IRS Form 8858 Instructions

In the United States, there is an additional tax filing requirement for someone who either owns a foreign entity or the foreign branch of a U.S. corporation. Sometimes the Internal Revenue Service requires a U.S. taxpayer who has an ownership interest in certain foreign entities to file IRS Form 8858 with their federal income tax return.

In this article, we’ll walk through this tax form and answer some frequent questions, such as:

- What is IRS Form 8858

- Who must file this tax form

- How to file IRS Form 8858, and when to submit it

Let’s begin by walking through this IRS form step by step.

Table of contents

How do I complete IRS Form 8858?

Let’s walk through this tax form, step by step, starting at the top.

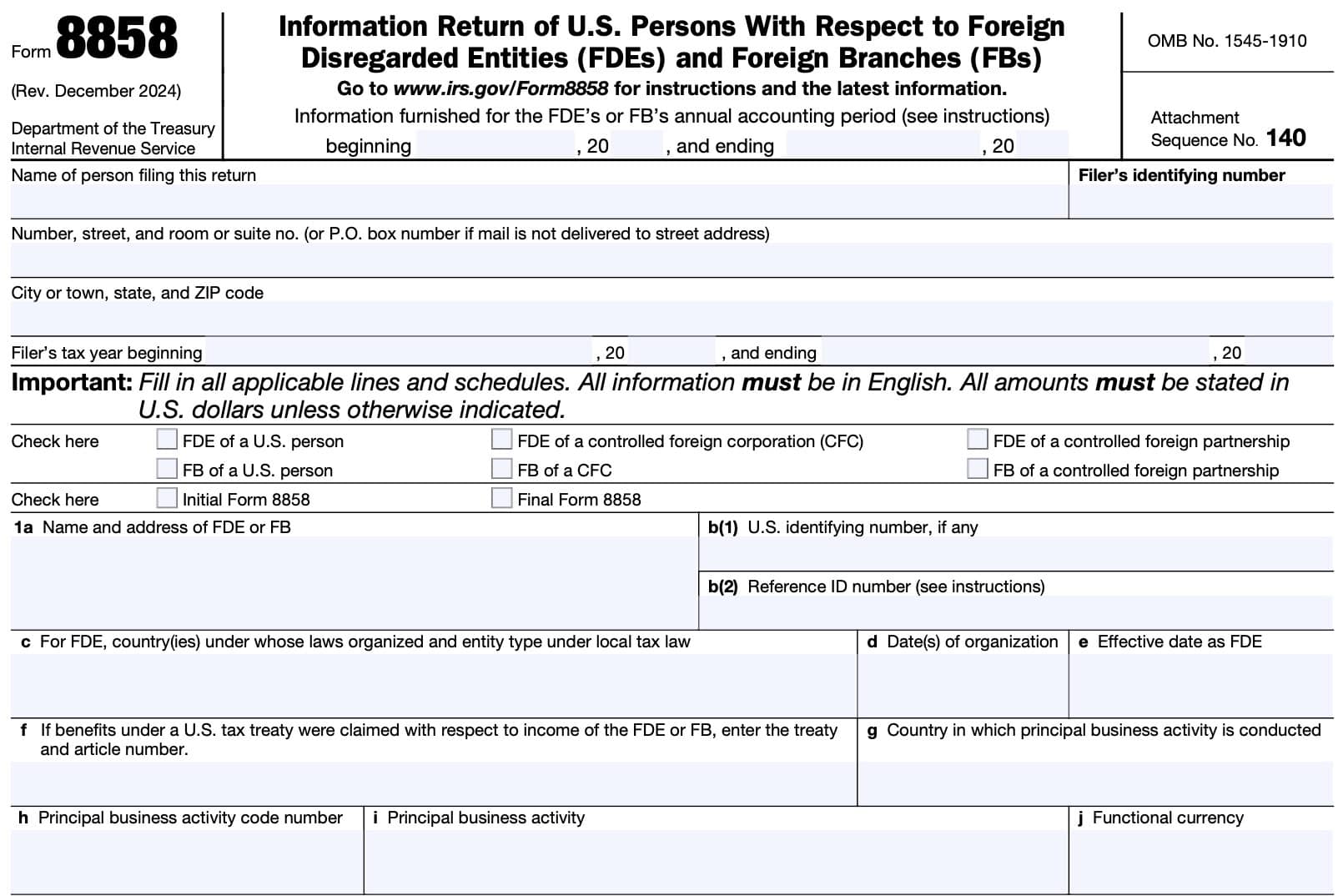

Taxpayer information

At the top of this form, fill in the beginning and ending dates of the accounting period of the respective FDE or FB.

Note: If you have multiple FDEs or FBs, you must file a separate form for each separate entity or business activity.

Identifying information

Complete the identifying information of the U.S. person completing this form, to include:

- Name

- Identifying number (taxpayer’s Social Security number)

- Address, including city, state, and zip code,

- Taxpayer’s tax year beginning and end dates

Check the appropriate box for whether the entity is:

- The FDE of a U.S. person

- FDE of a controlled foreign corporation (CFC)

- FDE of a controlled foreign partnership (CFP)

- The FB of a U.S. person

- FB of a CFC

- FB of a CFP

Also, check the appropriate box for whether this is an initial Form 8858 or final form.

Line 1

Under Line 1, fill in the following:

- Name and address of FDE or FB

- Identifying number-This will likely be the employer identification number (EIN). If there is no EIN, enter a reference ID number in Line 1b(2)

- Country under whose laws the FDE exists. Use the 2-letter IRS country code

- Date(s) of organization

- Effective date

- Treaty and article number, if applicable

- Principal business activity, and the country in which the FDE or FB conducts business

