9 Year End Tax Planning Tips for 2024

When I was a financial planner, new clients or prospective clients would always ask me for year end tax planning tips. I would usually ask a few questions about their situation, discuss a financial decision they were already contemplating, and politely offer a suggestion or two.

But every time, I would think about why my clients never did this. Usually, it’s because we never thought of tax planning as a year-end event. Instead, we would treat it as an important part of every significant financial decision, regardless of what part of the calendar year we make that decision.

However, the end of the year does present some opportunity to slow down, think about financial decisions, and get ready for the new year.

In this article, we’ll discuss:

- Benefits of tax planning throughout the tax year

- 9 year-end tax planning tips that may help you in the current tax year

- Ways to optimize those tax tips into next year’s routine so you get more of a benefit

- What you can do if you can’t take advantage of a tax tip

Let’s start with discussing some of the benefits of tax planning throughout the year.

Table of contents

- Year-Around Tax Planning Vs. Year-End Tax Planning

- Tax Tip #1: Utilize 529 College Savings Plans

- Tax Tip #2: Maximize Deductions to Lower Income

- Tax Tip #3: Accelerate Deductible Expenses

- Tax Tip #4: Donate to Charities for Tax Deductions

- Tax Tip #5: Implement a Tax-Loss Harvesting Strategy

- Tax Tip #6: Maximize Retirement Account Contributions

- Tax Tip #7: Leverage Health Savings Accounts

- Tax Tip #8: Use Annual Gift Tax Exclusion

- Tax Tip #9: Consider Roth conversions

- What do you think?

Year-Around Tax Planning Vs. Year-End Tax Planning

Imagine your neighborhood has an annual ‘Best Lawn’ competition. And you take pride in your lawn. Lots of pride. And as a result, you win the competition every year.

But this year, your neighbor decides to enter the competition, two weeks out. He never takes care of his lawn. It’s always brown and ratty because he never waters it.

And worst of all, he’s asked you for lawn care tips because he really wants to impress the neighborhood.

Of course, if you had 6 months, you could work with this guy to make a plan:

- Putting together a budget to overhaul his yard

- What kind of grass to plant

- Watering schedule, etc.

But with two weeks? Is he crazy?

That’s kind of how many accountants feel. Especially when your tax professional sees missed opportunities, after it’s too late to do anything about it.

But there are still some things that you can do before the end of the calendar year that might help lower your taxes, and help you get ready for tax season.

But don’t take my word for it. I’ve curated tax tips from a variety of tax and financial professionals, so you can hear it directly from them.

Mandatory disclosure: These tax tips do not represent tax, investment, or legal advice, and are for informational purposes only. These are the opinions of each contributor (including myself), and may not apply to every situation.

For best results, please consult with a tax professional before implementing any of these year end tax planning tips.

Tax Tip #1: Utilize 529 College Savings Plans

If you’re looking to save for your children’s college education, a qualified tuition plan, more commonly known as college savings plan, is one of the best ways to do so.

Keith Piscitello, a Certified Financial Planner™ with S2 Wealth Planning, offers the following:

Many states have 529 college savings plans that offer tax savings for those who contribute to the state-specific 529 plan. Contributions can be made for any family member, or even yourself.

The funds in the account will grow tax-deferred, and if used for qualified educational expenses in college, university, or even private elementary and high school tuition, all distributions will be tax-free.

If your child is already attending college, rather than paying tuition directly to the school, make a contribution to your state-sponsored 529 to get the tax credit, then immediately request the distribution to the school. This way, you can take advantage of tax-savings as you fund tuition.

Finally, rolling over a 529 account or Coverdell Educational Savings account from a non-state-specific plan to your home-state 529 savings plan (subject to certain contribution limits) may be a way to qualify as a current year tax-advantaged contribution as well.

Opportunities for next year

If you don’t already have a college savings plan, start one today. If you already have one, set aside an appropriate budget.

Most importantly, have frequent conversations with your children about the costs of college, as well as the benefits. This will help your children associate their collegiate future with a price tag, and allow them to make their own tradeoffs.

