IRS Schedule C Instructions

Many small business owners operate as a single-member LLC or sole proprietorship. Because of their focus on running their own business, these business owners might end up having difficulty calculating their own taxes on IRS Schedule C during tax time.

In this article, we’ll walk through IRS Schedule C, including:

- How to complete & file Schedule C with your tax return

- Who should file Schedule C

- Other tax forms you may need to complete when filing Schedule C

Let’s start with an overview of the tax form itself.

Table of contents

How do I complete IRS Schedule C?

There are 5 parts to this two-page tax form:

- Part I: Income

- Part II: Expenses

- Part III: Cost of Goods Sold

- Part IV: Information on Your Vehicle

- Part V: Other Expenses

Let’s start at the top of the form, with the taxpayer information fields.

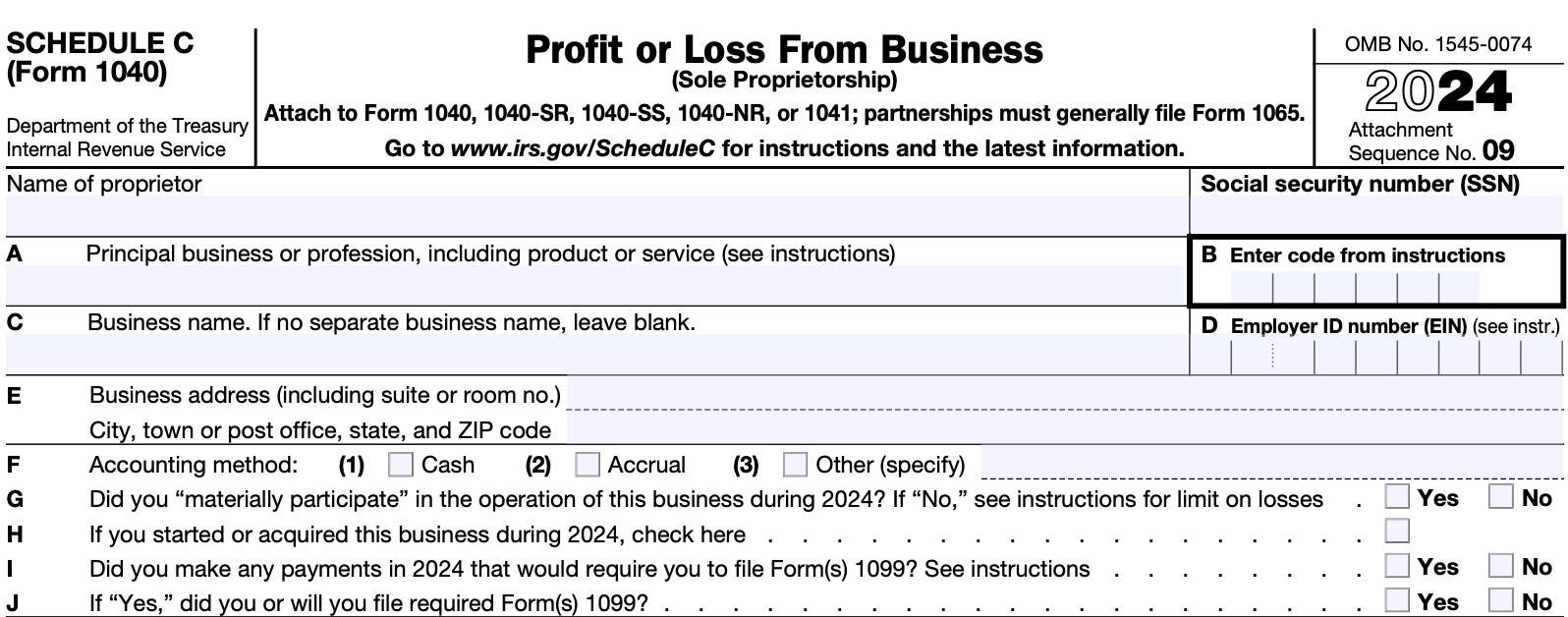

Taxpayer information

At the very top of the form, enter your name in the proprietor field, along with your Social Security number, in the SSN field. If you are filing IRS Form 1041 on behalf of an estate or trust, do not enter anything in the SSN field. Instead, include the employer identification number (EIN) in Line D, below.

Line A: Principal business or profession

Describe the business or professional activity that provided your principal source of income reported on Line 1. If you owned multiple business activities, you must complete a separate Schedule C for each business.

Give the general field or activity and the type of product or service. If your general field or activity is

wholesale or retail trade, or services connected with production services (mining, construction, or manufacturing), also give the type of customer or client.

Line B

Enter the six-digit Principal Business Activity code (PBA code) that corresponds to the primary purpose of your business.

For nonstore retailers, select the PBA code by the primary product that your establishment sells. For example, establishments primarily selling prescription and non-prescription drugs should select PBA code 456110: Pharmacies & drug retailers.

The IRS Schedule C Instructions contains a comprehensive list of PBA codes.

Line C: Business name

Enter the business name, if your sole proprietorship contains a separate name.

Line D: Employer ID number

Enter on line D the EIN that was issued to you on IRS Form SS-4.

Do not enter your SSN on this line, and do not enter another taxpayer’s EIN on this line. If you do not have an EIN, leave Line D blank.

Line E: Business address

Enter your business address. Use a street address instead of a P.O. Box number. Also, include the suite or room number, if your address contains one.

If you conducted your business from a home office at the address shown on Page 1 of your income tax return, leave this line blank.

Line F: Accounting method

Enter the type of accounting method used. Most taxpayers use either:

- Cash method

- Accrual method

- Another method approved by the Internal Revenue Service

If you use the cash method of accounting, you will need to show all items of taxable income actually received or constructively received during the tax year. Constructive receipt refers to income that is either credited to your account or set aside for you to use at your discretion.

If you wish to change your accounting method, you must generally file IRS Form 3115. You may also have to make a Section 481(a) adjustment to prevent amounts of income or expense from being double-recorded or omitted.

Line G

In Line G, indicate whether or not you materially participated in business operations during the tax year. If you check ‘No,’ this indicate that the business activity is primarily a passive one. Passive activities are subject to certain loss limitations.

Material participation

For passive activity purposes, if any of the following 7 conditions apply, you are considered to have materially participated in a business activity during the tax year:

- You participated in the activity for more than 500 hours during the tax year.

- Your participation in the activity for the tax year was substantially all of the participation in the activity of all individuals for the tax year

- This includes individuals who did not own any interest in the business activity

- You participated in the activity for more than 100 hours during the tax year, and you participated at least as much as any other person for the tax year.

- This includes individuals who did not own any interest in the activity.

- The activity is a significant participation activity for the tax year, and you participated in all significant participation activities for more than 500 hours during the year

- An activity is a “significant participation activity” if:

- It involves the conduct of a trade or business

- You participated for more than 100 hours during the tax year

- You did not materially participate under any other material participation tests

- An activity is a “significant participation activity” if:

- You materially participated in the activity for any 5 of the prior 10 tax years.

- The activity is a personal service activity in which you materially participated for any 3 prior tax years.