- Functional currency: Use the three-letter ISO currency code

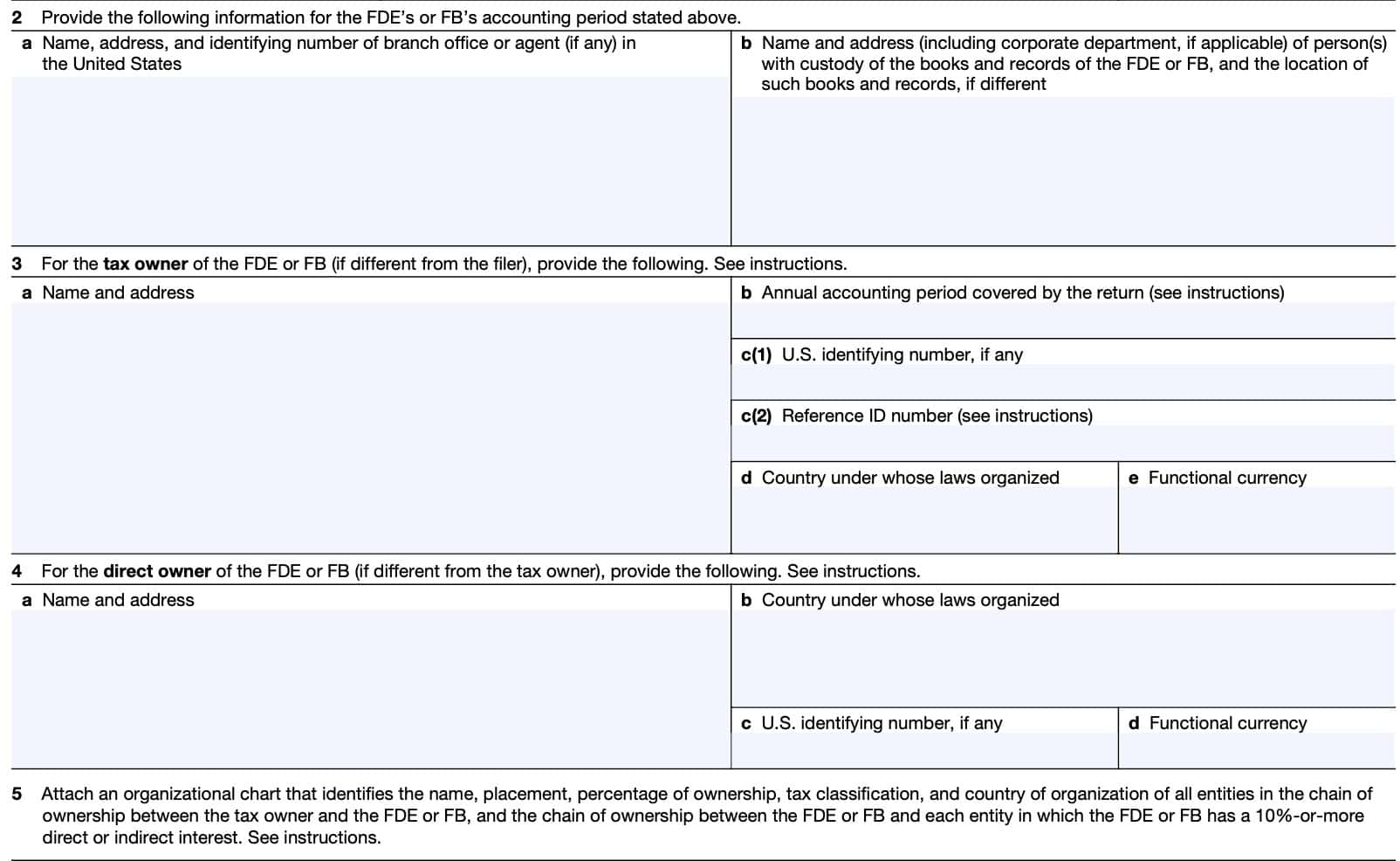

Line 2: Accounting period

In Line 2, provide the name, address, and identifying number of the branch office located in the United States. If different, also provide the name and address of the person(s) with custody of the books and records for the FDE or FB.

Line 3: Tax owner information

If the tax owner is different from the filer, provide:

- Name and address

- Accounting period covered by the return

- Identifying number or reference ID number

- Country and functional currency

Line 4: Direct owner

If different from tax owner, provide the following information for the direct owner:

- Name and address

- Country under whose laws organized

- Identifying number

- Functional currency

If there is more than one direct owner, provide a separate Form 8858 for each owner, containing the requested information.

Line 5: Organizational chart

The following requirement applies to any chains of ownership between the tax owner and the FDE or FB and all entities in which the FDE or FB has a 10% or more direct or indirect interest.

You must attach an organizational chart that includes the following information:

- The name and percentage of ownership of all entities in the chain of ownership. This includes partnerships and entities disregarded as separate from their owners

- The FDE’s or FB’s position in the chain of ownership

- The tax classification of all entities in the chain of ownership (see the Form 8832 instructions for tax classification rules and related definitions)

- The country under whose law each entity is organized

For these purposes, the rules of Section 958(a) relating to “direct and indirect ownership” apply.

Each filer of Form 8858 that is required to file an organizational chart may satisfy this requirement by filing a single organizational chart that includes the required information with respect to all FDEs and FBs.

