IRS Form 8995-A Instructions

In 2017, Congress passed the Tax Cuts and Jobs Act (TCJA), which created the qualified business income deduction to help business owners mitigate the impact of double taxation. The Internal Revenue Service (IRS) created a new tax form, IRS Form 8995, to help provide a simplified computation of their new deduction. In this article, we’ll review the complete version of that tax form, IRS Form 8995-A.

We’ll cover some of the basics of this tax form, to include:

- Key differences between Form 8995 and Form 8995-A

- Background information on the qualified business income deduction

- How to complete IRS Form 8995-A

Let’s start with some background information on the form itself.

Table of contents

How do I complete IRS Form 8995-A?

This two-page tax form has four parts. We’ll go through everything, step by step. But beforehand, let’s review each of the schedules to better understand when they must be completed.

Although the schedules are not included in this article, each section contains the IRS website link so you can download each schedule as required. If a given schedule is required, you must complete that schedule before starting Part I.

The form instructions for Form 8995-A contain additional guidance for each schedule.

Schedule A: Specified Service Trades or Businesses

Complete Schedule A only if:

- Your trade or business is a SSTB and

- Your taxable income is:

- More than $191,950 but not over $241,950 (for all filers except married couples filing jointly)

- More than $383,900 but not $483,900 (for married couples filing a joint tax return)

Owners of a publicly-traded partnership (PTP) need to complete Part II. All others need to complete Part I.

Simplified QBI computation

If your taxable income isn’t more than $191,950 ($383,900 if married filing jointly) and you’re not a patron of an agricultural or horticultural cooperative, don’t file this form. Instead, file IRS Form 8995, Qualified

Business Income Deduction Simplified Computation.

Otherwise, complete Schedule D (IRS Form 8995-A) before beginning Schedule A.

If your taxable income is more than $241,950 ($483,900 if married filing jointly), your specified service trade or business doesn’t qualify for the deduction.

More than 3 trades or businesses

If you have more than three trades or businesses, attach as many Schedules A as needed.

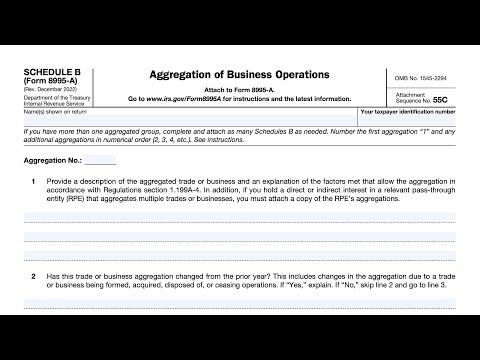

Schedule B: Aggregation of Business Operations

Complete Schedule B if you qualify and choose to aggregate multiple trades or businesses into a single trade or business for tax reporting services.

Schedule C: Loss Netting and Carryforward

You must complete Schedule C if:

- Any of your trades, businesses, or aggregations have a qualified business loss for the current year, or

- You have a qualified business net loss carryforward from prior years

This includes prior year loss carryforwards even if the loss was unreported or the trade or business that generated the loss is no longer in existence.

Schedule C (Form 8995-A) offsets your trade or business that generated a qualified business loss against the QBI from your other trades or businesses. The qualified business loss must be apportioned among all your trades or businesses with QBI in proportion to their QBI.

Schedule D: Special Rules for Patrons of Agricultural or Horticultural Cooperatives

You must complete Schedule D if you’re a patron in a specified agricultural or horticultural cooperative and are claiming a QBI deduction in relation to your trade or business conducted with the cooperative. Section 199A(g)(3) contains more details.

If you have more than three trades, businesses, or aggregations, attach as many Schedules D as needed.

Let’s turn our focus to Form 8995-A itself.

