IRS Form W-2 Instructions

If you’re an employee, you are probably aware of what IRS Form W-2 is. It’s one of the most important tax forms for virtually every taxpayer, and one of the most difficult forms to understand.

In this article, we’ll help you understand everything you need to know about IRS Form W-2, including:

- What you should expect to see in each box on this form

- How this tax information will impact your income tax return

- When you should expect your Form W-2 and what to do if you do not receive it on time

Let’s start by breaking down this tax form, one step at a time.

Table of contents

IRS Form W-2 Instructions

In most of our articles, we walk you through how to complete the tax form. However, most readers will probably want to understand the information reported on their W-2 form, instead of how to complete it.

Before we start breaking down this form, it’s important to understand that there can be up to 6 copies of Forms W-2. Here is a break down of where all these different forms end up:

- Copy A: Social Security Administration

- Copy B: To be filed with employee’s income tax return

- Copy C: For employee’s tax records

- Copy D: For employer’s tax records

- Copy 1: For state, city, or local tax department

- Copy 2: To be filed with employee’s state, city, or local tax return

For employees who do not pay state, city, or local income tax, copies 1 and 2 are optional.

Let’s get into the form itself, starting with the lettered boxes on the left side of the form.

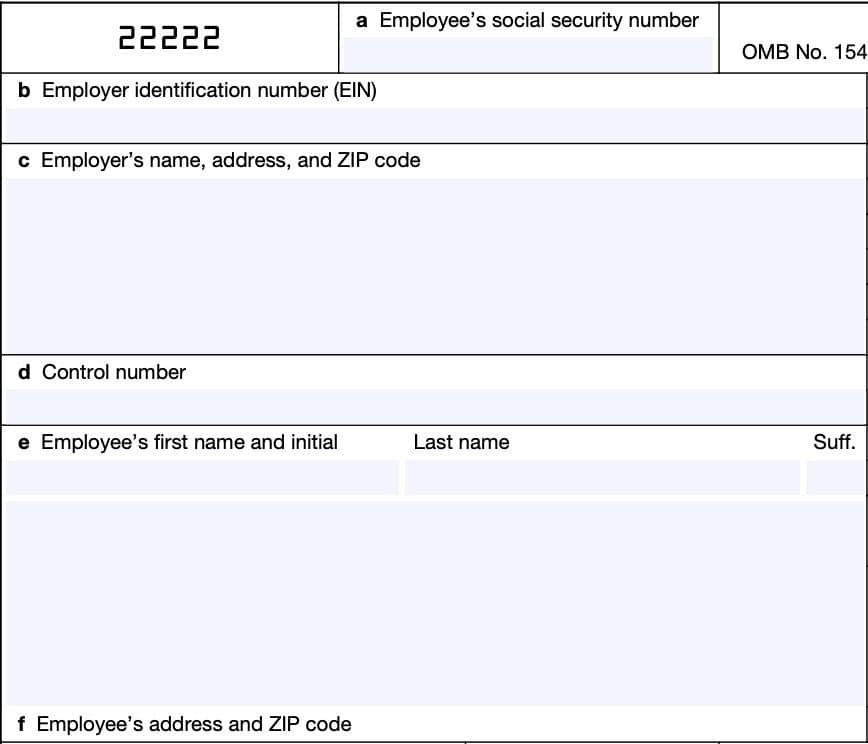

Boxes a through f

In these lettered boxes, you should see your employer’s tax record information and your personal information.

Review these for accuracy, to make sure that your earnings are properly reported to the Social Security Administration. Improperly reported Social Security earnings could impact your eventual Social Security retirement benefits.

Box a: Employee’s Social Security number

You should see your Social Security number (SSN) in Box a.

If you do not have a Social Security number, your employer may ask you to apply for one using Form SS-5, Application for a Social Security Card. If you applied for a Social Security card but have not received it by the time you receive your Form W-2, you may see ‘Applied For’ in this field.

For people who have a Social Security number, the Internal Revenue Service does not allow employers to enter an individual taxpayer identification number (ITIN) in this box.

Box b: Employer identification number (EIN)

You should see your employer’s EIN in Box b. If your employer has applied for an employer identification number but not yet received it, you may see ‘Applied For’ in Box b.

