IRS Form 8839 Instructions

For adoptive families who incurred certain qualified expenses in the adoption of a child, the Internal Revenue Service may allow a tax credit on your federal tax return on IRS Form 8839. Likewise, if you received employer-provided adoption benefits, you may be able to exclude the value of those benefits from your taxable income.

In this article, we’ll go over how you can use IRS Form 8839 to claim adoption tax benefits, as well as some

Table of contents

How do I complete IRS Form 8839?

There are three parts to IRS Form 8839, Qualified Adoption Expenses:

- Part I: Information About Your Eligible Child or Children

- Part II: Adoption Credit

- Part III: Employer-Provided Adoption Benefits

Let’s go over each part, step by step, starting with Part I.

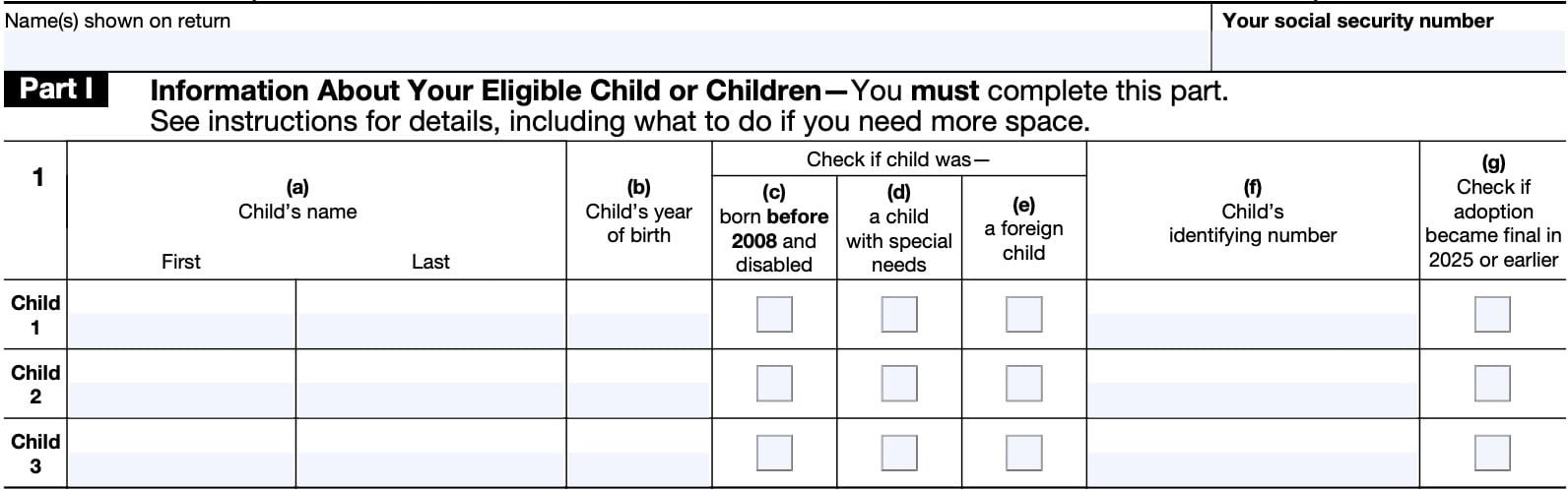

Part I: Information about your eligible child (or children)

All taxpayers must complete Part I, whether claiming a tax credit for eligible adoption expenses or excluding employer-provided benefits from your tax bill.

At the top of Part I, you’ll enter the taxpayer’s name and Social Security number as shown on your individual tax return.

For each child, you’ll enter the necessary information in the following manner:

Column (a)

Enter the first name and last name of the child.

Column (b)

Enter the child’s date of birth.

Column (c)

Check the box if the child was born before 2006 and is considered to be disabled. According to the IRS instructions, a disabled person is one who is physically or mentally unable to care for himself or herself.

A disabled person can be an eligible child regardless of his or her age at the time of adoption.

Column (d)

Check the box in column (d) if this child is a special needs child.

Special needs

The IRS considers a special needs child as one who meets all three of the following conditions:

- The child was a citizen or resident of the United States or its possessions at the time the adoption effort began.

- A state has determined that the child can’t or shouldn’t be returned to his or her parents’ home. This includes the District of Columbia.

- The state has determined that the child won’t be adopted unless assistance is provided to the adoptive parents.

States may use the following criteria to determine whether a child will be adopted without assistance:

- The child’s ethnic background and age,

- Whether the child is a member of a minority or sibling group, and

- Whether the child has a medical condition or a physical, mental, or emotional handicap.

Column (e)

Check this box if the child was considered to be a foreign child. A child is a foreign child if he or she wasn’t a citizen or resident of the United States or its possessions at the time the adoption effort began.

