IRS Form 8828 Instructions

If you purchased a home with a federal mortgage subsidy, you generally have a nine-year recapture period. If you sell or otherwise dispose of your home before the ninth year, you may have to file IRS Form 8828, Recapture of Federal Mortgage Subsidy, to calculate any federal subsidy recapture tax you might owe on the sale of your home.

In this article, we’ll walk through everything you need to know about IRS Form 8828, including:

- How to complete IRS Form 8828

- Types of federal subsidies that require recapture

- How to file Form 8828

- Other frequently asked questions

Let’s start with a step by step walkthrough of this tax form.

Table of contents

How do I complete IRS Form 8828?

There are two parts to this one-page tax form:

- Part I: Description of Home Subject to Federally Subsidized Debt

- Part II: Computation of Recapture Tax

Let’s start with Part I.

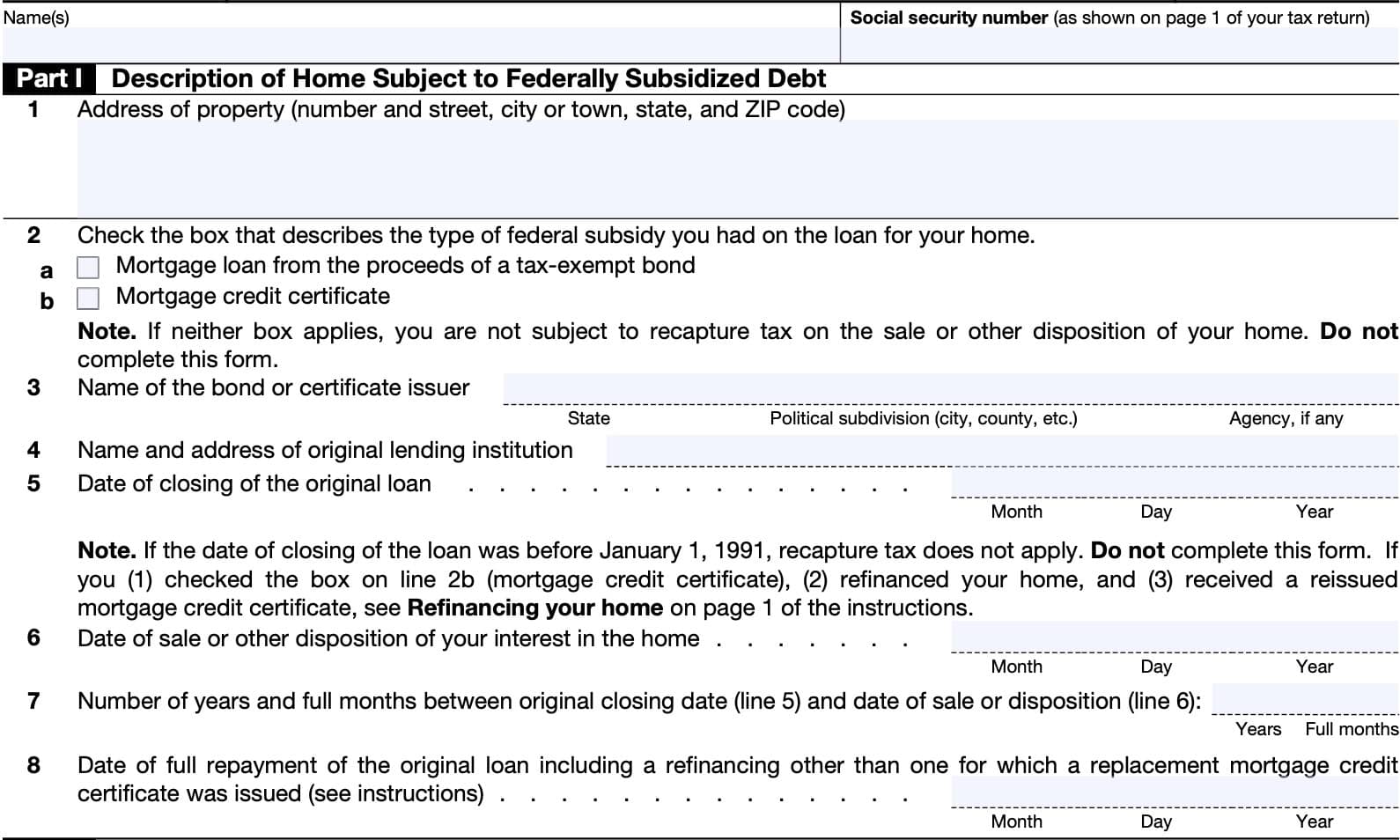

Part I: Description of Home Subject to Federally Subsidized Debt

At the very top of the form, just before Part I begins, enter the taxpayer name and Social Security number as they appear on your income tax return. If you’re using tax preparation software, this is probably done automatically for you.

