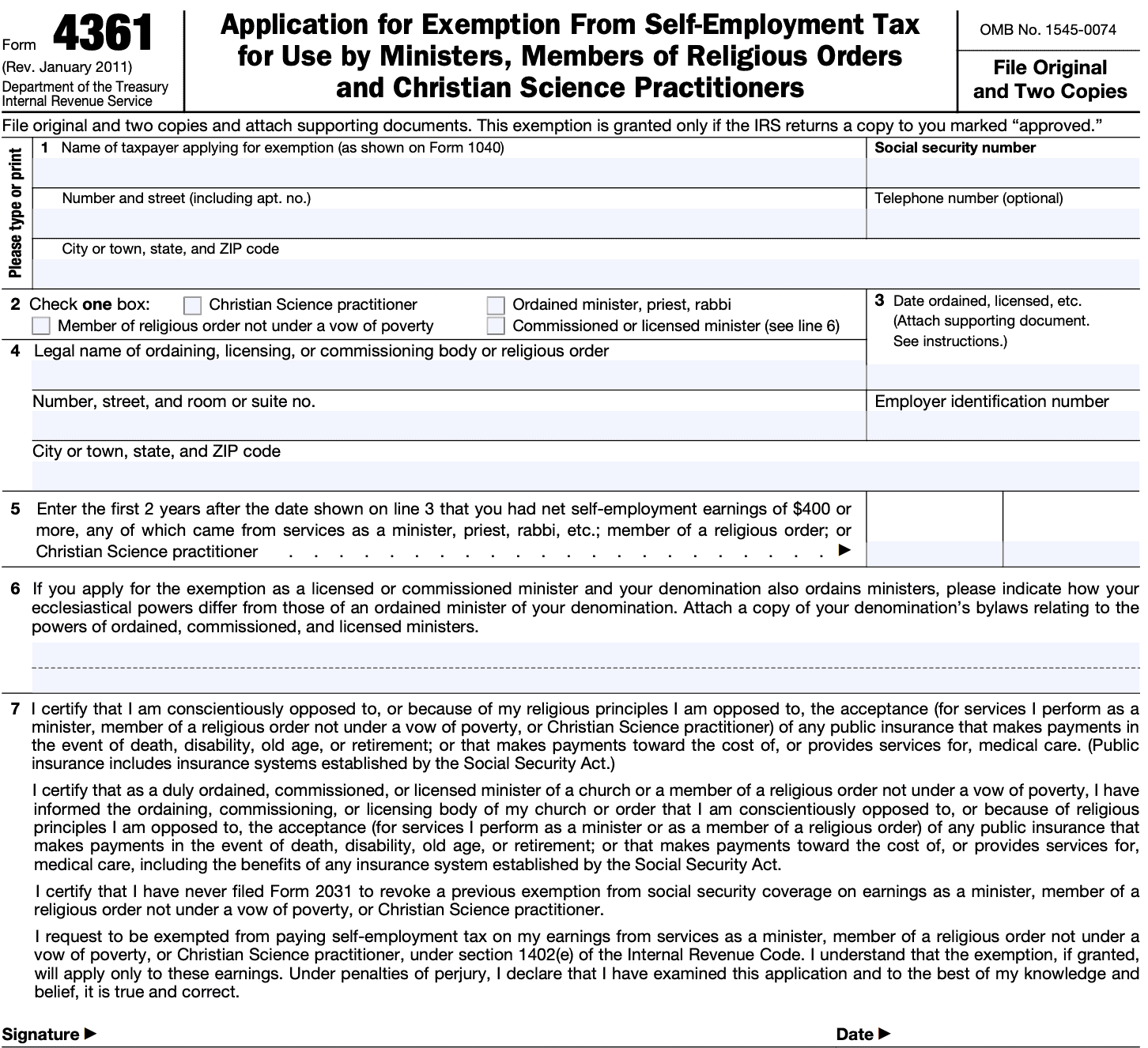

IRS Form 4361 Instructions

If you’re a minister of a church, clergy member, or member of a religious order, you may be eligible to claim an exemption from self-employment taxes when you file your income tax return. In this article, we’ll walk through IRS Form 4361 so you can better understand:

- Who is able to claim an exemption from SE tax on their self-employment income

- How to complete this tax form

- How to file Form 4361 to claim your exemption

Let’s start with step by step instructions for IRS Form 4361.

