IRS Schedule E Instructions

Taxpayers file IRS Schedule E, Supplemental Income and Loss, with their individual income tax return to report income from sources that are not subject to self-employment tax. This might include rental real estate, royalty income, income or loss from partnerships, S corporations, estates, trusts or real estate mortgage investment conduits (REMICs).

In this article, we’ll break down IRS Schedule E so you understand everything there is to know, including:

- How to complete and file Schedule E

- How to report the different types of income on Schedule E

- Commonly asked questions about Schedule E

Let’s start with a step by step walkthrough of this tax form.

Table of contents

How do I complete IRS Schedule E?

There are five parts to this two-page tax form:

- Part I: Income or Loss from Rental Real Estate and Royalties

- Part II: Income or Loss from Partnerships and S Corporations

- Part III: Income or Loss from Estates and Trusts

- Part IV: Income or Loss from Real Estate Mortgage Investment Conduits (REMICs)

- Part V: Summary

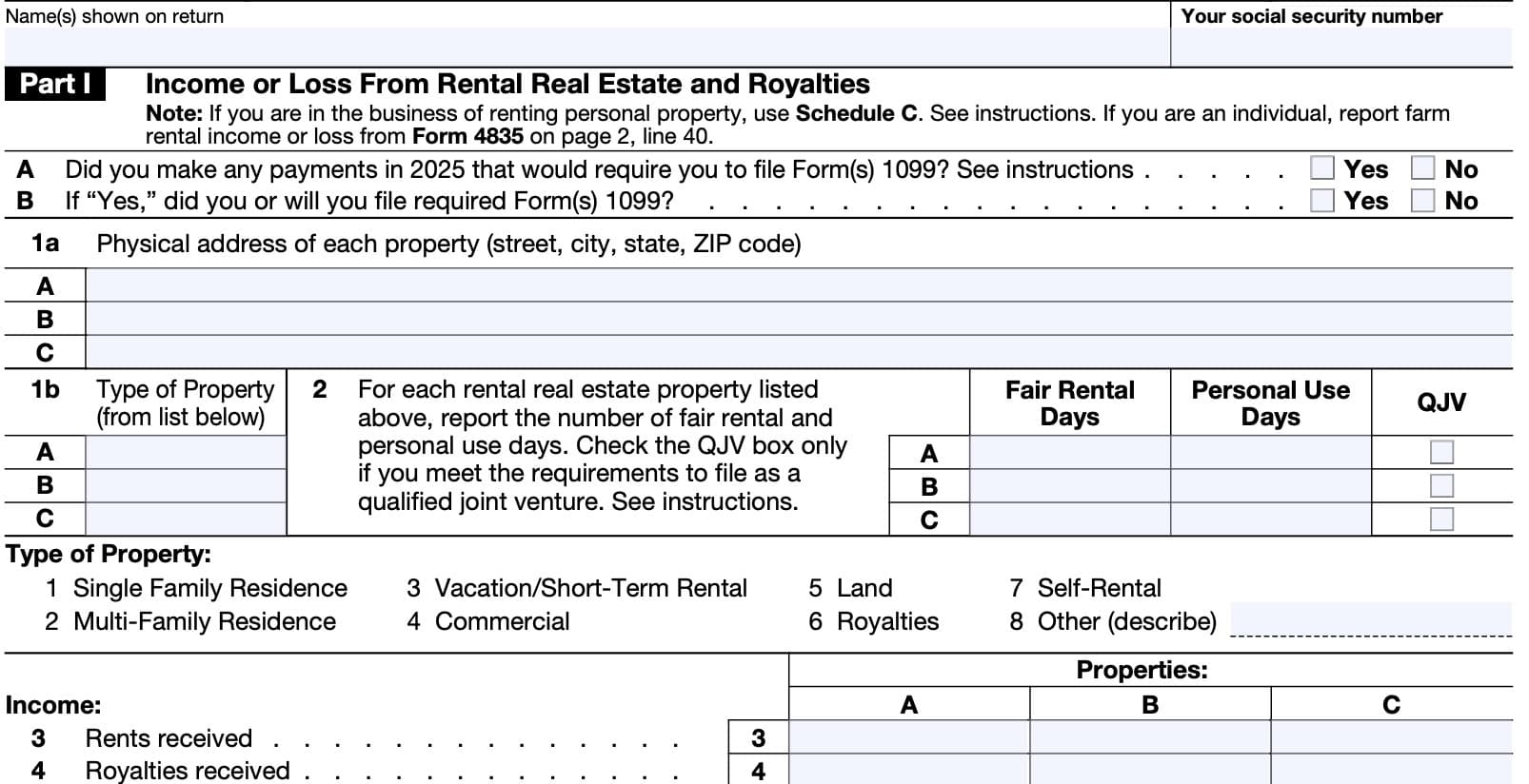

Let’s start with Part I, where we’ll determine rental real estate income or loss, and discuss royalty income. But before we do, make sure that your name and Social Security number are properly presented at the top of the form.