Finally, because of recent changes to the tax code, unused qualified tuition plan money can be converted to a Roth IRA, with certain additional guidelines. This can be a great way to help your child get a head start on their own retirement planning.

What to do if you can’t take advantage of this opportunity

If your child is already in college, you may look into other tax-advantaged opportunities.

For example, you may be able to claim either the American Opportunity Tax Credit or Lifetime Learning Credit for college related expenses. To learn more, check out our guide on IRS Form 8863, Education Credits.

Tax Tip #2: Maximize Deductions to Lower Income

Adam Fayed, an expat wealth-management specialist, says:

As an expat wealth-management specialist, I have worked with many individuals in the U.S. to manage their year-end tax planning.

One of my top tips I always give clients is to make sure to maximize deductions wherever possible. Specifically, look into ways that you can lower taxable income by utilizing things like:

- Retirement accounts and other investments

- Charitable donations

- Maximizing employer benefits, such as health insurance premiums

Even moving expenses for qualified opportunities—transfers between jobs separated by more than 50 miles—qualify.

You can find out more about Adam on his website: AdamFayed.com.

Opportunities for next year

Tax deductions can be vastly different for many people, depending on each person’s specific situation. Next year, you can get a handle on your tax situation by sitting down with your tax advisor and asking their advice.

For best results, do not ask tax planning questions in the middle of tax season. Rather, wait until May or later (many CPAs and accountants take a well-deserved break after the tax filing deadline).

Come prepared with specific questions, especially about tax impacts of future decisions that you might be pondering. This will show that you’re interested in your tax professional’s advice, instead of just wasting their time.

After you feel like you’ve had a productive meeting, wrap it up by asking: “What else am I missing?”

What to do if you can’t take advantage of this opportunity

Some taxpayers might not itemize tax deductions on Schedule A of their federal tax return. And if that’s you, then you might look at taking advantage of one of the other tax planning opportunities here.

But if you feel like you’ve done everything possible (and your tax advisor agrees), then congratulations! Now, stop worrying about taxes and do something that you enjoy! Just don’t lose the momentum next year!

Tax Tip #3: Accelerate Deductible Expenses

To take Tip #2 one step further, you may decide to accelerate certain tax deductions into the current year. This might be better in certain circumstances than in others.

For example, you may choose to accelerate deductible expenses if you’re in a higher tax bracket this year than you will be next year. Conversely, you may choose to defer certain tax deductions if you’re in a lower tax bracket now than you will be next year.

Lori Shao is the founder and CEO of Finli, a digital back office platform for small businesses. She says:

The best year-end tax planning tip I would recommend for individuals in the U.S. is to accelerate deductible expenses. This means paying certain deductible expenses before the end of the year, such as:

- State and local taxes

- Mortgage interest

- Charitable contributions

It can help you reduce your taxable income for the year and lower your tax bill.

Tax Tip #4: Donate to Charities for Tax Deductions

Speaking of charitable contributions, people who itemize tax deductions have several options available to them. Ricardo Ferrer, CFO of Culture.org, says:

One of the easiest ways to reduce tax is to donate to charities. Most of the time, there are special tax deductions when donating to charitable organizations.

By deducting the charitable donation amount from the donor’s gross income, the tax reduction reduces the amount of income that is required to be paid in taxes. The amount of the tax reduction is dependent upon the donor’s tax rate and the applicable tax rules.

This may set restrictions on the percentage of income that can be deducted or impose that the beneficiary organization meet legal criteria to be considered a charitable organization.

One thing to keep in mind is that you must itemize your tax deductions on your tax return to take advantage of charitable contributions, warns Meredith Lepore, editor & writer for Credello, an AI-driven fintech product company.

Opportunities for next year

If you’re charity-minded, talk to your tax advisor or your financial planner about ways to incorporate charitable gifting into your investment and tax planning strategy.

Here are a couple of concepts that your tax or financial professional should be able to discuss with you:

Gifting appreciated securities

Many people use cash to contribute to charity. However, you generally have to pay taxes to come up with that cash, regardless of where it came from. That’s tax inefficient.