Line 1: Address of property

In Line 1, enter the property address for the home for which you obtained the original mortgage, not your current address. Enter the following infformation:

- Street number and street name

- City or town

- State

- Zip code

Line 2

Check the appropriate box, based on the nature of the original federally subsidized loan.

Mortgage loan from the proceeds of a tax-exempt bond

This is a mortgage loan that had a lower interest rate than was usually charged because it was funded from a tax-exempt qualified mortgage bond (QMB) issue. This includes any qualified rehabilitation loans.

Mortgage credit certificate

Obtaining a mortgage credit certificate (MCC) through a mortgage credit certificate program can help reduce federal income taxes.

If neither box applies

If your home was financed with a federally subsidized loan, either the bond issuer or the lender should have given you written notification at the time your mortgage was provided.

The notification should state one of the following:

- That your home was financed with a mortgage loan from proceeds of a tax-exempt bond, or

- That you received a mortgage credit certificate with your mortgage loan.

The notification should include information needed to figure your recapture tax and it should advise you to keep it for your records.

If neither box applies, and there is no documentation to the contrary, then you are not subject to recapture tax on the sale of your home. You do not need to complete this tax form.

Line 3: Name of bond or certificate issuer

Enter the following information information about the bond issuer or certificate issuer:

- State

- Municipality or political subdivision

- Agency or organization, if applicable

Line 4: Name and address of original lending institution

Enter the name and address of the bank or loan originator.

Line 5: Date of closing of the original loan

Enter the closing date of the original loan here. Usually, this is the date of settlement on your home.

However, if the loan became federally subsidized debt at a later date, use that date instead.

Line 6: Date of sale or other disposition of your interest in the home

In Line 6, enter the date of sale, or other disposition of your ownership in the home.

If you sold your home, the date of settlement would also be the date of sale. If you did not sell your home, then it might be the date that you deeded the home to another person.

For example, if you gave your home away to a relative, then you would indicate the date that you deeded the property to that person.

Line 7: Number of years and full months between original closing date and date of sale or disposition

In Line 7, enter the number of years and complete months you owned the home prior to the sale of the home.

Line 8: Date of repayment of original loan

Enter the date the original federally subsidized loan was fully repaid. This may be the same as the date of sale or other disposition on Line 6.

A refinanced QMB loan is fully repaid on the date of its refinancing, with conventional financing. Once you have received permanent financing from the proceeds of a QMB, if the home is refinanced with conventional financing, the federal subsidy on your original QMB loan is subject to recapture when you sell or dispose of your home within the 9-year recapture period.

Let’s go to Part II, where we’ll calculate the recapture tax.