Box c: Employer’s name, address, and ZIP code

You should see your employer’s name, address, and ZIP code as they appear on other related tax forms:

- IRS Form 941, Employer’s Quarterly Federal Tax Return

- IRS Form 943, Employer’s Annual Federal Tax Return for Agricultural Employees

- IRS Form 944, Employer’s Annual Federal Tax Return

- IRS Schedule H, Household Employment Taxes

Box d: Control number

Employers may use this field to identify individual Forms W-2. However, this form is optional.

Box e: Employee’s name

Box e should contain your name as it appears on your Social Security card.

If your complete name does not fit in the allotted space, then you may only see your first and middle initials. However, your employer should report your complete last name, as this is the most important element in reporting your Social Security wages.

Box f: Employee’s address and ZIP code

Your complete mailing address should be listed in Box f.

Boxes 1 through 14: Federal tax information

Boxes 1 through 14 contain pertinent information for federal income taxes. We’ll cover exactly what should be reported in each box.

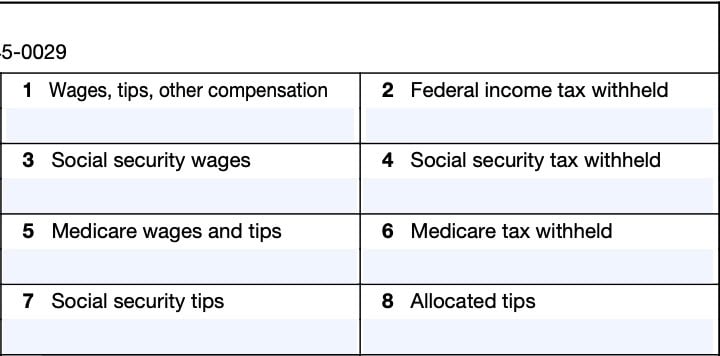

Box 1: Wages, tips, other compensation

In Box 1, your employer should report the total taxable, wages, tips, and other compensation that they paid to you during the tax year. Box 1 should not include elective deferrals, such as contributions to a 401k plan throughout the year.

Eligible compensation

Box 1 can contain the following:

- Total wages, bonuses, prizes, and awards paid during the taxable year, including signing bonuses

- Total non-cash payments, including certain fringe benefits

- Can report fringe benefits in Box 14

- Total tips reported by the employee to the employer

- Not including allocated tips

- Certain employee business expense reimbursements.

- The cost of accident and health insurance premiums paid by S-corporations

- For 2%-or-more shareholder-employees

- Taxable benefits from a Section 125 plan if the employee chooses cash.

- Employee contributions to an Archer MSA.

- Employer contributions to an Archer MSA if includible in employee income

- Employer contributions for qualified long-term care services provided through a flexible spending arrangement.

- Taxable cost of group-term life insurance over $50,000.

- Payments for non-job-related education expenses or payments under a nonaccountable plan.

- Up to $5,250 can be excluded if under an educational assistance program

- The amount includible as wages because your employer paid your share of Social Security and Medicare taxes (or RRTA taxes, if applicable).

- Designated Roth contributions made under a Section 401(k) plan, a Section 403(b) salary reduction agreement, or a governmental section 457(b) plan.

- Distributions to an employee or former employee from a non-qualified deferred compensation (NDQC) plan

- Amounts includible in taxable income under IRC Section 457(f) because amounts aren’t subject to substantial risk of forfeiture.

- Payments to statutory employees subject to Social Security and Medicare taxes but exempt from federal income tax withholding

- Cost of insurance protection under a compensatory split-dollar life insurance arrangement.

- Employee contributions to a health savings account (HSA).

- Employer contributions to an HSA if includible in employee’s income

- Amounts includible in income under IRC Section 409A from an NQDC

- Nonqualified moving expenses or reimbursements.

- Payments made to former employees on active duty in the Armed Forces or other uniformed services.

- Other compensation, including certain scholarship and fellowship grants

- Salary reduction contributions made to a Roth IRA as part of a SEP arrangement or SIMPLE IRA plan (Roth SEP IRA or Roth SIMPLE IRA)

Box 2: Federal income tax withheld

This box will show how much tax your employer withheld throughout the tax year.

