IRS Form 8886 Instructions

The Internal Revenue Service defines certain transactions to be reportable for federal income tax purposes. Taxpayers who participate in reportable transactions must report them on IRS Form 8886, Reportable Transaction Disclosure Statement, when they file their income tax return.

In this article, we’ll walk what you need to know about IRS Form 8886, including:

- How to complete & file IRS Form 8886

- Types of reportable transactions

- Frequently asked questions

Let’s start by going through IRS Form 8886, step by step.

Table of contents

How do I complete IRS Form 8886?

Let’s start at the top of this two-page tax form.

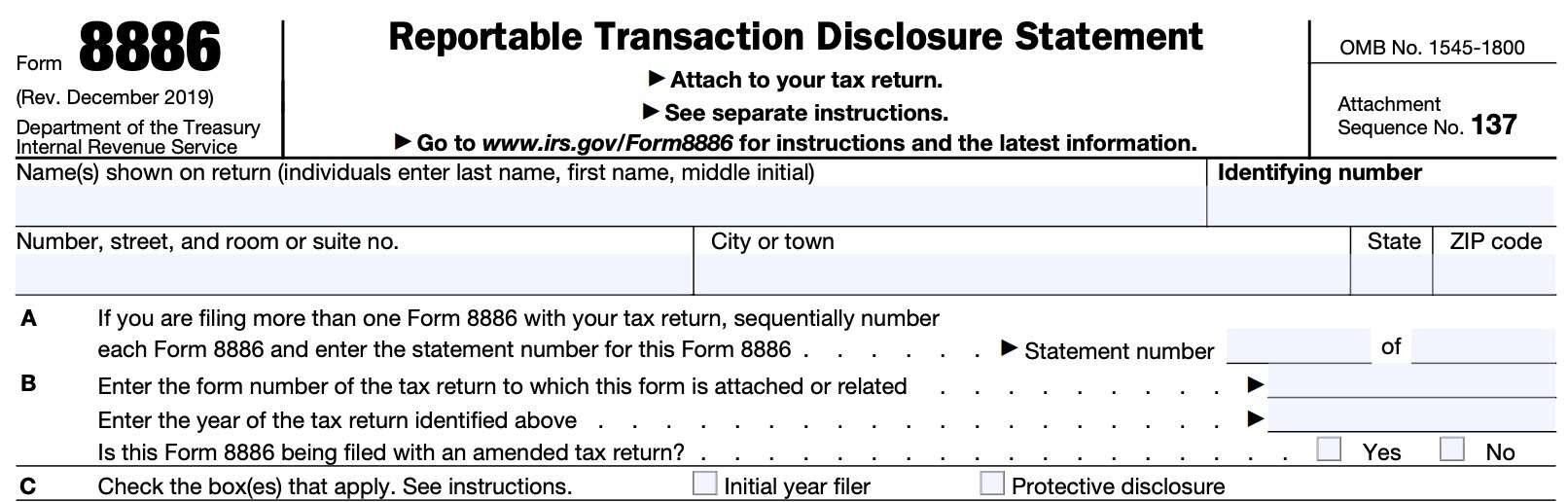

Top of form

At the very top of Form 8886, enter the taxpayer’s name and identifying number, as shown on the income tax return. For individuals, enter your name in the following order:

- Last name

- First name

- Middle initial

The identifying number can be a Social Security number (SSN) or individual taxpayer identification number (ITIN). For non-individuals, such as a pass-through entity, corporation, or tax-exempt entity, this can be an employer identification number (EIN).

Below the name and identifying number, enter the address as it appears on the federal tax return. Include the following:

- Street number and street name

- City or town

- State

- Zip code

Line A

If you file more than one IRS Form 8886 with your income tax return, you must number each of these forms in order, then enter the statement number for this specific form.

For example, “Statement number 1 of 3.”