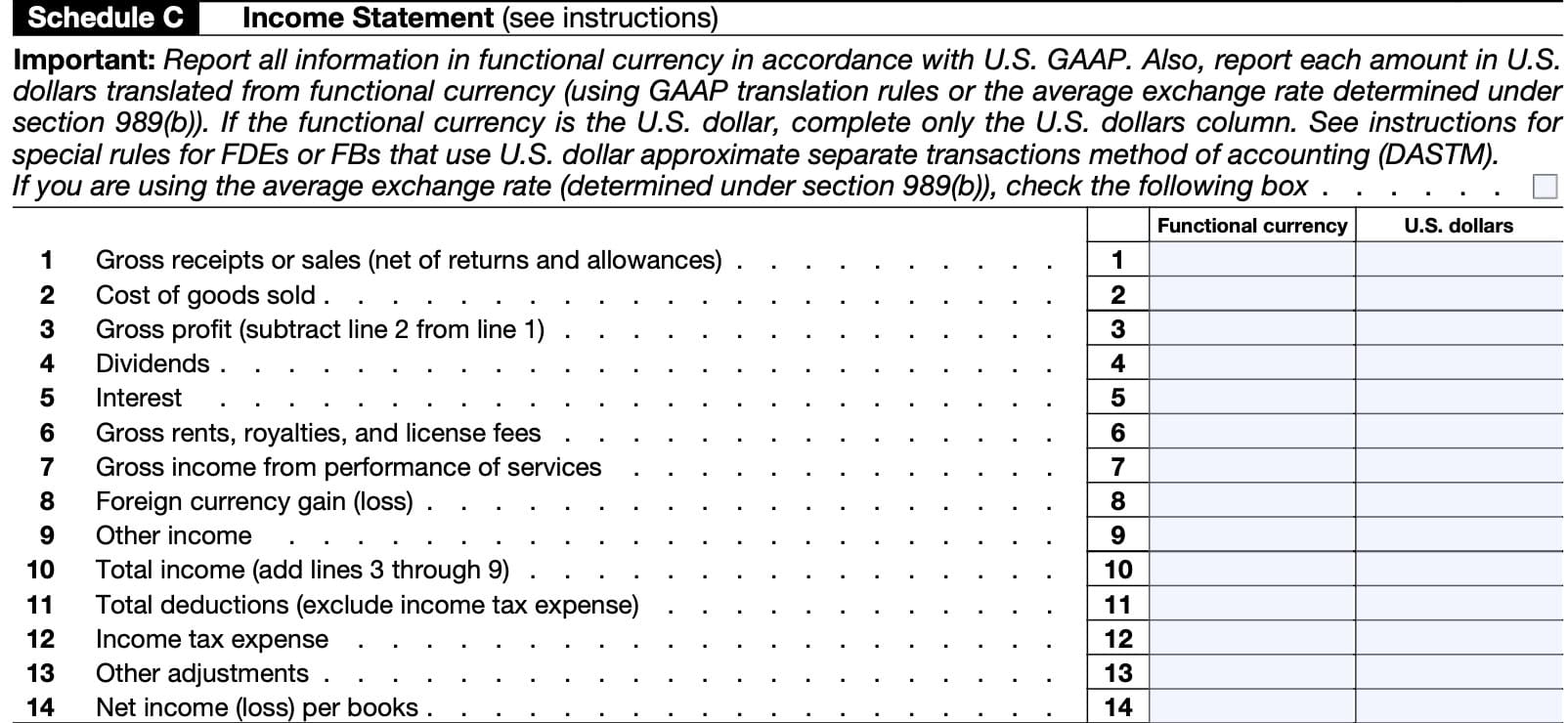

Schedule C: Income Statement

Use Schedule C to provide a summary income statement for the FDE or FB figured in the FDE’s or FB’s functional currency in accordance with U.S. GAAP (Generally Accepted Accounting Principles.

If the FDE or FB does not maintain U.S. GAAP income statements in U.S. dollars, you can use the average exchange rate as determined under Section 989(b).

The rate used should be same rate stated as on Schedule H, Line 8. If you choose to use the average exchange rate rather than the U.S. GAAP translation rules, check the box above Line 1 on Schedule C.

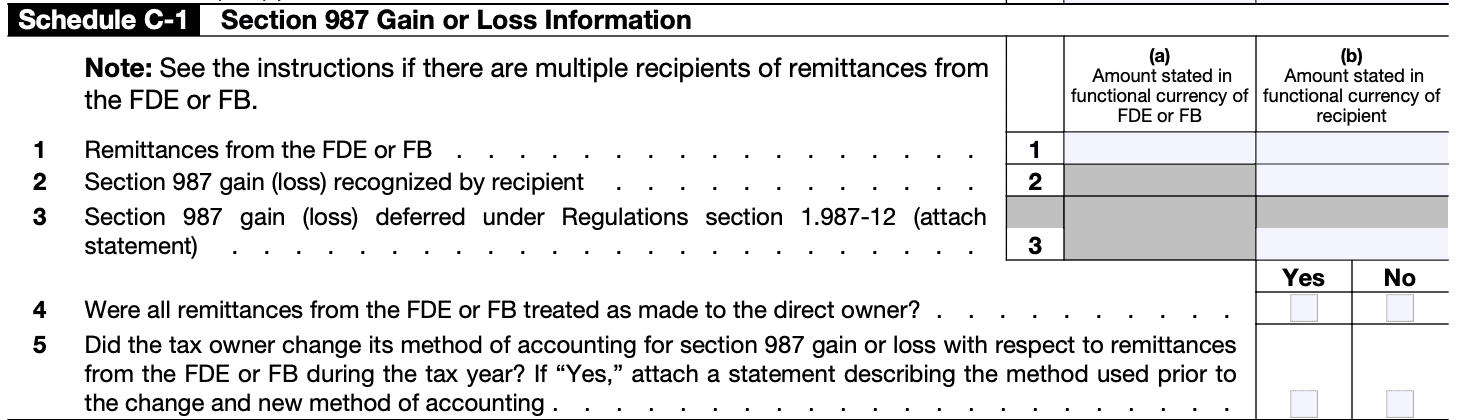

Schedule C-1: Section 987 Gain or Loss Information

Use Schedule C-1 to report Section 987 gain or loss realized by a QBU. If the QBU has a different functional currency than its owner, then such owner may be subject to Section 987 rules.

For an owner who owns multiple QBUs, complete a separate Schedule C-1 with respect to each QBU of the owner. If a QBU has multiple owners, complete a separate Schedule C-1 for each owner.

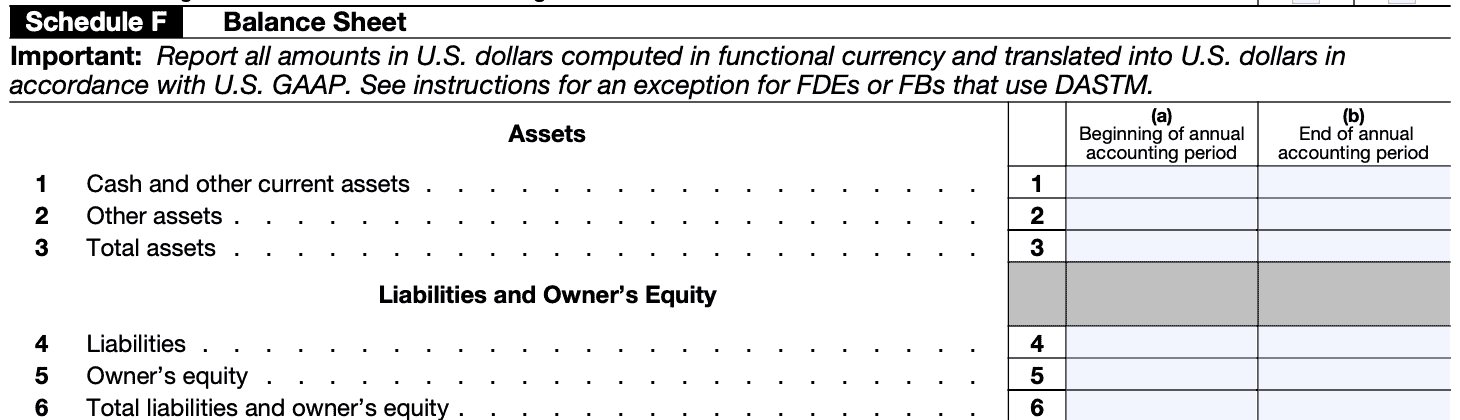

Schedule F: Balance Sheet

Use Schedule F to report a summary balance sheet translated into U.S. dollars from the functional currency.