Part I: Income or Loss From Rental Real Estate and Royalties

In Part I, we’ll go over income and expenses related to either rental real estate activities or royalties. Before completing Part I, you should ensure that you’re using the right schedule.

Should I file Schedule E?

There are certain types of business income that the Internal Revenue Service specifies to report somewhere besides Schedule E.

Farmers should report their income on IRS Form 4835.

Only estates and trusts should report farm rental income and expenses on IRS Schedule E.

Farmers should use IRS Form 4835, Farm Rental Income and Expenses and IRS Schedule F, Profit or Loss from Farming, to report business income from farming or farm rental activities.

Estates and trusts report farm rental income and expenses because they do not fill out IRS Form 4835 or use Schedule F.

When should I use Schedule C?

The IRS instructions indicate specific types of income activities that individual taxpayers should report using Schedule C forms instead of the Schedule E tax form.

Taxpayers should use Schedule C of your Form 1040 in the following situations:

You are in the business of renting personal property

The federal government considers to be in the business of renting personal property if:

- The primary purpose for renting the property is to generate business income or profit, and

- You are involved in the rental activity with continuity and regularity

If your rental activity is not a business, then you may need to see the instructions for IRS Schedule 1, specifically Lines 8l and 24b, for more information on how to properly report your business income from renting out personal property.

If you provided significant services to your customer in your rental real estate activity

According to IRS Publication 527, Residential Rental Property, significant or substantial services can include the following activities:

- Regular cleaning services

- Changing linens

- Maid service

For rental property owners who offer one or more of these services to your tenants or customers, then report your rental activities on IRS Schedule C, instead of Schedule E. However, do not use Schedule C if you only provide basic services, such as utilities, cleaning of public areas, or trash collection.

Certain rental real estate activities for real estate dealers

If you are a real estate dealer, then you may need to include rental activity on either Schedule C, Schedule E, or both.

On Schedule E, include only the rent received from real estate (including personal property leased with this real estate) you held for the primary purpose of renting to produce income.

Use Schedule C to report income and deductible expenses from rental activity related to a rental property or rental properties that you held for sale to customers in the ordinary course of your business as a real estate dealer.

Many real estate investors may end up using both schedules, particularly to report short-term rentals on property they intend to sell for profit.

Self-employed individuals reporting royalty income related to their business activity

If you are in business as a self-employed writer, inventor, artist, then you would report your royalties as business income on Schedule C.

Question A: Did you make any payments that would require you to file Form(s) 1099?

Answer ‘Yes’ or ‘No.”

In general, if you paid at least $600 for services performed by someone who is not your employee (nonemployee compensation), you must file Form 1099-NEC.

You must file IRS Form 1099-MISC if you paid at least $600 that would be considered taxable income to the recipient. Below are examples of the type of miscellaneous payments that warrant filing IRS Form 1099-MISC:

- Rents

- Prices

- Medical or health care payments

Question B: If ‘Yes,’ did you, or will you file the required form(s)?

This is a trick question. If applicable, the correct answer is ‘Yes.’

Line 1

There are two parts to Line 1. You may list up to three properties here. If you need more room, you can use as many copies of the IRS Schedule E form as you need to list them all.

However, you should fill in Lines 23a through 26 on only one Schedule E.

The figures on Lines 23a through 26 on that Schedule E should be the combined totals for all properties reported on your Schedules E.

Line 1a: Physical address of each property

In Line 1a, enter the physical address of the rental property listed. Be sure to include the following information:

- Street number and street name

- City and state

- ZIP code

Line 1b: Type of property

In Line 1b, indicate the type of property that best describes that particular piece of real estate. You may choose from the following:

- Single family residence

- Multi-family residence

- Vacation/Short-term rental

- Commercial real estate

- Vacant land

- Royalties

- Self-rental

- Other (enter your own description)

A business owner may enter code “7” for self-rental when renting property to a trade or business in which they materially participated.

