IRS Form 1099-PATR Instructions

If you are an investor in a cooperative, you may receive taxable distributions throughout the year, based upon the cooperative’s income. At the end of the year, the cooperative may issue IRS Form 1099-PATR, Taxable Distributions Received From Cooperatives.

In this article, we’ll walk through this tax form, including:

- Step by step guidance on understanding the information on IRS Form 1099-PATR,

- How to report income items on your tax return

- Which items may be deductible as tax credits on your return

- Other frequently asked questions

Let’s start with a step by step walkthrough of IRS Form 1099-PATR.

Table of contents

IRS Form 1099-PATR Instructions

In most of our articles, we walk you through how to complete the tax form.

However, since Form-1099 is issued to taxpayers for informational purposes, most readers will probably want to understand the information reported on their 1099-PATR form, instead of how to complete it.

Before we start breaking down this tax form, it’s important to understand that there can be up to 3 versions of 1099-PATR forms.

Here is a break down of where all these forms end up:

- Copy A: Internal Revenue Service center

- Copy B: For recipient’s tax records

- Copy C: For payer’s tax records

Let’s first look at the taxpayer information on the left-hand side of the form.

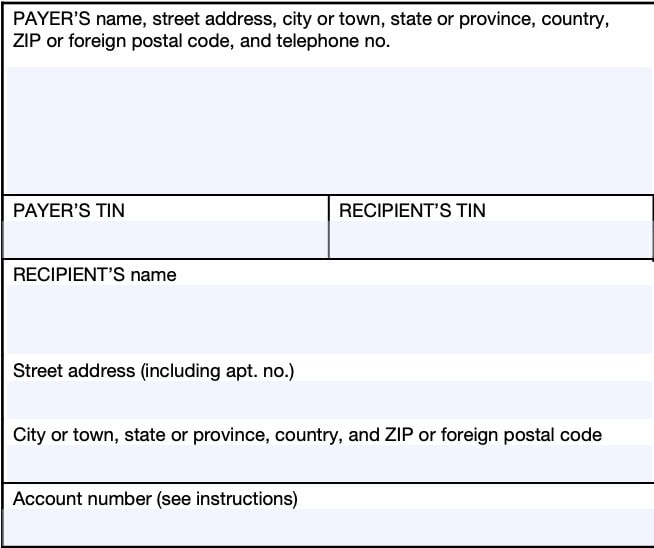

Taxpayer Information

On the left side, you’ll see the information for both the payer and the recipient. You’ll want to review these for accuracy.

Payer’s Name, Address, And Telephone Number

You should see the cooperative’s complete name, address, and telephone number in this field.

Payer’s TIN

This is the payer’s taxpayer identification number (TIN). In most situations, this will be the employer identification number (EIN).

The payer’s TIN should never be truncated.

Recipient’s TIN

As the recipient or payee, you should see your taxpayer identification number in this field. For payees, the TIN can be any of the following:

- Social Security number (SSN)

- Individual taxpayer identification number (ITIN)

- Adoption taxpayer identification number (ATIN)

- Employer identification number (EIN)

Please review this field to make sure that it is correct.

However, you may only see part of your taxpayer identification number (such as the last four digits of your SSN), for privacy protection purposes. Copy A, which the financial institution sends directly to the Internal Revenue Service, will not be truncated.

If you do not provide a TIN, your interest payments may be subject to backup withholding rules. To avoid backup withholding, you may want to obtain a Social Security number, ITIN, or EIN (for trusts and estates):

- Complete Form SS-5 to obtain a Social Security number

- Complete Form W-7 to obtain an ITIN

- File Form SS-4 for an Employer Identification Number (estates and trusts)

Recipient’s Name And Address

You should see your name and street address reflected in these fields. If your address is incorrect, you should notify the financial institution and the IRS.

You can notify the IRS of your new address by filing IRS Form 8822, Change of Address. Business owners can notify the IRS of a change in their business address by filing IRS Form 8822-B, Change of Address or Responsible Party, Business.

Account Number

This field may show an account or other unique number the payer has assigned to distinguish your account.

The Internal Revenue Service requires cooperatives to list an account number in this field for any recipients who have multiple accounts with the same cooperative and if the cooperative is issuing more than one Form 1099-PATR.