Table of contents

How do I complete IRS Form 4361?

Fortunately, this one-page IRS form is fairly straightforward. We’ll go through it one step at a time.

Recordkeeping notes

Before we begin, you’ll need to file the original Form 4361, as well as two copies and supporting attachments. As a best practice, you should keep a copy of the form for your records, even if a tax preparer completes the form for you.

Filing this form does not guarantee an exemption. The IRS must approve your signed copy before you can claim the exemption. Once you have an copy of the approved form, keep this important document in your records.

Completing IRS Form 4361

Line 1: Taxpayer information

Enter the name of the taxpayer applying for the exemption, as shown on IRS Form 1040. Include the taxpayer’s Social Security number, address (including city, state, and zip code), and telephone number.

Line 2: Religious order

Check one of the following boxes:

- Christian Science practitioner

- Ordained minister, priest, or rabbi

- Member of religious order not under a vow of poverty

- Commissioned or licensed minister

If you check the box for commissioned or licensed minister, you may need to attach additional documentation, as outlined in Line 6, below.

Line 3: Date ordained or licensed

Self-explanatory. Attach a letter from the governing body of your church that establishes your status as:

- An ordained, commissioned, or licensed minister

- Member of a religious order, or

- Christian Science practitioner

Do not file Form 4361 before the date on your certificate.

Line 4: Religious order information

Enter the legal name of the religious order, as well as employer identification number (EIN) and address (including city, state, and zip code).

You must demonstrate that your religious body is:

- Exempt from federal income tax under Section 501(a) as a religious organization described in Section 501(c)(3), and

- A church, or convention or association of churches, as described in IRC Section 170(b)(1)(A)(i).

To assist the IRS in processing your application, you can attach a copy of the exemption letter issued to the organization by the IRS.

Line 5

Enter the first 2 years after the date on Line 3 in which you had net self-employment earnings of $400 or more, any of which came from your services as a:

- Minister

- Priest

- Rabbi

- Member of a religious order, or

- Christian Science practitioner

Line 6

If you did not check the box for licensed or commissioned minister in Line 3, you may skip this line and proceed to Line 7.

If you apply for the exemption as a licensed or commissioned minister and your denomination also ordains ministers, you will need to explain how your ecclesiastical powers as an unordained worship minister differ from those of an ordained minister. Attach a copy of your church denomination bylaws relating to the powers of an ordained minister of the church.

Line 7

Line 7 simply states the following conditions, under penalties of perjury:

- Taxpayer certifies that he or she is conscientiously opposed to the acceptance of any public insurance (including insurance systems established by the Social Security Act) that makes payments:

- In the event of death or disability

- For old age or retirement

- Towards the cost of medical care or provides medical care services

- Taxpayer certifies that he or she has informed the ordaining, commissioning, or licensing body of the church that he or she opposes any public insurance

- Taxpayer certifies that he or she has never filed IRS Form 2031 to revoke a previous exemption from Social Security coverage on net earnings, and

- Taxpayer requests exemption from paying tax on net self-employment earnings from ministerial services under Section 1402(e) of the Internal Revenue Code

Remember, this declaration is under penalty of perjury. If you agree with these statements, sign and date the form.

Before claiming the exemption, you must receive approval from the IRS. The IRS will return your Form 4361 marked either:

- Approved for exemption from self-employment tax on ministerial earnings, or

- Disapproved for exemption from self-employment tax on ministerial earnings

What is IRS Form 4351?

IRS Form 4351 is titled, “Application for Exemption From Self-Employment Tax for Use by Ministers, Members of Religious Orders and Christian Science Practitioners.” This might be the longest title that the Internal Revenue Service has given to one of its tax forms. If you’re looking to exclude self-employment taxes from your ministerial earnings, this is the form you should file.

Who can claim an exemption from self-employment taxes with IRS Form 4361?

