IRS Form 7206 Instructions

If you work for yourself and have your own health insurance, you may be able to deduct your health insurance costs. Taxpayers can do this by filing IRS Form 7206 with their individual income tax return.

In this article, we’ll walk through everything you need to know about IRS Form 7206, including:

- How to complete IRS Form 7206

- Eligible health insurance costs

- How to deduct your health care costs on your tax return

Let’s start with an overview of this tax form.

Table of contents

How do I complete IRS Form 7206?

This one-page tax form appears to be more difficult than it actually is. However, you should know that you should file a separate Form 7206 for each trade or business under which you established a health insurance plan.

Enter your name and taxpayer identification number at the top of the form. Your taxpayer ID number is generally your Social Security number.

Let’s proceed to Line 1.

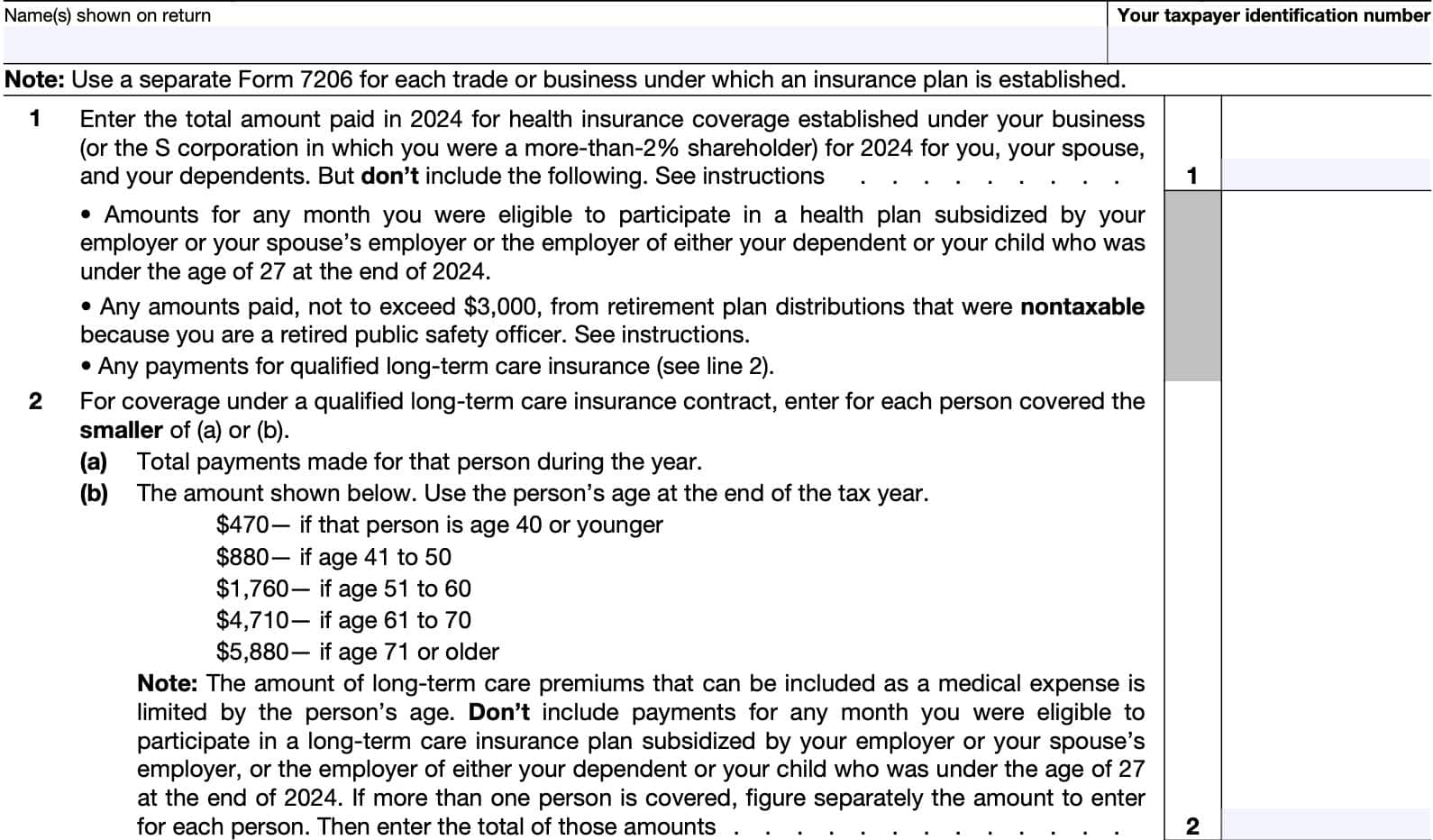

Line 1: Total amount paid for health insurance coverage

In Line 1, enter the total amount that you paid during the tax year for health insurance coverage on behalf of the following individuals:

- Yourself

- Your spouse

- Your dependents

However, you should not include the following amounts:

- Insurance amounts that you paid when you met the eligibility criteria to participate in an employer-sponsored health plan for:

- Yourself

- Your spouse

- Your child who was under age 27 at the end of the tax year

- Any amounts paid from retirement plan distributions that were nontaxable due to your status as a retired public safety officer if the amounts:

- Came directly from your retirement plan to the insurer for qualified health insurance premiums, or

- Received by you from the retirement plan, then used to pay the premiums

- Premium amounts that you paid for qualified long-term care insurance

Once you’ve entered the total amount for health insurance coverage in Line 1, we’ll go to Line 2 to report qualified long-term care insurance premiums.

Line 2: Qualified long-term care insurance contract costs

For Line 2, enter the smaller of:

- Total qualified long-term care contract payments made during the tax year

- The IRS limit based upon age:

- Age 40 or below: $470

- Ages 41 to 50: $880

- Ages 51 to 60: $1,760

- Ages 61 to 70: $4,710

- Ages 71 and older: $5,880

Do not include payments for any month in which you were eligible to participate in an employer-sponsored long-term care insurance policy, whether that plan was for yourself, your spouse, or a dependent.

Qualified long-term care contracts

According to the IRS form instructions, a qualified long-term care insurance contract is an insurance contract that only provides qualified long-term care services, and meets the following requirements:

- The contract must be guaranteed renewable

- The contract must provide that refunds and dividends under the contract can only reduce future long-term care premiums or increase future benefits.

- Except for refunds on the death of the insured or complete surrender or cancellation of the contract

- The contract must not provide for a cash surrender value or other money that can be paid out, assigned, pledged, or borrowed

- The long-term care contract must not pay or reimburse expenses incurred for services or items that Medicare would normally reimburse

- Except where Medicare is a secondary payer or the contract makes per diem or other periodic payments without regard to expenses.

Qualified long-term care services

According to the Internal Revenue Service, qualified long-term care services are:

- Necessary diagnostic, preventive, therapeutic, curing, treating, mitigating, and rehabilitative services; and

- Maintenance or personal care services.

The services must be required by a chronically ill individual and prescribed by a licensed health care practitioner.

Chronically ill individuals

A chronically ill individual is one who:

- Has been unable, due to loss of functional capacity for at least 90 days to perform at least two activities of daily living (ADLs) without substantial assistance from another person. ADLs include:

- Eating

- Toileting

- Transferring (mobility)

- Bathing

- Dressing

- Continence

- An individual requiring substantial supervision to be protected from health and safety threats due to severe cognitive impairment or decline.

The certification must have been made by a licensed health care practitioner within the previous 12 months.