- A personal service activity is one that involves performing personal services in

the field of health, law, engineering, architecture, accounting, actuarial science, performing arts, or consulting, or any other trade or business in which capital is not a material income-producing factor.

- A personal service activity is one that involves performing personal services in

- Based on all the facts and circumstances, you participated in the activity on a regular, continuous, and substantial basis for more than 100 hours during the tax year

Rental of personal property

As a general rule, a rental activity is considered to be passive, even if you materially participated in the business during the year. However, if you meet one of the exceptions as outlined in IRS Form 8582, Passive Activity Loss Limitations, then the material participation rules apply.

Exception for Oil and Gas income

If you are filing Schedule C to report income and deductions from an oil or gas well in which you own a working interest directly or through an entity that does not limit your liability, check the “Yes” box.

The activity of owning a working interest is not a passive activity, regardless of your level of participation.

Line H

Check the box in Line H if you purchased the business during the tax year.

Line I

Did you make any payments during the tax year that would require you to file IRS Form 1099? If so, check ‘Yes.’ Otherwise, check ‘No.’

You may have to file information returns for the following:

- Wages paid to employees

- Certain payments of fees and other nonemployee compensation

- Interest

- Rents

- Royalties

- Real estate transactions

- Annuities

- Pensions

- Sales exceeding $5,000 of consumer products to a person on a buy-sell, deposit-commission, or similar basis for resale

Line J

If you checked ‘Yes’ in Line I, indicate whether you plan to file the required Form 1099.

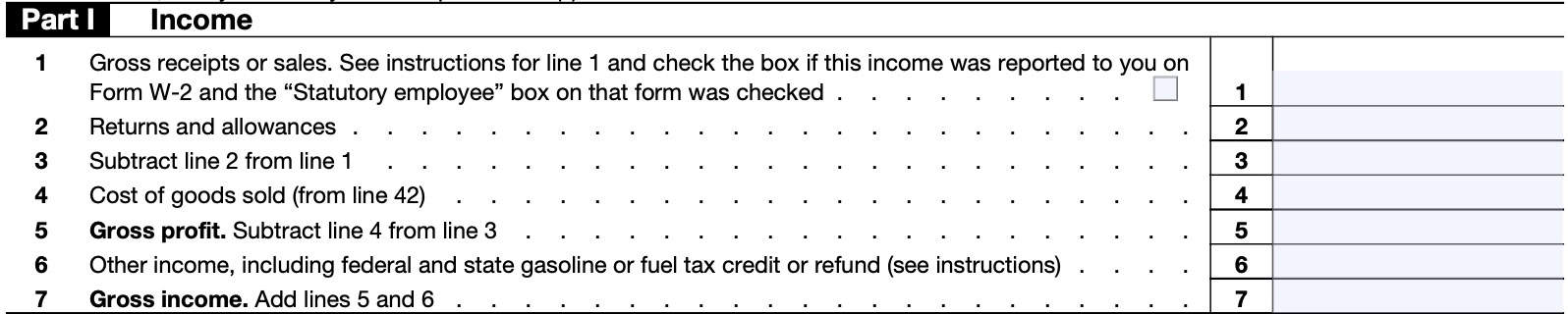

Part I: Income

In Part I, we’ll report all items of income, then subtract certain items to arrive at gross profit and gross income. Let’s start with Line 1.

Line 1: Gross receipts or sales

In Line 1, enter the gross receipts from your business or trade. This includes any business income that might have been reported on IRS Form 1099. Here are some common versions of Form 1099 that you might have received during the tax year:

- IRS Form 1099-MISC: Taxpayers can expect to receive Form 1099-MISC if they received at least:

- $10 in royalties or brokerage payments in lieu of dividends or tax-exempt interest, or

- $600 for any of the following:

- Rental income

- Prizes and awards

- Medical and health care payments

- Crop insurance

- Cash payments for fish or other aquatic life

- IRS Form 1099-NEC: Used to report non-employee compensation

- IRS Form 1099-K: Used to report income from the following sources:

- Payment cards, such as credit, debit, or gift cards

- Payment applications, online marketplaces, or other third-party payment networks

Statutory employees

If you received a Form W-2, Wage and Tax Statement, and the “Statutory employee” box in Box 13 of that form was checked, report your income and expenses related to that income on Schedule C.

Enter your statutory employee income from Box 1 of Form W-2 on Line 1, then check the applicable box.

Your employer should have withheld Social Security and Medicare tax from your earnings. You should not owe self-employment tax on these earnings.

Statutory employees include the following:

- Full-time life insurance agents

- Certain agent or commission drivers and traveling salespersons

- Certain homeworkers

If you had both self-employment income and statutory employee income, you must file a separate Schedule C form for each source of income.

Installment sales

In general, you cannot use the installment method to report income from the sale of

- Personal property regularly sold under the installment method, or

- Real property held for resale to customers

However, you can use the installment method to report income from sales of certain residential lots and timeshares if you elect to pay interest on the tax due on that income after the year of sale. IRC Section 453(l)(2)(B) contains additional details.

If you make this election, include the interest in the total on IRS Schedule 2, Line 14. Enter the amount of interest and ‘453(l)(3)’ on the line next to the box.

Line 2: Returns and allowances

Report your sales returns and allowances as a positive number here.

A sales return is a cash or credit refund you gave to customers who returned defective, damaged, or unwanted products.

A sales allowance is a reduction in the selling price of products, instead of a cash or credit refund.

Line 3

Subtract Line 2 from Line 1. Enter the difference here.

Line 4: Cost of goods sold

Enter the cost of goods sold, as calculated in Part III, below. This is the amount from Line 42.

Line 5: Gross profit

Subtract Line 4 from Line 3. This represents your gross profit.

Line 6: Other income

In Line 6, report other income that is not found elsewhere. Examples of other income include:

- Finance reserve income

- Scrap sales

- Bad debts you recovered

- Interest, such as on notes and accounts receivable

- State gasoline or fuel tax refunds you received in the tax year

- Any amount of credit for biofuel claimed as a producer on Line 3 of IRS Form 6478

- Any amount of credit claimed on Line 10 of IRS Form 8864 for any of the following:

- Biodiesel

- Renewable diesel

- Sustainable aviation fuel

- Credit for federal tax paid on fuels claimed on your income tax return in a prior year.

- Prizes and awards related to your trade or business

- Amounts you received in your trade or business as shown on IRS Form 1099-PATR

- The amount of any payroll tax credit taken by an employer for qualified paid sick leave and qualified paid family leave under either of the following:

- Families First Coronavirus Relief Act

- American Rescue Plan

Line 7: Gross income

Add Line 5 and Line 6, then enter the result in Line 7.

This represents your gross income for the tax year.

