IRS Form 1099-DIV Instructions

If you have investments that produce dividend income or capital gain distributions, you should expect to receive IRS Form 1099-DIV. While your financial institution is responsible for issuing this tax document, it’s worth taking the time to understand how to report this information on your income tax return.

In this article, we’ll help you understand everything you need to know about IRS Form 1099-DIV, including:

- What you should expect to see in each box on this form

- How this tax information will impact your income tax return

- When you should expect your Form 1099-DIV and what to do if you do not receive it on time

Let’s start by breaking down this tax form, one step at a time.

Table of contents

IRS Form 1099-DIV Instructions

In most of our articles, we walk you through how to complete the tax form. However, since Form-1099 is issued to taxpayers for informational purposes, most readers will probably want to understand the information reported on their 1099-DIV form, instead of how to complete it.

Before we start breaking down this tax form, it’s important to understand that there can be up to 5 copies of Forms 1099-DIV. Here is a break down of where all these forms end up:

- Copy A: Internal Revenue Service center

- Copy B: For recipient’s tax records

- Copy C: For payer’s tax records

- Copy 1: For state, city, or local tax department

- Copy 2: To be filed with employee’s state, city, or local tax return

For employees who do not pay state, city, or local income tax, copies 1 and 2 are optional.

Let’s get into the form itself, starting with the information fields on the left side of the form.

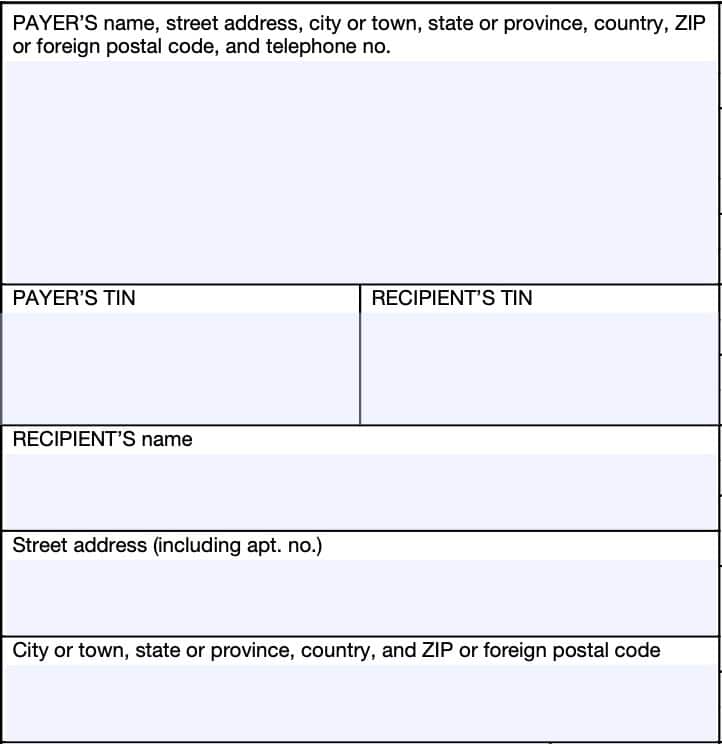

Taxpayer identification fields

Payer’s name, address, and telephone number

You should see the financial institution’s complete name, address, and telephone number in this field.

Payer’s TIN

This is the payer’s taxpayer identification number (TIN). In most situations, this will be the employer identification number (EIN).

The payer’s TIN should never be truncated.

Recipient’s TIN

As the recipient or payee, you should see your taxpayer identification number in this field. For payees, the TIN can be any of the following:

- Social Security number (SSN)

- Individual taxpayer identification number (ITIN)

- Adoption taxpayer identification number (ATIN)

- Employer identification number (EIN)

Please review this field to make sure that it is correct. However, you may see a truncated form of your TIN (such as the last four digits of your SSN), for privacy protection purposes. Copy A, which is sent to the Internal Revenue Service, is never truncated.