If the FDE or FB uses DASTM, Schedule F should be prepared and translated into U.S. dollars according to Regulations Section 1.985-3(d), rather than U.S. GAAP.

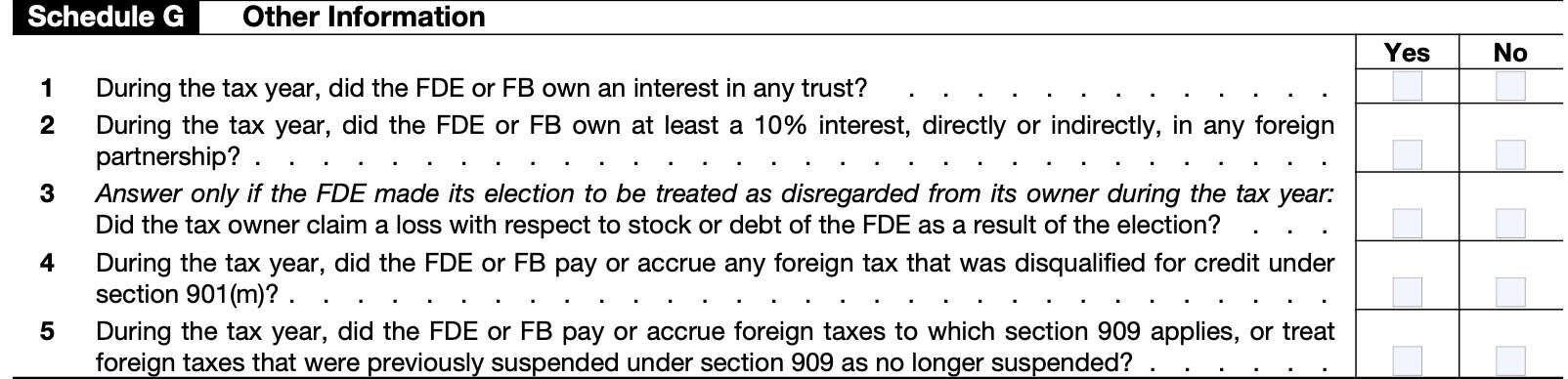

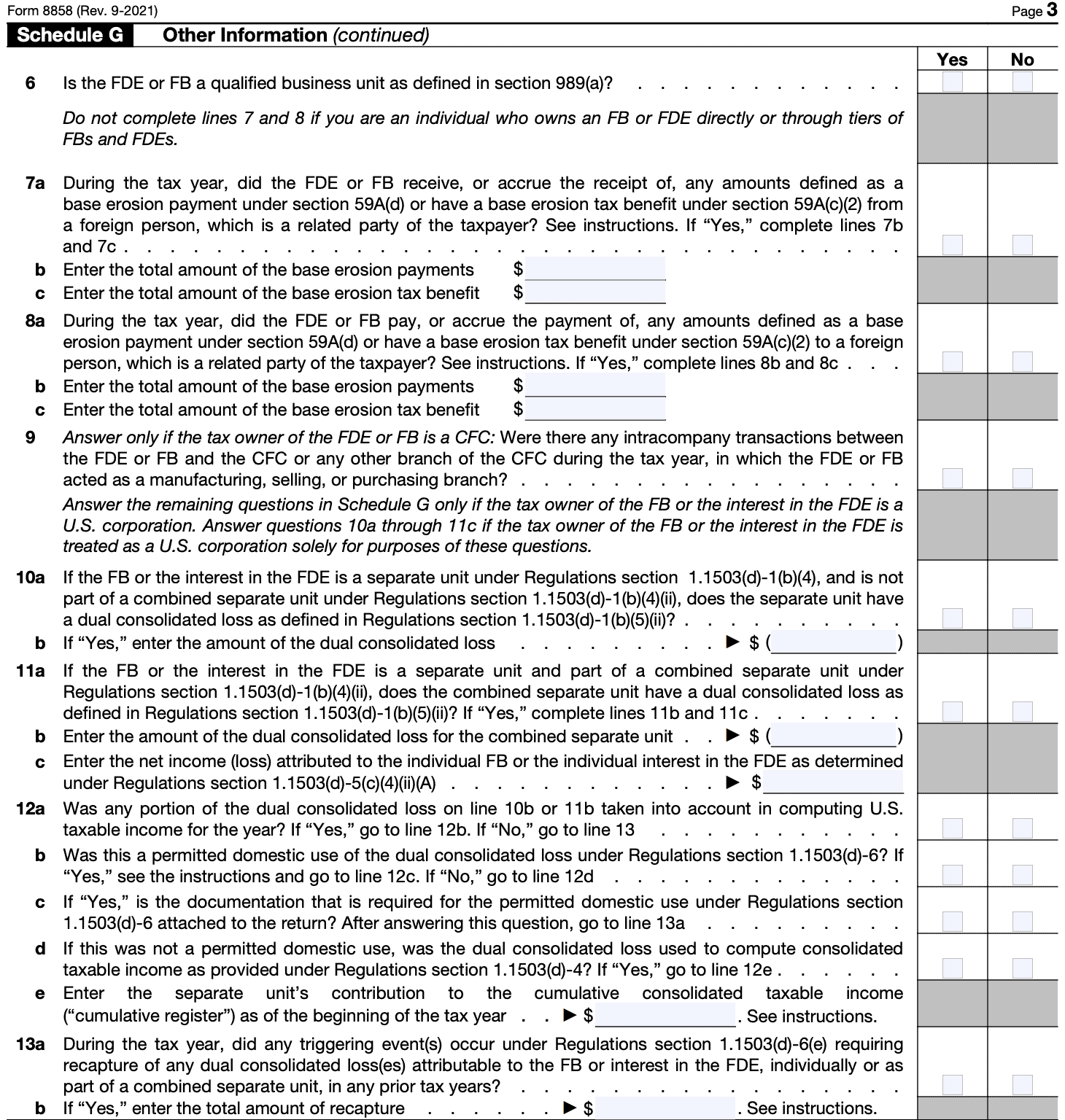

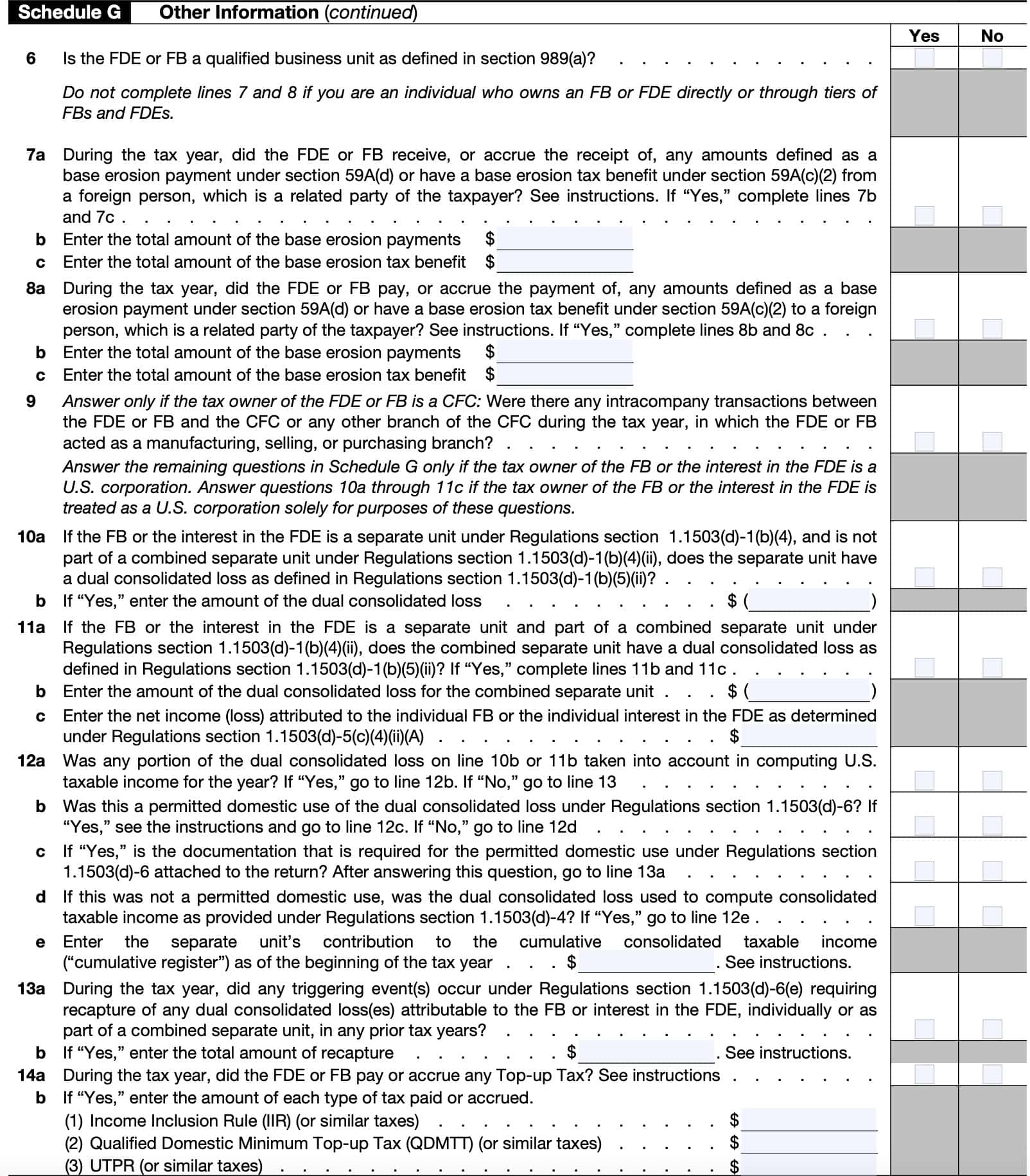

Schedule G: Other Information

Report other information in Schedule G, as applicable. Most fields are self-explanatory with the following exceptions:

Line 3

If the tax owner of the FDE is claiming a Section 165 loss with respect to worthless stock or with respect to certain tax obligations, see Regulations Section 1.6011-4. This section contains information about a disclosure statement that must be attached to Form 8858 in certain situations.

Line 6

Check “Yes” if the FB or FDE is a QBU as defined in Section 989(a). See Schedule C-1 if the QBU is subject to Section 987.