If you received golden parachute payments, this amount will include the 20% excise tax withholdings for excess parachute payments.

Box 3: Social security wages

Box 3 indicates the total wages that were subject to Social Security tax, before any payroll deductions. However, this will not include Social Security tips or allocated tips.

Wages reported in Box 3 can include:

- Signing bonuses an employer pays for signing or ratifying an employment contract.

- Revenue Ruling 2004-109, 2004-50 I.R.B. 958 contains additional information

- Taxable cost of group-term life insurance over $50,000 included in Box 1.

- Reduced by any amount of life insurance premiums paid by the W-2 employee

- Cost of accident and health insurance premiums for 2%-or-more shareholder-employees paid by an S corporation

- Only if not excludable under IRC Section 3121(a)(2)(B)

- Employee and nonexcludable employer contributions to an MSA or HSA.

- Should not include employee contributions to an HSA that were made through a cafeteria plan.

- Employee contributions to a SIMPLE retirement account.

- Adoption benefits

- Adoption benefits paid from a Section 125 plan are subject to Social Security withholding

Box 4: Social security tax withheld

This box should show the total amount of Social Security tax that your employer withheld from your compensation, including tip income, during the calendar year.

For 2024, this amount should not exceed $10,453.20. This represents the Social Security wage base limit ($168,600) multiplied by the Social Security tax, which is 6.2%.

Box 5: Medicare wages and tips

The amount of Medicare wages and tips should be the same as the amount of Social Security wages and tips. However, there is no wage base limit for Medicare taxes.

Box 5 should contain the total amount of Medicare wages and tips. This should also include tips that you reported, even if your employer did not collect Medicare tax on those tips.

Box 6: Medicare tax withheld

Box 6 should contain the total employee Medicare tax your employer withheld during the tax year. This should also include any Additional Medicare Tax you may need to report on IRS Form 8959.

Box 7: Social Security tips

This box will contain the tips that you reported to your employer, even if your employer did not have enough funds to collect the Social Security tax on these tips.

The total of Box 3 and Box 7 should not exceed the maximum Social Security wage base for the year, which is $168,600 for the 2024 tax year.

Box 8: allocated tips

If you work for a large food and beverage establishment, your employer may have to calculate allocated tips on IRS Form 8027.

If applicable, allocated tips will only appear in Box 8, and not elsewhere on the Form W-2 tax form.

Box 9

Blank.

Box 10: Dependent care benefits

If you received dependent care benefits under a dependent care assistance program, your employer will report the total fair market value of daycare provided in Box 10.

This will include all amounts paid or incurred, regardless of any employee contributions. This might include:

- Fair value of benefits provided in kind by your employer

- Amounts paid directly to a day care facility by the employer or reimbursed to you to subsidize the benefit, or

- Benefits from the pre-tax contributions you made under a cafeteria plan or flexible spending acocunt

This will include any amounts over your employer’s plan’s exclusion in Box 1, Box 3, or Box 5. IRS Publication 15-B contains additional details.

Box 11: Nonqualified plans

Your employer will report employee distributions from a nonqualified plan or nongovernmental deferred compensation plan here, as well as in Box 1. Governmental deferred compensation plan distributions will be reported on IRS Form 1099-R, not on your Form W-2.

The Social Security Administration uses Box 11 to determine if any part of the amount reported in Box 1 or Boxes 3 and/or 5 was earned in a prior tax year. The SSA uses this information to verify that they have properly applied the Social Security earnings test and paid the correct amount of benefits.

Box 12: Codes

Box 12 contains specific IRS codes related to special items not reported elsewhere on your Form W-2. There are up to 4 boxes, which can contain up to 4 coded items.

If there are more than 4 coded items, you may receive an additional Form W-2 reporting the additional items.

Below is a summary of each code, and what it means.

Code A: Uncollected Social Security or RRTA tax on tips

This will indicate any Social Security or RRTA tax on tip income that your employer did not collect because you did not have enough funds from which to deduct it.

Your employer should not include this amount in Box 4.