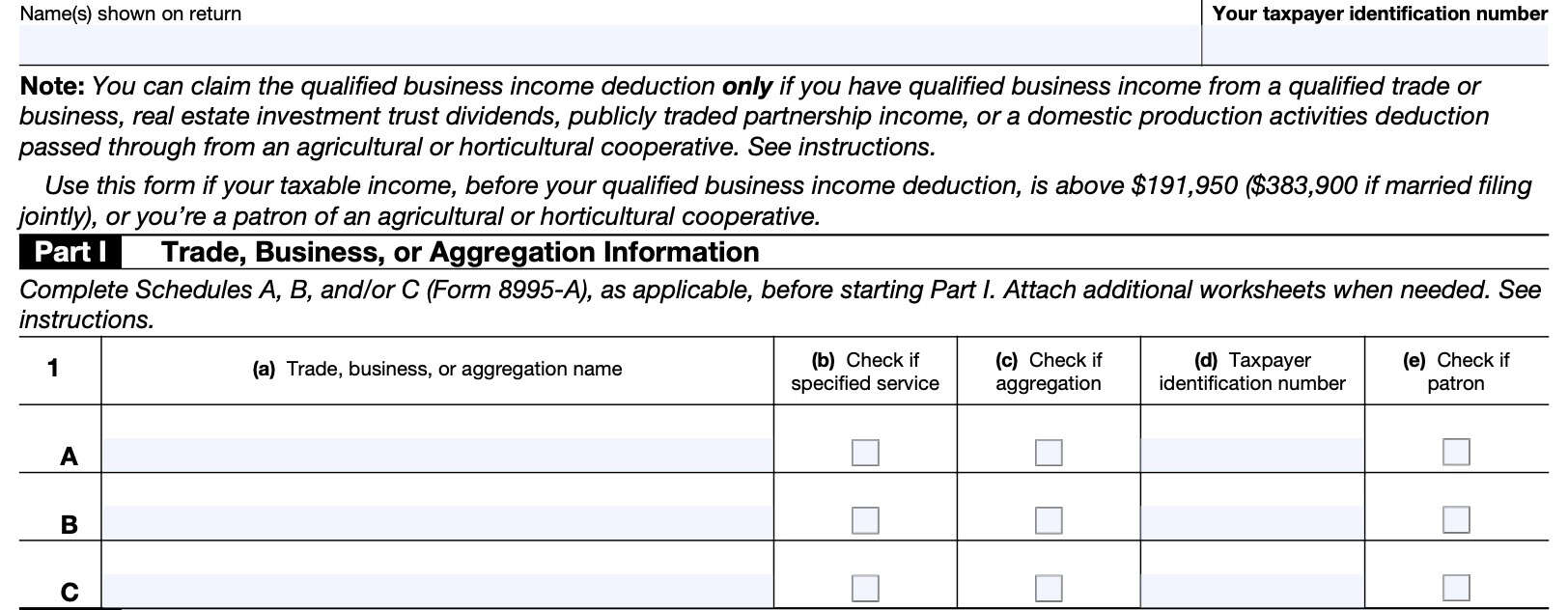

Part I: Trade, Business, or Aggregation Information

Complete accompanying schedules first

Before starting Part I, taxpayers must complete Schedules A, B, C, and/or D as appropriate. The form instructions provide the following guidance to help taxpayers determine whether they need to complete each schedule.

- Do you have an SSTB? If yes, then you must complete Schedule A.

- Are you choosing to aggregate multiple trades or businesses into a single trade or business? If yes, complete Schedule B (Form 8995-A) before starting Part I.

- Did any of your trades, businesses, or aggregations have QBI for the year or do you have a qualified business loss carryforward from prior years? If yes, complete Schedule C (Form 8995-A) before starting Part I.

- Are you a patron of an agricultural or horticultural cooperative? If yes, then you must complete Schedule D.

When is Part I required?

Only complete Part I if you have QBI. If you only have REIT, PTP, and/or a domestic production activities deduction (DPAD), then skip Part I, Part II, and Part III, and proceed to Part IV.

Line 1

If you completed Schedule B, enter the aggregation name in 1(a). Check the appropriate boxes, as required. For taxpayer identification number, enter the employer identification number (EIN), if one exists. Otherwise, enter the Social Security number (SSN) or individual taxpayer identification number (ITIN).

There are 3 lines, for up to 3 businesses. Add additional worksheets as needed.