Generally speaking, a taxpayer may file Form 4361 to apply for a self-employment tax exemption if they have ministerial earnings and are one of the following:

- An ordained, commissioned, or licensed minister of a church;

- A member of a religious order who has not taken a vow of poverty; or

- A Christian Science practitioner

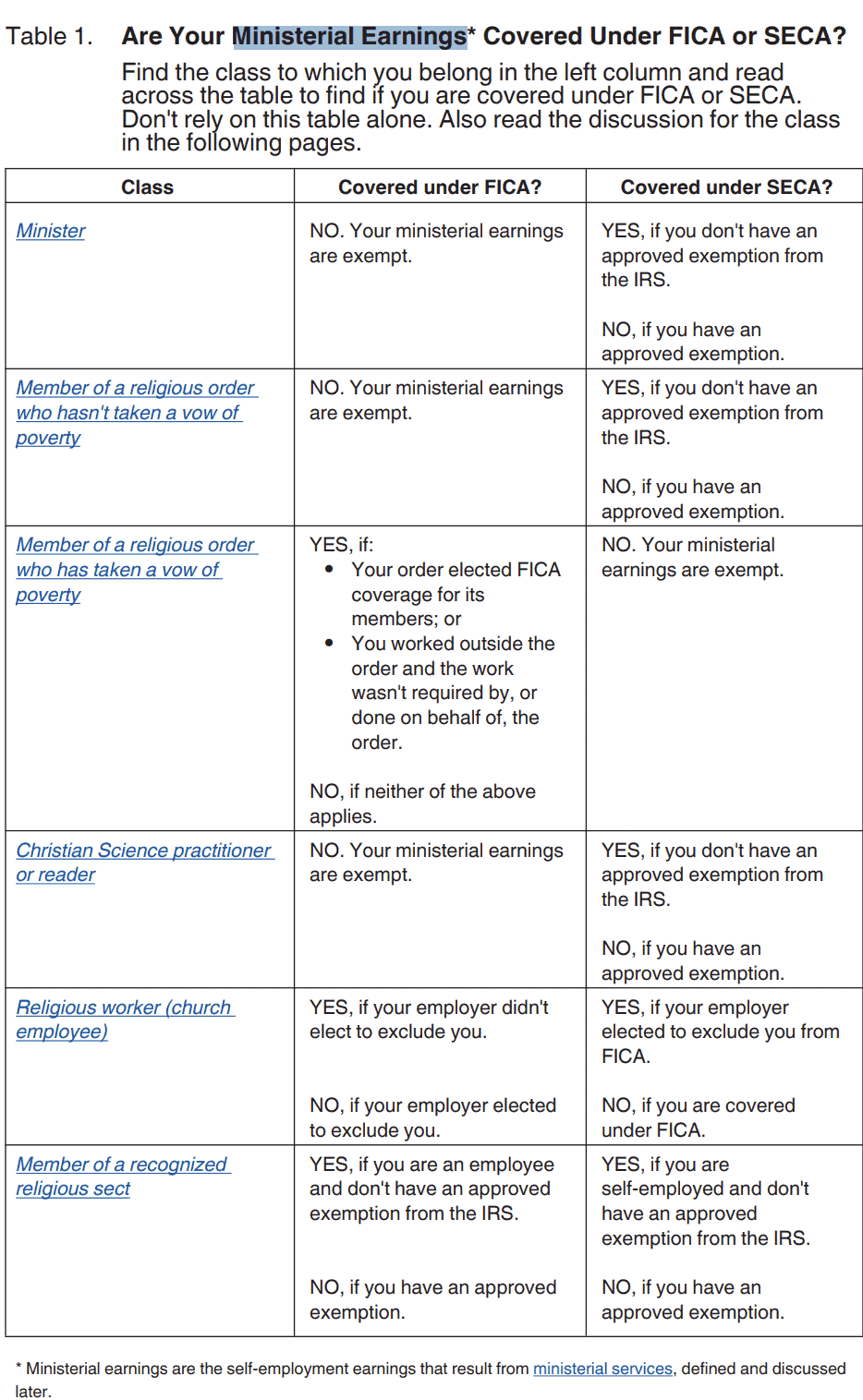

What are ministerial earnings?