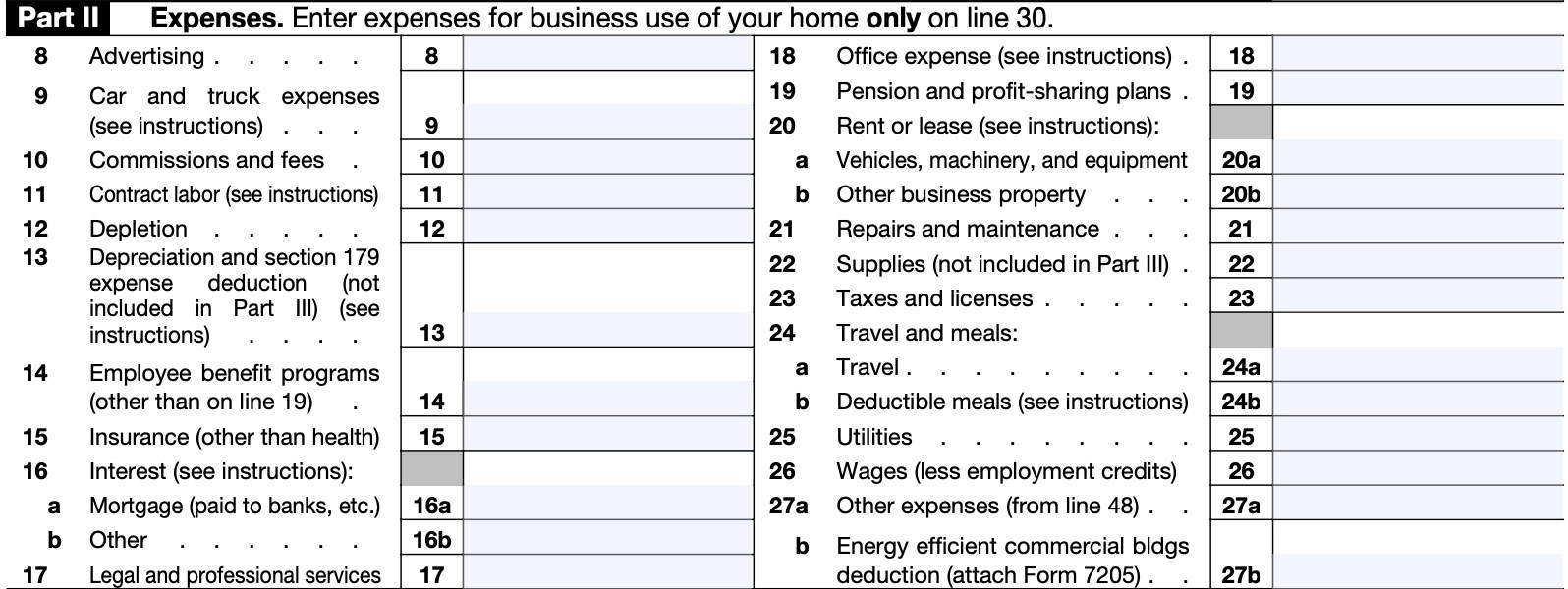

Part II: Expenses

In Part II, we’ll calculate expenses you may have incurred while operating your business during the tax year. First, we should discuss capitalizing expenses.

Capitalizing expenses

If you produced real or tangible personal property or acquired real or personal property for resale, you must generally capitalize certain expenses in inventory or other property.

These expenses include the direct costs of the property and any indirect costs properly allocable to that property. If applicable, you will need to reduce the amounts on Lines 8 through 26 and Part V by amounts capitalized.

Certain exceptions exist for artists of creative properties and small business taxpayers.

Small business taxpayer

The IRS considers a business entity to be a small business taxpayer if the business:

- Has average annual gross receipts of $27 million or less for the 3 prior tax years, and

- The business is not a tax shelter, as defined in IRC Section 448(d)(3)

IRS Publication 538, Accounting Periods and Methods, contains additional information about the uniform capitalization rules.

Line 8: Advertising

Enter any advertising expenses you incurred in the tax year.

Line 9: Car and truck expenses

You can select from two different methods of calculating driving expenses:

- Actual expenses of operating your car or truck

- Standard mileage rate

You can select either option, even if you used your vehicle for hire, such as operating a taxi or driving for a ride-sharing service, such as Uber or Lyft.

Actual expenses

You cannot use actual expenses for a leased vehicle if you previously used the standard mileage rate for that vehicle. You must use actual expenses if you used five or more vehicles simultaneously in your business.

If you deduct actual expenses, then include the business portion of expenses for the following on Line 9:

- Gasoline

- Oil

- Repairs

- Auto insurance

- License plates

Enter depreciation on Line 13, below. If you incurred any rent or lease payments, enter those on Line 20a, below.

Standard mileage rate

You can take the standard mileage rate for the current taxable year only if you:

- Owned the vehicle and used the standard mileage rate for the first year you placed the vehicle in service, or

- Leased the vehicle and are using the standard mileage rate for the entire lease period

If you take the standard mileage rate,

- Multiply the business miles that you drove during 2024 by 67 cents per mile;

- Add to this amount your parking fees and tolls; and

- Enter the total on Line 9

Do not include any of the following:

- Depreciation

- Rental or lease payments

- Actual operating expenses

Line 10: Commissions and fees

Enter the total commissions and fees for the tax year. However, do not include commissions or fees that are capitalized or deducted elsewhere on your return.

You must file Form 1099-NEC to report certain commissions and fees of $600 or more during the year. Generally, you must capitalize commissions and other fees paid to facilitate the sale of property.

However, if you regularly sell property in the ordinary course of your trade or business, then you may be considered a dealer in property. As a dealer in property, you may enter commissions and fees paid to sell property directly in Line 10.

Line 11: Contract labor

Enter the total cost of contract labor for the tax year. Contract labor includes payments to persons you do not treat as employees, such as independent contractors, for services performed for your trade or business.

Do not include contract labor deducted elsewhere on your return, such as contract labor includible on any of the following:

- Line 17: Legal and professional services

- Line 21: Repairs and maintenance

- Line 26: Wages

- Line 37: Cost of labor

You must file IRS Form 1099-NEC to report contract labor payments of $600 or more during the year.

Line 12: Depletion

Enter any depletion expenses in Line 12. IRS Publication 535, Chapter 9, contains additional information.

Line 13: Depreciation and Section 179 Deduction

Enter any depreciation or Section 179 deductions in Line 13.

Depreciation

Depreciation is the annual deduction allowed to recover the cost or other basis of business or investment property having a useful life substantially beyond the tax year. You can also depreciate improvements made to leased business property.

However, you may not depreciate the following:

- Stock in trade

- Inventories

- Land

For tax purposes, depreciation begins when you first use the property in your business or to produce income. Depreciation ends when one of the following happens:

- You take the depreciated property out of service

- You deduct all of the depreciable cost or other basis over the expected life of the property, or

- You no longer use the property in your business or to produce income

Section 179 expense deduction allows taxpayers to deduct a larger than normal amount of the property’s value for tax purposes. You may need to complete IRS Form 4562 to determine the amount you should enter in Line 13.

When to attach IRS Form 4562 to your tax return

You must attach a completed Form 4562 when you use Schedule C and you are claiming:

- Depreciation on property placed in service during the tax year

- Depreciation on listed property, regardless of the date it was placed in service; or

- A Section 179 expense deduction

Listed property

Listed property generally includes the following:

- Passenger automobiles weighing 6,000 pounds or less;

- Any other property used for transportation if the nature of the property lends itself to personal use,

- Can include vehicles such as motorcycles, pickup trucks, etc.; and

- Any property used for entertainment or recreational purposes, such as photographic, phonographic, communications, or video equipment

However, listed property does not include photographic, phonographic, communication, or video equipment used exclusively in your trade or business or at your regular business establishment.

