IRS Form 8594 Instructions

When conducting a business sale involving different types of assets, both the buyer and seller may have to file IRS Form 8594, Asset Acquisition Statement. This tax form helps both parties properly report for different assets, by class, involved in the business transaction.

In this article, we’ll go through what you need to know about IRS Form 8594, including:

- How to complete IRS Form 8594

- Different types of asset classes you will report

- Other frequently asked questions

Let’s start with a walkthrough of the tax form itself.

Table of contents

How do I complete IRS Form 8594?

There are three parts to this tax form:

- Part I: General Information

- Part II: Original Statement of Assets Transferred

- Part III: Supplemental Statement

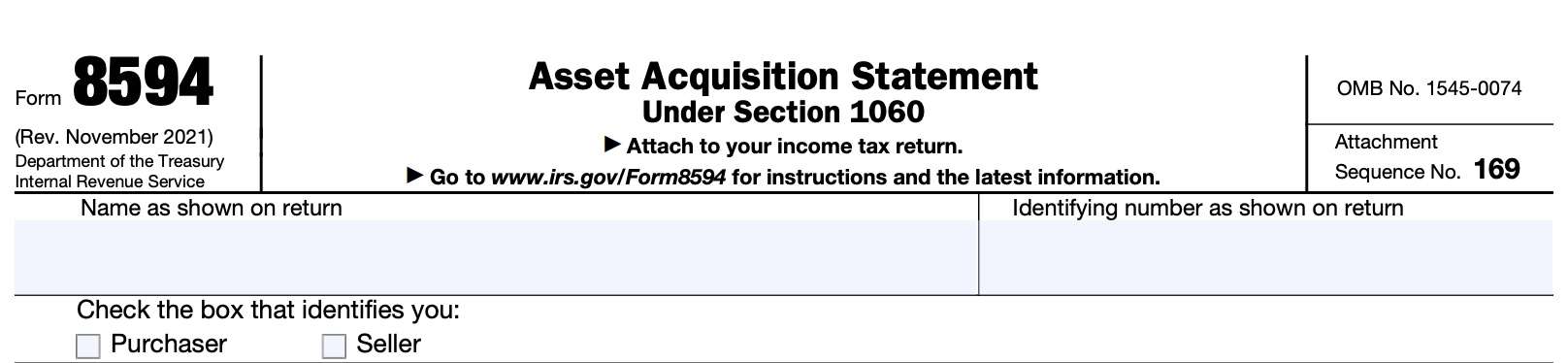

Before starting with Part I, let’s take a look at the information fields at the top of the form.

Top of form

Above Part I, you’ll need to enter information about yourself as the taxpayer. Enter the following information:

- Taxpayer name, as shown on your income tax return

- Identifying number, such as your Social Security number or individual taxpayer identification number (ITIN)

Below those fields, check whether you are the purchaser in this asset sale, or whether you are the seller.