Recipient’s name and address

You should see your name and address reflected in these fields. If your address is incorrect, you should notify the financial institution and the IRS.

You can notify the IRS of your new address by filing IRS Form 8822, Change of Address. Business owners can notify the IRS of a change in their business address by filing IRS Form 8822-B, Change of Address or Responsible Party, Business.

Boxes 1 through 10

On the right side of the form are boxes 1 through 10. In most circumstances, some of these boxes will be blank.

However, let’s go through each box so we can better understand what you should expect to see, and where you should report it on your federal income tax return.

Box 1a: Total ordinary dividends

In Box 1a, you should see the total amount of dividends issued from the payer during the calendar year. This includes dividends from:

- Money market funds

- Net short-term capital gains from mutual funds, and

- Other distributions on stock

- Reinvested dividends

- Section 404(k) dividends paid directly from a corporation

Box 1a will include amounts entered in the following other boxes:

- Box 1b: Qualified dividends

- Box 2e: Section 897 ordinary dividends

- Box 6: Recipient’s share of investment expenses

Generally, you’ll report total dividends in Line 3b of your Form 1040, Form 1040-SR, or Form 1040-NR. You may also need to report this amount on Line 5 of IRS Schedule B, if required.

Box 1b: Qualified dividends

Box 1b will contain the portion of the dividends from Box 1a that qualifies for a lower capital gains tax rate, instead of the ordinary income tax rate.

This may include dividends where it is impractical for the financial institution to determine whether the Section 1(h)(11)(B)(iii) holding period requirement has been met, to qualify for long-term capital gains treatment.

Qualified dividends Exceptions

In general, the IRS considers qualified dividends to be dividends paid during the tax year by domestic corporations and qualified foreign corporations, except for:

- Dividends the recipient received on any share of stock held for less than 61 days during the 121-day period that began 60 days before the ex-dividend date

- Dividends attributable to periods totaling more than 366 days that the recipient received on any share of preferred stock held for less than 91 days during the 181-day period that began 90 days before the ex-dividend date

- Dividends that relate to payments that the recipient is obligated to make with respect to short sales or positions in substantially similar or related property

- Dividends paid by a regulated investment company (RIC) that are not treated as qualified dividend income under Internal Revenue Code Section 854

- Dividends paid by a real estate investment trust (REIT) that are not treated as qualified dividend income under IRC Section 857(c)

- Deductible dividends paid on employer securities

This box cannot contain a negative number. Your qualified dividend total should never be less than zero.

In general, you’ll report qualified dividends in Line 3a of your Form 1040, Form 1040-SR, or Form 1040-NR.

Box 2a: Total capital gain distributions

This box will contain total capital gains distributions (long-term). This should include the total amounts from the following boxes:

- Box 2b: Unrecaptured Section 1250 gain

- Box 2c: Section 1202 gain

- Box 2d: Collectibles (28%) gain

- Box 2f: Section 897 capital gain

Let’s take a look at the first of these, unrecaptured Section 1250 gain.

Box 2b: Unrecaptured Section 1250 gain

If there is an amount reported here, you may need to complete the Unrecaptured Section 1250 gain worksheet, located in the IRS Schedule D instructions, to calculate the amount you enter on Schedule D. If applicable, you’ll enter the calculated amount on Line 19 of Schedule D.

What is unrecaptured Section 1250 gain?

Unrecaptured Section 1250 gain relates to rental real estate property where depreciation was taken or eligible to be taken on previous income tax returns. The maximum capital gains rate associated with unrecaptured Section 1250 gain on depreciable real property is 25%.

This video tutorial walks through the unrecaptured Section 1250 gain worksheet so you can better understand how to report on Schedule D.

Box 2c: Section 1202 gain

Box 2c contains any amount included in Box 2a that is a Section 1202 gain from certain qualified small business stock.

What is Section 1202 gain?

Section 1202 allows you to exclude a portion of the eligible gain on the sale or exchange of qualified small business (QSB) stock.