Special rules

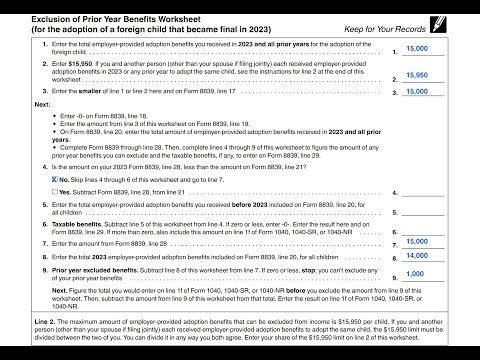

For the adoption of a foreign child that became finalized in the tax year, taxpayers may be able to exclude part of all of those employer-paid benefits from gross income. To make this determination, complete the Exclusion of Prior Year Benefits Worksheet, located in the form instructions.

Watch this video for step by step guidance on completing the exclusion of prior year benefits worksheet, located in the form instructions.

Column (f)

Enter the child’s identifying number in this column. An identifying number may be any of the following:

- Social Security number (SSN)

- Individual Taxpayer Identification Number (ITIN)

- Adoption Taxpayer Identification Number (ATIN)

You may apply for a Social Security number by filing Form SS-5, Application For Social Security Card. If you cannot get the child’s SSN before filing the income tax return, you may have to file one of the following:

- IRS Form W-7A to obtain an ATIN (if the child is a U.S. citizen or resident)

- IRS Form W-7 to obtain an ITIN (if the child is not a U.S. citizen or resident)

Column (g)

Check the box in column (g) if the adoption was finalized during the tax year or in a prior year.

More than three eligible children

In Line 1, there are spaces for up to three children.

If you have more than three adopted children for whom you are trying to claim a tax credit, you may use more than one Form 8839. In this scenario, simply write, “See attached” on the lower right-hand side of the Caution box, below Line 1.

After completing Part I, you’ll proceed to either Part II or Part III. If you paid qualifying adoption expenses and need to claim a tax credit, go to Part II. If you did not incur adoption expenses, but your employer provided benefits, go to Part III.