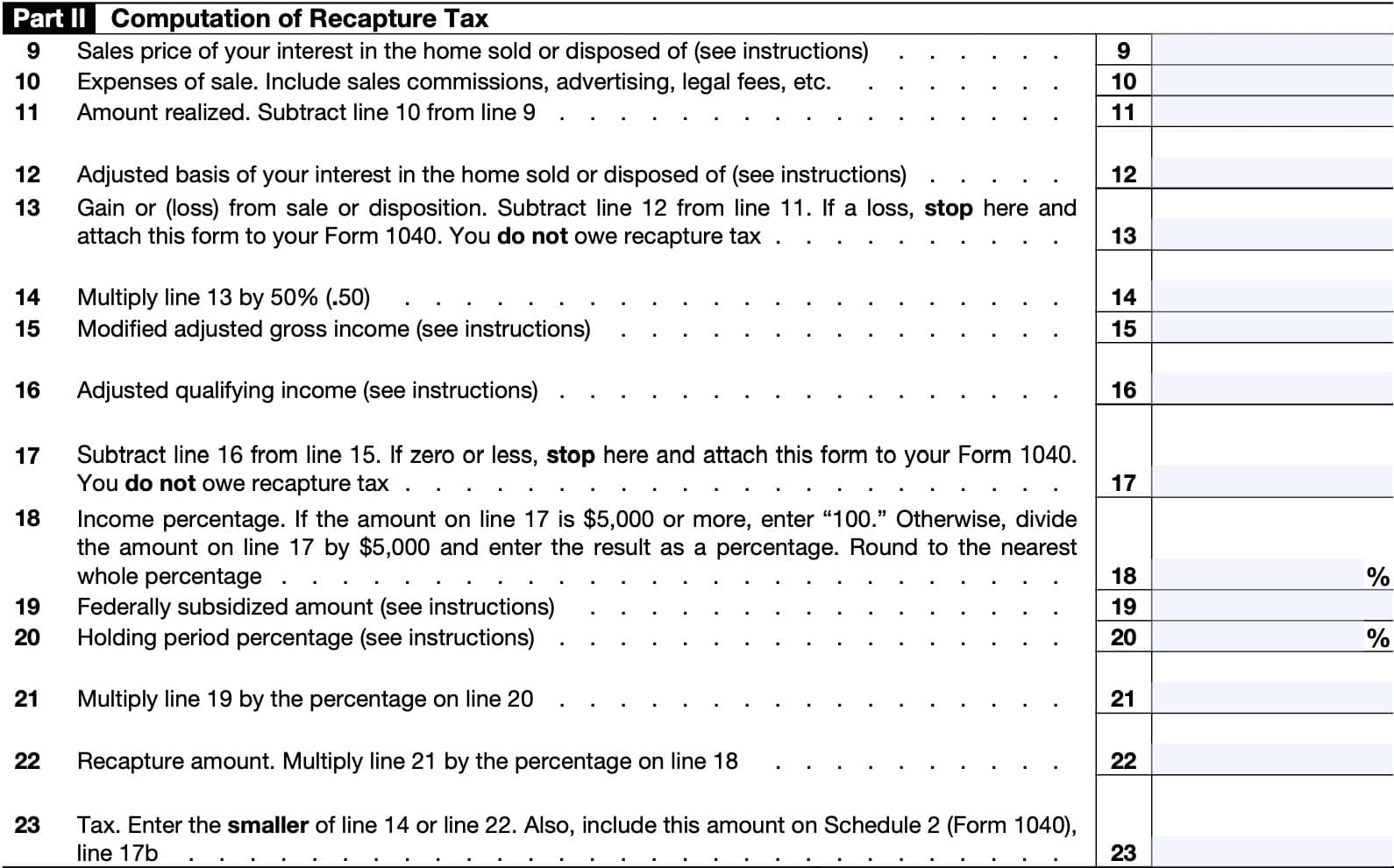

Part II: Computation of Recapture Tax

Line 9: Sales price of your interest in the home sold or disposed of

Enter the sales price of your home. If your home was disposed of other than by sale, the sales price is the fair market value of the home at the time of the disposition.

If there are two or more owners, report only the part of the sales price that represents your real property interests.

Line 10: Expenses of sale

Enter sales related expenses you incurred in selling your home. This might include the following expenses:

- Sales commissions

- Advertising costs

- Legal fees

- Closing fees

- Contingency-based repairs

Line 11: Amount realized

Subtract Line 10 from Line 9, then enter the result here. This is the net proceeds of the sale.

Line 12: Adjusted basis of your interest in the home sold or disposed of

Generally, the adjusted basis of your interest in the home is your share of the cost of the property plus purchase commissions and improvements, minus depreciation. Do not reduce the adjusted basis for any gain that you did not recognize on the sale of a previous home.

If you received your home, or interest in a home, incident to a divorce, your adjusted basis is generally the same as that of your spouse or former spouse.

IRS Publication 551, Basis of Assets, contains additional information on calculating the adjusted basis of your real property.

Line 13: Gain or loss from sale or disposition

Subtract Line 12 from Line 11, then enter the result here.

If the result is a loss, stop at Line 13 and attach this IRS Form 8828 to your federal tax return. You do not owe recapture tax.