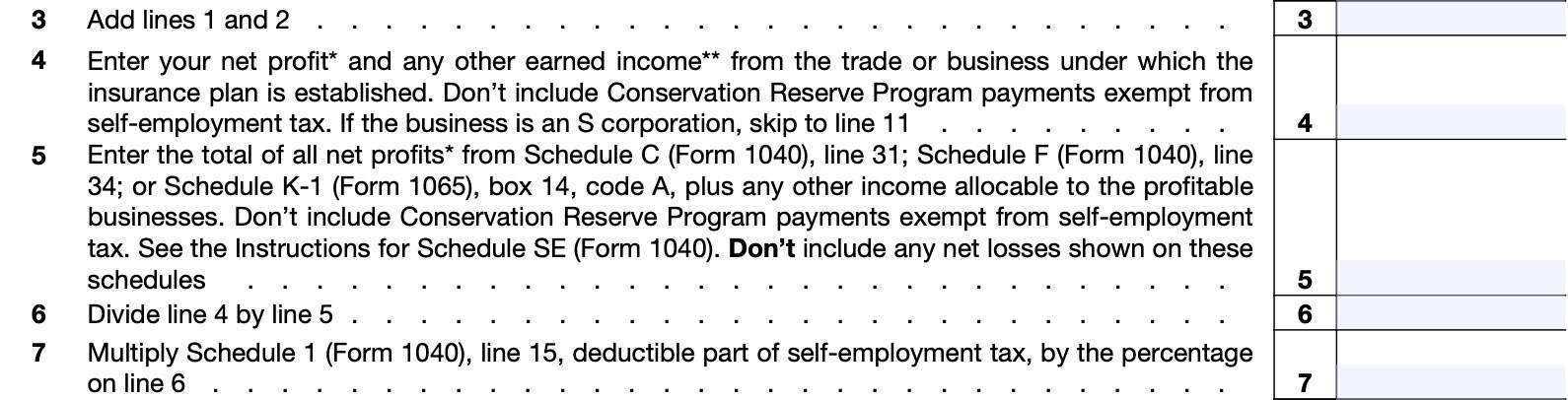

Line 3

Add Line 1 and Line 2. Enter the total here.

Line 4

For Line 4, enter the net profit and any other earned income from the trade or business under which you established the health insurance plan. However, do not include Conservation Reserve Program payments that are exempt from self-employment tax.

If you used either optional method to calculate your net earnings from self-employment from any business, enter the amount attributable to that business from IRS Schedule SE, Line 4b.

If your business is an S corporation, skip to Line 11, below. Otherwise, go to Line 5.

Earned income

Earned income includes net earnings and gains from the sale, transfer, or licensing of property that you created. However, earned income does not include capital gains from the sales or dispositions of property.

Line 5

Enter the total of all net profits from:

- IRS Schedule C, Line 31

- IRS Schedule F, Line 34, or

- Schedule K-1 (IRS Form 1065), Box 14, Code A

- Any other net income allocable to profitable businesses

Do not include Conservation Reserve Program payments that are exempt from self-employment taxes. Also, do not include net losses shown on any tax schedules.

Line 6

Divide Line 4 by Line 5. Enter the result here as a percentage or decimal figure.

Line 7

Multiply the deductible part of self-employment tax, found on IRS Schedule 1, Line 15, by the percentage from Line 6.