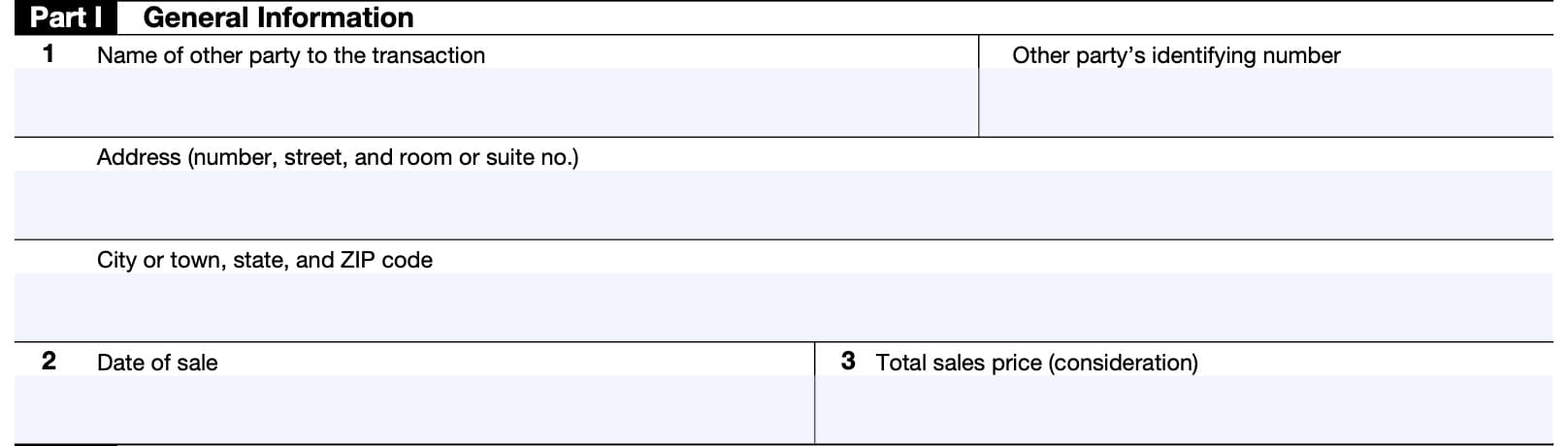

Part I: General Information

In Part I, we’ll document some basic information about this transaction.

Line 1

In Line 1, enter the following information about the other party:

- Name of the other party

- Address, including city, state, and zip code

- Taxpayer identification number (TIN).

You must enter the other party’s TIN. If the other party is an individual or sole proprietor, enter the person’s Social Security number. If the other party is a corporation, partnership, or other entity, enter the employer identification number (EIN).

Line 2: Date of sale

Enter the closing date of the sale.

Line 3: Total sales price

Enter the total purchase price of the transaction.