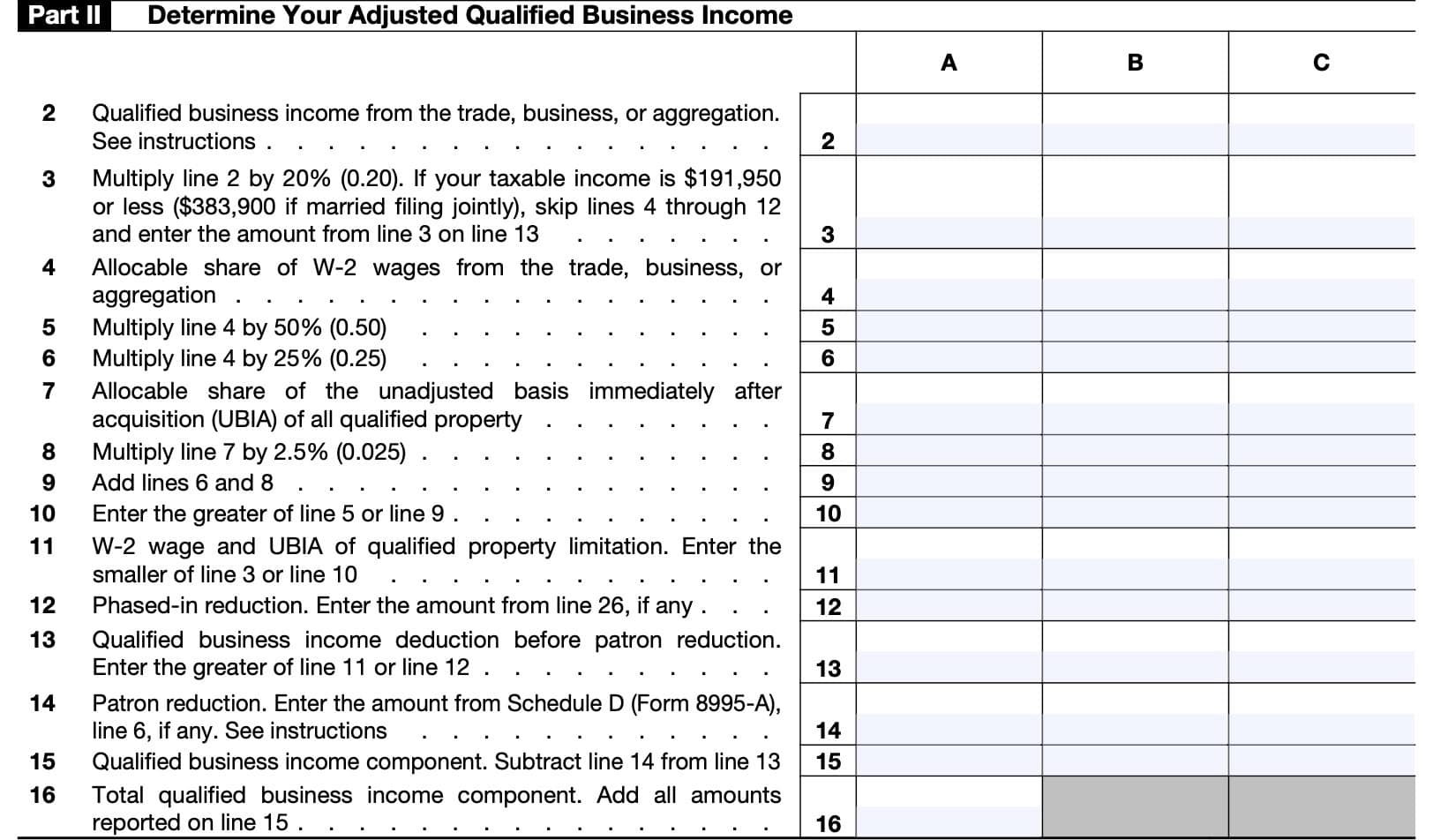

Part II. Determine Your Adjusted Qualified Business Income

Use Part II to calculate the QBI component from your qualified trade, business, or aggregation.

Line 2: QBI from the business, trade, or aggregation

Enter your QBI from each business.

If you have four or more trades or businesses, attach a statement with the information for Parts I, II, and III, as applicable.

Line 3

Self-explanatory. If your income is under the stated thresholds, skip Lines 4-12 and enter the amount from Line 3 directly onto Line 13.

Note: At the time this article was written, the 2022 version of this tax form was not available. This article will be updated when the 2022 version is online.

Line 4: Allocable share of W-2 wages

Enter any W-2 wages from the specific trade, business, or aggregation. If the QBI on Line 2, for the trade, business, or aggregation, is zero, then the amount reported on Line 4, for that trade or business, must also be zero.

Line 5

Multiply Line 4 by 50%.

Line 6

Line 7: UBIA of qualified property

Enter your share of the unadjusted basis immediately after acquisition (UBIA) for all qualified property for the trade or business.

If the QBI on Line 2, for the trade, business, or aggregation, is zero, then the amount reported on Line 7, for that trade or business, must also be zero.

Line 8

Multiply Line 7 by 2.5% (0.025).

Line 9

Add Lines 6 and 8 and enter the total.

Line 10

Enter the greater of:

- Line 5

- Line 9

Line 11: W-2 wage and UBIA of qualified property limitation

Enter the smaller of:

- Line 3

- Line 10

Line 12: Phased-in reduction

Enter the amount from Line 26, if any. Line 26 is located in Part III.

Line 13: QBI deduction before patron reduction

Enter the greater of:

Line 14: Patron reduction

If you’re a patron of an agricultural or horticultural cooperative, complete Schedule D (Form 8995-A) before completing Line 14. Report the amount from Schedule D (Form 8995-A), Line 6, if any.

Patrons of agricultural or horticultural cooperatives are required to reduce their QBI component by the lesser of:

- 9% of QBI allocable to qualified payments from a specified cooperative, or

- 50% of W-2 wages allocable to qualified payments.