Instead, you may consider gifting appreciated securities, such as stocks or mutual funds, from a taxable investment account. As long as your gift goes towards a qualified charity, then you get the full benefit of the tax deduction without paying any capital gains tax (or any income tax at all).

In other words, more bang for your buck.

Keep in mind that you can’t just bring paper stock certificates to your local church and put them in the collection plate. You’ll have to make sure that the charity can accept your donation through a brokerage firm.

But if it’s a public charity, then it probably will be able to accept your donation.

Establishing a donor-advised fund

To take donating appreciated securities one step further, you can establish a donor-advised fund. This allows you to put the securities into an investment account managed by a brokerage firm, such as Vanguard or Fidelity.

From there, you can direct a certain portion of the account balance to go to the qualified charity of your choice each year. You can change your selection from year to year, as well.

This can be a great opportunity to take tax deductions now, while allowing the securities to continue growing for future gifting opportunities.

Qualified charitable distributions

If you’re age 70 1/2 or older, you can contribute directly to a charity from your individual retirement account (IRA). This is known as a qualified charitable distribution, or QCD.

You don’t pay taxes on this withdrawal, as long as it is a check from your IRA directly to the charity. See your investment advisor or brokerage firm for specific details for your account. Generally, QCD checks must clear prior to December 31 of the year in question.

If you’re age 73 or older, you may have to take an annual required minimum distribution (RMD) from your traditional IRA. Fortunately, your QCD counts towards your RMD for the year.

For example, if your RMD for a given tax year is $50,000, and you had planned to gift $10,000 to charity, then you can do the following:

- Write a $10,000 check to the charity from your IRA (tax free)

- Take the remaining $40,000 as your RMD for the year (subject to income tax)

You could even write a check for the full $50,000 without having to pay any taxes! QCDs are limited to $100,000 per person, per year.

Tax Tip #5: Implement a Tax-Loss Harvesting Strategy

Tax-loss harvesting involves purposely selling some investments to create a taxable loss. This can help offset capital gains tax on other investments, or it can be used to offset ordinary income, subject to an annual limit. Any unused capital losses can be carried forward to future tax years.

Let’s hear what Susannah Harmon, a VP at CarTitleLoans123, has to say:

As the VP of Finance for a collateral-based loan company, one strategy I personally love is tax-loss harvesting.

Tax-loss harvesting involves reviewing your investment portfolio and selling investments that have incurred losses. By doing so, you can offset capital gains and potentially reduce your taxable income. This can be especially valuable if you have investments in stocks or other assets that have declined in value during the year.

Additionally, you can use any excess losses to offset up to $3,000 of your ordinary income, which can lead to a lower tax liability. Keep in mind that this strategy should be approached with care to ensure it aligns with your overall financial goals and risk tolerance. Consulting with a financial advisor or tax professional is advisable to make the most of this tax planning tip.

By strategically managing your investment losses, you can optimize your tax situation, potentially reducing your tax burden and keeping more of your hard-earned money.

Opportunities for next year

Incorporate tax-efficiency into your investment decision-making.

If you work with an advisor, make sure that your advisor is aware that you want to save money on taxes, and that their investment approach isn’t costing you a ton of money.

If you feel that they’re not paying attention to your wishes, then fire your advisor. There are too many tax-savvy financial advisors who can help you make sound financial decisions and save on your federal taxes.

If you like to DIY your finances, then robo-advisors, such as Betterment and Wealthfront do a great job of tax-loss harvesting as part of their rebalancing strategy.

Tax Tip #6: Maximize Retirement Account Contributions

The end of the year provides many people to evaluate their retirement account contributions to make sure they take complete advantage of the tax benefits. This can include:

- Maximizing IRA contributions

- Making catch-up contributions (for taxpayers age 50 and older)

- Maxing out pre-tax contributions in their workplace retirement plan

Here’s more guidance from Lee Hemming, sales director at ABC Finance Limited:

One year-end tax-planning tip I recommend for individuals in the U.S. is to maximize contributions to tax-advantaged retirement accounts, such as a 401(k) or a traditional IRA.