Line 2

For each property listed in Line 1, report the number of fair rental days and personal use days. Also, check the QJV box, if you meet the requirements to file as a qualified joint venture.

Fair rental days

Fair rental days are days in which the rental property was rented at fair rental value.

Personal use days

Conversely, personal use days may be any day, or part of a day, in which the property was used by any of the following:

- Yourself, as the business owner

- A co-owner, if used for personal purposes

- Family member

- Unless they are paying a fair rental price for use of the property

- Any person paying less than fair rental price

- Any person with whom you have an exchange agreement for use of their property

Qualified joint venture

A married couple cannot operate a sole proprietorship.

Generally, a married couple that materially participates in a business activity may elect for the IRS to treat them as a qualified joint venture (QJV) instead of a partnership.

For tax purposes, there generally isn’t a significant impact for selecting QJV. However, this allows the married couple to avoid having to file IRS Form 1065 as a partnership.

A married couple may only select QJV if they own their business activities directly. If they own the business through a limited liability company (LLC) or S corporation, the married couple cannot select this option.

Line 3: Rents received

Report any real estate rental income here. Use a separate column to report the total rental income for each property listed in Line 1. Include income that you received for renting a single room or other space, even if you did not rent the entire building.

If you need to report other income, attach a statement explaining the circumstances of how you received that income.

If you received goods or services as rent in lieu of cash, then report the fair market value of goods and services received as rental income here.

Line 4: Royalties received

As applicable, report any royalty income from

- Oil, gas, or mineral properties

- Copyrights

- Patents

Use a separate column for each property. If you received $10 or more in royalties during the tax year, you should receive a Form 1099-MISC or similar statement by February 1 of the following tax year. Report this amount here.