Line 15

Subtract the patron reduction on Line 14 from the amount on Line 13. If zero or less, enter zero.

Line 16

Add all amounts reported on Line 15. If there are four or more trades or businesses, then include Line 15 amounts from all trades or businesses and complete Line 16 only on the first page.

Leave Line 16 blank on the attached statements.

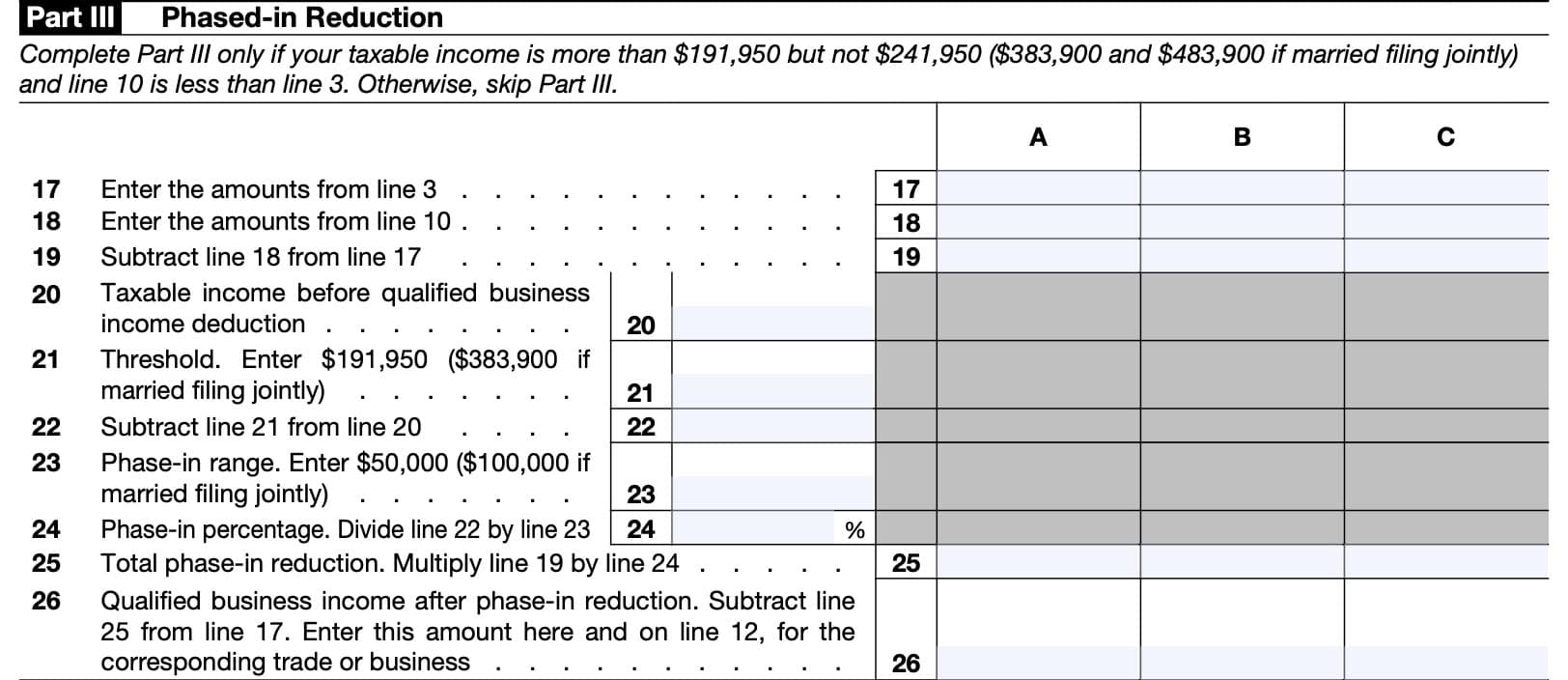

Part III. Phased-in Reduction

Only complete Part III if your income falls in the phase-out range:

- More than $170,050 but not $220,050 (for all filers except married couples filing jointly)

- More than $340,100 but not $440,100 (for married couples filing a joint tax return)

Line 17

Enter the amounts from Line 3 (Part II).

Line 18

Enter the amounts from Line 10 (Part II).

Line 19

Subtract Line 18 from Line 17.

Line 20: Taxable income before QBI deduction

Enter your taxable income before QBI deduction as determined by one of the following:

- Form 1040, 1040-SR, or 1040-NR filers: Line 11, minus Line 12c

- Form 1041 filers: Line 23, plus Line 20

- Form 1041-N filers: Line 13, plus qualified income deduction reported on Line 9.