Line 7/Line 8

Do not complete lines 7 and 8 if you are an individual who owns an FB or FDE directly or through tiers of FBs and FDEs. See IRC Section 59A for more information about base erosion payments.

Line 9

Do not answer unless the tax owner of the FDE or FB is a CFC.

Lines 10-13

Complete lines 10 through 14 only if the tax owner of the FB, or the tax owner of the interest in the FDE, is a U.S. corporation (other than a RIC, a REIT, or an S corporation).

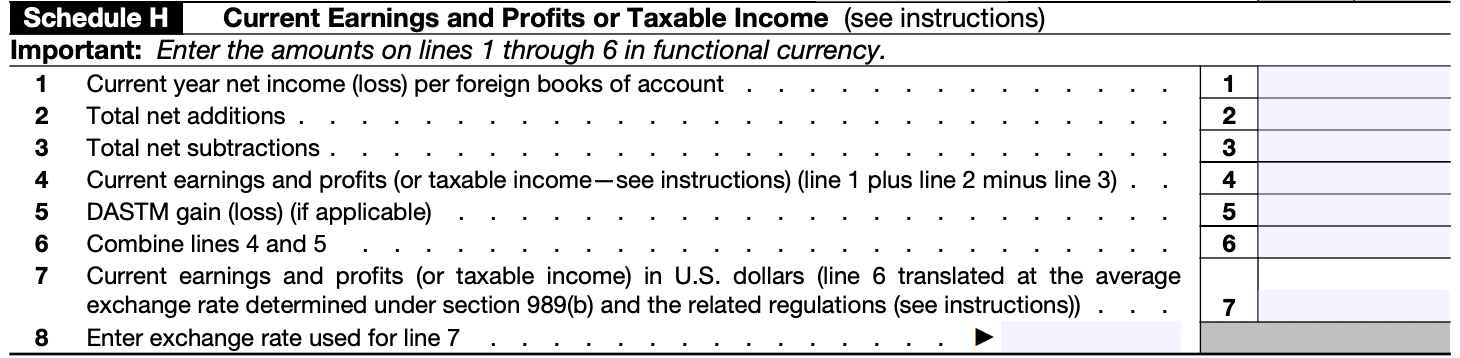

Schedule H: Current Earnings & Profits or Taxable Income

Use Schedule H to report either:

- The FDE’s current E&P or the FB’s income (if the tax owner is a CFC) or

- The FDE’s or FB’s taxable income (if the tax owner is a U.S. person or a CFP)

Generally, enter the amounts on Lines 1 through 6 in functional currency.