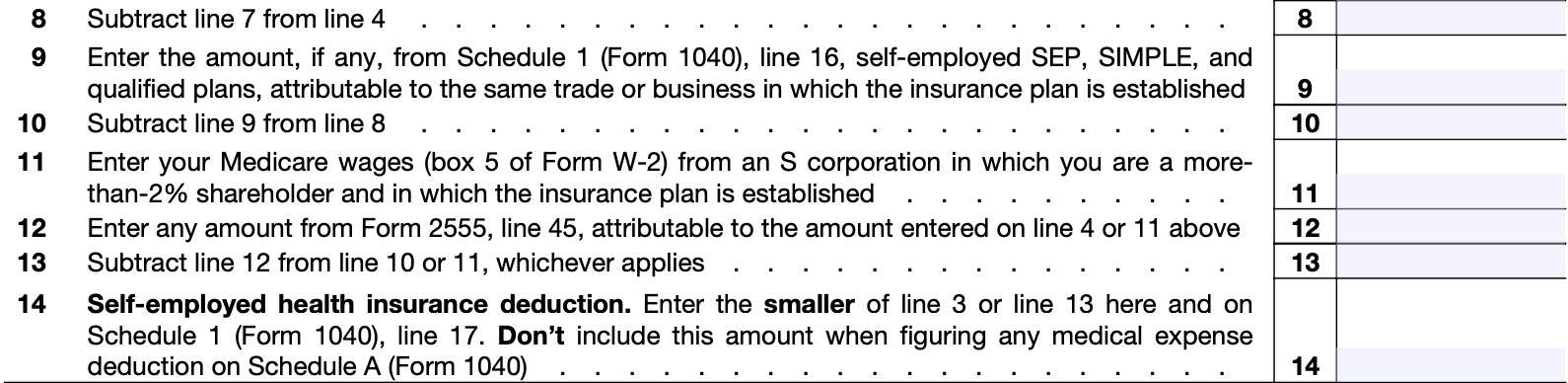

Line 8

Subtract Line 7 from Line 4. Enter the result in Line 8.

Line 9: Self-employed retirement plans

Enter any amount from Schedule 1, Line 16, attributable to the same trade or business in which the insurance plan was established. This should any self-employed SEP, SIMPLE, and qualified retirement plans.

Line 10

Subtract Line 9 from Line 8. Enter the total here.

Line 11: Medicare wages

From IRS Form W-2, Box 5, enter any Medicare wages includible in gross income from an S-corporation in which:

- You are a more-than-2% shareholder, and

- The insurance plan is established

Line 12

Enter any amount of foreign earned income exclusion from IRS Form 2555, attributable to the amount entered on either Line 4 or Line 11. You’ll find this number on Line 45.

Line 13

Subtract Line 12 from either Line 10 or Line 11, whichever is applicable.

Line 14: Self-employed health insurance deduction

Enter the smaller of either:

Include this amount on Schedule 1, Line 17.

Do not include this amount if you are calculating itemized deductions on IRS Schedule A. However, any medical insurance payments not deductible on Schedule 1, Line 17, can be included as medical expenses on Schedule A if you itemize deductions. This includes any health insurance deductions not reported on Schedule 1.

Requirements for filing IRS Form 7206

In order to claim health insurance costs, one of the following statements must be true:

- You were self-employed and had a net profit for the year reported on Schedule C or Schedule F on your Form 1040

- You were a partner with net earnings from self-employment for the year reported on Schedule K-1, Box 14, Code A

- You used one of the optional methods to figure your net earnings from self-employment on Schedule SE

- S Corporation shareholders: You received wages in 2024 from an S corporation in which you were a more-than-2% shareholder.

- Total premiums paid or reimbursed by the S-corporation are shown as wages on IRS Form W-2.

Video walkthrough

Watch this instructional video to learn more about claiming the health insurance premiums deduction by filing Form 7206 with your income tax return.

Frequently asked questions

Many taxpayers can use the worksheet in the Form 1040 instructions to calculate the health insurance deduction. However, self-employed taxpayers must file IRS Form 7206 if they had multiple sources of self-employment income, file IRS Form 2555, or include long-term care insurance costs.

Self-employed individuals may be able to deduct health insurance premiums on Schedule 1 of your Form 1040. However, you cannot deduct health insurance premiums that you pay as part of an employer-sponsored health care plan.

Where can I find IRS Form 7206?

As with other tax forms, you can find IRS Form 7206 on the IRS website. We’ve attached the latest version of this IRS form here, in this article, for your convenience.

Can I claim the Social Security Medicare payments if I am paying for Part B and D as well as at the same time working in my own business?

According to the form instructions: Medicare premiums you voluntarily pay to obtain insurance in your name that is similar to qualifying private health insurance can be used to figure the deduction.