Line 14: Employee benefit programs

Deduct contributions to employee benefit programs that are not an incidental part of a pension or profit-sharing plan included on Line 19. Examples can include the following:

- Accident and health plans

- Group-term life insurance policies

- Dependent care assistance programs

If you contributed to a dependent care assistance program on your own behalf as a self-employed individual, you should complete IRS Form 2441, Parts I and III, to calculate your deductible contributions.

You cannot deduct group-term life insurance premiums you paid on your own behalf as a self-employed person.

Also, do not include any contributions you made on your behalf as a self-employed person to an accident and health plan. However, you may be able to deduct the amount you paid for health insurance premiums for yourself, your spouse, and dependents on IRS Schedule 1, Line 17, even if you do not itemize your deductions using Schedule A.

You must reduce your Line 14 deduction by the amount of any credit for small employer health insurance premiums as calculated on IRS Form 8941.

Line 15: Insurance

Deduct business insurance premiums that you paid on Line 15. Do not deduct any amounts credited to a reserve for self-insurance or premiums paid for a policy that reimburses lost earnings due to sickness or disability.

Do not deduct employee accident or health insurance costs on Line 15. Instead, report these amounts on Line 14, above.

Line 16: Interest

Enter any business interest you paid during the tax year here. However, the tax treatment of interest depends on the type of interest, and what it is used for. This might impact the amount of interest you can allocate to Line 16 of Schedule C.

You generally must file IRS Form 8990 to deduct any interest expenses of this trade or business unless you are a small business taxpayer or meet one of the other filing exceptions listed in the form instructions.

If you received an IRS Form 1098 that reported mortgage interest on real property used for business purposes, enter the mortgage interest in Line 16a. If you did not receive a Form 1098, enter the interest in Line 16b.

Line 17: Legal and professional services

Include any fees charged by accountants and attorneys that are ordinary and necessary expenses directly related to operating your business. Also include any fees for:

- Tax advice related to your business

- Tax preparation related to your business

- Expenses incurred in resolving business-related tax deficiencies

Line 18: Office expense

In Line 18, enter any expenses for office supplies and postage.

Line 19: Pension and profit-sharing plans

Enter your deduction for the contributions you made for the benefit of your employees to any of the following:

- Pension plan

- Profit-sharing plan

- Annuity plan

If the plan included you, as a self-employed individual, enter your employer contributions on IRS Schedule 1, Line 16, not on Schedule C.

You may need to report plan contributions on one of the following IRS Forms:

- IRS Form 5500-EZ: If you have a one-participant retirement plan that meets certain requirements. This can be a plan that covers yourself only, or you and your spouse.

- IRS Form 5500-SF: You may file this form electronically with the Department of Labor if you have a small plan that meets certain requirements

- Fewer than 100 participants

- IRS Form 5500: File this electronically for a plan that doesn’t meet the requirements outlined above

The deduction for pension plan or profit-sharing contributions may be subject to limitations. IRS Publication 560, Retirement Plans for Small Business, contains additional details.

Line 20: Rental or lease expenses

If you rented or leased vehicles, machinery, or equipment, enter the business portion of your rental cost on Line 20a. If you leased a vehicle for a term of 30 days or more, you may need to reduce your tax deduction by an inclusion amount. IRS Publication 463, Chapter 4, contains additional information on how to calculate the inclusion amount for your vehicle rental.

On Line 20b, enter the amount you paid to rent or lease other property, such as commercial office space.

Line 21: Repairs and maintenance

In Line 21, enter the amount of incidental repairs and maintenance that do not add to property value or substantially prolong the life of your property.

Do not deduct the value of your own labor. Also, you must capitalize any amounts spent to restore or replace property. You cannot deduct these amounts in Line 21.

Line 22: Supplies

Enter the cost of materials and supplies that you actually used during the tax year.

In most cases, you can deduct the cost of materials and supplies only to the extent you actually consumed and used them in your business during the tax year, unless you deducted them in a prior tax year.

However, if you had incidental materials and supplies on hand for which you kept no inventories or records of use, you can deduct the cost of those you actually purchased during the tax year, provided that method clearly reflects income.

You can also deduct the cost of books, professional instruments, equipment, etc., if you normally use them within a year. However, if their usefulness extends substantially beyond a year, you must generally depreciate their costs, instead of expensing them within one year.

Line 23: Taxes and licenses

Enter the following taxes or licensing fees in Line 23:

- State and local sales taxes imposed on you as the seller of goods or services.

- If you collected this tax from the buyer, you must also include the amount collected in gross receipts or sales on Line 1.

- Real estate and personal property taxes on business assets

- Licenses and regulatory fees for your trade or business paid each year to state or local governments.

- You may have to amortize the cost of some licenses, such as liquor licenses.

- See chapter 8 of IRS Publication 535 for details

- Social Security and Medicare taxes paid to match required withholding from your employees’ wages.

- Reduce your deduction by the amount shown on IRS Form 8846, Line 4.

- Federal unemployment tax paid

- Federal highway use tax

- Contributions to a state unemployment insurance fund or disability benefit fund if they are considered taxes under state law.

Non-deductible taxes and license fees

Do not enter any of the following:

- Federal income tax, to include self-employment tax

- You can deduct 1/2 of your self-employment tax as calculated on IRS Schedule SE

- Estate and gift taxes

- Taxes assessed to pay for improvements

- Taxes on your home or personal use property

- You may be able to claim an itemized deduction on IRS Schedule A

- State and local sales taxes on property purchased for use in your business

- Treat these taxes as part of the cost of the property

- State and local sales taxes imposed on the buyer that you were required to collect and pay over to state or local governments.

- If the state or local government allowed you to retain any part of the sales tax you collected, you must include that amount as income on Line 6

- Other taxes and license fees not related to your business

Line 24: Travel and meals

Travel expenses

In Line 24a, enter your expenses for lodging and transportation connected with overnight travel for business while away from your tax home.

In most cases, your tax home is your main place of business, regardless of where you maintain your

family home. You cannot deduct expenses paid or incurred in connection with

employment away from home if that period of employment exceeds 1 year.

Also, you cannot deduct travel expenses for your spouse, your dependent, or any other individual unless:

- That person is your employee,

- The travel is for a bona fide business purpose

- That person would otherwise be able to deduct those travel expenses

Do not include entertainment expenses on this line.

For incidental expenses, you may keep records of your actual expenses. This would include fees and tips given to porters, baggage carriers, maids, bell hops or hotel servants. Incidentals do not include laundry, dry cleaning, lodging tax, or the costs of telephone calls.

You may use a standard rate of $5 per day, but not on any day that you use the standard meal allowance.

Business meals

In Line 24b, enter your deductible meal expenses.

The business meal deduction equals 50% of deductible meal costs. For tax years 2021 and 2022, you may deduct up to 100% of total meal costs.

The following conditions apply to meal expenses for deductibility purposes:

- The meal expense must be an ordinary and necessary expense in carrying on your trade or business.

- The expense cannot be not lavish or extravagant under the circumstances

- You or your employee was present at the meal.