Line 2/3

Certain adjustments must be made to the FDE’s or FB’s line 1 net book income or loss to determine its current E&P or taxable income. See the form instructions for more details.

Line 5

DASTM gain or loss, reflecting unrealized exchange gain or loss, only applies if the entity uses DASTM.

Line 7

On Line 7, enter the functional currency amount translated into U.S. dollars at the average exchange rate for the FDE’s or FB’s tax year. If the FDE or FB uses DASTM, enter the same amount entered on Line 6.

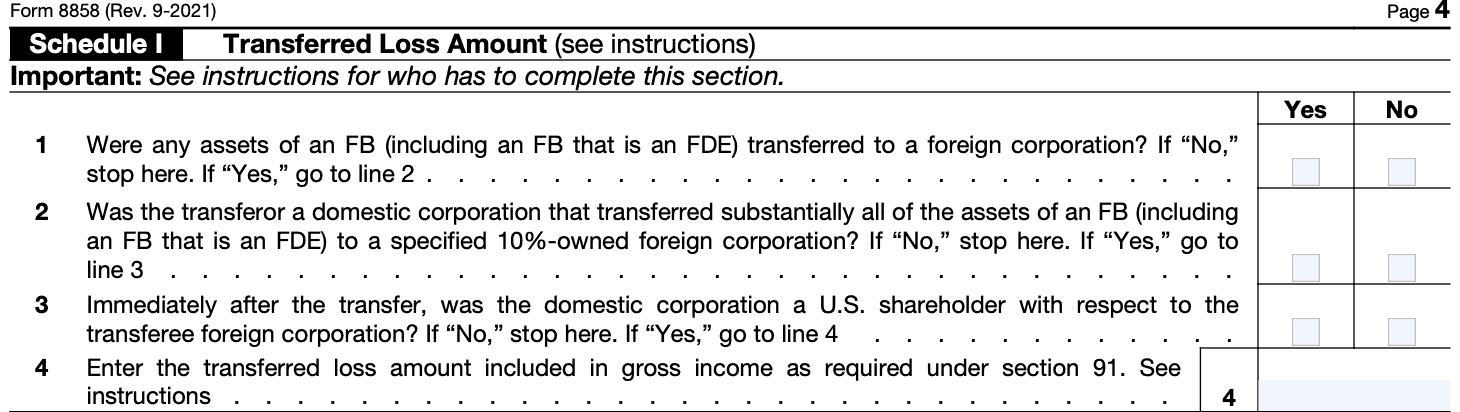

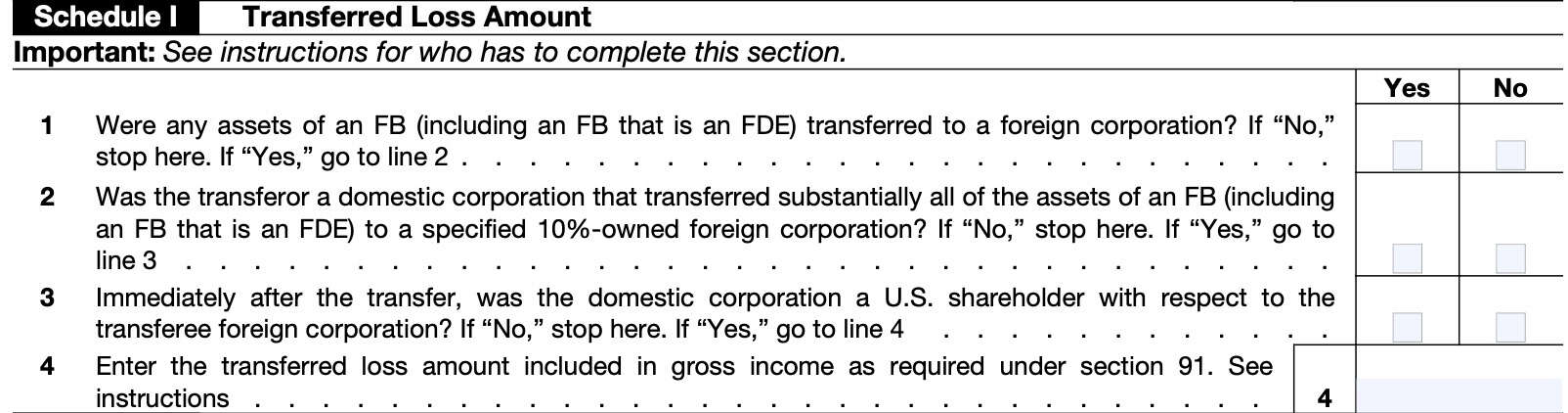

Schedule I: Transferred Loss Amount

Only complete Schedule I if the FB or FDE is owned:

- Directly by a domestic corporation, or

- Indirectly by a domestic corporation through a tiered structure of FDEs or FBs.

Schedule I should not be completed if the FB or FDE is owned by a CFC.

Line 1

Check “Yes” if any assets of an FB (or a branch that is an FDE) were transferred to a foreign corporation during the tax year.

If “Yes,” continue to Line 2. Otherwise, check “No” and do not complete the rest of Schedule I.

Line 2

Check “Yes” if the transferor was a domestic corporation that transferred substantially all of the foreign assets of an FB (or a branch that is an FDE) to a specified 10%-owned foreign corporation. Section 245A(b)(1) defines a specified 10%-owned foreign corporation as any foreign corporation with respect to which any domestic corporation is a U.S. shareholder with respect to such corporation.

If “Yes,” continue to Line 3.