Qualifying Subordinate Mortgage Loans

Enter “QSML” on the dotted line to the left of the Line 13 entry space if you meet the following conditions:

- You sold your home at a gain within the 9-year recapture period, and

- Paid a share of that gain to the QSML governmental lender.

In the amount column for Line 13, enter your share of the gain. Attach a worksheet to your completed Form 8828 to explain how you calculated your share of the gain. Show the date you paid the QSML governmental lender its share of the gain and the amount of that share.

Line 14

Multiply Line 13 by 50% (0.50). Enter the result here.

Line 15: Modified adjusted gross income

Enter your modified adjusted gross income (MAGI) here. For purposes of calculating the recapture tax, follow these steps:

- Start with your adjusted gross income (Line 11) from your IRS Form 1040

- Add tax-exempt interest that you received or accrued for the tax year (Line 2a)

- Subtract any gain included in gross income due to the disposition of your home

For taxpayers who are familiar with IRMAA and its impact on Medicare premiums, the MAGI calculation is very similar.

Line 16: Adjusted qualifying income

If your home was financed with a federally subsidized loan, you should have received notification in writing from the bond issuer or the lender at the time your mortgage was provided.

The notification contains a table which lists adjusted qualifying income figures. Your adjusted qualifying income is found in the contents of that column of the table which corresponds to your family size on the line of the table that corresponds to the number of full and partial years that you held your home.

According to the Internal Revenue Service, your family size is based on the number of family members living with you at the time of the sale or disposition.

Line 17

Subtract Line 16 from Line 15.

If the result is zero or a negative number, stop and attach this form to your income tax return. You do not owe recapture tax.

Line 18: Income percentage

If the amount on Line 17 is $5,000 or more, enter ‘100.’

Otherwise, divide the Line 17 amount by $5,000, then enter the result as a percentage. Round to the nearest whole percentage point.

Line 19: Federally subsidized amount

You should find the federally subsidized amount on the notification you received from the bond issuer or from your lender.

It is equal to 6.25% of the highest amount of the federally subsidized mortgage loan. Enter this figure here.