Line B

In Line B, you’ll need to enter the following information:

- IRS Form number of the attached tax return

- Tax year being reported

- Whether you are filing IRS Form 8886 with an amended return

For a fiscal year tax return, enter the date the fiscal year ends using the MM/DD/YYYY format. For example, you would use “06/30/2021” to report a fiscal tax year that ends on that date.

Line C

For Line C, check the box or boxes that apply to your tax situation.

Initial year filer

If this is the first time that you are using Form 8886 to disclose this transaction, check this box. You’ll need to file a duplicate copy of the disclosure statement with the IRS Office of Tax Shelter Analysis (OTSA).

File by mail

You may mail your completed disclosure statement to the OTSA at this address:

Internal Revenue Service

OTSA Mail Stop 4915

1973 Rulon White Blvd.

Ogden, UT 84201

File by fax

You may also fax the exact copy to 844-253-2553.

Protective disclosure

You may indicate that you are filing on a protective basis by checking this box, under the option provided in Treasury Regulations Section 1.6011-4(f). Generally, the IRS will not treat a Form 8886 filed on a protective basis any differently from other Forms 8886.

An incomplete form containing a statement that information will be provided on request is not a complete disclosure statement. For a protective disclosure to be effective, you must properly complete and file IRS Form 8886 and provide all required information.

Let’s move on to Line 1.

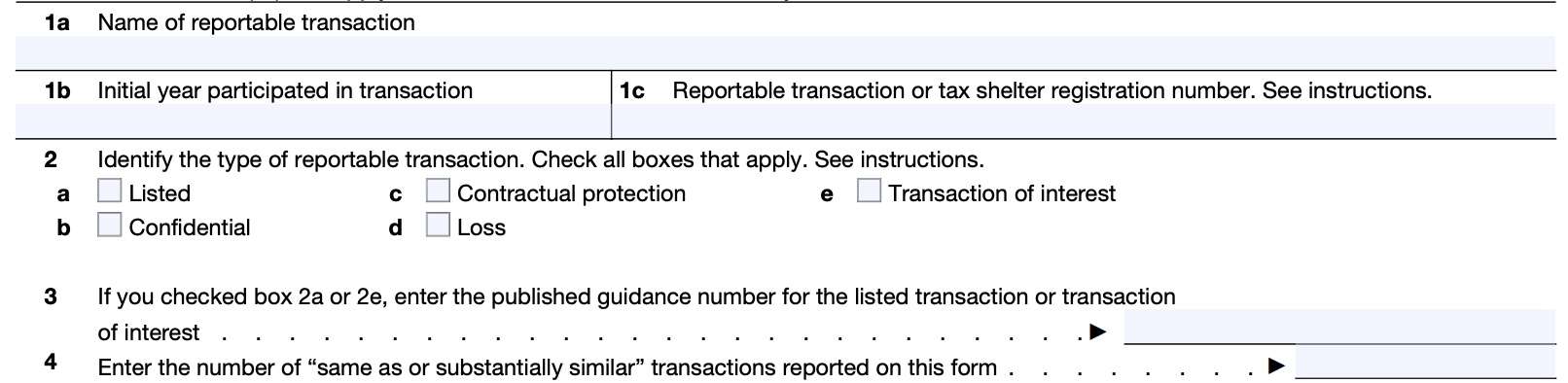

Line 1

Line 1a: Name of reportable transaction

In Line 1a, enter the name of the reportable transaction. If no name exists, then provide a brief identifying description of this particular transaction that might distinguish it from other reportable transactions.

If you are reporting multiple transactions, and each transaction has a different name, enter all names in the space provided. For more space, write “See Additional List” in the space, then attach a list containing your additional transactions.

Line 1b: Initial year

Enter the first year that you participated in this transaction in year format (YYYY). If you are reporting for more than one transaction, enter all initial years in the space provided. If additional space is needed, write “See Additional List” and attach a list.

This may not be the same as the year for which you are disclosing a reportable transaction.

Line 1c: Reportable transaction or tax shelter registration number

Enter the 9-digit and/or 11-digit number that was provided to you. This number may be referred to as a registration number or reportable transaction number and may begin with the letters “MA.”