Line 3

Check “Yes” if the transferor was a domestic corporation and immediately after the transfer the domestic corporation was a U.S. shareholder.

If “Yes,” continue to Line 4. Otherwise, stop.

Line 4

Under Section 91, the U.S. transferor must include in gross income an amount equal to the transferred loss amount (TLA), if any, as defined in section 91(b) upon a transfer of substantially all of the assets of an FB (including an FB that is an FDE) to a foreign corporation.

See the form instructions for more detail about Line 4.

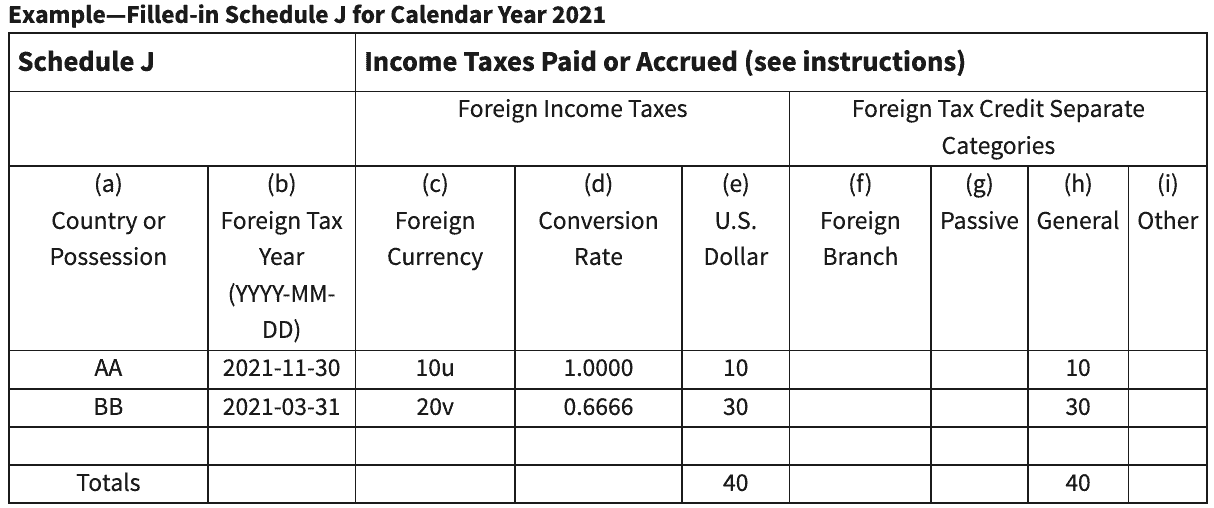

Schedule J: Income Taxes Paid or Accrued

List income, war profits, and excess profits taxes (“income taxes”) paid or accrued to the United States and to each foreign country or U.S. possession for the foreign entity’s foreign tax year(s) that end with or within its U.S. tax year.

Column (a)

For Column (a), use the two-letter IRS country code.

Column (b)

Enter the foreign tax year (YYYY-MM-DD) of the foreign entity’s applicable tax.

Column (f) Through Column (i)

Enter the appropriate in each column, by category. Below is an example of a completed Schedule J from the IRS form instructions.

What is IRS Form 8858?

IRS Form 8858, Information Return of U.S. Persons With Respect to Foreign Disregarded Entities (FDEs) and Foreign Branches (FBs), is an additional federal tax return that certain US taxpayers must file, according to the Internal Revenue Code (IRC). This tax form helps the taxpayer to report required information according to the following tax laws, and associated regulations:

- Section 6011: General requirement of return, statement, or list

- Section 6012: Persons required to make returns of income

- Section 6031: Return of partnership income

- Section 6038: Information reporting with respect to certain foreign corporations and partnerships

Who files IRS Form 8858?

The IRS requires the following U.S. persons that are tax owners of FDEs, operate an FB, or that own certain interests in tax owners of FDEs or FBs to file Form 8858 and Schedule M (Form 8858):

A U.S. person that is a tax owner of an FDE or operates an FB at any time during the U.S. person’s tax year or annual accounting period.

In this situation, the taxpayer will complete the entire Form 8858, including Schedule M, Transactions Between Foreign Disregarded Entity (FDE) or Foreign Branch (FB) and the Filer or Other Related Entities. Schedule M is a separate tax form.

A U.S. person that directly (or indirectly through a tier of FDEs or partnerships) is a tax owner of an FDE or operates an FB.

The taxpayer must complete the entire Form 8858, including Schedule M.

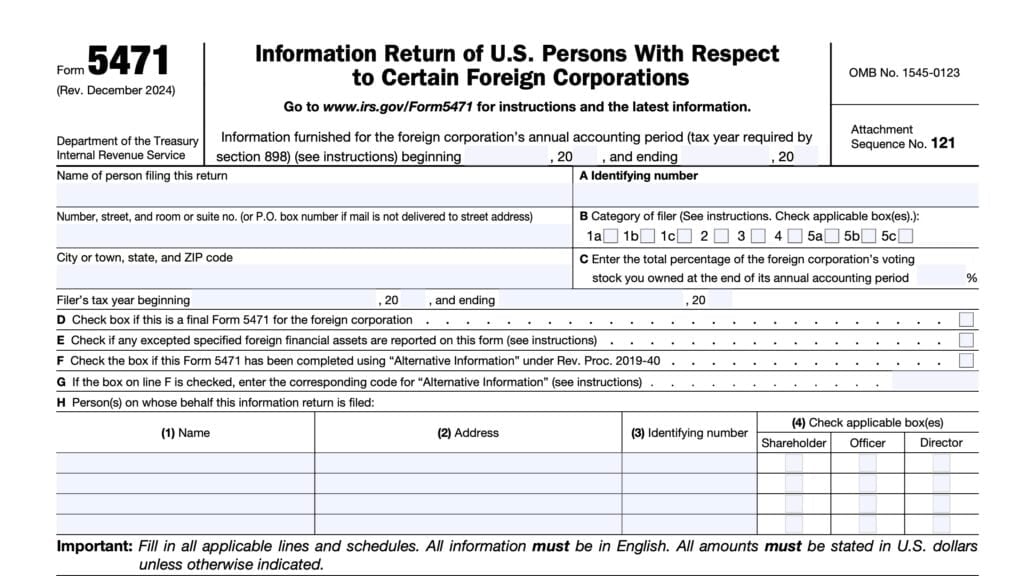

Certain U.S. persons that are required to file IRS Form 5471

These taxpayers might be required to file IRS Form 5471 with respect to a controlled foreign corporation (CFC) that is a tax owner of an FDE or operates an FB at any time during the CFC’s annual accounting period.