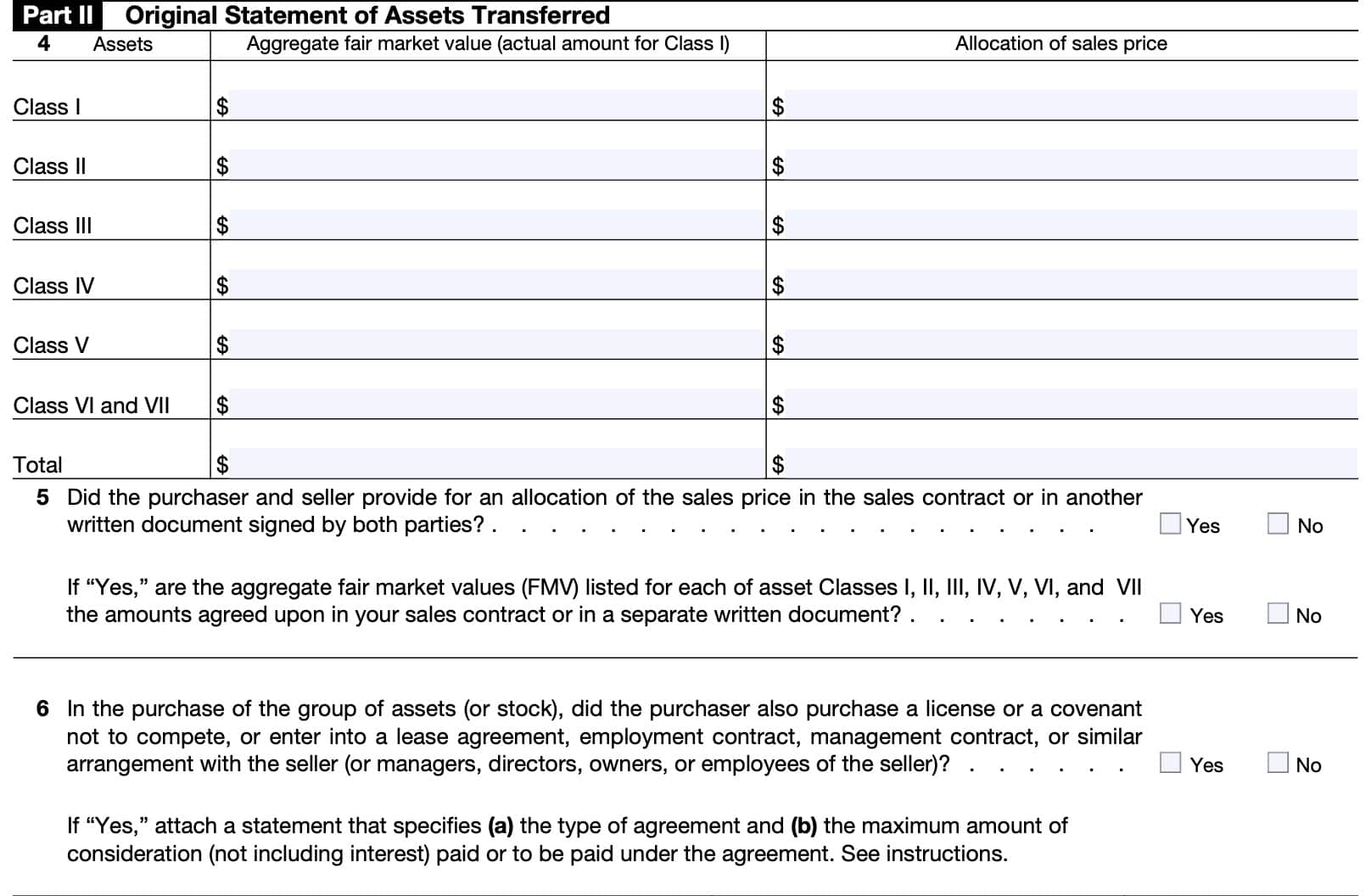

Part II: Original Statement of Assets Transferred

In Part II, we’ll document the fair market value of the assets transferred at the time of the sale, by asset class. Before we get to Line 4, let’s briefly go over the different classes of assets.

Classes of assets

For federal income tax purposes, below are the different asset classes, according to the Internal Revenue Service.

Class I

Class I assets are liquid assets, such as cash and general deposit accounts (including savings and checking accounts). However, this does not include certificates of deposit held in banks, savings and loan associations, and other depository institutions.

Class II

Class II assets are actively traded personal property within the meaning of Section 1092(d)(1) and Treasury Regulations section 1.1092(d)-1.

In addition, Class II assets include certificates of deposit and foreign currency even if they are not actively traded personal property. Class II assets do not include stock of seller’s affiliates, whether or not actively traded, other than actively traded stock described in Internal Revenue Code Section 1504(a)(4).

Examples of Class II assets include U.S. government securities and publicly traded stock.

Class III

Class III assets are assets that the taxpayer marks to market at least annually for federal income tax purposes and debt instruments, including accounts receivable.

However, Class III assets do not include:

- Debt instruments issued by persons related at the beginning of the day following the acquisition date to the target under IRC Section 267(b) or IRC Section 707;

- Contingent debt instruments subject to Treasury Regulations Sections 1.1275-4 and 1.483-4, or IRC Section 988

- Unless the instrument is subject to the noncontingent bond method of Treasury Regulations Section 1.1275-4(b) or is described in Regulations section 1.988-2(b)(2)(i)(B)(2); and

- Debt instruments convertible into the stock of the issuer or other property

Class IV

Class IV assets are the following:

- Stock in trade of the taxpayer, or

- Other property of a kind that would properly be included in the inventory of the taxpayer if on hand at the close of the tax year, or

- Property held by the taxpayer primarily for sale to customers in the ordinary course of business or trade

Class V

Generally, Class V assets are all assets other than Class I, II, III, IV, VI, and VII assets. The following items that constitute all or part of a trade or business are examples:

- Furniture and fixtures

- Real estate, such as buildings and land

- Vehicles

- Equipment

Class VI

This category of assets are Section 197 intangibles (as defined in IRC Section 197) except goodwill and going concern value.