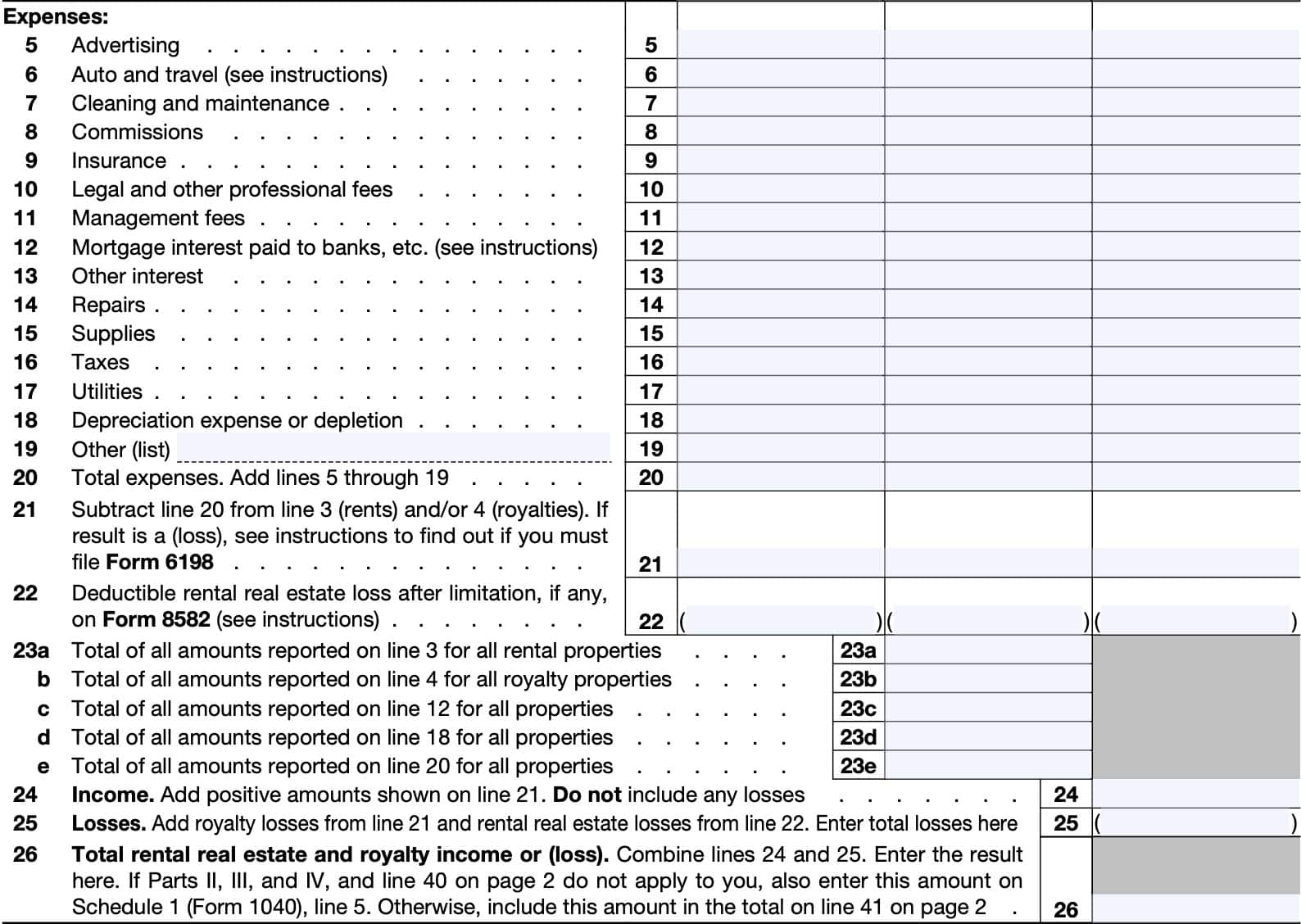

Line 5: Advertising

For expenses outlined in Lines 5 through 21, you can generally deduct all ordinary and necessary expenses related to your real estate investments. Enter the appropriate expense amount related to each listed property.

However, you are not allowed to deduct any of the following:

- The value of your own labor

- Capital investments or improvements

For Line 5, enter advertising expenses related to your rental property.

Line 6: Auto and travel

You can deduct ordinary and necessary auto and travel expenses related to your rental activities. This includes 50% of meal expenses that you incurred while traveling away from home.

Unless you used more than four vehicles, you may use either of the following methods for reporting auto expenses:

- Actual expenses method

- Standard mileage rate

Actual expenses method

If you deduct actual auto expenses, then you’ll need to include on Line 6 the cost of the following, as related to each rental activity:

- Gasoline

- Oil

- Repairs

- Auto insurance

- Tires

- Registration, tolls, license plates, etc

Enter depreciation expenses on Line 18, below. For auto rental or lease payments, use Line 19.

If you claim any auto expenses (actual or the standard mileage rate), you must complete Part V of Form 4562, Depreciation and Amortization. Attach your completed Form 4562 to your tax return.

If you used more than four vehicles, you must use the actual expenses method. However, if you’ve previously used the standard mileage rate, then you cannot use the actual expenses method.

Standard mileage rate

For taxpayers using the standard mileage rate, multiply the mileage related to each rental activity by the mileage rate for the specific tax year:

- 2023: 65.5 cents per mile

- 2024: 67 cents per mile

- 2025: 70 cents per mile

You may also include parking fees and tolls if you use the standard mileage rate on Line 6. However, you may not deduct any of the following:

- Rental or lease payments

- Depreciation

- Actual auto expenses

Line 7: Cleaning and maintenance

Enter any cleaning and maintenance related to each rental activity in Line 7. Do not include the cost of major renovations, capital improvements, or any investment intended to increase property value.

See Line 14 for more details on the difference between maintenance and capital improvements.

Line 8: Commissions

Enter any commissions that you paid related to each business activity.

Line 9: Insurance

In Line 9, enter any insurance costs for each applicable property.

Line 10: Legal and other professional fees

Enter any legal or other professional fees incurred for each property. This may include fees that you paid for tax advice or tax return preparation related to your properties.

Do not deduct legal fees paid or incurred for any of the following purposes:

- To defend or protect title to property

- To recover property

- To develop or improve property

These fees must be capitalized and added to the property’s basis.

Line 11: Management fees

Enter any management company fees that you incurred related to your real estate investments.

Line 12: Mortgage interest paid to banks, etc.

Enter any mortgage interest paid to a bank or other financial institution in Line 12. You must have documentation showing how the proceeds for each mortgage or loan were used.

Interest you paid as part of your rental real estate activity is not subject to the limitation on business interest unless your rental real estate activity is considered to be a trade or business.

If that is the case, then you must file IRS Form 8990 to deduct any interest expenses related to that rental real estate activity, unless you meet one of the filing exceptions outlined in the form instructions. If Form 8990 indicates a limitation to your business interest deduction, then you must complete that form before completing Line 12 or Line 13.

Reporting mortgage interest

Here is additional guidance on reporting mortgage interest.

Enter your total mortgage interest expenses on Line 23c, even if you only have one property.

