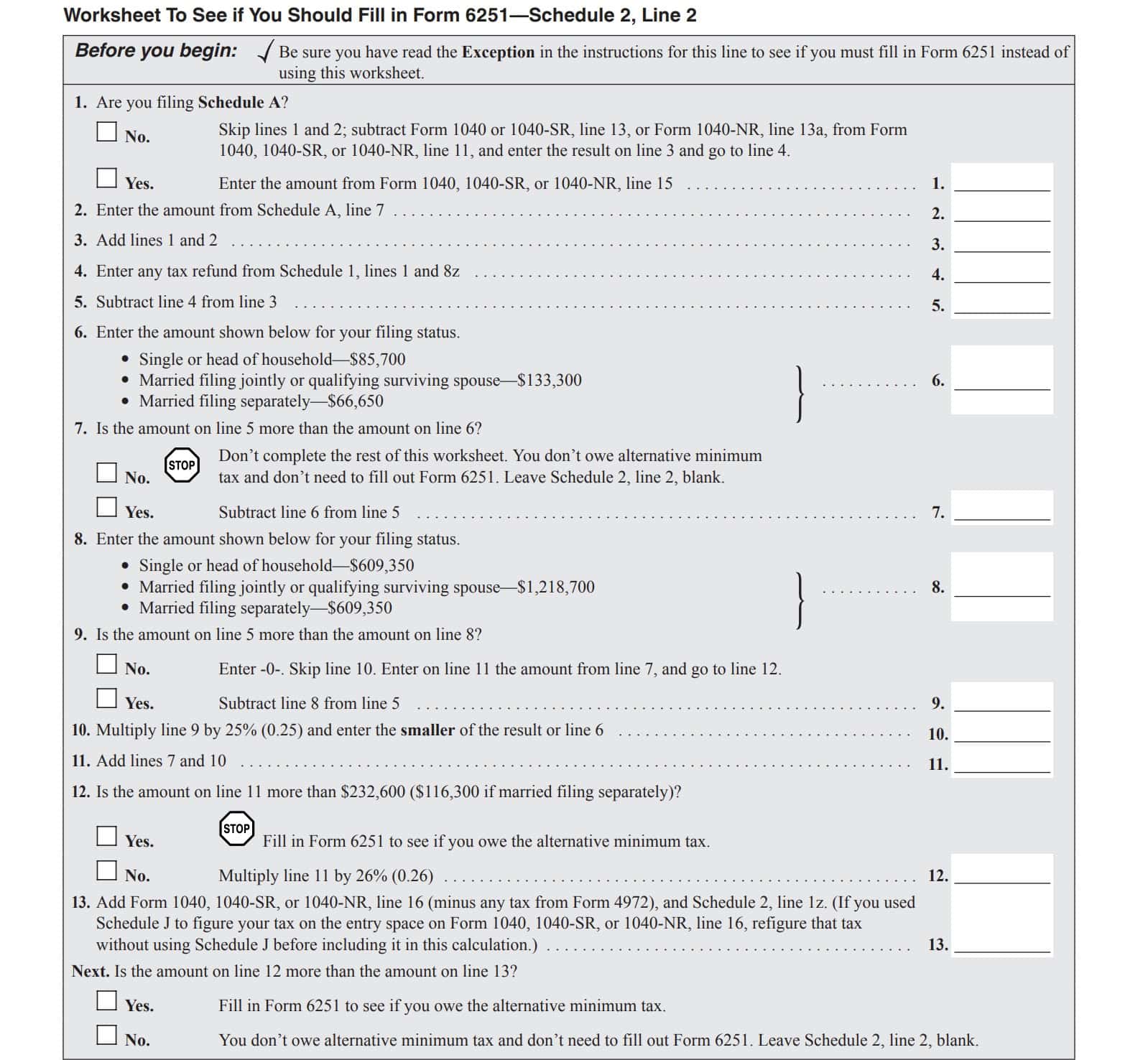

In either case, if AMT applies, then the taxpayer must complete Form 6251. Let’s take a look at the Schedule 2 instructions.