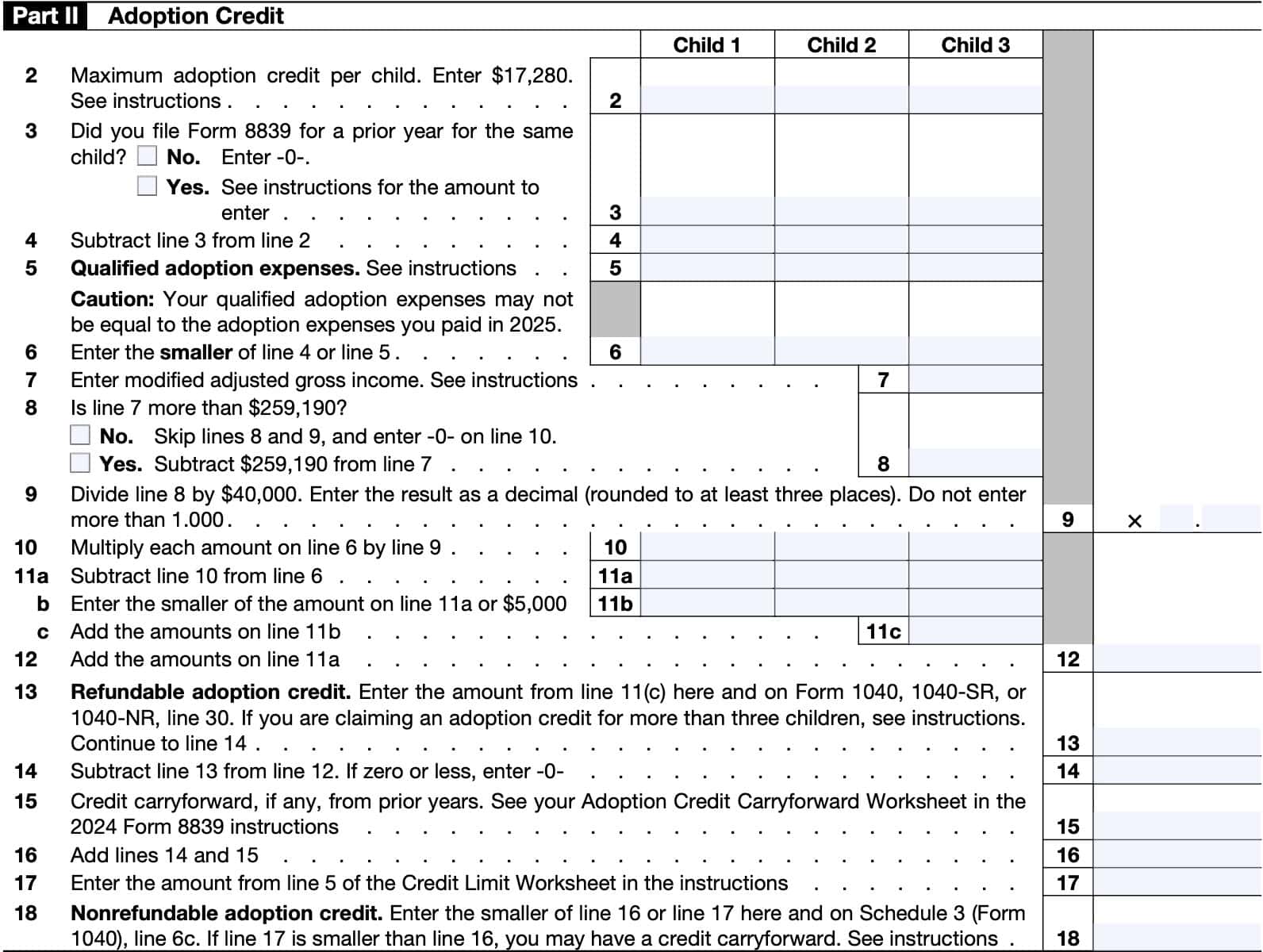

Part II: Adoption Credit

In Part II, we’ll calculate the adoption credit that you may take for each child.

In 2025, the maximum amount of the credit that you can take for the legal adoption of an eligible child is $17,280 per child.

For 2026, the maximum adoption credit is $17,670.

Line 2: Maximum adoption credit per child

In Line 2, the maximum credit amount for each child, unless you and another person (besides your spouse filing a joint return) each paid adoption-related expenses for the same child.

Two taxpayers claiming the adoption tax credit for the same child

In this case, you must divide the amount of the credit between yourself and the other taxpayer. You may divide this in any manner, as long as you both agree to the amount that each person can claim, and as long as the total amount does not exceed the maximum amount.

Line 3

If you did not file Form 8839 last year for the same child, select No and move to Line 4.

If you filed Form 8839 in one or more previous years, enter the total of the amounts shown on Lines 3 and 6 (or corresponding line) of the last form you filed for the child.

Line 4

If you selected Yes in Line 3, subtract Line 3 from Line 2. Otherwise, carry the amount down from Line 2.

Line 5: Qualified adoption expenses

On Line 5, enter the total qualified adoption expenses you paid in:

- 2024 if the adoption wasn’t final by the end of 2025,

- 2024 and 2025 if the adoption became final in 20235, or

- 2025 if the adoption became final before 2025.

Note: Your qualifying adoption expenses may not be the same amount as the adoption-related expenses actually paid in 2025.

Qualified adoption assistance program

If you incurred expenses that were reimbursed by your employer under a qualified adoption assistance program, you do not need to pay federal income tax on the reimbursement. However, you cannot claim a federal tax credit for reimbursed expenses under a qualified adoption program.

In other words, you may choose to exclude expenses from your income, or use the same expenses to claim a tax credit that will reduce your federal income tax liability. But you cannot do both.

Line 6

In Line 6, enter the smaller of:

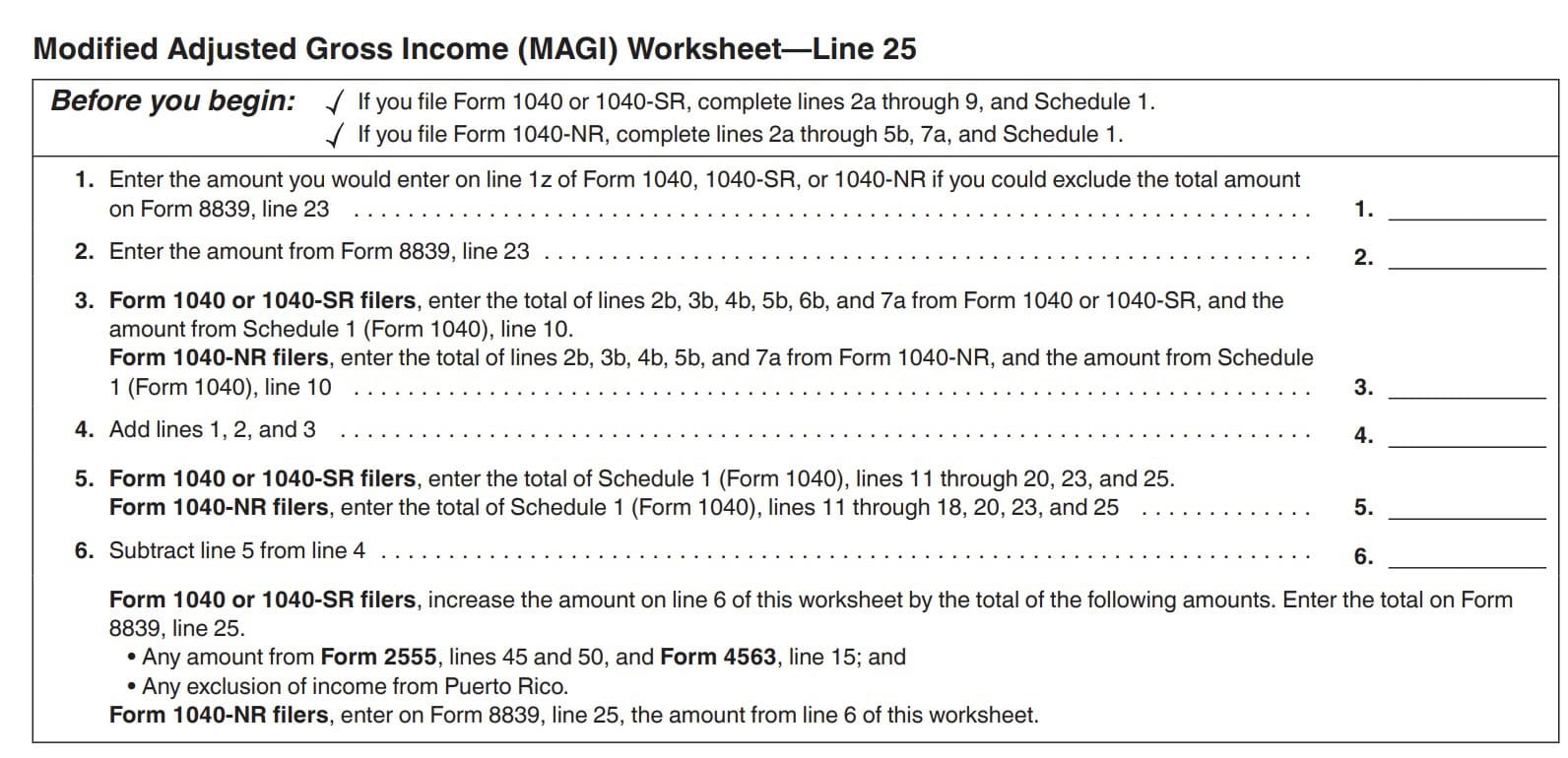

Line 7: Modified adjusted gross income

Enter your modified adjusted gross income. This includes your adjusted gross income from Line 11 of your Form 1040, Form 1040-SR, or Form 1040-NR, plus the following:

- Exclusion of income from Puerto Rico

- Amounts from IRS Form 2555, Lines 45 and 50; and

- Amount excluded from income by residents of American Samoa filing IRS Form 4563, Line 15

Line 8

Check the appropriate box.

If your modified adjusted gross income is more than $259,190, then subtract $259,190 from the number in Line 7.

If your MAGI is less than the phaseout threshold

For eligible taxpayers with modified adjusted gross incomes of $259,190 or less, you are below the phaseout threshold and that you can take the full benefit of the credit this year.

Skip Lines 8 and 9, enter ‘0’ on Line 10, then go to Line 11.

Line 9

In Line 9, divide the amount in Line 8 by $40,000.

This should result in a decimal value, which you can round to three places. Do not enter a number that exceeds 1.000.

If the number that you enter is 1.000, then your modified adjusted gross income exceeds the income limits for claiming the adoption tax credit for. However, you may be able to carry forward any unused credit for paid qualified adoption expenses from previous tax years.

Line 10

Multiply each amount on Line 6 by the decimal value on Line 9.

Line 11

There are several line entries for each column in Line 11.

Line 11a

In each column, subtract Line 10 from Line 6.

Line 11b

Enter the smaller of Line 11a or $5,000.

Line 11c

Add the amounts on Line 11b, then enter the total in Line 11c.

Line 12

Add the amounts on Line 11a, then enter the total in Line 12.

Line 13: Refundable adoption credit

Beginning in 2025, up to $5,000 of the adoption credit is refundable. The refundable credit amount is determined per eligible child. The amounts per child are then added together for a total, refundable credit amount.

This means that depending on the amount of qualified adoption expenses, if you have more than one eligible child with qualified adoption expenses, the refundable credit amount may be different for each child.

You will figure the refundable credit amount for each eligible child on Lines 11a and 11b, add the credit amounts for a total on Line 11c, then report the total refundable credit amount on Line 13.

Enter the amount from Line 11(c) here and on Form 1040, 1040-SR, or 1040-NR, Line 30.

If you are claiming an adoption credit for more than three children, you may need to add additional sheets with the required information for each child.

Line 14

Subtract Line 13 from Line 12, then enter the result here.