Prepaid interest: Do not deduct prepaid interest when you paid it. You can deduct it only in the

year to which it is properly allocable.

Points: Points, including loan origination fees, charged only for the use of money must be deducted over the life of the loan.

Form 1098: If you paid $600 or more in interest on a mortgage during the tax year, the recipient should send you a Form 1098 or similar statement by February 1 of the following year, reporting the total interest received.

If you paid more interest than shown on your Form 1098, then use IRS Publication 535 to determine if you can deduct part or all of the additional interest.

If you can, enter the deductible amount here, and attach an explanation to your personal income tax return.

Line 13: Other interest

If you paid non-mortgage interest on debt related to your business property, then enter that interest here, using the same guidelines outlined in Line 12.

Line 14: Repairs

Enter repair costs to each of your properties in Line 14.

You can deduct the amounts paid for repairs and maintenance. However, you

cannot deduct the cost of improvements.

Repairs vs. capital improvements

Repairs and maintenance costs are those costs that keep the property in an ordinarily efficient operating condition. Examples include fixing a broken door or painting a room.

Repairs and maintenance costs can be expensed in the year they are paid or incurred.

In contrast, improvements are amounts paid to:

- Improve or restore your property, or

- Adapt your property to a new or different use

Examples of improvements include replacing an entire air conditioning system or roof.

Unlike repair or maintenance costs, capital improvements must be capitalized and depreciated. You cannot deduct the entire cost of capital improvements in the year they are paid or incurred.

Line 15: Supplies

Enter the cost of supplies you procured for each property in Line 15.

Line 16: Taxes

Enter property taxes paid that are directly attributable to each property.

Line 17: Utilities

Enter the cost of utilities in Line 17.

You can deduct the cost of ordinary and necessary telephone calls related to your rental activities or royalty income.

However, the base rate (including taxes and other charges) for the first telephone line into your residence is a personal expense and is not deductible for tax purposes.

Line 18: Depreciation expense or depletion

Enter the depreciation expense for each property in Line 18. Enter the total depreciation expense for all properties in Line 23d, even if you only have one property.

Depreciation is the annual deduction you must take to recover the cost or other basis of business or investment property having a useful life substantially beyond the tax year.

Depreciation begins when the property is available and ready for use in your business, or to generate income. It ends when either:

- You have deducted all of your depreciable cost or other basis, or

- No longer use the property for business purposes or for producing income

Use IRS Form 4562 to calculate the amount of depreciation expense you must enter here. You must complete and attach IRS Form 4562 if you are claiming any of the following:

- Depreciation on property first placed into service during the tax year

- Depreciation on listed property

- Including vehicles, regardless of when placed in service, or

- A Section 179 expense deduction or amortization of costs that began in the taxable year

Land is not depreciable.

Line 19: Other expenses

Enter on any ordinary and necessary expenses not previously listed.

For example, you may use IRS Form 7205 to deduct part or all of the cost of modifying commercial buildings to make them more energy efficient. Revenue Procedure 2022-14 contains more details.

Line 20: Total expenses

For each property, add Lines 5 through 19. Enter the total in the appropriate column on Line 20.

Line 21

Subtract Line 20 from either Line 3 (rents), Line 4 (royalties), or the combination of both lines.

If there is a loss, you may need to complete IRS Form 6198 to determine any at-risk limitations that might apply to your loss deduction.

If at-risk rules apply, then:

- Enter the deductible amount in the appropriate column of Line 21

- Enter ‘Form 6198’ in the space to the left of Line 21

- Attach your completed Form 6198 to your income tax return

At-risk rules

If any of the following pertain to your tax situation, then at-risk rules might apply:

- You used nonrecourse loans to finance your business activity, or to acquire property or your interest in the activity

- Certain exceptions apply to qualified nonrecourse financing, which is secured by other real property

- You used cash, property, or borrowed amounts, which are protected against loss by a guarantee, stop-loss agreement, or similar arrangement

- You borrowed amounts from a person who has an interest in the activity (not as a creditor), or who is a related person

Line 22: Deductible rental real estate loss after limitation

If Line 21 is from royalty properties only, do not complete Line 22.

If you have a loss related to your rental income, then you may be limited under passive activity rules, described below. You may need to complete IRS Form 8582 to determine how much of your loss is deductible.

If your rental real estate loss is not from a passive activity or you meet the exception for certain rental real estate activities, you do not have to complete Form 8582. Instead, enter the Line 21 loss directly on Line 22.

If you have an unallowed rental real estate loss that you carried forward from a prior year, you can include that loss on Line 22.

