IRS Form 1098 Instructions

If you’re a homeowner paying interest on a mortgage, you might receive IRS Form 1098, Mortgage Interest Statement, in January of the following year. In this article, we’ll walk through what you need to know about IRS Form 1098, including:

- How to read and understand IRS Form 1098

- How to report mortgage interest and other payments on your income tax return

- Frequently asked questions

Let’s start with an overview of the tax form itself.

Table of contents

IRS Form 1098 instructions

In most of our articles, we walk you through how to complete the tax form. However, since Form-1098 is issued to taxpayers for informational purposes, most readers will probably want to understand the information reported on their 1098 form, instead of how to complete it.

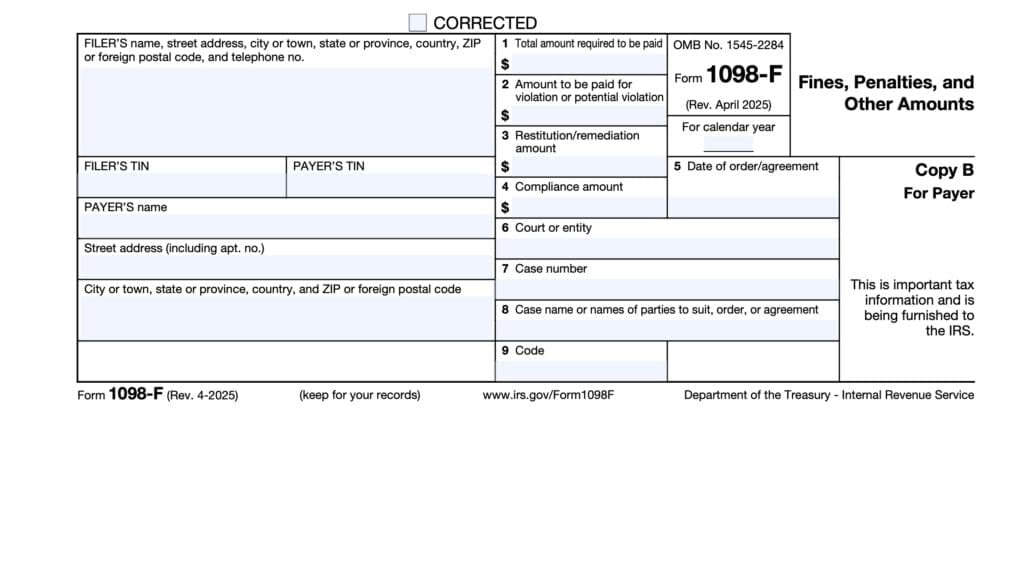

Before we start breaking down this tax form, it’s important to understand that there can be up to 3 copies of IRS Form 1098. Here is a break down of where all these forms end up:

- Copy A: Internal Revenue Service center

- Copy B: For payer or borrower

- Copy C: For the lender

Let’s get into the form itself, starting with the taxpayer information fields on the left side of the form.

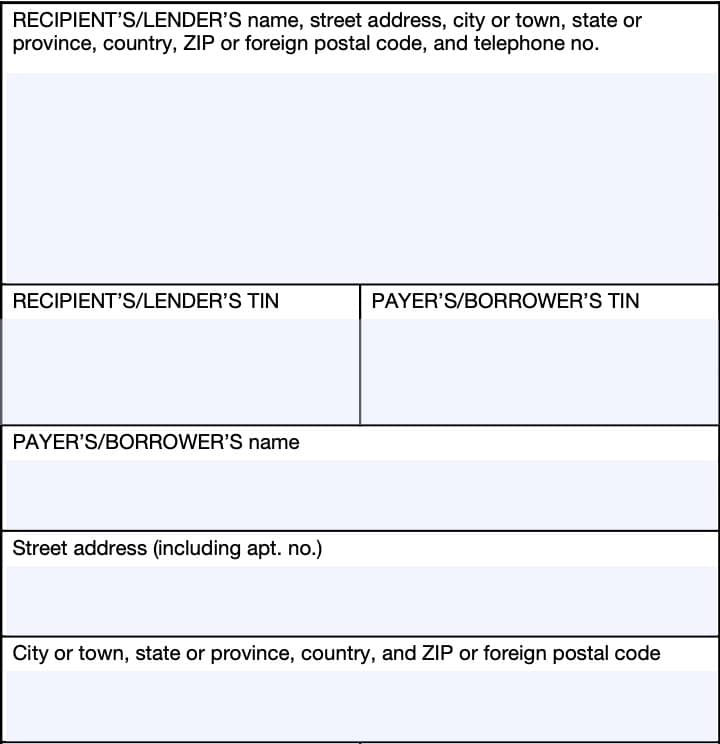

Taxpayer identification fields

On the left-hand side of the tax form, you’ll see important information for both the lender and the borrower.