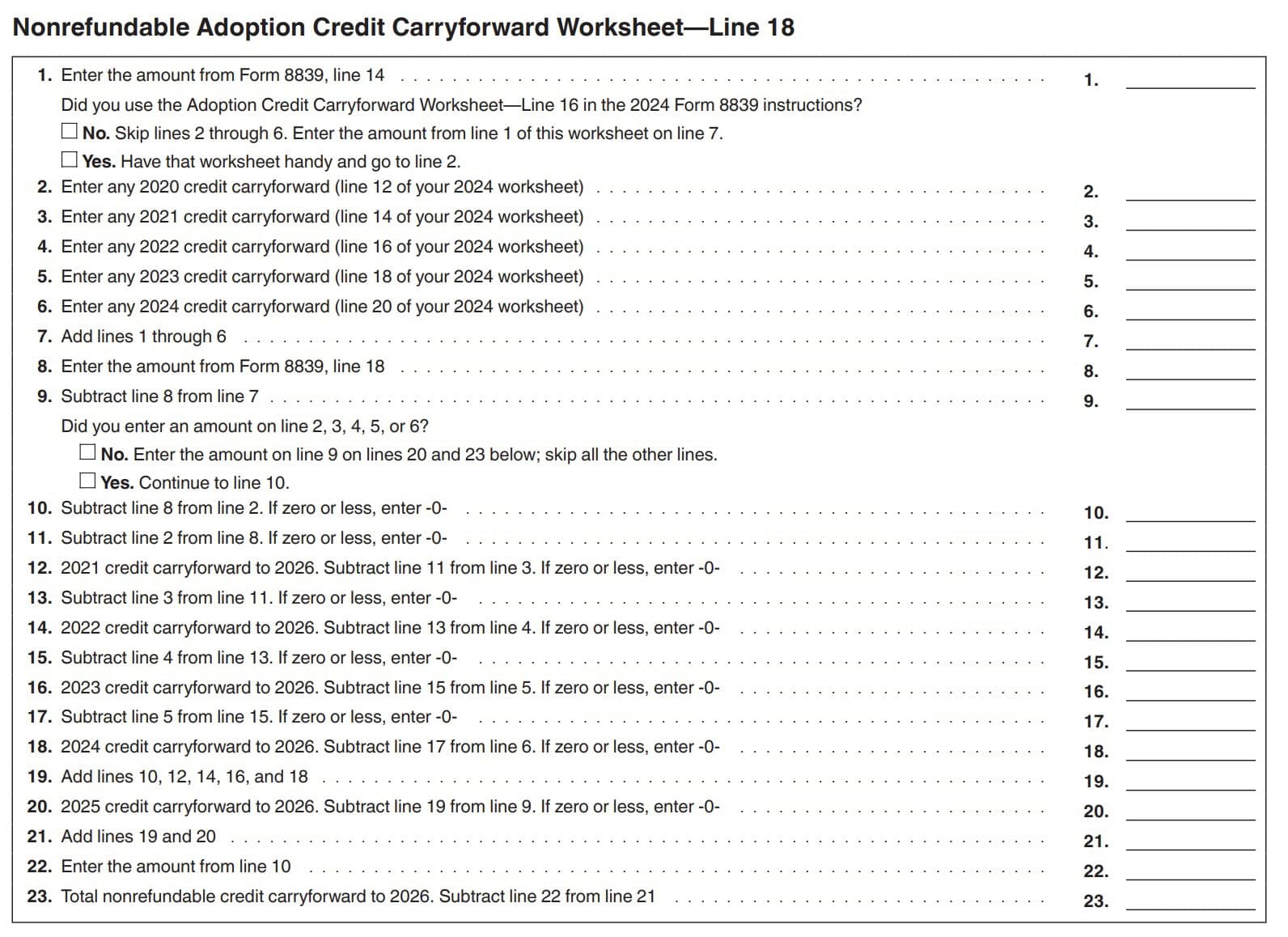

Line 15: credit carryforward

Enter the credit carryforward, if any, from prior years. See your Adoption Credit Carryforward Worksheet in the 2024 Form 8839 instructions

Line 16

Add Lines 14 and 15. Enter the result here.

