IRS Form 8869 Instructions

When treating an eligible subsidiary as a qualified subchapter S subsidiary, a parent corporation files IRS Form 8869 with the Internal Revenue Service.

This article will walk you through some of the key points of how this works, including:

- What is IRS Form 8869

- How to complete and file Form 8869

- Frequently asked questions about QSub elections

Let’s start by walking through the tax form itself.

Table of contents

How do I complete IRS Form 8869?

In this section, we’ll walk through this tax form, step by step. There are two parts to this one-page form:

- Part I: Parent S Corporation Making the Election

- Part II: Subsidiary Corporation For Which the Election is Made

Let’s begin with Part I.

Part I: Parent S Corporation Making the Election

Part I contains information about the parent corporation.

Line 1: Parent S Corporation information

In Line 1, enter the following:

- Line 1a: Name of parent corporation

- Line 1b: Address of parent corporation

- Including suite, room, or other unit number, or P.O. Box number, if applicable

- Line 1c: City, state, zip code of parent company

Line 2: Employer identification number

Include the full employer identification number (EIN) of the parent company. This should be the same information on the parent company’s U.S. income tax return.

Line 3: Tax year

This should be the last day of the parent company’s taxable year.

Line 4: Service center where last return was filed

Enter the IRS service center where the parent company filed their most recent tax return.

Line 5: Name and title of officer or legal representative

Enter the name and title of the company’s representative.

Line 6: Telephone number

Enter the telephone number of the company’s representative.

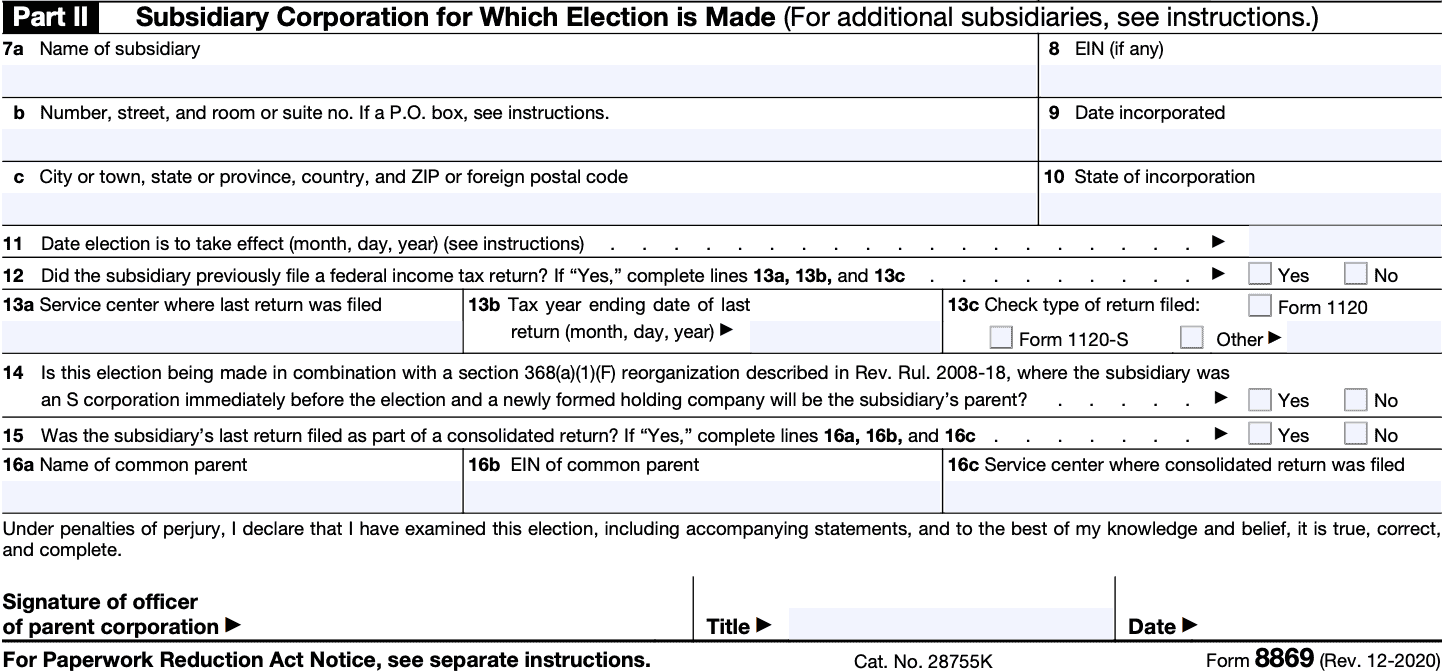

Part II: Subsidiary Corporation for Which Election is Made

This part contains information about the subsidiary company.

Line 7: Subsidiary information

In Line 7, enter the following:

- Line 7a: Name of subsidiary

- Line 7b: Address of subsidiary

- Including suite, room, or other unit number, or P.O. Box number, if applicable

- Line 7c: City, state, zip code of subsidiary

Line 8: Employer identification number (if applicable)

Not all QSub entities have an EIN. If this is the case, enter ‘N/A’ for Line 8.