- The meal was provided to a current or potential business customer, client, consultant, or similar business contact.

- In the case of food or beverages provided during or at an entertainment event, the food and beverages were either:

- Purchased separately from the entertainment, or

- Stated separately from the cost of the entertainment on one or more bills, invoices, or receipts

You may also use a standard meal allowance rate, as prescribed by the General Services Administration, to calculate your meal deduction.

Line 25: Utilities

Deduct the utility costs for your business.

If you used your home phone for business, do not deduct the base rate (including taxes) of the first phone line into your residence. However, you may enter any additional costs above and beyond the first phone line.

Line 26: Wages (less employment credits)

Enter total wages and salaries reduced by the following tax credits:

- Work Opportunity Credit, calculated on IRS Form 5884

- Employee Retention Credit for Employers Affected by Qualified Disasters, on IRS Form 5884-A

- Empowerment Zone Employment Credit, reported on IRS Form 8844

- Indian Employment Credit, determined on IRS Form 8845

- Credit for Employer Differential Wage Payments, from IRS Form 8932

- Employer Credit for Paid Family and Medical Leave, reported on IRS Form 8994

Do not reduce your deduction for any portion of a tax credit that was passed through to you from a pass-through entity, such as an S corporation or limited liability company.

Do not include salaries and wages deducted elsewhere on your return or amounts you paid yourself.

Line 27

Line 27 is broken down into two parts:

- Line 27a, Other Expenses

- Line 27b, Energy Efficient Commercial Buildings Deduction

Line 27a: Other expenses

Enter other expenses, as reported on Line 48, below.

Line 27b: Energy Efficient Commercial Buildings Deduction

If applicable, attach a copy of your completed Form 7205 to your tax return.

Line 28: Total expenses before expenses for business use of home

Add Lines 8 through 27b, then enter the result here.

Line 29: Tentative profit or loss

Subtract Line 28 from Line 7. Enter the difference here.

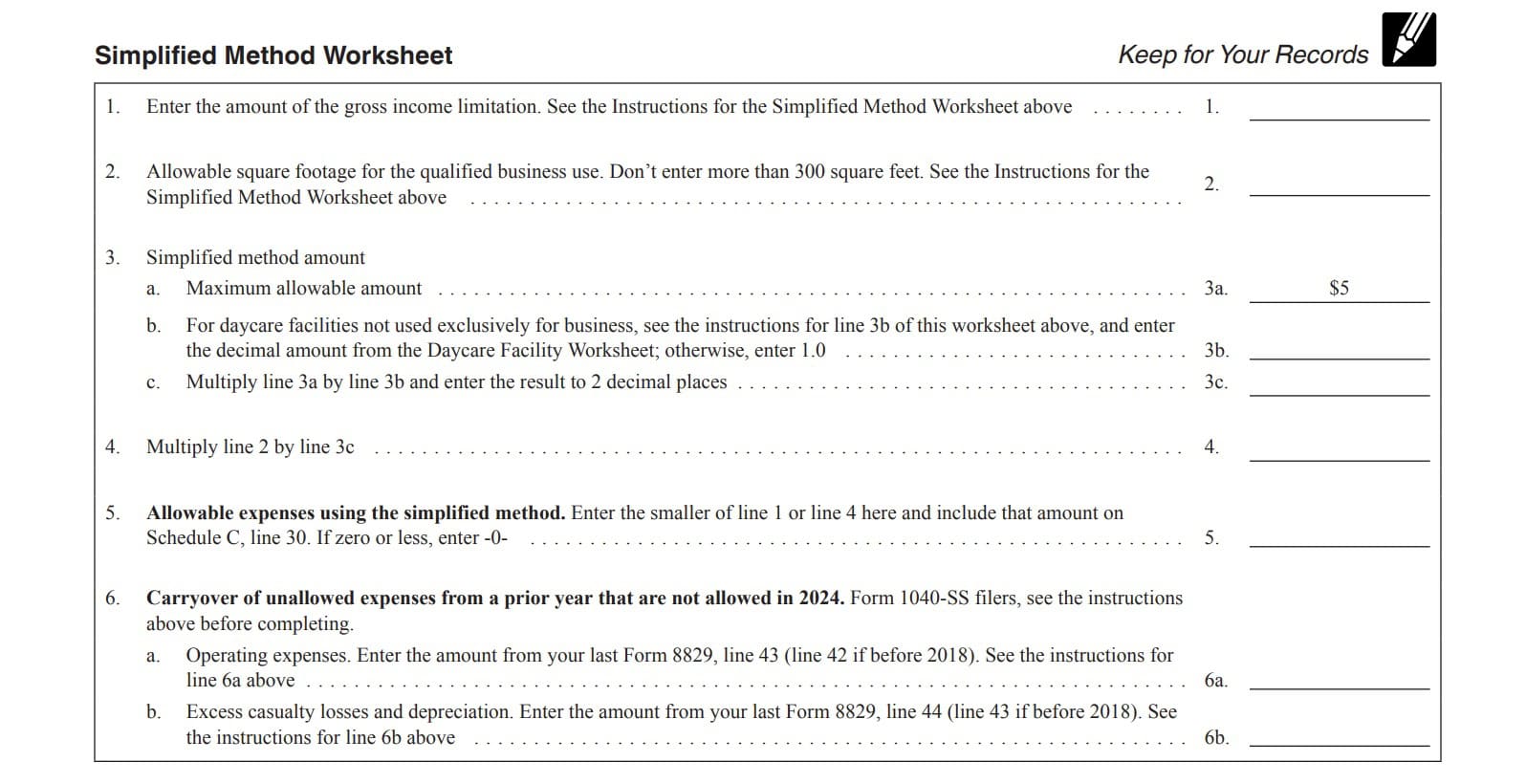

Line 30: Expenses for business use of your home

If you use your home for business use, you may enter expenses incurred in Line 30. There are two ways to do this:

- Complete and attach IRS Form 8829 with your tax return

- Simplified method, if you cannot, or do not wish to complete Form 8829

Simplified method

Simplified method filers will need to use the Simplified Method Worksheet, below, to determine the Line 30 amount. Also, the limit for home business expenses using the simplified method is $1500, or $5 times the maximum square footage allowed (300 square feet).

If your actual expenses exceed $1,500, you may be better off capturing them on IRS Form 8829.

Line 31: Net profit or (loss)

Subtract Line 30 from Line 29. This represents your net profit or loss from business activities.

If you recorded a loss from your business activities, you must go to Line 32 to determine whether at-risk rules apply to your tax situation.

Individual taxpayers

If you have recorded a net profit, enter your profit on the following:

- IRS Schedule 1, Line 3

- IRS Schedule SE, Line 2

Estates and trusts

Estates and trusts report profits on Line 3 of IRS Form 1041.

Line 32

Check either Line 32a or Line 32b, depending on how much of your investment is at risk. Check the box in Line 32b if any of the following conditions apply:

- Nonrecourse loans used to finance the business, to acquire property used in the business, or to acquire the business that are not secured by your own property (other than property used in the business).

