IRS Form 8275 Instructions

Many taxpayers may have tax positions disallowed by the IRS simply because there is not enough information in the tax return to support it. These situations may result in unnecessary accuracy-related tax penalties. However, you can avoid these situations by filing IRS Form 8275 with your income tax return.

In this article, we’ll walk you through everything you need to know about IRS Form 8275, including:

- How to complete IRS Form 8275

- What this form is used for

- Who should file IRS Form 8275

Let’s start with a step by step overview of the tax form itself.

Table of contents

How do I complete IRS Form 8275?

There are four parts to this two-page tax form:

- Part I: General Information

- Part II: Detailed Explanation

- Part III: Information About Pass-Through Entity

- Part IV: Explanations

Before we start with Part I, let’s look at the information fields at the very top of the form.

Top of Form

The top of IRS Form 8275 contains some information fields you must complete before starting Part I.

First, enter the taxpayer name and identifying number as shown on your income tax return. The identifying number can be a Social Security number (SSN) or individual taxpayer identification number (ITIN).

Following the taxpayer information, you must enter the following information if you are submitting Form 8275 related to an information return on behalf of a foreign entity:

- Name of foreign entity

- Employer identification number, if applicable

- Reference ID number

- Be sure that the reference ID number you enter on Form 8275 matches the number for the foreign entity on the information return

If you need to report a tax return position for multiple foreign entities, then you must complete a separate IRS Form 8275 for each entity.

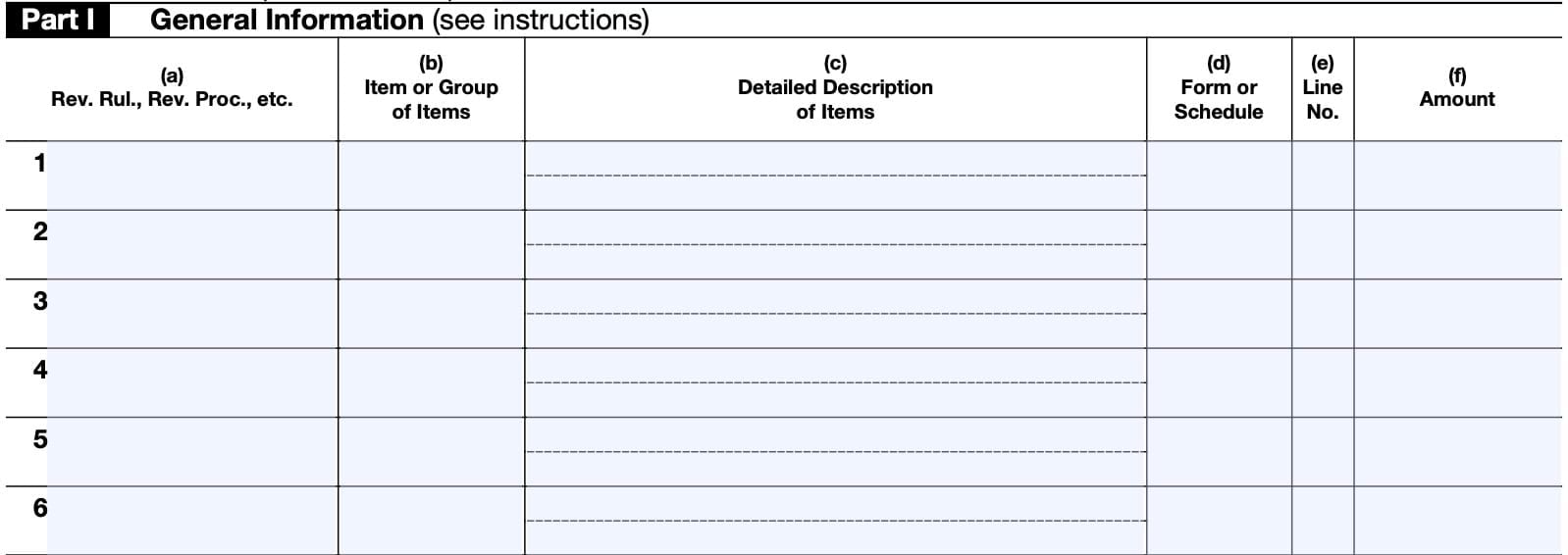

Part I: General Information

As you go through the form, be sure to supply all the information for Parts I, II, and, if applicable, Part III. Your disclosure will be considered adequate if you file IRS Form 8275 and supply the information requested in detail.