Category 4 filers of Form 5471 will need to complete the entire Form 8858 and Schedule M (Form 8858).

Category 5 filers of Form 5471 only need to complete the identifying information on Page 1 of Form 8858 and Schedules G, H, and J. They do not need to complete the separate Schedule M.

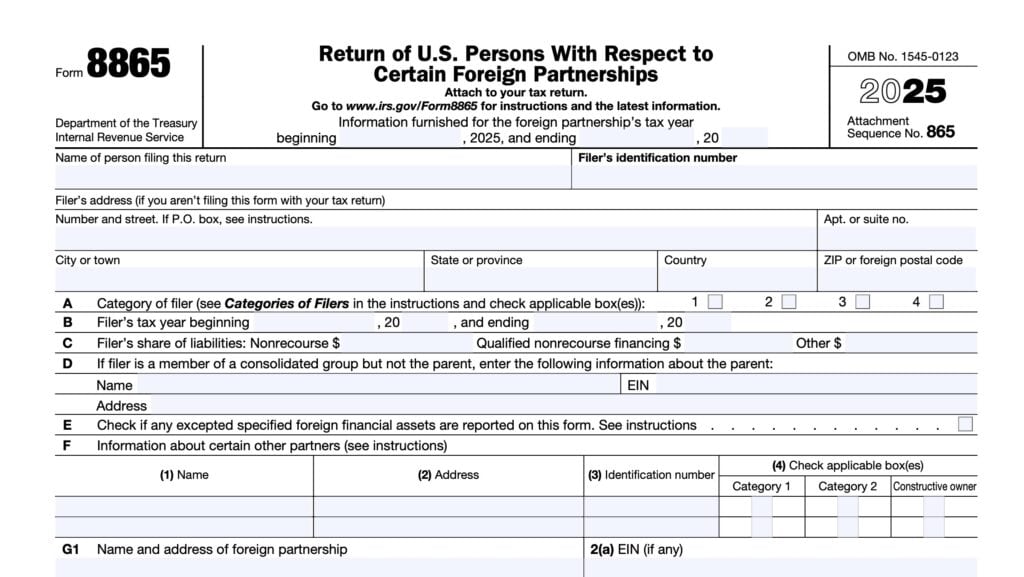

Certain U.S. persons that must file Form 8865 with respect to a controlled foreign partnership (CFP).

This applies to U.S. taxpayers that are tax owners of an FDE or operate an FB at any time during the CFP’s annual accounting period.

If the U.S. person required to file by operation of this rule is a U.S. individual:

the U.S. person is not required to complete lines 10 through 13 of Schedule G.

If the U.S. person is not an individual:

The U.S. person must report its distributive share of the items on lines 10 through 13 of Schedule G.

Category 1 filers of Form 8865:

Complete the entire Form 8858 and the separate Schedule M (Form 8858).

Category 2 filers of Form 8865:

Complete only the identifying information on page 1 of Form 8858 (for example, everything above Schedule C) and Schedules G, H, J, and the separate Schedule M (Form 8858).

You are not required to complete Form 8858 if there is a Category 1 filer of Form 8865 that completes the entire Form 8858 and separate Schedule M (Form 8858) with respect to the FDE or FB.

A U.S. partnership that directly (or indirectly through a tier of FDEs or partnerships) is a tax owner of an FDE or operates an FB.

Complete lines 10 and 11 of Schedule G. Do this as if the U.S. partnership filing the Form 8858 were a U.S. corporation.

A U.S. partnership is not required to complete lines 10 and 11 of Schedule G if all partners are:

- Individuals

- Regulated investment companies (RICs)

- Real estate investment trusts (REITs), and/or

- S corporations.

A U.S. corporation (other than a RIC, a REIT, or an S corporation) that is a partner in a U.S. partnership.

In situations where the corporation must Form 8858 because the U.S. partnership is the tax owner of an FDE or an FB.

What happens if I don’t file IRS Form 8858?

There are significant civil and criminal penalties for taxpayers who are required to, but do not file IRS Form 8858.

Failure to file penalty

A $10,000 penalty is imposed for each annual accounting period of each CFC or CFP for failure to furnish the required information within the time prescribed.

After 90 days, the IRS will impose an additional $10,000 penalty (per CFC or CFP) for each 30-day period, or fraction after the 90-day period has expired.

The additional penalty is limited to a maximum of $50,000 for each failure.

Reduction of taxes available for foreign tax credit

Any person who fails to file or report all of the information required within the time prescribed will be subject to a reduction of 10% of the foreign taxes available for credit under Sections 901 and 960.

After 90 days, the IRS will impose an additional 5% reduction for each 3-month period, or fraction thereof, during which the failure continues after the 90-day period has expired.

According to IRC Section 6038(c)(2), the limit is the greater of:

- $10,000, or

- The income of the foreign business entity for its annual accounting period the failure occurred in

Criminal penalties

The federal government may press criminal charges under the Internal Revenue Code. Potential penalties under the following IRC Sections may apply for failure to file the information required by Section 6038:

- IRC Section 7203: Willful failure to file

- IRC Section 7206: Fraud and false statements

- IRC Section 7207: Fraudulent returns, statements, or other documents

Video walkthrough

Watch this instructional video to learn how to complete Form 8858 and its accompanying schedules, step by step.

Frequently asked questions

Form 8858 is due when your income tax return or information return is due, including extensions.

According to the IRS, a foreign disregarded entity (FDE) is an entity that is not created in the United States, and is disregarded as an entity separate from its owner for U.S. income tax purposes under Treasury Regulations Sections 301.7701-2 and 301.7701-3.

According to Treasury Regulations Section 1.367(a)-6T(g), a foreign branch (FB) is an integral business operation carried on by a U.S. person outside the United States. For purposes of filing IRS Form 8858, an FB also includes a foreign qualified business unit (QBU), as defined in Treasury Regulations Section 1.989(a)-1(b)(2)(ii)).

Where can I find IRS Form 8858?

You may find this tax form, as well as the separate Schedule M on the IRS website. For your convenience, we’ve attached both forms to this article.