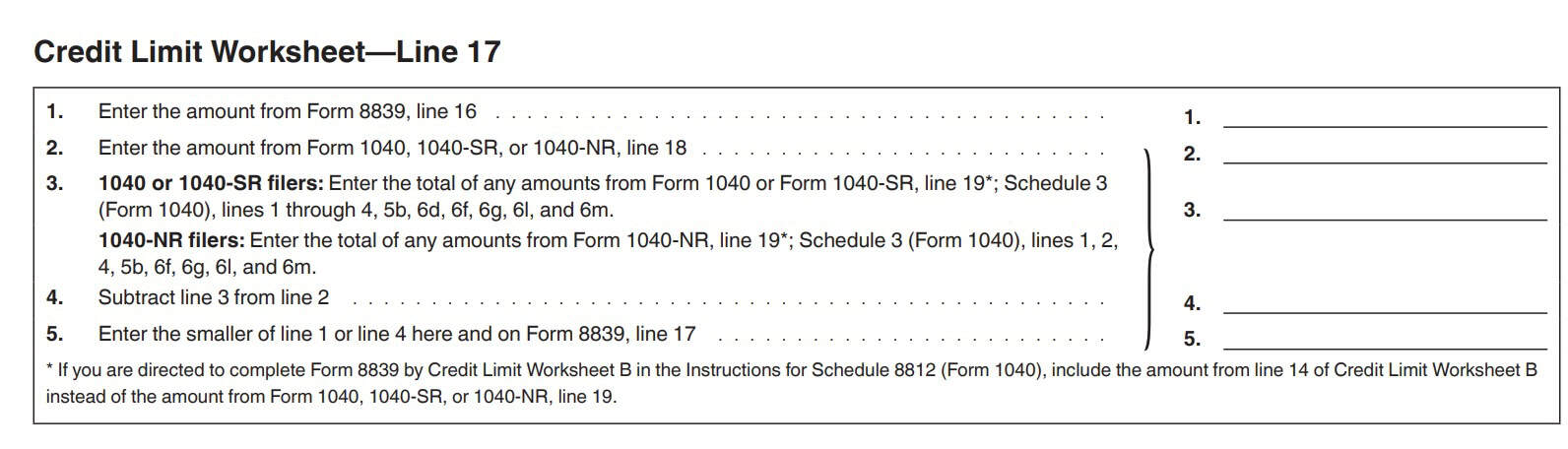

Line 17

Enter the amount from Line 5 of your Adoption Credit Limit Worksheet here.

Calculating the Adoption credit limit

To determine the adoption credit limit, you’ll need to complete these steps in the credit limit worksheet:

- Enter the amount from Line 16

- Enter the amount from Line 18 on any of the following:

- IRS Form 1040

- IRS Form 1040-SR

- IRS Form 1040-NR

- Form 1040 or Form 1040-SR filers: Enter the total of any amounts from the following:

- IRS Form 1040 or Form 1040-SR, Line 19 (Child tax credit or credit for other dependents from Schedule 8812)

- Schedule 3, Line 1 (Foreign tax credit, claimed on IRS Form 1116)

- Schedule 3, Line 2 (Child and dependent care expenses on IRS Form 2441)

- Schedule 3, Line 3 (Education credits on IRS Form 8863)

- Schedule 3, Line 4 (Retirement savings contribution credit on IRS Form 8880)

- Schedule 3, Line 5b (Residential clean energy credit on IRS Form 5695)

- Schedule 3, Line 6d (Credit for the elderly or disabled on Schedule R)

- Schedule 3, Line 6f (Clean vehicle credit from IRS Form 8936)

- Schedule 3, Line 6g (Mortgage interest credit from IRS Form 8396)

- Schedule 3, Line 6l (Amount on IRS Form 8978, Line 14)

- Schedule 3, Line 6m (Credit for previously owned clean vehicles from Form 8936)

- Form 1040-NR filers: Enter the total of the following amounts:

- IRS Form 1040-NR, Line 19

- Schedule 3, Line 1 (Foreign tax credit, claimed on IRS Form 1116)

- Schedule 3, Line 2 (Child and dependent care expenses on IRS Form 2441)

- Schedule 3, Line 4 (Retirement savings contribution credit on IRS Form 8880)

- Schedule 3, Line 5b (Residential clean energy credit on IRS Form 5695)

- Schedule 3, Line 6f (Clean vehicle credit from IRS Form 8936)

- Schedule 3, Line 6g (Mortgage interest credit from IRS Form 8396)

- Schedule 3, Line 6l (Amount on IRS Form 8978, Line 14)

- Schedule 3, Line 6m (Credit for previously owned clean vehicles from Form 8936)

- Subtract Line 3 from Line 2 in the worksheet.

- Enter the smaller of Line 1 or Line 4 here, and on Line 17 of Form 8839.

Line 18: Nonrefundable adoption credit

Enter the smaller of Line 16 or Line 17 here, and on Schedule 3, Line 6c, of your income tax return.

Tax credit carryforward

If Line 17 is smaller than Line 16, you may have an unused credit to carry forward to a future tax year.

To calculate your total tax credit carryforward, you’ll need to complete the Adoption Credit Carryforward Worksheet for Line 18. Follow the steps outlined below.

Be sure to keep a copy of this worksheet for next year.