- Form 990-T filers: Line 11, plus qualified business income deduction reported on Line 9

- S corporation portion of an ESBT filer: ESBT Tax Worksheet, Line 13, plus ESBT Tax Worksheet, Line 11

Line 21: Threshold

Enter either of the following:

- $170,050 (unless married filing jointly)

- $340,100 (married filing jointly)

Line 22

Subtract Line 21 from Line 20.

Line 23: Phase-in range

Enter either of the following:

- $50,000 (unless married filing jointly)

- $100,000 (married filing jointly)

Line 24: Phase-in percentage

Divide Line 22 by Line 23.

Line 25: Total phase-in reduction

Multiply Line 19 by Line 24.

Line 26: QBI after phase-in reduction

Subtract Line 25 from Line 17. Enter this amount here and on Line 12.

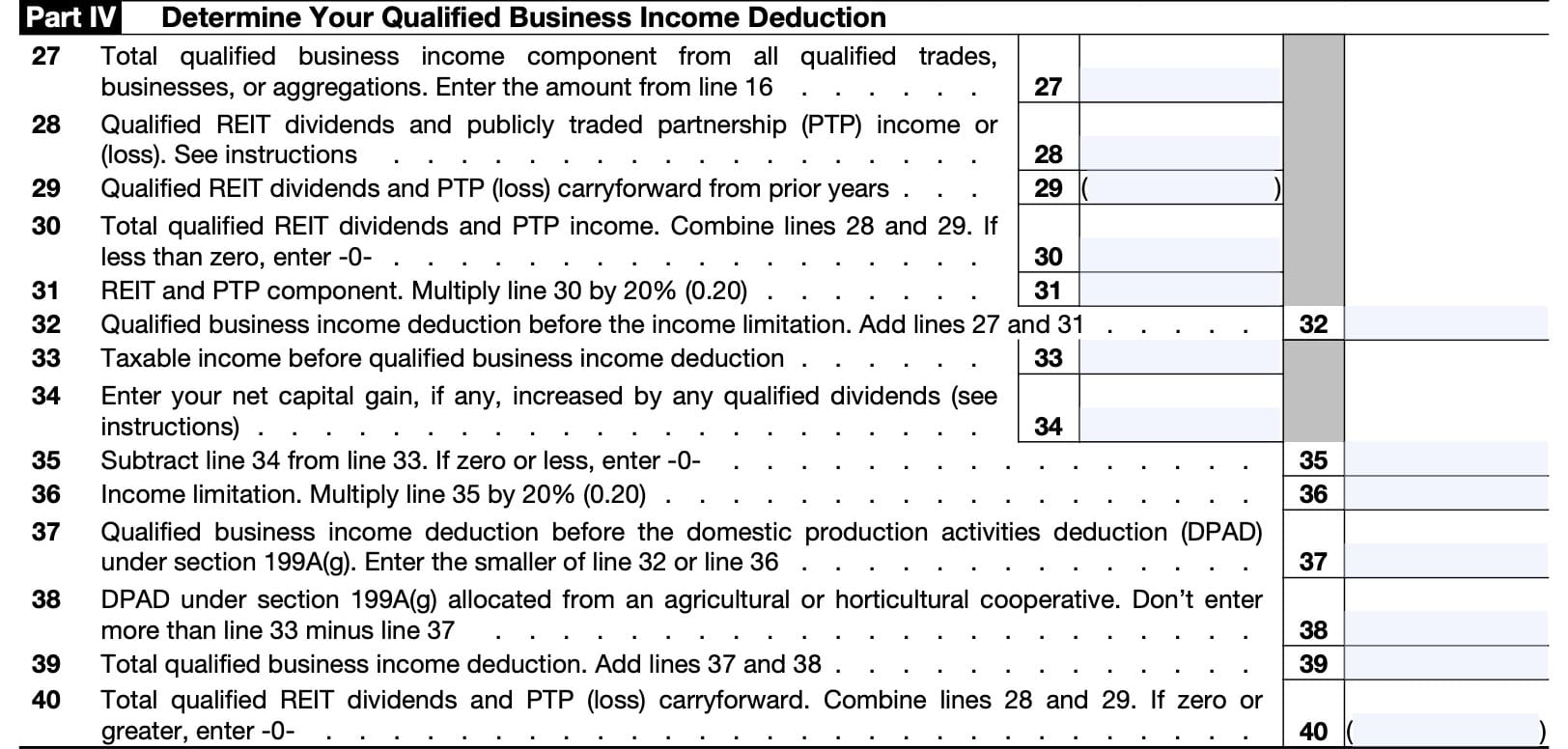

Part IV. Determine Your Qualified Business Income Deduction

All taxpayers claiming a QBI deduction must complete Part IV.