Passive activity rules

A passive activity is any business activity in which you did not materially participate and any rental activity, except as explained later.

In a partnership, if you are a limited partner and not a general partner, the IRS usually will not consider you to have materially participated in the partnership’s activities in the taxable year.

Exceptions for certain rental real estate activities

If you meet all of the following conditions, your rental real estate losses are not limited by the passive activity loss rules, and you do not need to complete Form 8582.

- Rental real estate activities are your only passive activities.

- You do not have any prior year unallowed losses from any passive activities.

- All of the following apply if you have an overall net loss from these activities.

a. You actively participated in all of the rental real estate activities.

b. If married filing separately, you lived apart from your spouse all year.

c. Your overall net loss from these activities is $25,000 or less ($12,500 or less if married filing separately).

d. You have no current or prior year unallowed credits from passive activities.

e. Your modified adjusted gross income (MAGI) is $100,000 or less ($50,000 or less if married filing separately).

f. You do not hold any interest in a rental real estate activity as a limited partner or as a beneficiary of an estate or a trust.

If you do not meet all of these conditions, you may need to attach a completed Form 8582 to your tax return.

Active participation

You can meet the active participation requirement without regular, continuous, and substantial involvement in real estate activities. But you must have participated in making management decisions or arranging for others to provide services (such as repairs) in a significant and bona fide sense.

Such management decisions include:

- Approving new tenants,

- Deciding on rental terms,

- Approving capital or repair expenditures, and

- Other similar decisions

If your ownership interest is less than 10% by value of all interests in the activity, the IRS does not consider you to be an active participant.

Line 23

There are five parts to Line 23:

Line 23a

Enter the total of all amounts reported on Line 3, for all rental properties.

Line 23b

In Line 23b, enter all income for royalty properties, as reported on Line 4.

Line 23c

Enter the total of all amounts reported on Line 12 for all properties.

Line 23d

In Line 23d, enter the total for all items reported on Line 18 for all properties.

Line 23e

Enter the total of all amounts reported on Line 20 for all properties.

Line 24: Income

Enter the total of all positive amounts from Line 21.

Line 25: Losses

Add the following passive losses:

Line 26: Total rental real estate and royalty income (or loss)

Combine Line 24 and Line 25. Enter the result here.

If none of the following apply to you, then enter this amount on IRS Schedule 1, Line 5:

Otherwise, include this amount in the total income or loss number that you report on Line 41.

Part II: Income or Loss from Partnerships and S Corporations

If you are a member of a partnership or joint venture or a shareholder in an S corporation, complete Part II to report your share of the partnership or S corporation income (even if not received) or loss.

If you elected to be taxed as a qualified joint venture instead of a partnership, you’ll need to follow the reporting rules under Qualified Joint Venture.

You should receive a Schedule K-1 from each partnership or S corporation, as well as a copy of the accompany instructions to the partner or shareholders.

Your copy of Schedule K-1 and its instructions will tell you where on your return to report your share of the items. If you are treating items differently on your tax return than the way they were reported to you, you might need to file IRS Form 8082 to explain the difference.

As a cautionary note, you can expect the Internal Revenue Service to compare the amounts reported on your Schedule K-1 forms to the amounts you report on IRS Schedule E.

Line 27

Are you reporting any of the following:

- A loss not allowed in a prior tax year due to at-risk or basis limitations

- A prior year loss that was:

- Unallowed for that year

- From a passive activity

- Not reported on IRS Form 8582

- Unreimbursed partnership expenses

If not, proceed to Line 28.

If so, follow the guidance below, based upon your specific tax situation.

Losses Not Allowed in Prior Years Due to the Basis or At-Risk Rules

- Enter your total prior year unallowed losses that are now deductible on a separate line in column (i) of Line 28.

- Do not combine these losses with, or net them against, any current year amounts from the partnership or S corporation.

- Enter “PYA” in Column (a) of the same line.

Prior Year Unallowed Losses from a Passive Activity Not Reported on IRS Form 8582

- Enter your total prior year unallowed losses not reported on Form 8582 on a separate line in Column (g) of Line 28. These losses can include prior year unallowed losses that you can now deduct because:

- You did not have an overall loss from passive activities, or

- You disposed of your entire interest in a passive activity in a fully taxable transaction

- Do not combine these losses with, or net them against, any current year amounts from the partnership or S corporation.

- Enter “PYA” in Column (a) of the same line.