In Part I, you will need to disclose the following information for each position that you take:

- Column (a): Revenue Ruling, Revenue Procedure, etc.

- Column (b): Item or group of items

- Column (c): Detailed description

- Column (d): Form or Schedule

- Column (e): Line number

- Column (f): Amount

Let’s take a closer look at each one in detail.

Column (a): Rev. Rul., Rev. Proc., etc.

If you are disclosing a position contrary to a rule, such as a statutory provision or IRS revenue ruling, you must identify the rule in Column (a).

Column (b): Item or Group of Items

In column (b), identify the item by name.

If you disclose any item from a pass-through entity, you must identify the item as coming from that pass-through entity. If you disclose items from two or more pass-through entities, you must complete a separate Form 8275 for each entity.

Column (c): Detailed Description of Items

Enter a complete description of the item or items that you are disclosing.

For example, if you reported entertainment expenses in column (b), use column (c) to list additional detail about those expenses, such as:

- Theater tickets

- Catering expenses

- Banquet hall rental

If you claim the same tax treatment for a group of similar items in the same tax year, you need to enter a description identifying the group of items you are disclosing rather than a separate description of each item within the group.

Column (d): Form or Schedule

Enter the IRS form or schedule that pertains to the tax position you are assuming for this line item.

Column (e): Line Number

Enter the corresponding line number for the form or schedule that you listed in Column (d), above.

Column (f): Amount

In Column (f), enter the dollar amount related to the taxpayer’s position you are taking on the disclosure form.