Line 27: Total QBI component from qualified trades, businesses, or aggregations

Enter the amount found on Line 16.

Line 28: Qualified REIT dividends and PTP income/loss

If the net amount is a loss, enter as a negative number.

Any negative amount will be carried forward to the next year. This carryforward doesn’t affect the deductibility of the loss for purposes of any other provisions of the Internal Revenue Code.

Line 29: Qualified REIT dividends and PTP (loss) carryforward from prior years

If you have any carryforward from a prior tax year, enter that number here.

Line 30: Total qualified REIT dividend and PTP income

Combine Lines 28 and 29. If less than zero, enter ‘0.’

Line 31: REIT & PTP component

Multiply Line 30 by 20% (0.20).

Line 32: QBI deduction before income limitation

Add Lines 27 and 31.

Line 33: Taxable income before QBI deduction

Enter the same number that you entered on Line 20 (Part III). If you did not complete Part III, enter your taxable income before QBI deduction as determined by one of the following:

- Form 1040, 1040-SR, or 1040-NR filers: Line 11, minus Line 12c

- Form 1041 filers: Line 23, plus Line 20

- Form 1041-N filers: Line 13, plus qualified income deduction reported on Line 9.

- Form 990-T filers: Line 11, plus qualified business income deduction reported on Line 9

- S corporation portion of an ESBT filer: ESBT Tax Worksheet, Line 13, plus ESBT Tax Worksheet, Line 11

Line 34: Net capital gain

Enter the amount from your tax return as follows

- Form 1040, 1040-SR, or 1040-NR filers: Qualified dividends on line 3a, plus your net capital gain.

- If you’re not required to file Schedule D (Form 1040), your net capital gain is the amount reported on Line 7.

- If you file Schedule D (Form 1040), your net capital gain is the smaller of Schedule D Line 15 or 16. If either line is zero or less, nothing is added to your qualified dividends

- Form 1041 filers: Line 2b(2).

- For estates or trusts required to file Schedule D (Form 1041), add the qualified dividends to the smaller of Schedule D Line 18a(2), or Line 19(2). If either line is zero or less, nothing is added to your qualified dividends.

- Form 1041-N filers: Line 2b, plus the smaller of Form 1041-N, Schedule D, Lines 10 or 11.

- If line 10 or 11 is zero or less, e nothing is added to your qualified dividends.

- Form 990-T filers who are trusts: Schedule D (Form 1041), the smaller of line 18(a)(2) or 19(2), unless either line 18(a)(2) or 19(2) is zero or less, in which case the net capital gain for purposes of section 199A is zero.

- S-corporation portion of an ESBT, your ESBT Tax Worksheet, line 2b, plus the smaller of your ESBT’s Schedule D (Form 1041), line 18(a)(2), or line 19(2), is zero or less, in which case nothing is added to your qualified dividends.

Line 35

Subtract Line 34 from Line 33. If zero or less, enter ‘0.’

Line 36: Income limitation

Multiply Line 35 by 20% (0.20).

Line 37: QBI deduction before DPAD

Enter the smaller of:

- Line 32

- Line 36

Line 38: DPAD under Section 199A(g) allocated from an agricultural or horticultural cooperative

Do not enter more than Line 33 minus Line 37.

Line 39: Total QBI deduction

Add Lines 37 and 38. Enter this amount on one of the following:

- Form 1040 or 1040-SR: Line 13

- Form 1040-NR: Line 13a

- Form 1041: Line 20

- Form 1041-N: Line 9

- Form 990-T: Line 9

- S-corporation portion of an ESBT: Line 11

Line 40: Total qualified REIT dividends and PTP (loss) carryforward

Combine Lines 28 and 29. If zero or greater, enter ‘0.’ If negative, this number must be carried forward to subsequent years.

What is IRS Form 8995-A?

IRS Form 8995-A, Qualified Business Income Deduction, is the tax form that certain taxpayers must use when they cannot use the simplified computation method for determining their qualified business income (QBI) deduction in the current year on Form 8995.

Taxpayers must use Form 8995-A if they have QBI, qualified REIT dividends, or qualified PTP income or loss, and either of the following apply:

- Taxable income before QBI deduction is above the QBI threshold amount:

- $170,050 if single, married filing separately, head of household, qualifying widow(er), or are a trust or estate,

- $340,100 if married filing jointly

- Taxpayer belongs to either an agricultural or horticultural cooperative

In addition to a lengthier tax form, Form 8995-A also has 4 schedules that each taxpayer should know about:

- Schedule A: Specified Service Trades or Businesses

- Schedule B: Aggregation of Business Operations

- Schedule C: Loss Netting and Carryforward

- Schedule D: Special Rules for Patrons of Agricultural or Horticultural Cooperatives

Before moving on, we should probably cover a couple of key definitions.