This percentage can range from 50% to 100% depending on when you acquired the stock, as long as you held the stock for at least 5 years and meet other IRS criteria. The maximum tax rate on any Section 1202 gain that is included in income is 28%.

Reporting Section 1202 gain

If you received a Form 1099-DIV with a gain in Box 2c, part or all of that gain may be eligible

for the Section 1202 exclusion.

Report the total gain (box 2a) on Schedule D, Line 13.

Report the following information in the appropriate columns on IRS Form 8949, Sales and Dispositions of Capital Assets:

- Column (a): Name of the corporation whose stock was sold

- Column (f): ‘Q’

- Column (g): Enter the amount of the excluded gain as a negative number

If you are also completing Line 18 on Schedule D, you may need to make adjustments to the 28% Rate Gain worksheet (details in Box 2d, below).

Box 2d: Collectibles (28%) gain

Box 2d contains amounts included in Box 2a attributable to the 28% capital gains rate from the sales or exchanges of collectibles.

If there is an amount here, you may need to complete IRS Form 8949. Additionally, you may need to complete the 28% gains rate worksheet located in the Schedule D instructions to determine the amount you’ll enter on Line 18 of Schedule D.

Box 2e: Section 897 ordinary dividends

Box 2e contains any amounts from Box 1a related to Section 897 gain from dispositions of U.S. real property interests (USRPI).

Most individual taxpayers who are citizens of the United States should not see entries in Box 2e or Box 2f. However, nonresident aliens and foreign corporations may need to account for this on their tax return.

Box 2f: Section 897 capital gain

Box 2f contains any amounts from Box 2a related to Section 897 gain from dispositions of U.S. real property interests (USRPI).

Most individual taxpayers who are U.S. citizens should not see an entry in Box 2f.

Box 3: Nondividend distributions

If determinable, the corporation will report non-dividend distributions to shareholders in Box 3.

As a general rule, Box 3 amounts are considered a return of invested capital. These usually result in a negative adjustment to basis (lowering your tax basis), and taxpayers usually do not need to report them on their individual tax return.

However, IRS Publication 550, Investment Income and Expenses, instructs taxpayers to report any amounts in excess of your investment basis on IRS Form 8949 in the following manner:

- Use Part I to report amounts on mutual fund shares held for 1 year or less

- Use Part II to report amounts on mutual fund shares held for over 1 year

Box 4: Federal income tax withheld

You should see backup withholding amounts reported in Box 4. If you have not given your TIN to the financial institution, you may be subject to backup withholding on certain dividend payments reported on IRS Form 1099-DIV.

In this case, you may be asked to complete IRS Form W-9, Request for Taxpayer Identification Number and Certification, so they can report the correct TIN to the IRS. Foreign recipients may be asked to complete IRS Form W-8 instead.

Backup withholding rules

Generally speaking, backup withholding rules apply to certain items of income when it is not clear that the taxpayer has provided the correct taxpayer identification number to the payer.

In many cases, people are reluctant to give certain entities (such as banks or other financial institutions) their personal information out of fear of identity theft. While this is an understandable concern, it is important to note that these payers must apply the backup withholding tax rules when it is not clear that the taxpayer has provided the correct TIN.

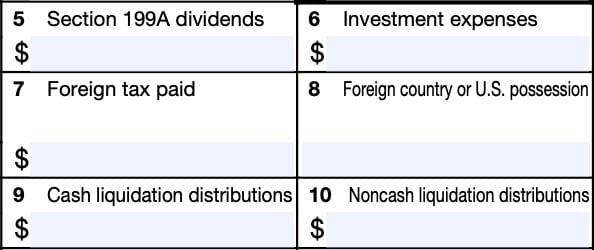

Box 5: Section 199A dividends

If you received dividends from a REIT, or Section 199A dividends paid by a regulated investment company, that amount will be included in Box 5. This amount is also included in the amount reported in Box 1a.

This also includes REIT dividends, besides capital gains dividends or qualified dividends, where the REIT cannot determine whether you’ve met the holding period requirements as described in Treasury Regulations Section 1.199A-3(c)(2)(ii).