Lender’s Name, Address, And Telephone Number

You should see the lender’s contact information, with complete business name, address, zip code, and phone number in this field.

Lender’s TIN

This is the filer’s taxpayer identification number (TIN). In most situations, this will be the employer identification number (EIN).

The lender’s TIN should never be truncated.

Borrower’s TIN

As the recipient of IRS Form 1098, you should see your taxpayer identification number in this field. The TIN can be any of the following:

- Social Security number (SSN)

- Individual taxpayer identification number (ITIN)

- Adoption taxpayer identification number (ATIN)

- Employer identification number (EIN)

Please review this field to make sure that it is correct. However, you may see a truncated form of your tax identification number (such as the last four digits of your SSN), for privacy protection purposes.

Copy A, which is sent to the Internal Revenue Service, is never truncated.

Borrower’s Name And Address

You should see your legal name and address reflected in these fields. If your address is incorrect, you should notify the lender and the IRS.

You can notify the IRS of your new address by filing Form 8822, Change of Address. Business owners can notify the IRS of a change in their business address by filing IRS Form 8822-B, Change of Address or Responsible Party, Business.

Let’s check out the numbered fields, which start on the right-hand side of this tax form.

Boxes 1 through 11

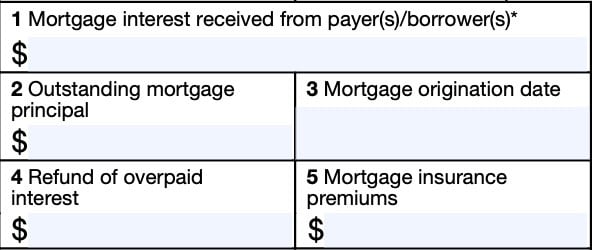

Box 1: Mortgage interest received from payer(s)/borrower(s)

Box 1 shows the amount of interest received by the recipient/lender during the calendar year. This amount includes interest on any obligation secured by real property, including

- Mortgage

- Home equity loan, or

- Home equity line of credit

The amount of mortgage interest reported in Box 1 does not include any of the following:

- Points

- Government subsidy payments, or

- Seller payments on a ‘buydown’ mortgage loan

Interest does include prepayment penalties and late charges unless the late charges are for a specific mortgage service.

Prepaid interest

If you prepaid interest in the calendar year that accrued in full by January 15, of the subsequent tax year, this prepaid interest may be included in Box 1. However, you cannot deduct the prepaid portion of the interest even though it may be included in Box 1.

Mortgage credit certificate

If you hold a mortgage credit certificate and are eligible for the mortgage interest credit, you may need to complete IRS Form 8396 to claim the mortgage interest credit on your federal income tax return.

If you paid the interest on a mortgage, home equity loan, or line of credit secured by a qualified residence, you can only deduct the interest paid on acquisition indebtedness in the reporting year. Even then, the Internal Revenue Code may limit your deduction based on how much mortgage interest you paid or your tax liability.

Box 2: Outstanding mortgage principal

This box shows the outstanding principal on the mortgage as of January 1 of the calendar year. If the mortgage originated in the calendar year, Box 2 shows the mortgage principal as of the date of origination, in Box 3.

If the recipient or mortgage lender acquired the loan in the calendar year, shows the mortgage principal as of the date of acquisition.

Box 3: Mortgage origination date

Box 3 shows the date that your lender originated the current mortgage.

For mortgage providers who acquired this mortgage, Box 3 will show the the date that the original lender originated the mortgage. The date of acquisition will appear in Box 11, below.

Box 4: Refund of overpaid interest

Box 4 contains any refund or credit for overpayment(s) of interest you made last year or in a prior year.

If you itemized deductions in the year or years that you paid this interest, you may have to include part or all of the Box 4 amount on the ‘Other income’ line of your calendar year Schedule 1 when filing your individual tax return.

For tax purposes, you do not need to make any adjustments to a federal tax return that you filed in a previous year. You can find additional information in the following IRS publications:

- IRS Publication 936, Home Mortgage Interest Deduction

- IRS Publication 525, Taxable & Nontaxable Income

According to the Form 1098 instructions, taxpayers should not deduct any amounts listed in Box 4.