The following are considered Class VI assets:

- Workforce in place

- Business books and records, operating systems, or any other information base, process, design, pattern, know-how, formula, or similar item

- Any customer-based intangible

- Any supplier-based intangible

- Any license, permit, or other right granted by a government unit

- Any covenant not to compete entered into in connection with the acquisition of an interest in a trade or a business and

- Any franchise, trademark, or trade name (however, see exception below for certain professional sports franchises)

Section 197 intangible assets do not include:

- An interest in a corporation, partnership, trust, or estate;

- Interests under certain financial contracts;

- Interests in land;

- Certain computer software;

- Certain separately acquired interests in films, sound recordings, videotapes, books, or other similar property;

- Interests under leases of tangible property;

- Certain separately acquired rights to receive tangible property or services;

- Certain separately acquired interests in patents or copyrights;

- Interests under indebtedness;

- Professional sports franchises acquired before October 23, 2004; and

- Certain transactions costs.

Class VII

Class VII assets are goodwill and going concern value, regardless of whether the goodwill or going concern value qualifies as a Section 197 intangible.

Line 4

For each particular class of assets, enter the following:

- Total fair market value of all the assets in the class, and

- Total allocation of the sales price in that asset class

For Classes VI and VII, enter the combined total fair market value of both classes, and the total combined portion of the sales price allocated to both classes.

Line 5

Did the purchaser and seller provide for an allocation of the sale price of the business in the sales contract, or in another written agreement signed by both parties? Answer Yes or No.

If the answer is yes, did you list the aggregate fair market values for each asset class as agreed upon in the sales contract or separate written document?

Line 6

In Line 6, answer Yes or No to the following question:

In the purchase of business assets (or stock sale), did the purchaser also:

- Purchase a license or covenant not to compete (noncompete agreement)

- Enter into a lease agreement, employment or management contract, or similar agreement with the seller

If Yes, attach a statement that specifies:

- The type of agreement and

- The maximum amount of consideration paid or to be paid under the agreement

- Not including interest

Both the purchaser and seller must complete Line 6. To determine the maximum consideration to be paid, assume that any specified contingencies in the written agreement have been met, resulting in the highest possible amount to be paid.

If you cannot determine maximum consideration, state how you will compute the consideration and the payment period.