Although qualified REIT dividends are already included in taxable income, you may be able to claim a qualified business income (QBI) tax deduction on either:

- IRS Form 8995, Qualified Business Income Deduction, Simplified Computation, or

- IRS Form 8995-A, Qualified Business Income

Box 6: Investment expenses

This box will contain your pro rata share of certain amounts deductible by a nonpublicly offered RIC in computing its taxable income.

This amount is includible in the recipient’s gross income under IRC Section 67(c) and must also be included in Box 1a. Since Box 1a includes these investment expenses, you do not need to account for them separately in your annual tax return.

Box 7: Foreign tax paid

If applicable, Box 7 will contain any foreign tax paid on dividends and other distributions on stock.

A regulated investment company must report only the amount it elects to pass through to you. This amount should appear in U.S. dollars, regardless of the country where the foreign tax was paid.

You may be able to reduce your taxable income by the amount of foreign taxes paid by filing IRS Form 1116, Foreign Tax Credit. Under certain circumstances, you may be able to claim this tax credit without having to file Form 1116.

Box 8: Foreign country or U.S. possession

If applicable, Box 8 should contain the name of the foreign country or U.S. possession for which the foreign tax was paid and reported in Box 7.

However, there are certain situations in which investment companies do not need to complete this box.

Box 9: Cash liquidation distributions

Box 9 and Box 10 generally only pertain to corporations in partial or complete liquidation.

If applicable, Box 9 contains cash that was distributed as part of a liquidation event.

Box 10: Noncash liquidation distributions

Box 10 contains noncash distributions that were made as part of a liquidation. If applicable, this should reflect the fair market value as of the date of distribution.

Boxes 11 through 13

At the bottom of the form, you’ll see Boxes 11 through 16. Before reviewing those fields, let’s discuss the other fields that you’ll see on the left-hand side of the form.

Account number

If applicable, you’ll see an account number posted in this box. Although the IRS encourages financial institutions to include an account number, an account number is only required if:

- You are receiving multiple 1099-DIV forms from the same institution for different accounts, or

- If Box 11 is checked

Box 11: FATCA filing requirement

The reporting institution will check the FATCA filing requirement box if it needs to satisfy certain reporting requirements related to the Foreign Account Tax Compliance Act (FATCA).

If the payer has checked this box, you may need to complete IRS Form 8938, Statement of Specified Foreign Financial Assets, if your reported foreign assets exceed the reporting threshold.

Box 12: Exempt-interest dividends

If you received exempt interest dividends from a mutual fund or other RIC, they will report those dividends in Box 12.

Box 12 also includes any amounts reported in Box 13.

Report any exempt-interest dividends in Line 2a on your IRS Form 1040, or Form 1040-SR.

Box 13: Specified private activity bond interest dividends

Box 13 contains any specified private activity bond interest dividends. Even though they are tax-exempt for income tax purposes, these dividends may be subject to alternative minimum tax (AMT).

These amounts are already included in the amounts reported on Line 2a of your tax return. However, you may also need to report them on IRS Form 6251, Alternative Minimum Tax.

State tax information

Boxes 14 through 16 contain state income tax information. If you live in a state without an income tax, these fields may be left blank.

Box 14: State

If you live in a state without income tax, you may not see any information in Boxes 14 through 16. However, Boxes 14 through 16 may contain relevant tax information for up to 2 different states.

If applicable, Box 14 will contain the abbreviated name of the applicable state(s).

Box 15: State identification number

If your financial institution has a specific state tax identification number, that TIN will appear in Box 15.

Box 16: State tax withheld

Box 16 contains any state income tax withheld on income items reported on Form 1099-DIV.

Filing IRS Form 1099-DIV

For tax entities who must file this tax form with the Internal Revenue Service, the IRS requires certain paper versions of information returns to be accompanied by IRS Form 1096, Annual Summary and Transmittal of U.S. Information Returns.