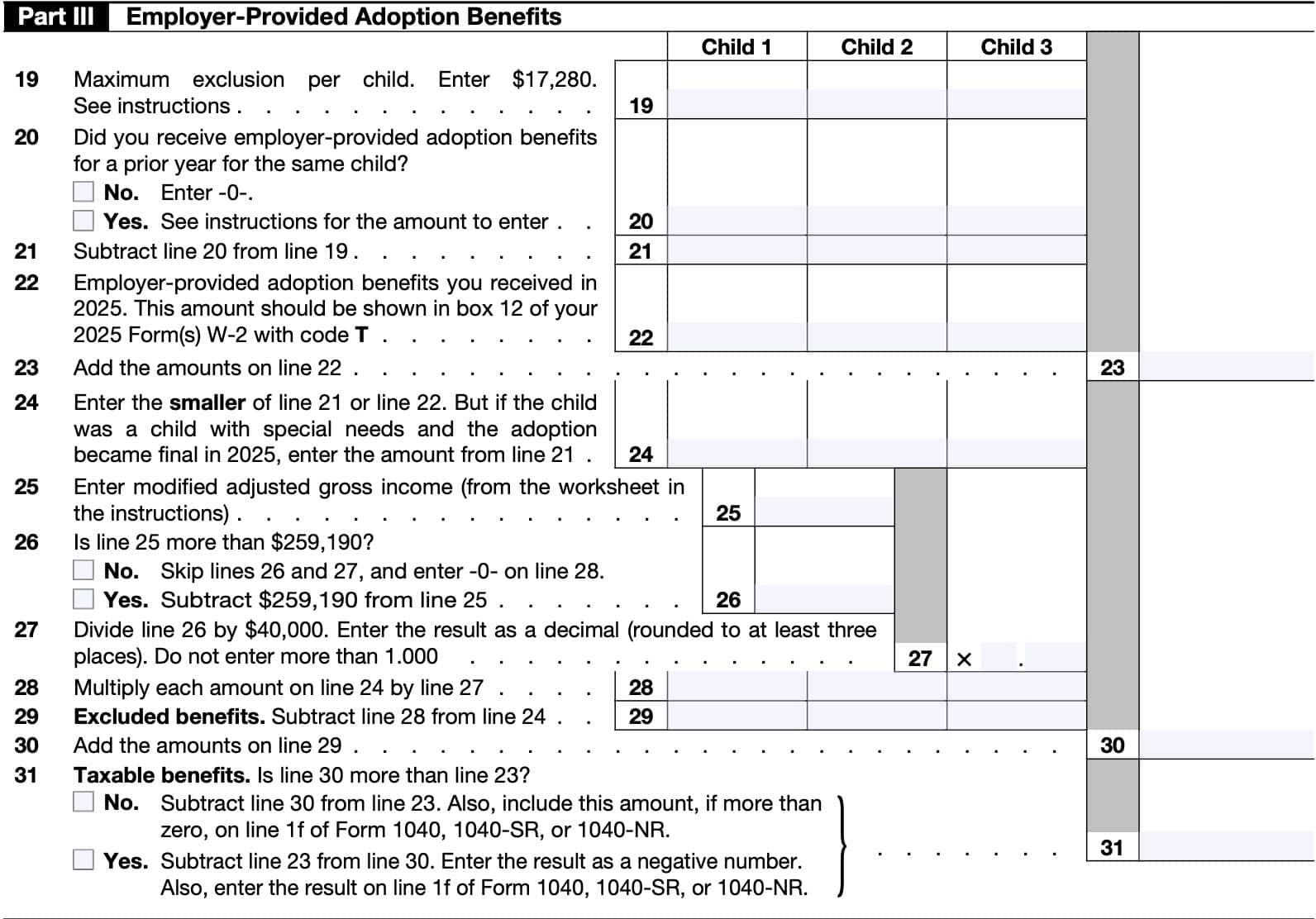

Part III: Employer-provided adoption benefits

If your employer funded some or all of the necessary expenses for the legal adoption of child, you may be able to exclude part or all of these expenses from your taxable income. In Part III, we’ll determine how much of these necessary costs you can exclude from taxable income for the given tax year.

The maximum amount of employer-paid adoption expenses that you can exclude from income is the same as the maximum adoption tax credit:

- 2025: $17,280 per qualifying child

- 2026: $17,670 per child

Line 19

In Line 19, enter the maximum exclusion dollar limit, unless you and another person (besides your spouse filing a joint tax return) each had employer-provided adoption expenses for the same child for the same child.

If you and another taxpayer each had employer-provided adoption assistance

In this case, you must divide the amount of the income exclusion between yourself and the other taxpayer. You may divide this in any manner, as long as you both agree to the amount that each person can claim, and as long as the total amount on both federal tax returns does not exceed the maximum exclusion.