- An exception exists for certain nonrecourse financing borrowed in connection with holding real property

- Cash, property, or borrowed amounts used in the business (or contributed to the business, or used to acquire the business) that are protected against loss by a guarantee, stop-loss

agreement, or other similar arrangement - Amounts borrowed for use in the business from a related person, or a person who has an interest in the business under IRC Section 465(b)(3)(C)

If you checked the box in Line 32b, you will need to complete IRS Form 6198, At-Risk Limitations, to determine the extent of the loss you can deduct on your personal tax return to calculate federal income taxes that you owe.

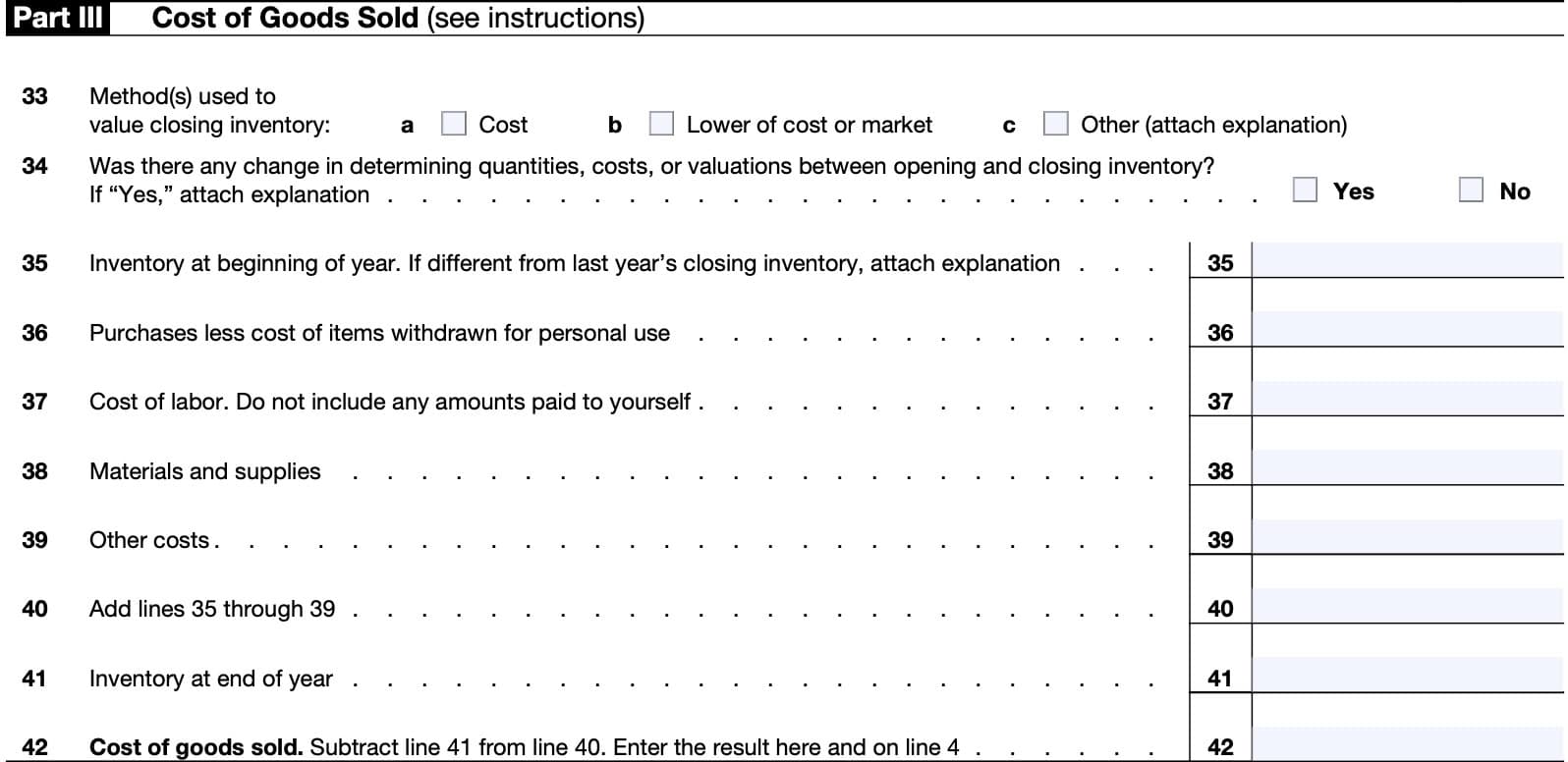

Part III: Cost of Goods Sold

In most cases, if you engaged in a trade or business where the production, purchase, or sale of merchandise was an income-producing factor, you must account for inventories at the beginning and at the end of your tax year.

If you are a small business taxpayer, you can choose not to keep an inventory, but you must still use a method of accounting for inventory that clearly reflects income.

Line 33: Method used to value closing inventory

You may select cost, lower of cost or market, or another method to value closing inventory. If using another method, attach an explanation that details how the IRS approved your inventory method.

Line 34

Indicate whether there was any change in your method of determining costs, valuations, or quantities between opening and closing inventories.

If there was a change, attach a written explanation.

Line 35: Inventory at beginning of year

Enter the inventory at the beginning of the tax year. If this amount is different from the closing inventory from the prior tax year, attach an explanation.

Line 36: Purchases less cost of items withdrawn for personal use

Enter the amount of purchases made throughout the year. Do not include any items that you withdrew for non-business purposes.

Line 37: Cost of labor

Enter the cost of labor. Do not include any compensation entered in another line, and do not include any amount that you paid to yourself.

Line 38: Materials and supplies

Enter the cost of materials and supplies purchased throughout the year.

Line 39: Other costs

Enter any other costs incurred during the year.

Line 40

Add Lines 35 through 39. Enter the total here.

Line 41: Inventory at end of year

Enter the value of inventory at the end of the tax year. This should match the beginning inventory for next year’s Schedule C.

Line 42: Cost of goods sold

Subtract Line 41 from Line 40. This represents the cost of goods sold.