Code B: Uncollected Medicare tax on tips

Code B indicates any Medicare tax on tip income that your employer did not collect because you did not have enough funds from which to deduct it.

Your employer should not include this amount in Box 6.

Code C: Taxable cost of group-term life insurance over $50,000

This would show the taxable cost of group-term life insurance coverage over $50,000 provided to you. This amount is also included in:

- Box 1

- Box 3 (up to the Social Security wage base)

- Box 5

Code D: Elective deferrals under a Section 401(k) cash or deferred arrangement plan

This represents employee 401(k) contributions. Will also show deferrals under a SIMPLE retirement account that is part of a Section 401(k) arrangement.

Code E: Elective deferrals under a Section 403(b) salary reduction agreement

This represents employee 403(p) contributions.

Code F: Elective deferrals under a Section 408(k)(6) salary reduction SEP

This represents employee contributions to a Section 408(k)(6) plan, also known as a SARSEP.

Code G: Elective deferrals and employer contributions to any governmental or nongovernmental Section 457(b) deferred compensation plan

Should not include any amounts that are subject to a substantial risk of forfeiture.

Code H: Elective deferrals under Section 501(c)(18)(D) tax-exempt organization plan

These will also be included in Box 1 as wages.

Be sure to deduct this amount from your IRS Form 1040 or Form 1040-SR.

Code J: Nontaxable sick pay

This will show any sick pay that was paid by a third party and was not includible in income because you contributed to the sick pay plan. No amounts should be shown in:

- Box 1

- Box 3

- Box 5

This should not include nontaxable disability payments made directly by a state.

Code K: 20% excise tax on excess golden parachute payments

If your employer made excess golden parachute payments because you are a key corporate employee, Code K will report the 20% excise tax on these payments.

If the excess payments are considered to be wages, your employer will also report the 20% excise tax withheld as income tax withheld in Box 2.

Code L: Substantiated employee business expense reimbursements

Your employer should use this code only if:

- You were reimbursed for employee business expenses using a per diem or mileage allowance, and

- The amount that reimbursed exceeds the amount treated as substantiated under IRS rules

Box 12 should contain only the amount treated as substantiated , or the nontaxable part.

Boxes 1, 3 (up to the Social Security wage base), and 5 should include the part of the reimbursement that is more than the amount treated as substantiated.

Railroad employers will report the unsubstantiated amounts in Box 14.

Code M: Uncollected Social Security or RRTA tax on taxable cost of group-term life insurance over $50,000 for former employees

If your former employer provided you more than $50,000 of group-term life insurance coverage for periods during which an employment relationship no longer exists, this code will contain the amount of uncollected Social Security tax or RRTA tax on the coverage.

This amount should not be included in Box 4.

Code N: Uncollected Medicate tax on taxable cost of group-term life insurance over $50,000 for former employees

If your former employer provided you more than $50,000 of group-term life insurance coverage for periods during which an employment relationship no longer exists, this code will contain the amount of uncollected Medicare tax on the coverage. This amount should not be included in Box 6.

This will not show uncollected Additional Medicare tax.

Code P: Excludable moving expense reimbursements paid directly to a member of the U.S. Armed Forces

The exclusion for qualified moving expense reimbursements applies only to members of the U.S. Armed Forces on active duty who move pursuant to a military order and incident to a permanent change of station. This is also known as permanent change of station or PCS orders.

Code P will indicate the total moving expense reimbursements paid directly to you for qualified (allowable) moving expenses.

Code Q: Nontaxable combat pay

If you received nontaxable combat pay, it will be reported here.

Code R: Employer contributions to an Archer MSA

Indicates employer contributions to an Archer MSA.

Code S: Employee salary reduction contributions under a Section 408(p) SIMPLE plan

Shows deferrals under a Section 408(p) salary reduction SIMPLE retirement account.

However, if the SIMPLE plan is part of a Section 401(k) arrangement, your employer may use code D.

Code T: Adoption benefits

Code T shows the total that your employer paid or reimbursed for qualified adoption expenses furnished to you under an adoption assistance program.

This also includes adoption benefits paid or reimbursed from the pre-tax contributions you made under a cafeteria plan. However, this does not include adoption benefits forfeited from a cafeteria plan.