Line 9: Date of incorporation

Enter the effective date of the subsidiary’s incorporation.

Line 10: State of incorporation

Enter the state in which the QSub was incorporated.

Line 11: Effective date

Enter the effective date of QSub election. To be a valid QSub election, this date cannot be more than:

- 12 months after filing IRS Form 8869, or

- 2 months and 15 days before filing

Line 12: Did the subsidiary previously file a federal income tax return?

Select the appropriate box. If the QSub did not previously file a tax return, proceed to Line 14. If the QSub did file a previous tax return, complete Line 13.

Line 13: Last tax return information

Complete this line by providing the following information:

- Line 13a: Service center where the S corporation’s return was filed

- Line 13b: Ending date of the most recent return.

- Include day, month, and year

- Line 13c: Type of return filed.

- Indicate whether this was IRS Form 1120, IRS Form 1120-S, or another tax form.

Line 14

Was this election made in combination with a reorganization under tax code Section 368(a)(1)(F)? Select the appropriate box.

Line 15

If the subsidiary’s last return was part of a consolidated return, check ‘Yes’ and proceed to Line 16. If not, select ‘No’ and go to the signature field.

Line 16: Common parent information

List the following information about the common parent entity:

- Line 16a: Name of common parent

- Line 16b: Common parent’s EIN

- Line 16c: IRS service center where the common parent filed their most recent tax return

Signature

This field should contain the signature and title of an officer authorized to file the S-corporation’s income tax return. This may include the following positions:

- President

- Vice President

- Treasurer

- Assistant Treasurer

- Chief Accounting Officer

- Other responsible corporate officer, such as tax officer

The responsible officer will sign this form under penalty of perjury.

What is IRS Form 8869?

IRS Form 8869, Qualified Subchapter S Subsidiary Election (QSub election), is the tax form that a parent corporation will file with the IRS to treat one of its eligible subsidiaries as a QSub. The Qsub election results in a deemed liquidation of the subsidiary corporation into the parent.

For federal income tax purposes, all of the following are treated as those of the parent corporation:

- Assets

- Liabilities

- Items of income

- Deductions

- Credits

Because this is a deemed liquidation, there is no requirement to file IRS Form 966, Corporate Dissolution or Liquidation. However, if the subsidiary was a separate corporation prior to the deemed liquidation, the S corporation parent may need to file a last federal income tax return for the QSub.

The IRS does not require final tax returns if the parent corporation makes this election pursuant to a reorganization under Internal Revenue Code Section 368(a)(1)(F). Rev. Rul 2008-18, contains more details about the requirements of Section 368.

Who must file IRS Form 8869?

Filing this form is completely optional for federal tax purposes. A domestic corporation may file such form at any point during the tax year.

However, the requested effective date of the QSub election generally cannot be more than:

- 12 months after the date the election is filed, or

- 2 months and 15 days before the date the election is filed

If, in good faith, the parent company needs extra time, the IRS may accept an election filed more than 2 months and 15 days after the effective date. However, the parent corporation must show reasonable cause by requesting a private letter ruling and paying a user fee in accordance with Revenue Procedure 2021-1.

Relief from the ruling and user fee requirements might be available. Rev. Proc. 2013-30 might have more details on how to request relief.

How do I file IRS Form 8869?

Once the form is complete, the parent company should send the completed form to the service center where the subsidiary filed its most recent return.

However, if the parent S corporation forms a subsidiary, and makes a valid election effective upon formation, then submit Form 8869 to the service center where the parent S corporation’s return was most recently filed.

Video walkthrough

Watch this instructional video to learn more about how to make a QSub election with Form 8869.

Frequently asked questions

IRC Section 1361(b)(3) authorizes a company to report tax-related information on behalf of one or more subsidiaries as part of a consolidated return, as opposed to separate entities.

While the net effect of a QSub election should not have an immediate tax effect, a QSub election may impact create unexpected taxable events if the QSub is eventually sold.

An eligible subsidiary is a domestic corporation, located in the United States, whose stock is 100% owned by an S corporation and is not a domestic international sales corporation (DISC) or former DISC, an insurance company subject to tax under subchapter L of the tax code, or a bank or thrift institution that uses the reserve method of accounting for bad debts under IRC Section 585.

A QSub election is completely voluntary. The parent company may file a QSub election at any time for one or more eligible subsidiaries, so there is no late election. However, this election may generally not be made more than 1 year prior to the effective date of election, or more than 2 months and 15 days after the effective date of election.

No. You must File Form 8869 with the service center where the subsidiary filed its most recent return. If the parent S corporation forms a subsidiary, and makes a valid election effective upon formation, submit Form 8869 to the service center where the parent S corporation filed its most recent return.

Where can I find IRS Form 8869?

You may find this tax form on the IRS website or download an electronic copy below.