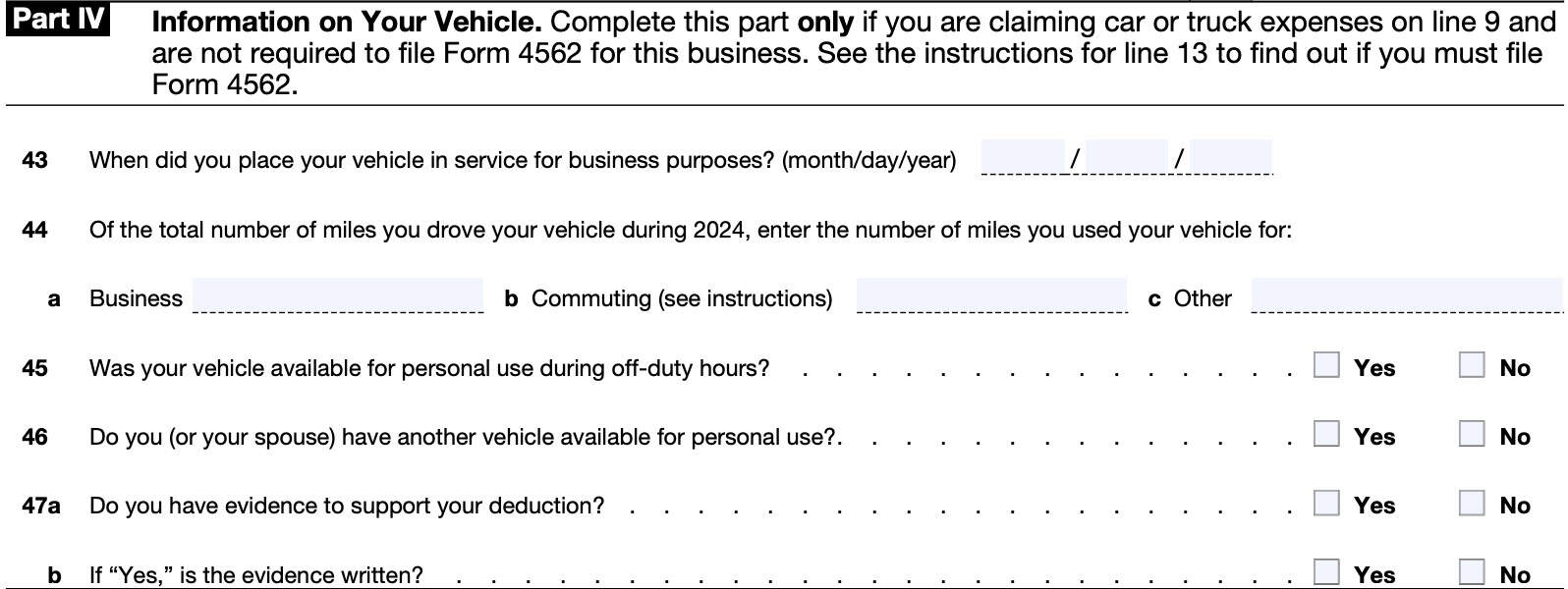

Part IV: Information on Your Vehicle

Only complete Part IV if:

- You are claiming car or truck expenses on Line 9, and

- You are not required to file IRS Form 4562, Depreciation and Amortization, for this business

Otherwise, proceed to Part V.

Line 43

In Line 43, enter the date you placed your vehicle into service, using MM/DD/YYYY format.

Line 44

In Line 44, enter the total number of miles that you drove your vehicle, as follows:

- Line 44a: Business

- Line 44b: Commuting

- Line 44c: Other

Commuting miles vs. business miles

In most cases, commuting is travel between your home and a work location. If you converted your vehicle during the year from personal to business use (or vice versa), you should enter your commuting miles only for the period you drove your vehicle for business.

Travel that meets any of the following conditions isn’t commuting:

- You have at least one regular work location away from your home and the travel is to a temporary work location in the same trade or business, regardless of the distance.

- A temporary work location is one where your employment is expected to last 1 year or less.

- The travel is to a temporary work location outside the metropolitan area where you live and normally work.

- Your home is your principal place of business under IRC Section 280A(c)(1)(A) (for purposes of deducting expenses for business use of your home) and the travel is to another work location in the same trade or business, regardless of whether that location is regular or temporary and regardless of distance

In other words, any mileage meeting the above requirements should be listed as business mileage, not commuting mileage.

Line 45

Indicate whether your vehicle was available for personal use during off duty hours.

Line 46

Indicate whether you or your spouse have access to another vehicle for personal use.

Line 47

Indicate whether you have evidence to support your tax deduction. If so, state whether the evidence is written down or otherwise verifiable. (i.e. mileage logs, electronic mileage tracking application, etc.).

IRS Publication 463, Travel, Gift, and Car Expenses, contains more information about documentation requirements. IRS Publication 583, Starting a Business and Keeping Records, contains additional details about electronic recordkeeping.

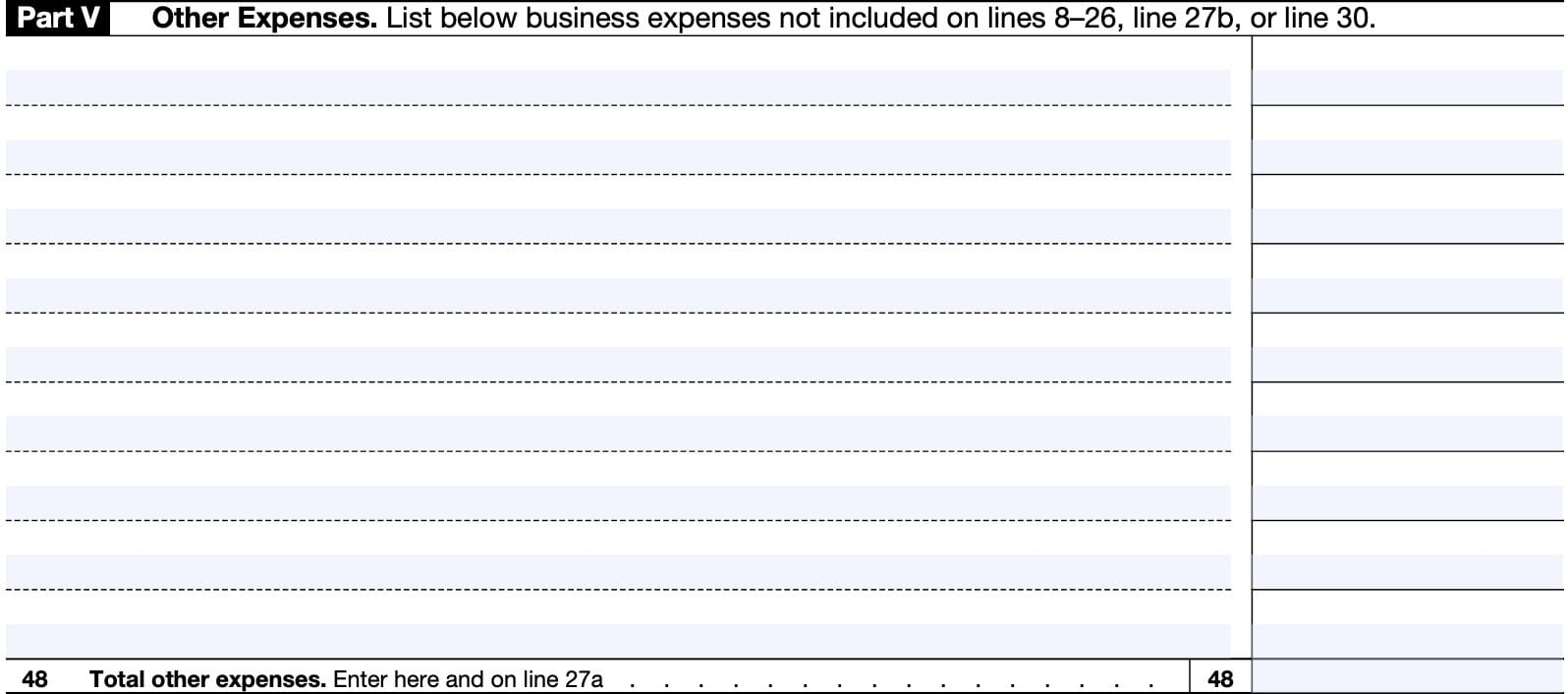

Part V: Other Expenses

In Part V, list other any ordinary and necessary expenses that you did not deduct elsewhere on the Schedule C tax form. List the type of expense and amount separately in the provided space.