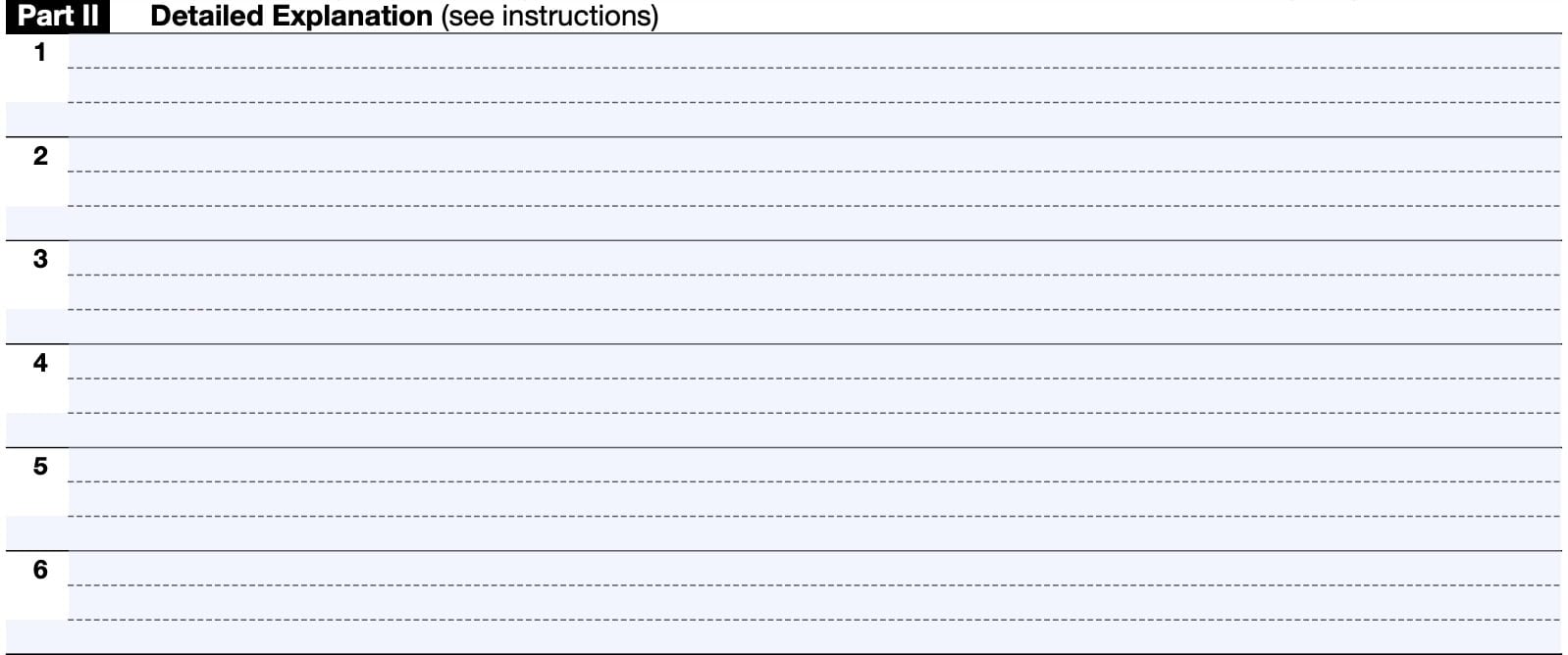

Part II: Detailed Explanation

In Part II, provide a detailed explanation for each position that you disclosed in Part I.

Your disclosure statement must include a description of the relevant facts affecting the tax treatment of the item. To satisfy this requirement, you must include information that can reasonably be expected to apprise the IRS of the following:

- Identity of the item

- Amount involved

- Nature of the controversy or possible controversy

- This can include a description of the legal issues presented by the relevant facts

Your disclosure will not be considered accurate unless the information described above is provided using Form 8275. If Form 8275 is not completed and attached to the return, the disclosure will not be considered valid even if the pertinent information is provided using another method, such as a different form or an attached letter.

For example, your disclosure will not be considered adequate if you attach a copy of an acquisition agreement to your tax return to disclose the issues involved in determining the basis of certain acquired assets without a properly completed Form 8275 accompanying the attached agreement.

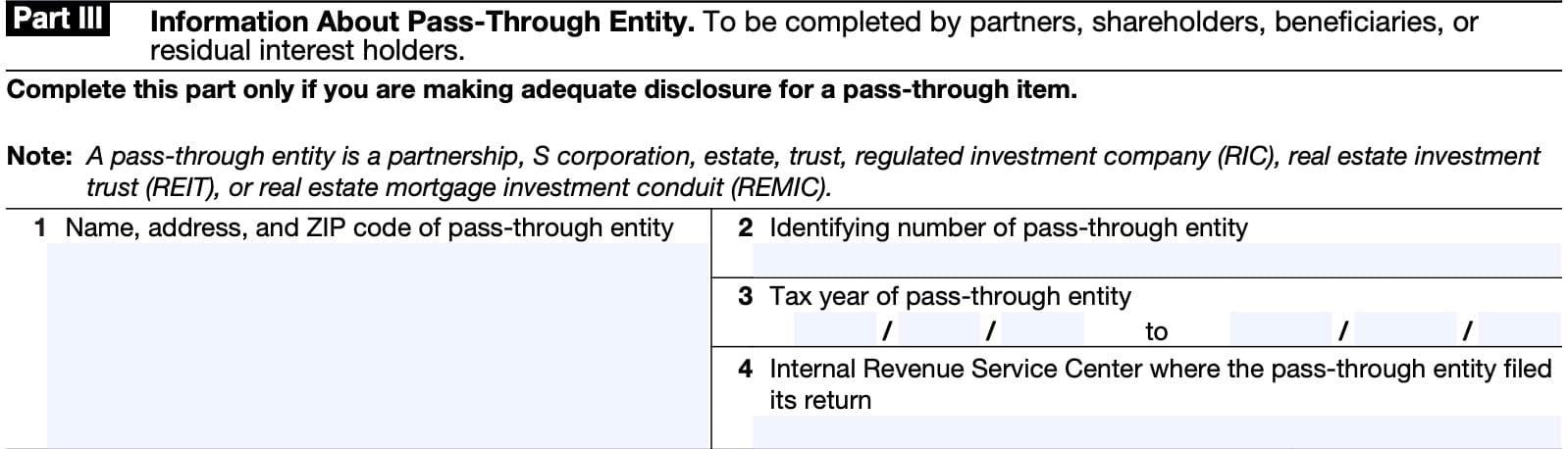

Part III: Information About Pass-Through Entity

Part III applies to the following:

- Partners

- Shareholders

- Beneficiaries

- Residual interest holders

Only complete Part III if you are making adequate disclosure for a pass-through item.

Line 1

Enter the name, address, and ZIP code of the pass-through entity.

Line 2: Identifying number of passthrough entity

Enter the identifying number of the pass-through entity. This usually is the entity’s employer identification number (EIN).