In all other instances, the IRS encourages, but does not mandate the use of an account number.

Next, let’s look at the numbered boxes on the right-hand side of the form.

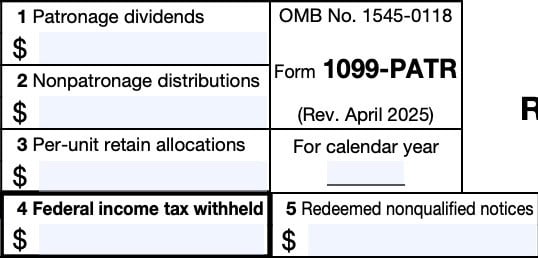

Boxes 1 through 13

At the top, you’ll see information that might appear unfamiliar if you’ve never seen it before. Let’s take a look at each box, one at a time, to get a better understanding.

Box 1: Patronage Dividends

Box 1 will show patronage dividends paid to you during the tax year as allowed by Internal Revenue Code Section 1382(b)(1) in the form of one or more of the following:

- Cash

- Qualified written notices of allocation, at face value, or

- Other property

- Not including nonqualified written notices of allocation

Dividends are not considered taxable if paid on:

- Property bought for personal use, or

- Capital assets or depreciable property used in your business

However, dividends paid on capital assets or business property may reduce the basis of those assets.

Individual taxpayers: Unless nontaxable, you must enter any income items reported on Box 1 as ordinary income on your federal tax return.

Box 2: Nonpatronage distributions

Box 2 will show nonpatronage distributions paid to you during the calendar year in the form of:

- Cash

- Qualified written notices of allocation

- Other property (except nonqualified written notices of allocation)

- Amounts you received in redemption of nonqualified written notices of allocation from nonpatronage sources

Farmers’ cooperatives

Farmers’ cooperatives that are tax-exempt under IRC Section 521 may enter the patron’s share (your share) of the total amount paid on a patronage basis with respect to the cooperative’s earnings from business done for:

- The United States or any federal agency, or

- Nonpatronage sources allowable as a tax deduction under IRC Section 1382(c)(2)(A)

Individual taxpayers: Unless nontaxable, you must enter any income items reported on Box 2 as ordinary income on your federal tax return.

You also must report any redemptions reported in Box 5 as ordinary income to the extent of the stated dollar value, because they were not taxable when first issued to you.

Box 3: Per-unit retain allocations

Box 3 will show patronage per-unit retain allocations paid to you during the year either:

- Cash

- Qualified per-unit retain certificates, or

- Other property, not including nonqualified per-unit retain certificates

Individual taxpayers: Unless nontaxable, you must enter any income items reported on Box 3 as ordinary income on your individual tax return.

Box 4: Federal Income Tax Withheld

Shows backup tax withholding.

Under backup withholding rules, a payer must backup withhold if:

- You did not provide your taxpayer identification number (TIN), or

- You provide an incorrect TIN

When filing Form 1099-PATR, your co-op owner must include taxes withheld on patronage payments in cash or qualified check as reported in:

IRS Form W-9 instructions contain more information on backup withholding. You should include this amount on your income tax return as tax withheld.

Box 5: Redeemed Nonqualified Notices

Box 5 amounts that you received when you redeemed nonqualified written notices of allocation and nonqualified per-unit retain allocations from patronage sources.

Individual taxpayers must these Form 1099-PATR amounts as ordinary taxable income on their tax return.

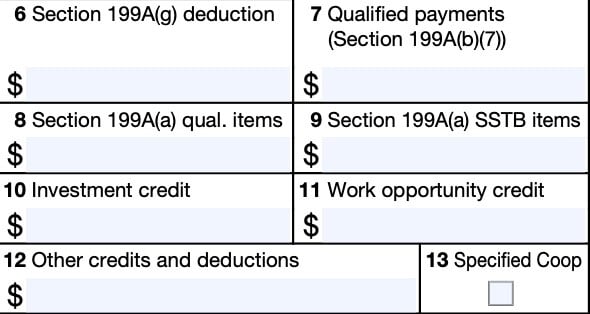

Box 6: Section 199A(g) Deduction

Box 6 indicates your share of the cooperative’s Section 199A(g) deduction passed through to you.

The amount must have been designated in a written notice of allocation sent to you from the cooperative during the Section 1382(d) payment period.