As noted above, ministerial earnings are the self-employment earnings that result from providing ministerial services. In turn, ministerial services are the services performed in:

- The exercise of a ministry

- The exercise of duties required by one’s religious order, or

- The exercise of one’s profession as a Christian Science practitioner or reader

The below chart from IRS Publication 517, Social Security and Other Information for Members of the Clergy and Religious Workers outlines the various types of religious workers, and who may apply for a self-employment tax exemption.

Other requirements to claim an exemption from self-employment taxes

Besides filing IRS Form 4361, IRS Publication 517 outlines other criteria a taxpayer must meet in order to be exempt from self-employment taxes on their ministerial earnings.

In addition to completing Form 4361, a taxpayer must:

- Be conscientiously opposed to the acceptance of public insurance because of their individual religious considerations, or opposed because of the principles of their religious denomination

- A taxpayer’s general conscience does not count

- File for other than economic reasons

- Inform the ordaining, commissioning, or licensing body of their church or order that they are opposed to public insurance

- This does not apply to Christian Science practitioners or readers

- Establish that the religious order is a tax-exempt religious organization

- Establish that the organization is a church or convention or association of churches

- Did not previously make an election earlier that:

- Revoked their exemption from Social Security by filing IRS Form 2031, or

- Before 1968, covered the taxpayer under Social Security for ministerial earnings

- Sign and return the IRS statement to certify they are requesting an exemption, per IRC Section 1402(e), based upon the grounds listed on the statement

In other words, a taxpayer must demonstrate that their religious principles preclude their acceptance of Social Security benefits or Medicare benefits in order to be excluded from paying Social Security taxes or Medicare taxes.

Let’s move on to how to complete this tax form.

How do I file IRS Form 4361?

A taxpayer seeking to exclude their net ministerial income from self-employment taxes must file Form 4361 by the due date of their tax return for the second year in which he or she had at least $400 of net earnings from self-employment, any of which came from ministerial services.

To do this, mail the original and two copies of this tax form to:

Department of the Treasury

Internal Revenue Service Center

Philadelphia, PA 19255-0733

Be sure to wait for the IRS approval before claiming the exemption on your federal tax return.

Video walkthrough

Watch this instructional video to learn more about obtaining your self-employment tax exemption by filing Form 4361.

Frequently asked questions

You should file Form 4361 by your tax return’s due date, including extensions, for the second tax year in which you had at least $400 of net earnings from self-employment, any of which came from ministerial services.

No. Exemption from self-employment tax does not apply to earnings from

services that are not ministerial.

If the IRS approves your application marked and your only self-employment income was from

ministerial services, enter “Exempt—Form 4361” on the self-employment tax line in the Other

Taxes section of Form 1040.

Where do I find a copy of IRS Form 4361?

You can download a copy of this tax form from the IRS website or by selecting the link below.

I found you on YouTube. My husband is a pastor who received an approved form 4361 in 1995 from the IRS while pastoring a church in IL. We have just moved to a new church in VA and I cannot find the approved paperwork. How can I request a copy from the IRS to provide to the new church?

Thanks for any guidance you can provide

If your husband has had an approved Form 4361 for that long, he should still be able to maintain his exemption.

To find proof that his Form 4361 is on file, you may try creating an IRS online, then checking your husband’s IRS transcript: https://youtu.be/W4HH11VWYJ4

If you cannot find his exemption in the transcript, you may need to call the IRS at 1-800-829-1040 to confirm that the form is still on file. Finally, if you use a tax preparation service, they might have a copy on file as documentation from previous returns.

If the priests receive a salary and taxes are withheld, can they complete Form 4361 to seek exemption from taxes? Are their salaries classified as self-employment earnings?

Certain religious practitioners and minsters can request an exemption from self-employment tax due to religious grounds. This would be Social Security and Medicare tax that the person would otherwise pay into. However, this is only for ministerial earnings, and does not apply to self-employment income from non-ministerial sources. Also, this does not apply to income tax.