Line 3: Tax year

In Line 3, enter the beginning date and the ending date for the pass-through entity’s tax year.

Line 4: IRS Center where the pass-through entity filed its tax return

Enter the IRS center where the pass through entity’s tax return was filed. Contact your pass-through entity if you do not know where its return was filed.

However, for partners and S corporation shareholders, information for Line 4 can be found on the Schedule K-1 that you received from the partnership or S corporation.

If the pass-through entity filed its return electronically using e-file, enter “e-file” on Line 4.

Part IV: Explanations

Use Part IV to provide additional narrative to support your statements in Part I, Part II, or both.

Purpose of IRS Form 8275

IRS Form 8275 is used by taxpayers and tax return preparers to:

- Disclose items or positions not otherwise adequately disclosed on a tax return, to avoid penalties

- Except items or positions taken contrary to a Treasury Regulation

- Avoid portions of the accuracy-related penalty due to:

- Disregard of rules

- Substantial understatement of income tax for non-tax shelter items

- If the return’s position has a reasonable basis

- Provide disclosures related to the following penalties:

- Economic substance penalty

- Tax preparer penalties for tax understatements due to unreasonable positions or disregard of IRS rules

However, there are certain areas of misconduct where a taxpayer cannot avoid accuracy-related tax penalties, even when filing Form 8275.

Situations where IRS Form 8275 will not help avoid penalties

Filing Form 8275 will not prevent an accuracy related tax penalty in the following situations:

- Negligence

- Intentional or reckless disregard of regulations

- Any substantial understatement of income tax on a tax shelter item

- Any substantial or gross valuation misstatement under Internal Revenue Code Chapter 1.

- Includes misstatements attributable to non-arm’s length prices

- Any substantial overstatement of pension liabilities

- Any substantial estate or gift tax valuation understatements

- Any claim of tax benefits from a transaction lacking economic substance or failing to meet the requirements of any similar rule of law.

- Within the meaning of IRC Section 7701(o)

- Any otherwise undisclosed foreign financial asset understatement

- Any inconsistent estate basis

Who should file IRS Form 8275

The following taxpayers file IRS Form 8275 to disclose a position:

- Individuals

- Corporations

- Pass-through entities

- Tax return preparers

If you are disclosing a position taken contrary to a regulation, use IRS Form 8275-R, Regulation Disclosure Statement, instead of IRS Form 8275.

For items attributable to a pass-through entity, disclosure should be made on the tax return of the entity. If the entity does not make the disclosure, the partner (or shareholder, etc.) can make adequate disclosure of these items.

Exceptions to filing requirements

Guidance is published annually in a revenue procedure in the Internal Revenue Bulletin that identifies circumstances when an item reported on a return is considered adequate disclosure for purposes of:

- Substantial understatement aspect of the accuracy-related penalty and

- Avoiding the preparer’s penalty related to understatements due to unreasonable positions

For example, the IRS considers a taxpayer to have met requirements for adequate disclosure of a charitable deduction if you:

- Complete the contributions section of Schedule A

- Supply required information, and

- Attach all required forms according to statute or regulation

Video walkthrough

Watch this instructional video for additional information about avoiding accuracy-related penalties using IRS Form 8275.

Frequently asked questions

Taxpayers and tax return preparers file IRS Form 8275 to disclose items or positions that are not otherwise adequately disclosed on a tax return, to avoid certain penalties. IRS Form 8275 does not cover items or positions taken contrary to a regulation. Taxpayers must use IRS Form 8275-R to disclose items taken contrary to Treasury Regulations.

Yes. IRS Form 8275 can be filed electronically, as long as you file this form with your tax return. However, many tax preparation programs, such as TurboTax, do not support electronic filing for Form 8275.

Where can I find IRS Form 8275?

You can find IRS Form 8275 on the Internal Revenue Service website. For your convenience, we’ve enclosed the latest version of this tax form in this article.

Related tax forms

This tax form is one of the fillable tax forms provided by the Internal Revenue Service, to help taxpayers reduce their tax preparation costs. To see more forms like this, visit our free fillable tax forms page, where you’ll also find articles like this.

Unlike the IRS, our articles contain step by step instructions for each tax form, as well as video walkthroughs. You can also check out all of our videos by subscribing to our YouTube channel!