Your employer should report all amounts, including those in excess of the $15,950 exclusion.

Code V: Income from the exercise of nonstatutory stock option(s)

This code should reflect the spread you received from your stock options. The spread represents the fair market value of the stock over the stock’s exercise price.

This amount should also be reflected as compensation in Box 1, Box 3, and Box 5.

Code W: Employer contributions to a health savings account (HSA)

Shows any employer contributions (including amounts you elected to contribute using a cafeteria plan) to an HSA.

Code Y: Deferrals under a Section 409A nonqualified deferred compensation plan

Your employer may not report these deferrals with Code Y.

If your employer does report them, this should show current year deferrals, including earnings during the year on current year and prior year deferrals.

Code Z: Income under a nonqualified deferred compensation plan that fails to satisfy Section 409A

This includes all amounts deferred (including earnings on amounts deferred) that are includible in income under IRC Section 409A because the NQDC plan fails to satisfy the Section 409A requirements.

These should not include amounts properly reported on a previous year copy of:

- IRS Form 1099-MISC (or corrected version)

- Form W-2

- Form W-2c

Code AA: Designated Roth contributions under a Section 401(k) plan

Your employer will use this code to report designated Roth contributions under a Section 401(k) plan. This should not include elective deferrals under code D.

Code BB: Designated Roth contributions under a Section 403(b) plan

Use this code to report designated Roth contributions under a section 403(b) plan. This should not include elective deferrals under code E.

Code DD: Cost of employer-sponsored health coverage

Your employer will use this code to report the cost of employer-sponsored health coverage. The amount reported with code DD is not taxable.

Code EE: Designated Roth contributions under a governmental Section 457(b) plan

Under this code, your employer will report designated Roth contributions under a governmental Section 457(b) plan. This should not include elective deferrals under code G.

Code FF: Permitted benefits under a qualified small employer health reimbursement arrangement

Use this code to report the total amount of permitted benefits under a qualified small employer health reimbursement arrangement (QSEHRA).

The maximum reimbursement for an eligible employee under a QSEHRA for 2024 is:

- $6,150 for individuals

- $12,450 for family coverage

Code GG: Income from qualified equity grants under Section 83(i)

This code will report the amount includible in gross income from qualified equity grants under Section 83(i)(1)(A) for the given year.

Code HH: Aggregate deferrals under Section 83(i) as of the close of the calendar year

Your employer will report the aggregate amount of income deferred under section 83(i) elections as of the close of the calendar year as Code HH.

Code II: Medicaid waiver payments excluded from gross income under Notice 2014-7

Your employer will report the amount of Medicaid waiver payments not reported in box 1.

Box 13

In this part, there are 3 boxes indicated:

- Statutory employee

- Retirement plan

- Third-party sick pay

Your employer will check all that apply. Let’s take a closer look at each.

Statutory employee

Your employer will check this box for statutory employees whose earnings are subject to Social Security and Medicare taxes, but not subject to federal income tax withholding.

This does not include common-law employees. There are workers who are independent contractors under the common-law rules but are treated by statute as employees. They are called “statutory employees.”

Statutory employees include the following:

- A driver who distributes beverages (other than milk) or meat, vegetable, fruit, or bakery products; or who picks up and delivers laundry or dry cleaning, if the driver is an agent of the employer or is paid on commission.

- A full-time life insurance sales agent whose principal business activity is selling life insurance or annuity contracts, or both, primarily for one life insurance company.

- An individual who works at home on materials or goods supplied by the employer and that must be returned to the employer or a person designated by the employer, if the employer also furnishes specifications for the work to be done.

- A full-time traveling or city salesperson who works on the employer’s behalf and turns in orders from wholesalers, retailers, contractors, or operators of hotels, restaurants, or other similar establishments.

- The goods sold must be merchandise for resale or supplies for use in the buyer’s business operation.

- The work performed must be the salesperson’s principal business activity.

Retirement plan

Your employer will check this box if you were an “active participant” in any of the following at any point in the tax year:

- A qualified pension, profit-sharing, or stock-bonus plan described in Section 401(a)

- Includes 401(k) retirement plans

- An annuity plan described in Section 403(a).