Unreimbursed Partnership Expenses

You can deduct unreimbursed ordinary and necessary partnership expenses you paid on behalf of the partnership on Schedule E if you were required to pay these expenses under the partnership

agreement.

You can only deduct unreimbursed expenses on Schedule E that are trade or business expenses under IRC Section 162. Do not report these expenses separately if they are from a passive activity and you must file Form 8582. Otherwise, follow these steps:

- Enter unreimbursed partnership expenses from nonpassive activities on a separate line in Column (i) of Line 28.

- Do not combine these losses with, or net them against, any current year amounts from the partnership or S corporation.

- If the expenses are from a passive activity and you are not required to file Form 8582, enter the expenses related to a passive activity on a separate line in column (g) of line 28.

- Enter “UPE” in Column (a) of the same line.

Line 28

For nonpassive income or loss and passive income or losses for which you are not filing Form 8582, enter the following information in the applicable column of Line 28, after applying any special rules that limit losses:

- Column (a): Name of partnership or S corporation

- Column (b): Enter either of the following:

- Partnership: P

- S corporation: S

- Column (c): Check if this is a foreign partnership

- Column (d): Employer identification number (EIN)

- Column (e): Check only if basis computation is required

- Column (f): Check only if there is an amount not at risk

- Column (g): Passive loss allowed

- Attach IRS Form 8582 if required

- Column (h): Passive income from Schedule K-1

- Column (i): Nonpassive loss allowed

- Column (j): Section 179 expense deduction

- Directly from IRS Form 4562

- Column (k): Nonpassive income from Schedule K-1

If you are filing IRS Form 8582, be sure to follow the form instructions before completing Line 28.

Line 29: Totals

There are two portions to Line 29.

Line 29a

Line 29a pertains only to the income items from Column (h) and Column (k). Add these two columns and enter the totals in Line 29a.

Line 29b

Line 29b pertains only to the loss or deduction items from Column (g), Column (i), and Column (j). Add these three columns and enter the totals in Line 29b.

Line 30

Add the totals of Columns (h) and (k) from Line 29a. Enter the sum here.

Line 31

Add the totals of Columns (g), (i), and (j) from Line 29b. Enter the sum here.

Line 32: Total partnership and S corporation income or (loss)

Combine Line 30 and Line 31. Enter the total here.

This represents your total income or loss from partnerships and S corporations.

Part III: Income or Loss from Estates and Trusts

If you are a beneficiary of an estate or trust, use Part III to report your part of the income or loss, even if you did not actually receive income.

You should receive a Schedule K-1 (IRS Form 1041) from the fiduciary. Your copy of Schedule K-1 and its instructions will tell you where on your return to report the items from Schedule K-1.

Do not attach Schedule K-1 to your return. Keep it for your records.

If you are treating items on your tax return differently from the way the estate or trust reported them on its return, you may have to file IRS Form 8082.

Estimated taxes

If you have estimated taxes credited to you from a trust (Schedule K-1 (Form 1041), box 13, code A), enter “ES payment claimed” and the amount on the dotted line next to Line 37.

However, do not include this amount in the total on line 37. Instead, enter the amount on Form 1040, 1040-SR, or 1040-NR, Line 26.

Line 33

Enter the following information in the applicable column of Line 33:

- Column (a): Name of estate or trust

- Column (b): Employer identification number (EIN)

- Column (c): Passive loss or deduction allowed

- Attach IRS Form 8582, if required

- Column (d): Passive income from Schedule K-1

- Column (e): Deduction or loss from Schedule K-1

- Column (f): Other income from Schedule K-1

Line 34

There are two portions to Line 34.

Line 34a

Line 34a pertains only to the income items from Column (c) and Column (f). Add these two columns and enter the totals in Line 34a.

Line 34b

Line 34b pertains only to the loss or deduction items from Column (c) and Column (e). Add these two columns and enter the totals in Line 34b.

Line 35

Add the totals of Columns (d) and (f) from Line 34a. Enter the sum here.

Line 36

Add the totals of Columns (c) and (e) from Line 34b. Enter the sum here.

Line 37: Total estate and trust income or (loss)

Combine Line 35 and Line 36. Enter the total here.

This represents your total income or loss from estates and trusts.

Part IV: Income or Loss from Real Estate Mortgage Investment Conduits (REMICs)-Residual Holder

If you are the holder of a residual interest in a REMIC, use Part IV to report your total share of the REMIC’s taxable income or loss for each quarter included in your tax year.