Contributing the maximum to either tax-deferred account can reduce your taxable income for the year and help you save for retirement.

For 2023, the maximum 401(k) contribution limit is $21,000 for those under 50 and $27,000 for those 50 and older, while the IRA contribution limit is $6,000 for those under 50 and $7,000 for those 50 and older.

By contributing the full amount, you not only build your retirement savings but also potentially lower your tax liability for the current year. However, be sure to consult a tax professional or financial advisor to ensure that this strategy aligns with your specific financial situation and goals.

Opportunities for next year

If you don’t have enough money to fill up your retirement accounts this year, you can contribute to your IRA up until the tax filing deadline, and have your contribution count for the 2023 tax year.

Beyond that, you can take a look at your workplace retirement plan and make sure to:

- At least contribute enough to get the matching contribution (which most plans offer) throughout the tax year

- Set aside part of your future salary increases and bonuses towards increasing your retirement plan contributions

If you’ve maxed out your retirement plan contributions and still have money left over, then start a taxable investment account. As you build your investment account, you will be more able to incorporate tax-loss harvesting as part of your tax planning strategy (See Tax Tip #5).

Tax Tip #7: Leverage Health Savings Accounts

If your workplace offers, putting money towards a health savings account (HSA) can be a great thing.

HSAs have a triple tax benefit:

- Contributions are pre-tax. Pre-tax contributions mean that they reduce your taxable income, dollar for dollar.

- Earnings grow tax-deferred. This means that you don’t pay taxes on the money in your HSA, regardless of what investments you have.

- Qualified withdrawals are tax free.

Here are some more thoughts from Abid Salahi, co-Founder and CEO at FinlyWealth, a technology firm that uses AI to help people select credit cards:

In the ever-evolving tech world, change is the only constant, and the same applies to year-end tax planning. As a tech CEO, one uncommon yet effective tip I’d recommend is to utilize Health Savings Accounts (HSAs).

Individuals with high-deductible health plans can make tax-deductible contributions to HSAs. The distributions for qualified medical expenses from this account are tax-free, providing twin advantages.

It’s a smart way to guard your health and finances, cutting down your taxable income. Yet, discuss with a tax professional first to make sure it suits your situation.

What to do if you can’t take advantage of this opportunity

If your company doesn’t offer HSAs, or if you can’t find the right high deductible health plan for your situation (a requirement for HSAs), then take a closer look at the benefits that your company does offer. Here are some examples:

- Flexible spending accounts (FSAs): A flexible spending account allows the employee to contribute pre-tax money towards an account that they can use for specific benefits. Benefits might include:

- Dependent care assistance

- Health benefits

- Vision & dental coverage

- Adoption assistance: Some companies offer adoption benefits for employees who choose to adopt. Although you may be able to exclude adoption-related expenses from your income, you’ll need to file IRS Form 8839, Qualified Adoption Expenses, with your tax return

Tax Tip #8: Use Annual Gift Tax Exclusion

John Ross, CEO of Test Prep Insight, says:

For older Americans looking to transfer wealth to their children or grandchildren, make the most of your annual gift tax exclusion. Every year, you can give up to $17,000 to another person without even having to file a gift tax return.

This means a couple can collectively gift up to $34,000 without tax implications. Thus, if you’re trying to help out your kids or grandkids, don’t waste your annual gift allowance.

Spread your gifts out over many years and transfer this wealth without the need for gift-tax returns or long-term implications. As the year closes out, consider a Christmas gift to make use of your gift rights under the tax code.

Opportunities for next year

If gift tax (or estate tax) is a long-term concern, then create a long-term estate plan to account for it. Your estate plan should include a wealth distribution component, which can help you strategically plan for:

- Where your wealth should ultimately go

- How your wealth is distributed

- Minimizing tax liability associated with your wealth

One overlooked tax liability aspect has to do with inherited IRAs, where beneficiaries must follow certain tax rules. We’ll cover this in the next tax tip.