Schedule 2, Line 1 instructions

These instructions contain a worksheet that taxpayers may use to determine whether AMT applies in their situation.

If it does, then they will complete IRS Form 6251 to perform their alternative minimum tax calculation.

For step by step guidance on using the Schedule 2 worksheet, watch the following YouTube video:

IRS Form 6251

However, the instructions also state that taxpayers who may have received or claimed any of the following do not need to complete the Schedule 2 worksheet.

- Accelerated depreciation

- Tax-exempt interest from private activity bonds

- Intangible drilling, circulation, research, experimental, or mining costs

- Amortization of pollution-control facilities or depletion

- Income or (loss) from tax-shelter farm activities, passive activities, partnerships, S corporations, or activities for which you aren’t at risk

- Income from long-term contracts not figured using the percentage-of-completion method

- Investment interest expense reported on IRS Form 4952

- Net operating loss deduction

- Alternative minimum tax adjustments from an estate, trust, electing large partnership, or cooperative

- Section 1202 exclusion

- Stock by exercising an incentive stock option and you didn’t dispose of the stock in the same year.

- Any general business credit claimed on Form 3800 if either Line 6 (in Part I) or line 25 of Form 3800 is more than zero

- Qualified electric vehicle credit

- Alternative fuel vehicle refueling property tax

- Credit for prior year minimum tax

- Foreign tax credit

- Net qualified disaster loss and you are reporting your standard deduction on Schedule A, line 16

Simply go straight to Form 6251 to calculate the amount of alternative minimum tax that may apply.

If any of the above apply to your situation, you’ll need to complete IRS Form 6251.

Video walkthrough

Watch this video for step by step instructions on completing Form 6251.

Are you tired of dreading tax season?

If you’re like most people, you push through the stress of filing, only to be hit with a bigger bill than expected—then put it all behind you until the same cycle repeats next year.

But what if you could change the game?

Tax planning puts you in control. It’s about being proactive, not reactive—taking small, smart steps throughout the year to reduce your tax burden, increase your savings, and keep more of your hard-earned money working for you.

Here’s what effective tax planning helps you do:

✅ Avoid the surprise of a high tax bill

✅ Understand how your income and decisions affect your taxes

✅ Strategically lower your tax liability over time

Ready to make smarter tax moves?

👉 Join my free weekly tax planning newsletter and get one actionable tip every week to help you reduce your taxes legally and effectively.

Start taking control—your future self will thank you.

Frequently asked questions

Below are some frequently asked questions about AMT and Form 6251.

According to the Internal Revenue Service, certain tax benefits can significantly reduce a taxpayer’s regular tax amount. The alternative minimum tax (AMT) applies to taxpayers with high economic income by setting a limit on those benefits to ensure that taxpayers with higher incomes pay at least a minimum amount of tax.

IRS Form 6251, Alternative Minimum Tax, is the tax form that individual taxpayers may use to calculate and report their alternative minimum tax income, or AMTI, on their federal income tax return.

Yes, if you file Form 1040 electronically as well.

Where can I find a copy of Form 6251?

You may find tax forms, such as IRS Form 6251, on the IRS website. For your convenience, we’ve included the latest version below.

Related Posts

This tax form is one of the fillable tax forms provided by the Internal Revenue Service, to help taxpayers reduce their tax preparation costs. To see more forms like this, visit our free fillable tax forms page, where you’ll also find articles like this.

Unlike the IRS, our articles contain step by step instructions for each tax form, as well as video walkthroughs. You can also check out all of our videos by subscribing to our YouTube channel!

Dear Forrest

I found your website while looking for information regarding how to complete form 1116. The website is chock full of helpful, practical information. Many thanks for such a generous helpful source.

Best wishes

James Taylor