Box 5: Mortgage insurance premiums

Box 5 contains any mortgage insurance premiums, such as private mortgage insurance, or PMI. For itemized deductions on IRS Schedule A, mortgage insurance premiums are no longer allowed.

However, the IRS website states that taxpayers may deduct mortgage insurance premiums paid for rental property in the year premiums were paid. Taxpayers with rental property can report mortgage insurance premiums and other related expenses on Line 9 of IRS Schedule E, Supplemental Income.

If an amount is reported in Box 5, it may qualify to be treated as deductible mortgage interest. You may find more detailed information on the deductibility of mortgage premiums in the Schedule A instructions and in Publication 936.

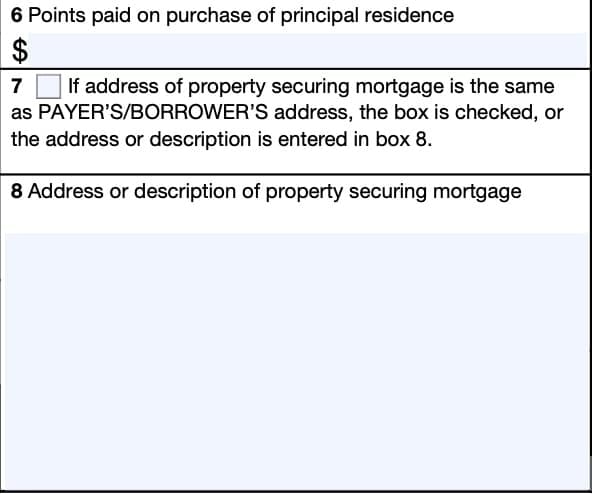

Box 6: Points paid on purchase of principal residence

Box 6 shows points you or the seller paid this year for the purchase of your principal residence that are required to be reported to you.

Generally, these points are fully deductible from taxable income in the year paid. However, you must subtract seller-paid points from the basis of your residence.

You may be able to deduct other points not reported in Box 6.

Reportable points

According to the Form 1098 instructions, your financial institution must report points that

meet all the following conditions:

- They are clearly designated on the Settlement Statement (Form HUD-1) or HUD Closing Disclosure as points. They may contain the following verbiage:

- Loan origination fee (this includes origination fees for VA loans and FHA loans)

- Loan discount

- Discount points

- Points

- They are computed as a percentage of the stated principal loan amount.

- They are charged under an established business practice of charging points in the area where the loan was issued and do not exceed the amount generally charged in that area.

- They are paid for the acquisition of the payer of record’s principal residence, and the loan is secured by that residence.

- They are paid directly by the payer of record.

Points that are not reportable

Financial institutions are not required to include the following points on a mortgage interest statement, even if you might be able to deduct a portion of them on your tax return:

- For loans to improve a principal residence

- For loans to purchase or improve a residence that is not the payer of record’s principal residence

- Examples include second home, vacation, investment, or trade or business property, even

- The borrower may be entitled to amortize points paid for the purchase and deduct them over the life of the mortgage

- For a home equity or line of credit loan, even if secured by the principal residence;

- For refinancing, including a loan to refinance a debt owed by the borrower

under one of the following:- Land contract

- Contract for deed,

- or similar forms of seller financing

- In lieu of items ordinarily stated separately on the Form HUD-1:

- Appraisal fees

- Inspection fees

- Title fees

- Attorney fees, and

- Property taxes

- To acquire a principal residence to the extent the points are allocable to an amount of principal in excess of the amount treated as acquisition indebtedness

Box 7

If the address of the property securing the mortgage is the same as the payer’s/borrower’s address, then either:

- A checkmark will appear in Box 7

- The filer will have completed Box 8 with the property address

If the address or description of the property securing the mortgage is not the same as the payer’s/borrower’s mailing address, the address or description of the property that is securing the mortgage will appear in Box 8.

Box 8: Address or description of property securing mortgage

This box will show the address or description of the property securing the mortgage. If the property securing the mortgage does not have an address, then you may see a legal description in Box 8 instead.

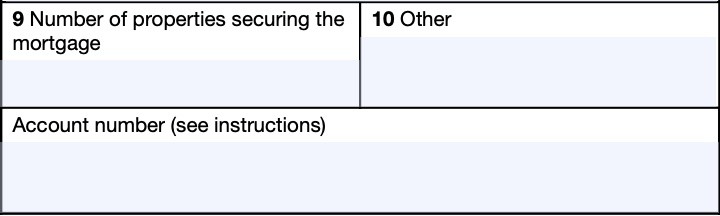

Box 9: Number of properties securing the mortgage

If more than one property secures the loan, Box 9 should indicate the number of properties securing the mortgage. If only one property secures the loan, this box may be blank.