What is the qualified business income deduction?

Individual taxpayers and some trusts and estates may be entitled to a deduction of up to 20% of:

- Net QBI from a trade or business, which includes income from a pass-through entity

- Qualified real estate investment trust (REIT) dividends

- Qualified publicly traded partnership (PTP) income

Examples of pass-through entities include:

- Sole proprietorships

- S corporations

- Limited liability partnerships

- Limited liability companies

Net QBI does not include income from a C corporation.

The total QBI deduction is limited to the lesser of:

- The QBI component plus the REIT/PTP component, or

- 20 percent of the taxable income minus net capital gains

What is qualified business income?

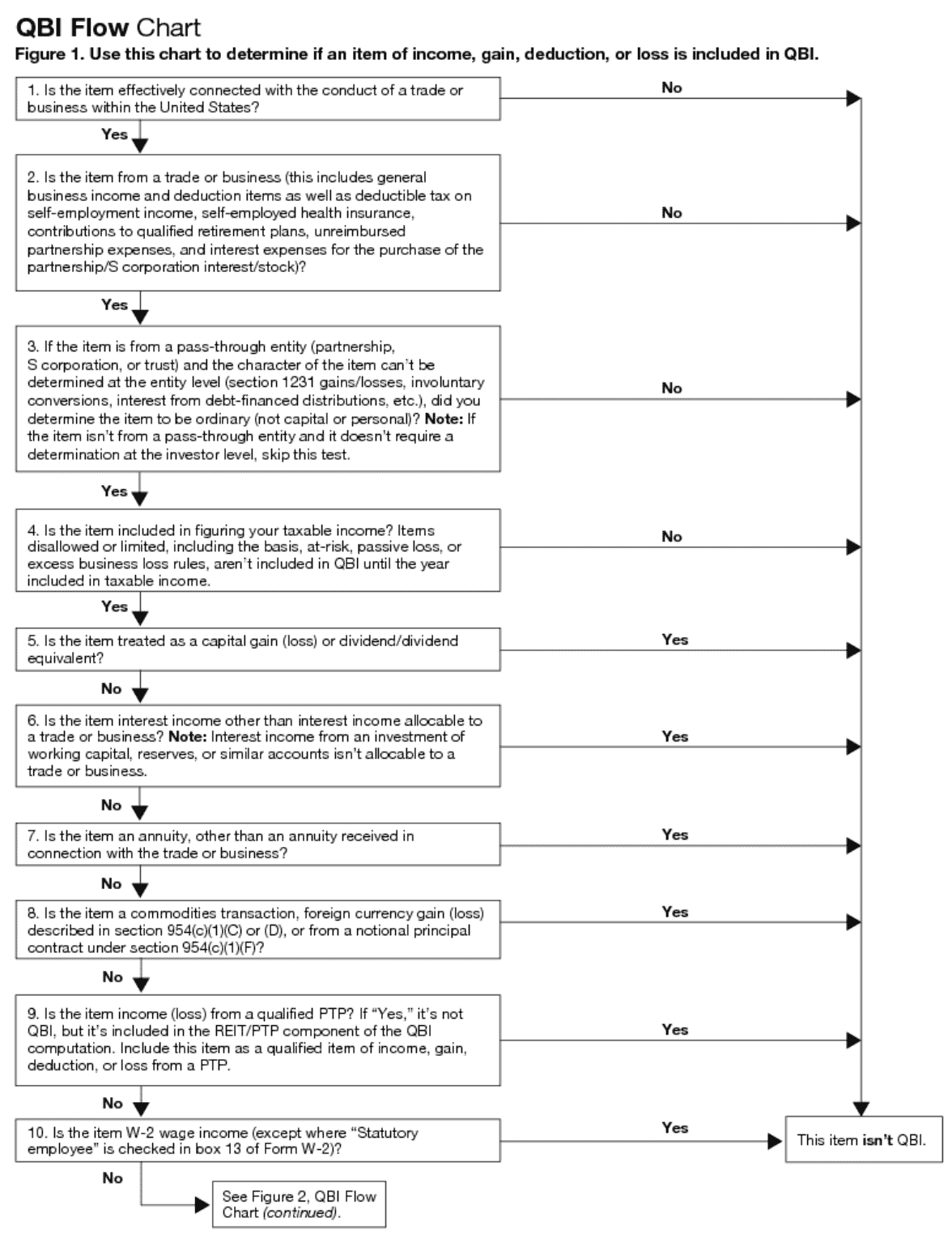

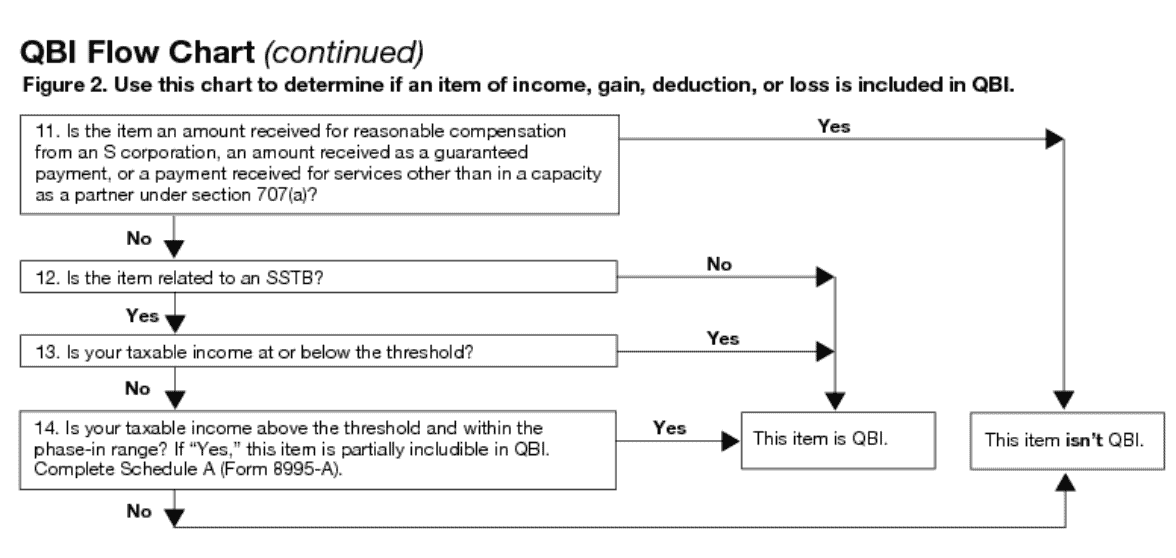

The IRS defines QBI as the “net amount of qualified items of income, gain, deduction and loss from any qualified trade or business.” This includes income from partnerships, S-corporations, sole proprietorships, and certain trusts.

The IRS contains two flow charts to help taxpayers determine whether or not an item is included in QBI calculations.

Assuming you complete Figure 1 without excluding the item as a QBI component, Figure 2 contains a few more items to determine inclusion as QBI.

What is a qualified trade or business?

According to the IRS website, a qualified trade or business is any Section 162 trade or business, except for:

- Any trade or business conducted by a C corporation

- Any services performed as an employee

- Specified service trades or businesses for taxpayers with taxable income exceeding the threshold amount in the given tax year

What is a specified service trade or business?

The IRS defines a specified service trade or business (SSTB) as:

“A trade or business involving the performance of services in the fields of health, law, accounting, actuarial science, performing arts, consulting, athletics, financial services, investing and investment management, trading or dealing in certain assets, or any trade or business where the principal asset is the reputation or skill of one or more of its employees or owners. The principal asset of a trade or business is the reputation or skill of its employees or owners if the trade or business consists of the receipt of income from endorsing products or services, the use of an individual’s image, likeness, voice, or other symbols associated with the individual’s identity, or appearances at events or on radio, television, or other media formats.”

Tax Cuts and Jobs Act, Provision 11011 Section 199A – Qualified Business Income Deduction FAQs

Are you tired of dreading tax season?

If you’re like most people, you push through the stress of filing, only to be hit with a bigger bill than expected—then put it all behind you until the same cycle repeats next year.

But what if you could change the game?

Tax planning puts you in control. It’s about being proactive, not reactive—taking small, smart steps throughout the year to reduce your tax burden, increase your savings, and keep more of your hard-earned money working for you.

Here’s what effective tax planning helps you do:

✅ Avoid the surprise of a high tax bill

✅ Understand how your income and decisions affect your taxes

✅ Strategically lower your tax liability over time

Ready to make smarter tax moves?

👉 Join my free weekly tax planning newsletter and get one actionable tip every week to help you reduce your taxes legally and effectively.

Start taking control—your future self will thank you.

Video walkthrough

Where can I find IRS Form 8995-A?

You may download this form from the IRS website or by selecting the file below.

This tax form is one of the fillable tax forms provided by the Internal Revenue Service, to help taxpayers reduce their tax preparation costs. To see more forms like this, visit our free fillable tax forms page, where you’ll also find articles like this.

Unlike the IRS, our articles contain step by step instructions for each tax form, as well as video walkthroughs. You can also check out all of our videos by subscribing to our YouTube channel!