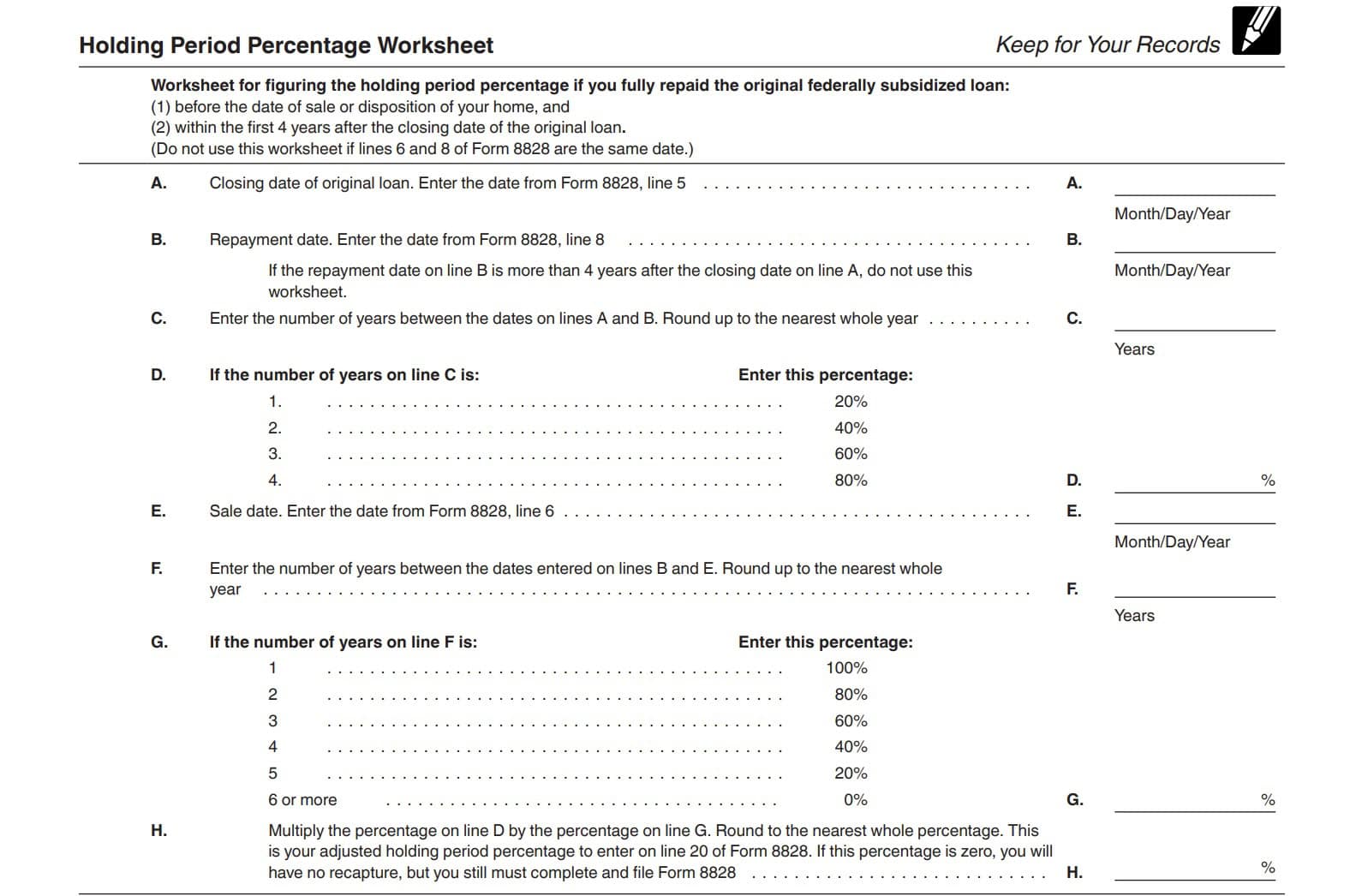

Line 20: Holding period percentage

You can find your holding period percentage on the same line of the table from which you obtained your adjusted qualifying income in Line 16.

However, if you fully repaid the federally subsidized loan within 4 years of the closing date of the loan, and before selling or otherwise disposing of your home, you will need to use the following worksheet to redetermine your holding period percentage.

Line 21

Multiply the federally subsidized amount on Line 19 by the holding period percentage amount in Line 20.

Line 22: Recapture amount

Multiply Line 21 by the income percentage on Line 18.

Line 23: Tax

Enter the smaller of:

Also enter this recapture tax amount on Line 17b of IRS Schedule 2.

Video walkthrough

Below is a walkthrough of IRS Form 8828. For more video walkthroughs on different IRS forms, subscribe to our YouTube channel!

Frequently asked questions

IRS Form 8828 is the tax form that taxpayers file to calculate any federal subsidy recapture they might owe on the sale or disposition of a house they purchased with a federal mortgage subsidy before the end of the nine-year recapture period.

Attach your completed Form 8828 with your individual tax return on or before your tax return’s due date, including extensions.

The transfer of your interest in the home to a former spouse does not result in recapture tax to either person if the transfer is incident to a divorce, and if no gain or loss was included in or deducted from income on your income tax return.

Based upon the formulas contained in IRS Form 8828, the maximum tax you should expect to pay for federal subsidy recapture on a home you sold before the recapture period expired is 50% of the capital gain from the sale of the property

Where can I find IRS Form 8828?

Related tax articles

This tax form is one of the fillable tax forms provided by the Internal Revenue Service, to help taxpayers reduce their tax preparation costs. To see more forms like this, visit our free fillable tax forms page, where you’ll also find articles like this.

Unlike the IRS, our articles contain step by step instructions for each tax form, as well as video walkthroughs. You can also check out all of our videos by subscribing to our YouTube channel!

Hi there,

Regarding recapture tax..If the form I received from IHCDA stated 6.25% is approx $14,000 of my original loan amount, would I have to pay more than that $14000 if the gain is more than that? Or would $14,000 be the worst case scenario?

I’m planning to sell this year and have resided in the home 5 years effective Oct 2024. Thank you so much for any wisdom you may provide, I greatly appreciate it!

The $14,000 should be the most recapture that you’d be responsible for. If you’ve owned and lived in the home for 2 of the past 5 years, then you should be able to exclude up to $250,000 ($500K for married couples filing jointly) from capital gains. Any capital gains beyond that would be your tax responsibility.