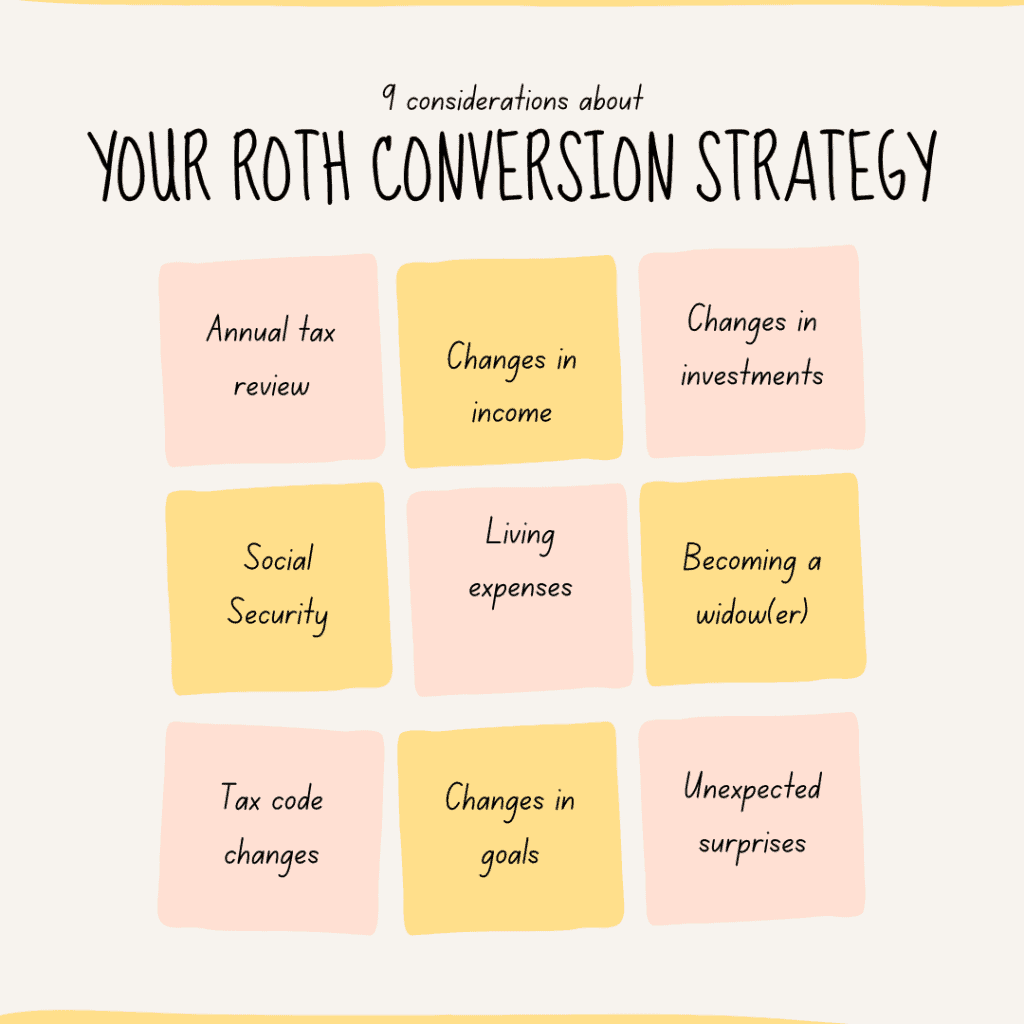

Tax Tip #9: Consider Roth conversions

If you have a significant amount of wealth tied up in pre-tax accounts, then you may consider creating a Roth IRA conversion strategy.

Having a Roth IRA conversion strategy will allow account holders to make strategic Roth conversions on an annual basis. Done correctly, this approach allows people to remain in a lower tax bracket and pay lower tax rates over a longer period of time than if they tried to do massive Roth conversions over a short period of time.

A successful Roth conversion strategy can help:

- Reduce the likelihood of RMDs down the road (or reduce the amount of RMDs you have to take)

- Keep a lower taxable income for Medicare purposes

- Provide tax-free inherited Roth IRAs for beneficiaries

While we’ve written a series of articles about Roth conversion strategies, the best advice would be to consult your tax professional or investment advisor to get started.