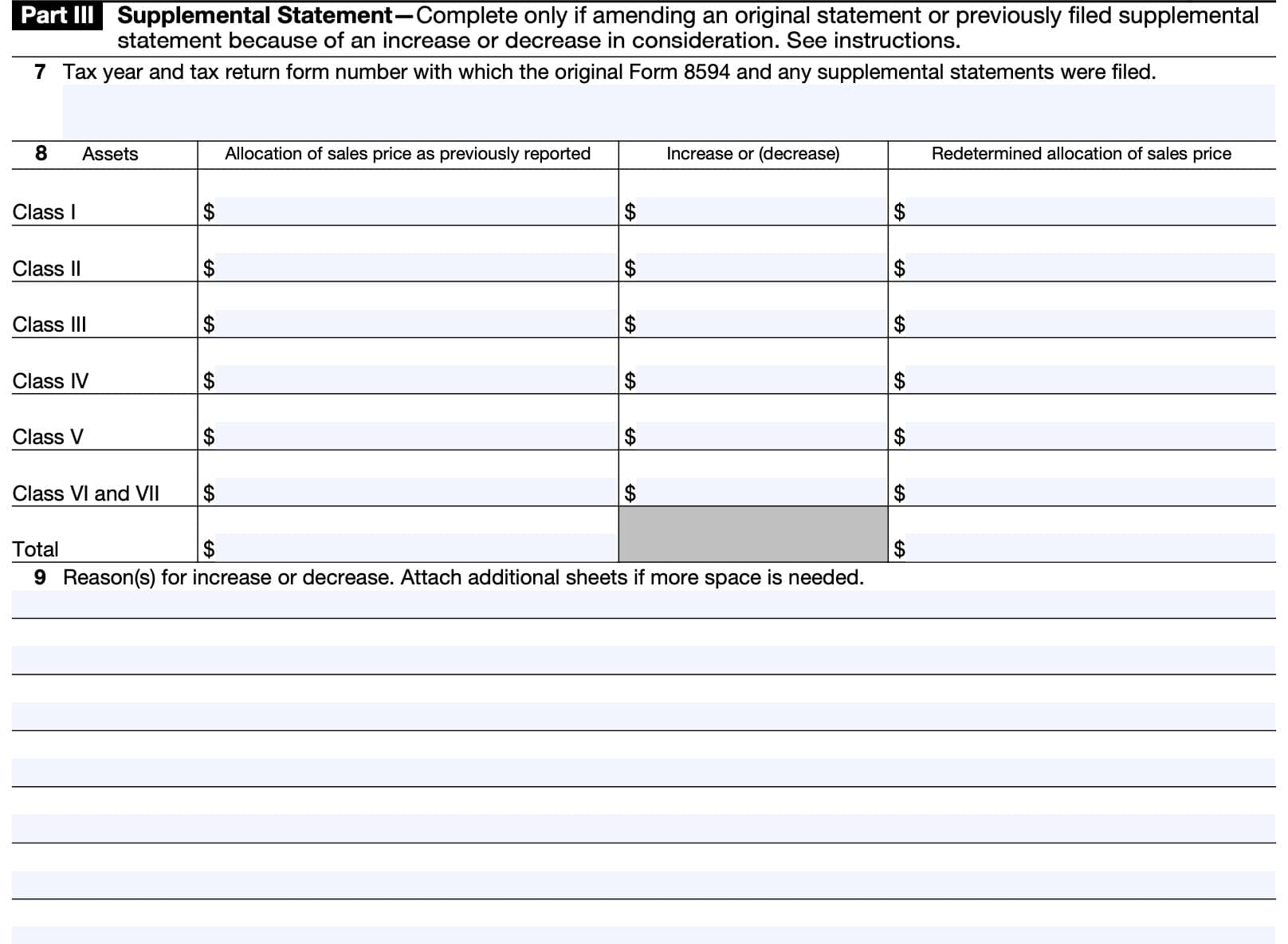

Part III: Supplemental Statement

You only need to complete Part III if an increase or decrease in consideration results in you amending:

- The original statement

- Previously filed supplemental statement

Line 7

In Line 7, enter the tax year and tax return form number that accompanied the original Form 8594 or any supplemental statements.

Line 8

For each class of asset, enter the following information:

- Previously reported allocation of the purchase price

- Increase or decrease in purchase price allocations

- Recalculated allocation

Ensure that the total amounts at the bottom of each column equal the total purchase price allocation for each of the different types of assets.

Line 9

In Line 9, enter any reasons for the increase or decrease in the value of the assets of the business. You may attach additional sheets as necessary.

Video walkthrough

Watch this informative video to learn more about reporting assets as part of a business sale using IRS Form 8594.

Frequently asked questions

Generally, both the purchaser and seller must file IRS Form 8594 and attach it to their respective tax returns when there is a purchase of a group of assets that makes up a trade or business and the purchaser’s basis in such assets is determined entirely by the amount paid for such assets.

You may file IRS Form 8594 electronically, as this fillable form is part of the IRS Free File fillable forms series. However, only one Form 8594 may be added to each income tax return.

Section 1060 of the Internal Revenue Code determines special allocation rules for different types of assets. Section 1060 helps taxpayers determine purchase price allocations for specific assets as part of a business transaction, as opposed to purchasing a piece of equipment.

Where can I find IRS Form 8594?

You can find this IRS Form 8594 on the IRS website. For your convenience, we’ve attached the latest version of this fillable form to this article.

Related tax forms

This tax form is one of the fillable tax forms provided by the Internal Revenue Service, to help taxpayers reduce their tax preparation costs. To see more forms like this, visit our free fillable tax forms page, where you’ll also find articles like this.

Unlike the IRS, our articles contain step by step instructions for each tax form, as well as video walkthroughs. You can also check out all of our videos by subscribing to our YouTube channel!