Line 20: Did you receive employer-provided Adoption benefits in a prior year for the same child?

If you did not file Form 8839 last year for the same child, select ‘No’ and move to Line 21.

If you filed Form 8839 in one or more previous years, enter the total of the amounts shown on Lines 18 and 22 (or corresponding line) of the last form you filed for the child.

Line 21

If you selected ‘Yes’ in Line 20, subtract Line 20 from Line 19. Otherwise, carry the amount down from Line 19.

Line 22: Employer-provided adoption benefits received in the tax year

Enter the amount of employer-funded adoption benefits you received in the given tax year. You can find this amount in Box 12 of your Form W-2, with code T.

Line 23

Add the amounts for each qualifying child on Line 22, then enter the total on Line 23.

Line 24

For each column, enter the smaller of:

However, if the child was a child with special needs and the legal adoption of the child became finalized during the tax year, enter the amount from Line 21.

Line 25: Modified adjusted gross income

Enter the modified adjusted gross income as calculated using the worksheet from the form instructions (see below)

Line 26

If the amount from Line 25 does not exceed $259,190, then you may be eligible for the maximum exclusion with no phaseout.

In this case, skip Lines 26 and 27, enter ‘0’ on Line 28, and proceed to Line 29.

If the amount in Line 25 does exceed $259,190, then subtract $259,190 from the number in Line 25 and enter the result here.

Proceed to Line 27.

Line 27

In Line 27, divide the amount in Line 26 by $40,000.

This should result in a decimal value, which you can round to three places. Do not enter a number that exceeds 1.000.

Line 28

Multiply each amount in Line 24 by the decimal value in Line 27.

Line 29: Excluded benefits

Subtract Line 28 from Line 24. This represents the benefits that are excluded from taxable income.

Line 30

Add the excluded benefits on Line 29 and enter the total on Line 30.

Line 31: Taxable benefits

If the answer is No, then subtract Line 30 from Line 23. Include this amount, if greater than zero on Line 31 and Line 1f of IRS Form 1040, Form 1040-SR, or Form 1040-NR.

If the answer is Yes, then subtract Line 23 from Line 30. Include this amount as a negative number on Line 31 and Line 1f of Form 1040, Form 1040-SR, or Form 1040-NR.

Video walkthrough

Watch this instructional video to go through IRS Form 8839, step by step.

Are you tired of dreading tax season?

If you’re like most people, you push through the stress of filing, only to be hit with a bigger bill than expected—then put it all behind you until the same cycle repeats next year.

But what if you could change the game?

Tax planning puts you in control. It’s about being proactive, not reactive—taking small, smart steps throughout the year to reduce your tax burden, increase your savings, and keep more of your hard-earned money working for you.

Here’s what effective tax planning helps you do:

✅ Avoid the surprise of a high tax bill

✅ Understand how your income and decisions affect your taxes

✅ Strategically lower your tax liability over time

Ready to make smarter tax moves?

👉 Join my free weekly tax planning newsletter and get one actionable tip every week to help you reduce your taxes legally and effectively.

Start taking control—your future self will thank you.

Frequently asked questions

Below are some commonly asked tax questions about IRS Form 8839 and qualified adoption expenses.

In 2025, the maximum tax credit that you can claim for necessary adoption expenses is $17,280 per qualifying child. In 2026, the maximum credit is $17,670 per child.

In 2025, the maximum amount of employer funded adoption expenses that you can exclude from gross income is $17,280 per qualifying child. In 2026, the maximum exclusion amount is $17,670 per child.

Qualified adoption expenses are reasonable and necessary expenses directly related to, and for the principal purpose of, the legal adoption of an eligible child. These may include necessary adoption fees, attorney fees and court costs, travel expenses and re-adoption expenses if adopting a foreign child.

Examples of adoption costs that the IRS does not consider as qualified expenses include expenses for which you were reimbursed under a government program or by your employer, illegal expenses, or expenses for a surrogate arrangement or for adopting your spouse’s child.

You can claim both a tax credit for expenses that you incurred and an an income exclusion for expenses paid by your employer. However, you cannot claim a tax credit and an income exclusion for the same adoption expenses.

Where can I find a copy of IRS Form 8839?

You can find this tax form on the IRS website. For your convenience, we’ve enclosed the latest version of Form 8839 below.

Related tax articles

This tax form is one of the fillable tax forms provided by the Internal Revenue Service, to help taxpayers reduce their tax preparation costs. To see more forms like this, visit our free fillable tax forms page, where you’ll also find articles like this.

Unlike the IRS, our articles contain step by step instructions for each tax form, as well as video walkthroughs. You can also check out all of our videos by subscribing to our YouTube channel!