Check out our step-by step instructional guide for more information on how to submit your information return with IRS Form 1096.

Video walkthrough

Watch this instructional video to learn more about reporting your dividend and distribution income when filing your income tax return.

Are you tired of dreading tax season?

If you’re like most people, you push through the stress of filing, only to be hit with a bigger bill than expected—then put it all behind you until the same cycle repeats next year.

But what if you could change the game?

Tax planning puts you in control. It’s about being proactive, not reactive—taking small, smart steps throughout the year to reduce your tax burden, increase your savings, and keep more of your hard-earned money working for you.

Here’s what effective tax planning helps you do:

✅ Avoid the surprise of a high tax bill

✅ Understand how your income and decisions affect your taxes

✅ Strategically lower your tax liability over time

Ready to make smarter tax moves?

👉 Join my free weekly tax planning newsletter and get one actionable tip every week to help you reduce your taxes legally and effectively.

Start taking control—your future self will thank you.

Frequently asked questions

The IRS requires financial institutions to issue Form 1099-DIV by January 31 of the year following the tax year they issued dividends. This requirement only applies in situations where the recipient received more than $10 in dividend income during the year.

The IRS recommends that you first contact your financial institution if you haven’t received your year-end statement by the January 31st due date. If you still haven’t received your Form 1099-DIV by early February, you may call the IRS at: 800-829-1040 for additional assistance.

The IRS expects taxpayers to report all income on their tax return. However, if you received less than $10 in dividend income during the tax year, the IRS does not require your financial institution to file IRS Form 1099-DIV, nor should you expect to receive a recipient statement.

Where can I find IRS Form 1099-DIV?

As with other tax forms, you may find IRS Form 1099-DIV on the IRS website. For your convenience, we’ve included the most recent copy of the form in this article.

Related tax articles

This tax form is one of the fillable tax forms provided by the Internal Revenue Service, to help taxpayers reduce their tax preparation costs. To see more forms like this, visit our free fillable tax forms page, where you’ll also find articles like this.

Unlike the IRS, our articles contain step by step instructions for each tax form, as well as video walkthroughs. You can also check out all of our videos by subscribing to our YouTube channel!

Let me say thank you for your service to our country! We need men like you to serve.

I have a quick question regarding the 1099-DIV. My investment company in 2022 taxes sent me the 1099-DIV and as you have gone over in your video regarding Box 1a and 2a. In these boxes there were less than $10 in each one of these fields. However, when they reported to IRS they said that I had over $3000 and had income of $300 that I should have reported. However, I did not see this any where on my 1099-DIV for 2022 that they mailed me. Could there have been a mistake on the part of my investment company reporting to me incorrectly?

Thanks for your time

Peggy,

Thank you for writing! My first inclination is that your investment company might have issued a consolidated Form 1099, or that your company should have sent another statement for any sales transactions that might have occurred with your investments. Do you know if there were any transactions in your account other than dividends?

If there isn’t a reason that you can determine on your own, I would suggest contacting the investment company directly and asking about the difference. It seems that there should have been a form (or an updated form) that you should have received but did not, for some reason.

Hi Forrest, Thank you for providing all of this useful info! I have a question on how to handle a C Corp closing down and the owner having $1,000 in common stock. The owner pulled out the cash before closing the bank account for the corporation and therefore have that to report on Box 1a and Box 1b. However, should the $1,000 common stock equity be reported on the 1099-DIV somewhere?

I’m not sure there’s enough information here for me to answer this question, primarily because I don’t know anything about the history of the corporation (i.e. what the owner’s basis in the company is, one-time distribution or multiple distributions are two factors). For example, if the owner’s basis was $10,000, this would look a lot different from if the owner’s basis was $0.

Here is a link to an accounting article with a summary of tax rules for liquidating corporations: https://www.thetaxadviser.com/issues/2020/oct/tax-rules-liquidating-corporations.html

That’s part of the hiccup, is not getting enough info from the CPA firm that originally set up the $1,000 common stock in the books. Thanks for the link!