Box 10: Other

The interest recipient may use this box to give you other information, such as real estate taxes or insurance paid from escrow. However, this field is optional.

Account number

Just below Boxes 9 & 10, you’ll see the field for Account number.

This field is present in many information returns, such as IRS Form 1099-INT or IRS Form 1099-DIV.

Your lender have established a unique account number for you, which may appear in this field. If the field is blank, you may ignore it.

However, IRS instructions dictate that the account number is required if the filer has:

- Created multiple accounts for a recipient, and

- Is filing more than one Form 1098 for that person

In this situation, you would expect to see a separate Form 1098 for each account number.

Let’s move on to the last item, Box 11.

Box 11: Mortgage acquisition date

If the recipient/lender acquired the mortgage in the calendar year, Box 11 will show the date of acquisition. Otherwise, it should be blank.

Filing IRS Form 1098

For tax entities who must file this tax form with the Internal Revenue Service, the IRS requires certain paper versions of information returns to be accompanied by IRS Form 1096, Annual Summary and Transmittal of U.S. Information Returns.

Check out our step-by step instructional guide for more information on how to submit your information return with IRS Form 1096.

Deducting mortgage payments on your tax return

Most people are familiar with the tax benefits of deducting mortgage interest payments as an itemized deduction on Schedule A. However, this is only one way that mortgage payments may be used to lower taxable income.

However, there are different ways that interest payments may be deducted from your income, based upon your situation. IRS Publication 936, Table 2 outlines how taxpayers may be able to deduct interest paid, so we’ve re-created that table here:

| IF you have … | THEN deduct it on … | AND for more information, go to … |

| Deductible student loan interest (i.e. student loan interest deduction) | IRS Schedule 1, Line 21 | IRS Publication 970, Tax Benefits for Education |

| Deductible home loan interest & points reported on Form 1098 | IRS Schedule A, Line 8a | IRS Publication 936 |

| Deductible home mortgage interest not reported on Form 1098 | IRS Schedule A, Line 8b | IRS Publication 936 |

| Deductible points not reported on Form 1098 | IRS Schedule A, Line 8c | IRS Publication 936 |

| Deductible investment interest (not incurred to produce rents or royalties) | IRS Schedule A, Line 9 | IRS Publication 550, Investment Income & Expenses |

| Deductible business interest (non-farm) | IRS Schedule C | |

| Deductible farm business interest | IRS Schedule F | IRS Publication 225, Farmer’s Tax Guide |

| Deductible interest incurred to produce rental income or royalties | IRS Schedule E | IRS Publication 527, Residential Rental Property |

| Personal interest (such as debt used to pay off car loans) | Not deductible |

Video walkthrough

Watch this informative video to learn more about your mortgage interest statement!

Frequently asked questions

Lenders, such as banks and financial institutions must use Form 1098, Mortgage Interest Statement, to report mortgage interest payments of $600 or more received during the year, in the course of your trade or business from an individual, including sole proprietorships.

As with other information returns, taxpayers should expect to receive IRS Form 1098 by January 31st of the tax year following the year in which they paid mortgage interest.

Most lenders and mortgage servicers file information returns such as IRS Form 1098 electronically, and make them available to taxpayers online. If you have not received your form by the end of January, or for more information, you should contact your lender.

Where can I find IRS Form 1098?

As with other tax forms, you may find IRS Form 1098 on the IRS website. For your convenience, we’ve included the most recent version of this IRS tax form right here in our article.

I need my filled out form emailed to me today I’m doing my taxes and I don’t see where they mailed it to me

If it’s a mortgage statement, and you have an online account, then you might be able to download this form from your account. If not, you should contact your mortgage company to see how you can get this form from them.

The form 1098’s paper form has 2, 1098’s per page. Are we supposed to fill out both if you only have 1 Owner Financed Mortgage to report?

If you’re issuing a Form 1098 to someone who has paid mortgage interest to you, then you’ll need to file 1 copy with the IRS, and give the other copy to the borrower. These two should be identical, except for the taxpayer identification number. The IRS copy should contain the full 9-digit number, while the borrower copy should be redacted (***-**-1234).