You should receive Schedule Q (Form 1066) and instructions from the REMIC for each quarter. Do not attach Schedule(s) Q to your return. Keep it for your records.

If you are treating REMIC items on your tax return differently from the way the REMIC reported them on its return, you may have to file Form 8082.

If you hold residual interests in more than one REMIC, attach a continuation sheet using the same format as in Part IV. Enter the combined totals of columns (d) and (e) on Line 39.

If you also completed Part I on more than one Schedule E, use the same Schedule E on which you entered the combined totals in Part I.

REMIC income or loss is not income or loss from a passive activity.

If you are the holder of a regular interest in a REMIC, do not report the income received on IRS Schedule E. Instead, report it on Form 1040 or Form 1040-SR, Line 2b.

Line 38

Enter the following information in the applicable column of Line 38:

- Column (a): Name of REMIC

- Column (b): Employer identification number (EIN)

- Column (c): Excess inclusion from Schedules Q, Line 2c

- Smallest amount you are allowed to report as taxable income, or as alternative minimum taxable income (AMTI) on IRS Form 6251

- Column (d): Taxable income (or loss) from Schedules Q, Line 1b

- Column (e): Income from Schedules Q, Line 3b

Line 39

Combine Columns (d) and (e) from Line 38. Enter the result here, and on Line 41.

Part V: Summary

In Part V, we summarize applicable income and loss items. For certain occupations, Part V is also used to reconcile certain items that might be reported elsewhere on a tax return.

Line 40: Net farm rental income or (loss)

Enter any farm rental income or loss from IRS Form 4835.

If you complete Line 40, you must also complete Line 42, below.

Line 41: Total income or (loss)

Combine the following items:

- Line 26: Part I, Total rental real estate and royalty income or (loss)

- Line 32: Part II, Total partnership and S corporation income or (loss)

- Line 37: Part III, Total estate and trust income or (loss)

- Line 39: Part IV, Total income or loss from REMICs

- Line 40: Farm rental income or loss from IRS Form 4835

Line 42: reconciliation of farming and fishing income

Special estimated tax rules may apply to taxpayers with gross farming or fishing income. Taxpayers generally will avoid tax penalties for underpayment if:

- Gross farming or fishing income for the current tax year or previous tax year is at least two-thirds of the taxpayer’s gross income

- The taxpayer files the income tax return and pays taxes due by March 1 of the subsequent year

In Line 42, enter gross farming and fishing income as reported on the following:

- IRS Form 4835, Line 7

- Partnerships: Schedule K-1 (IRS Form 1065), Box 14, Code B

- S corporations: Schedule K-1 (IRS Form 1120-S), Box 17, Code AD

- Estates & Trusts: Schedule K-1 (IRS Form 1041), Box 14, Code F

Line 43: Reconciliation for real estate professionals

The Internal Revenue Service considers a taxpayer to be a real estate professional only if the taxpayer meets the following conditions:

- More than half of the personal services performed in trades or businesses during the year were performed in real property trades or businesses in which the taxpayer materially participated.

- The taxpayer performed more than 750 hours of services during the year in real property trades or businesses in which the taxpayer materially participated.

For married taxpayers filing a joint return, either spouse must meet both conditions without respect to the other spouse’s activity.

If you were a real estate professional, enter the net income or (loss) you reported anywhere on Form 1040, Form 1040-SR, or Form 1040-NR from all rental real estate activities in which you materially participated under the passive activity loss rules.

Video walkthrough

Frequently asked questions

Taxpayers use Schedule E to report income or loss from rental real estate property, royalties, partnerships, S corporations, estates, trusts, and residual interests in real estate mortgage investment conduits, known as REMICs.

Taxpayers generally file Schedule E, Supplemental Income and Loss, with their individual income tax return.

Taxpayers use Schedule C to report taxable income that may be subject to self-employment tax, known as FICA. Taxpayers file Schedule E to report supplemental income that generally is not subject to FICA taxes.

How can I find IRS Schedule E?

You can find tax forms like Schedule E on the Internal Revenue Service website. For your convenience, we’ve enclosed the most recent version here as a PDF file.

Related tax articles

This tax form is one of the fillable tax forms provided by the Internal Revenue Service, to help taxpayers reduce their tax preparation costs. To see more forms like this, visit our free fillable tax forms page, where you’ll also find articles like this.

Unlike the IRS, our articles contain step by step instructions for each tax form, as well as video walkthroughs. You can also check out all of our videos by subscribing to our YouTube channel!