Do not include any of the following:

- Cost of business furniture or equipment

- Replacements or permanent property improvements

- Personal, living, or family expenses

- Charitable contributions

- Fines or penalties paid to a government for law violations

Below are types of other expenses you can enter as tax deductions on Schedule C:

Amortization

You may be able to amortize the following expenses on IRS Form 4562:

- The cost of pollution-control facilities

- Amounts paid for research and experimentation

- Amounts paid to acquire, protect, expand, register, or defend trademarks or trade names; or

- Goodwill and certain other intangibles

At-risk loss deduction

A disallowed loss from the previous year because of the at-risk rules is treated as a deduction allocable to this business in the current tax year.

Bad debts

Include debts and partial debts from sales or services that were included in income and are definitely known to be worthless.

If you eventually collect on a debt that you had previously written off, you will have to declare that collected debt as income in the year you receive it.

Business startup costs

You can elect to deduct up to $5,000 of certain business startup costs.

This $5,000 limit is reduced (but not below zero) by the amount by which your total startup costs

exceed $50,000.

Your remaining startup costs can be amortized over a 180-month period (15 years), beginning with the month the business began.

Deduction for removing barriers to individuals with disabilities and the elderly

You may be able to deduct up to $15,000 of costs paid or incurred to remove architectural or transportation barriers to individuals with disabilities and the elderly.

However, you cannot take a tax credit on IRS Form 8826 for providing disabled access while taking a tax deduction for the same expenditures.

De minimis safe harbor for tangible property

If you elect to use the de minimis safe harbor for tangible property, you may deduct de minimis amounts paid to acquire or produce certain tangible property if these amounts are deducted by you for financial accounting purposes or in keeping your books and records.

If you have an applicable financial statement, you may deduct up to $5,000 per item or per invoice using the de minimis method. Otherwise, you may deduct up to $2,500 per item or invoice.

Energy efficient commercial buildings deduction

You may be able to deduct some or all of the costs for modifying a commercial building to make it more energy efficient. If applicable, complete IRS Form 7205 to determine your tax deduction.

Film and television and live theatrical production expenses

You can elect to deduct costs of certain qualified film and television productions or qualified live theatrical productions. IRS Publication 535 contains additional details.

Forestation and reforestation costs

Reforestation costs are generally capital expenditures.

However, for each qualified timber property, taxpayers can elect to expense up to $10,000 ($5,000 if married filing separately) of qualifying reforestation costs paid or incurred in the tax year.

You can elect to amortize the remaining costs over 84 months, or 7 calendar years.

What other tax forms do I need to complete when I file Schedule C?

The IRS Schedule C instructions contains a long list of tax forms that taxpayers may need to complete when filing Schedule C. Below is a list of tax forms and schedules that have not already been mentioned in this article.

Tax schedules not previously mentioned

Below are tax schedules, not previously mentioned in this article, that taxpayers may need to file with Schedule C.

IRS Schedule E

Taxpayers may file IRS Schedule E to report rental real estate and royalty income not subject to self-employment tax.

IRS Schedule F

Farmers use IRS Schedule F to report profits or losses from farming activities.

IRS Schedule J

Farmers and fishermen may file Schedule J to calculate their tax liability by averaging farming or fishing income over the previous 3 year period. This may reduce their overall tax bill.

Tax forms not previously mentioned

Below are tax forms, not previously mentioned in this article, that taxpayers may need to file with Schedule C.

IRS Form 461

Use IRS Form 461 to report excess business losses.

IRS Form 3800

Use IRS Form 3800 to report general business credits.

IRS Form 4684

Taxpayers may file IRS Form 4684 to report a casualty or theft gain or (loss) involving property used in trade or business or income-producing property.

IRS Form 4797

Taxpayers use IRS Form 4797 to report the following transactions involving trade or business property:

- Sales

- Exchanges

- Involuntary conversions

- Not from casualty or theft

IRS Form 6252

Taxpayers file IRS Form 6252 to report income from installment sales.

IRS Form 8594

File IRS Form 8594 to report certain purchases or sales of groups of assets that comprise a trade or business.

IRS Form 8824

Use IRS Form 8824 to report like-kind exchanges.

IRS Form 8960

Taxpayers file IRS Form 8960 to report and pay net investment income tax on certain income from passive activities.

IRS Form 8995/IRS Form 8995-A

Taxpayers may use either IRS Form 8995 or IRS Form 8995-A to claim a tax deduction on qualified business income.

Video walkthrough

Watch this instructional video for step by step guidance on reporting your business profit or loss on IRS Schedule C.

Do you use TurboTax?

If you use TurboTax, and you’re completing this tax form for the first time, you might be ready to try TurboTax Federal Premium instead of the free or deluxe versions. TurboTax Federal Premium comes in two offerings, DIY or Live Assisted.

Do it yourself

To learn more about using TurboTax Federal Premium’s DIY option, click here.

Live Assisted

If you feel more comfortable having a tax expert guide you for the first time through this new form (or any other new forms), get started here.

Ready to hand the reins over to someone else completely? Go here to learn more about TurboTax’s Live Assisted Full Service offering!

Frequently asked questions

Taxpayers generally file Schedule C to report income they made as a sole proprietor. However, they may also use Schedule C to report earnings as a statutory employee, income and deductions of certain qualified joint ventures, or certain amounts shown on Form 1099.

Taxpayers may use Schedule C to report profit or loss from a sole proprietorship on IRS Form 1040 or Form 1041. However, partnerships generally must file IRS Form 1065 to report profit or loss from the partnership.

You may be able to deduct certain expenses related to the business use of your home if they meet certain IRS criteria. You can deduct actual expenses paid or use the simplified method worksheet located in the Schedule C instructions to calculate your business use deduction.

Where can I find IRS Schedule C?

You can find this schedule on the IRS website. For your convenience, we’ve attached the latest version to the article, below.

Related tax articles

This tax form is one of the fillable tax forms provided by the Internal Revenue Service, to help taxpayers reduce their tax preparation costs. To see more forms like this, visit our free fillable tax forms page, where you’ll also find articles like this.

Unlike the IRS, our articles contain step by step instructions for each tax form, as well as video walkthroughs. You can also check out all of our videos by subscribing to our YouTube channel!

This is so incredibly helpful…..I just have a question about filing separate in a community state where one spouse has a W2 and the other has a 1099NEC and has to do this form.

Do I put half the final amount on my spouses form, or do I have to put half the exact amount on the 1099NEC without the deductions?

I’m so confused….

Thanks!

For married couples filing separate returns in a community property state, the IRS generally will want you to complete IRS Form 8958. This helps properly allocate income items equally on each spouse’s return. If you go step by step through Form 8958, it should help you account for all income items, deductions, and credits.

Below are links to an article and video we created to cover this tax form.

IRS Form 8958, Allocation of Tax Amounts Between Certain Individuals in Community Property States

Article: https://www.teachmepersonalfinance.com/irs-form-8958-instructions/

Video: https://youtu.be/Kbxa_uDIbMI