- An annuity contract or custodial account described in Section 403(b).

- A simplified employee pension (SEP) plan described in Section 408(k).

- A SIMPLE retirement account described in Section 408(p).

- A trust described in Section 501(c)(18).

- A plan for federal, state, or local government employees or by an agency or instrumentality thereof (other than a Section 457(b) plan).

Does not include contributions to a nonqualified or Section 457(b) plan.

Generally, an employee is an active participant if covered by:

- A defined benefit plan for any tax year that they are eligible to participate in, or

- A defined contribution plan, such as a 401(k) plan, for any tax year that employer or employee contributions (or forfeitures) are added to their account.

Third-party sick pay

This box will be checked only by a third-party sick pay payer filing a Form W-2 for an insured’s employee or are an employer reporting sick pay payments made by a third party.

Box 14: other

If your employer included 100% of a vehicle’s annual lease value in the your income, your employer must also report that value here or on another statement.

This box can also contain other information your employer may wish to give you. This might include:

- State disability insurance taxes withheld

- Union dues

- Uniform payments

- Health insurance premiums deducted

- Nontaxable income

- Educational assistance payments, or

- Minister’s parsonage allowance and utilities

- Fringe benefits

Your employer may also include the following pension plan contributions:

- Nonelective employer contributions made on your behalf

- Voluntary after-tax contributions (not designated Roth contributions) deducted from your pay

- Required employee contributions

- Employer matching contributions

Boxes 15 through 20: State and local tax information

Your employer may use the following boxes to report state and local income tax information. This section can hold state and local information for wages and taxes for two states and two localities.

If you are subject to taxation from more than two states or localities, your employer may file a second Form W-2.

Box 15: State

Should contain the two-letter abbreviation for the state’s name.

Box 16: Employer’s state ID number

May contain a different identification number, as assigned by the state government.

Box 17: State wages, tips, etc.

Your employer will report income subject to state taxes.

Box 18: State income tax

Includes the amount of state income tax calculated for the income reported in Box 17.

Box 19: Local wages, tips, etc.

Income subject to local tax is reported in Box 19.

Box 20: Local income tax

Actual amount remitted for local income tax purposes.

Video walkthrough

Watch this instructional video to learn more about your pay and taxes, as reported on Form W-2.

Are you tired of dreading tax season?

If you’re like most people, you push through the stress of filing, only to be hit with a bigger bill than expected—then put it all behind you until the same cycle repeats next year.

But what if you could change the game?

Tax planning puts you in control. It’s about being proactive, not reactive—taking small, smart steps throughout the year to reduce your tax burden, increase your savings, and keep more of your hard-earned money working for you.

Here’s what effective tax planning helps you do:

✅ Avoid the surprise of a high tax bill

✅ Understand how your income and decisions affect your taxes

✅ Strategically lower your tax liability over time

Ready to make smarter tax moves?

👉 Join my free weekly tax planning newsletter and get one actionable tip every week to help you reduce your taxes legally and effectively.

Start taking control—your future self will thank you.

Frequently asked questions

Generally, your employer should give all employees Form W-2 no later than January 31st of the calendar year after the end of the tax year. Employers may request a 30-day extension from the Internal Revenue Service.

You can request that your employer give you a corrected Form W-2. If you have not received a correct W-2 Form by the end of February, contact the IRS at (800) 829-1040 to initiate a complaint and to receive an income transcript of your W-2 information.

If you filed a tax return with information provided by the IRS, and it is different from the corrected W-2 your employer provided, you will need to file an amended tax return on IRS Form 1040-X.

Where can I find IRS Form W-2?

As with other tax forms, you can find IRS Form W-2 on the IRS website. Your employer should provide your copy no later than January 31st following the end of the tax year.

For your convenience, we’ve enclosed the latest version of IRS Form W-2 below.

Related tax articles

This tax form is one of the fillable tax forms provided by the Internal Revenue Service, to help taxpayers reduce their tax preparation costs. To see more forms like this, visit our free fillable tax forms page, where you’ll also find articles like this.

Unlike the IRS, our articles contain step by step instructions for each tax form, as well as video walkthroughs. You can also check out all of our videos by subscribing to our YouTube channel!