The amount allocated to each patron cannot exceed 9% of the qualified payments reported in Box 7. However, this amount will not reduce amounts reported in Box 1 or Box 3.

To claim the deduction, you must not be a C corporation.

Box 7: Qualified payments (Section 199A(b)(7))

Non C corporation taxpayers may need the information reported in Boxes 7 through 9 to calculate and report the qualified business income (QBI) on their income tax return. For further guidance, refer to the instructions for:

- IRS Form 8995-A, Qualified Business Income Deduction, or

- IRS Form 8995, Qualified Business Income Deduction, Simplified Computation

Box 7 shows the amount of Form 1099-PATR income paid to you on which the cooperative computed its Section 199A(g) deduction.

If there is an amount in this box and the amount is related to a trade or business for which you are

claiming a Section 199A(a) deduction, you must reduce the amount of deduction that you take.

Box 8: Section 199A(a) qualified items

Box 8 contains items that may qualify as qualified items from trades or businesses that are not a specified service trade or business (SSTB) for calculating the QBI deduction. These qualified items are reported in:

Items that relate to SSTBs are reported separately in Box 9, below.

Nonqualified items

Examples of income that are not qualified items include:

- Tax-exempt income

- Capital gains

- Income that isn’t effectively connected with the conduct of a trade or business within the United States

Box 9: Section 199A(a) SSTB items

Box 9 amounts are items received from an SSTB that may qualify for the QBI deduction. These items have been reported in:

SSTBs

Examples of SSTBs include the provision of services in the fields of:

- Health

- Law

- Accounting

- Actuarial science

- Performing arts

- Consulting

- Athletics

- Financial services

- Brokerage services

- Investing and investment management

Box 10: Investment credit

Box 10 shows investment credits passed through to you by the cooperative. Co-op members can file IRS Form 3468 to compute your total investment credit.

Box 11: Work opportunity credit

Box 11 shows work opportunity credits passed through to you. You may need to file IRS Form 5884 to calculate the work opportunity credit. Certain taxpayers may also need to file IRS Form 3800, General Business Credit, to apply these credits to their income tax return.

Box 12: Other credits and deductions

Box 12 may contain other credits and tax deductions passed down to co-op members. This may include the following federal tax credits:

- Empowerment zone employment credit, which you can report on IRS Form 8844

- Low sulfur diesel fuel production credit, reported on IRS Form 8896

- Credit for small employer health insurance premiums, reported on IRS Form 8941

- Credit for employer differential wage payments, which you can report on IRS Form 8932

- The tax deduction for capital costs incurred by small refiner cooperatives when complying with EPA sulfur regulations.

- The biodiesel, renewable diesel, or sustainable aviation fuel mixture credit, reported on IRS Form 8864

Box 13: Specialized cooperative

If Box 13 is checked, the information reported to you is from a specified agricultural or horticultural cooperative, as defined in Section 199A(g)(4)(A) of the tax code.

Filing IRS Form 1099-PATR

For tax entities who must file this tax form with the Internal Revenue Service, the IRS requires certain paper versions of information returns to be accompanied by IRS Form 1096, Annual Summary and Transmittal of U.S. Information Returns.

Check out our step-by step instructional guide for more information on how to submit your information return with IRS Form 1096.

Video walkthrough

Watch this informative video to learn more about income, deductions, and tax credits reported to you on IRS Form 1099-PATR.

Frequently asked questions

Taxpayers should expect to receive their 1099-PATR forms no later than January 31 of the year following the tax year they received taxable income from the cooperative.

Cooperatives are only required to file Form 1099-PATR to report taxable distributions of $10 or more in a calendar year, or if backup withholding was required. If you have not received your form by January 31, you should contact the cooperative for assistance.

Where can I find IRS Form 1099-PATR?

As with other tax forms, you can download a copy of IRS Form 1099-PATR from the IRS website. For your convenience, we’ve enclosed the latest version in this article.

Related tax articles

This tax form is one of the fillable tax forms provided by the Internal Revenue Service, to help taxpayers reduce their tax preparation costs. To see more forms like this, visit our free fillable tax forms page, where you’ll also find articles like this.

Unlike the IRS, our articles contain step by step instructions for each tax form, as well as video walkthroughs. You can also check out all of our videos by subscribing to our YouTube channel!