Reportable transactions can have more than one number. If you have more than one number for this transaction, include all numbers in the space provided.

If additional space is needed, write “See Additional List” and attach a list.

Reportable transaction numbers used to be known as tax shelter registration numbers or registration numbers. Reportable transaction numbers are issued to any material adviser who files a disclosure of reportable transactions under Internal Revenue Code Section 6111.

Material advisers are required to provide this number to their list of investors or advisees.

Line 2

In Line 2, check the appropriate type of reportable transaction from the following list:

- a) Listed

- b) Confidential

- c) Contractual protection

- d) Loss

- e) Transaction of interest

Check the box(es) for all categories that apply to the transaction being reported. Let’s look into the types of reportable transactions in more detail.

Listed transaction

The Internal Revenue Service describes a listed transaction as a transaction that is the same as or substantially similar to one of the types of transactions that the IRS has determined to be a tax avoidance transaction.

These transactions are identified by notice, regulation, or other form of published guidance as a listed transaction.

For existing guidance, see Internal Revenue Notice 2009-59, 2009-31 I.R.B. 170. The IRS website continuously posts updates to this list on the IRS website and in future updates of the Internal Revenue Bulletin.

You have participated in a listed transaction if any of the following applies.

- Your federal tax return reflects tax consequences or a tax strategy described in published IRS guidance that lists the specific transaction.

- You know or have reason to know that tax benefits reflected on your tax return are derived directly or indirectly from such tax consequences or tax strategy.

- You are in a type or class of individuals or entities that published guidance treats as participants in a listed transaction.

Confidential transaction

A confidential transaction is a transaction that is offered to you or a related party under conditions of confidentiality as described in either:

- IRC Section 267(b): Relationships

- IRC Section 707(b): Certain sales or exchanges of property with respect to controlled partnerships

A transaction is considered to be offered under conditions of confidentiality if

- The advisor places a limitation on your disclosure of the tax treatment or tax structure of the transaction, and

- The limitation on disclosure protects the confidentiality of the advisor’s tax strategies.

The transaction is treated as confidential even if the conditions of confidentiality are not legally binding on you. Treasury Regulations Section 1.6011-4(b)(3) contains additional information.

A confidential transaction also involves a minimum fee for tax strategy, tax advice, or for transaction implementation. These fees may include payments for services to:

- Analyze the transaction

- Regardless of whether this analysis is related to the tax consequences of the transaction

- Implement the transaction

- Document the transaction

- Prepare tax returns

- To the extent that the return preparation fees are considered unreasonable

For a corporation, partnership or trust in which all owners or beneficiaries are corporations, the minimum fee is $250,000. For all other taxpayers, the minimum fee is $50,000.

You have participated in a confidential transaction if your tax return reflects a tax benefit from the transaction and your disclosure of the tax treatment or tax structure of the transaction is limited as described above.

Contractual protection transaction

A transaction with contractual protection is one for which you or a related party have the right to a full refund or partial refund of fees if all or part of the intended tax consequences from the transaction are not sustained.

Contractual protection also includes a transaction for which fees are contingent on your realization of tax benefits from the transaction.

You have participated in a transaction with contractual protection if your tax return reflects a tax benefit from the transaction and, as described above, you have the right to a full or partial refund of fees or the fees are contingent.

All facts and circumstances relating to the transaction will be considered when determining whether a fee is refundable or contingent. This includes:

- The right to reimbursements of amounts that the parties to the transaction have not designated as fees, or

- Any agreement to provide services without compensation

Loss transaction

A loss transaction is a transaction that results in your claiming a loss under IRC Section 165 if the amount of the Section 165 loss is as follows:

- Individuals

- At least $2 million in any single tax year, or

- $4 million in any combination of tax years, or

- $50,000 in a single tax year if the loss arose from foreign currency transactions described in IRC Section 988(c)(1)

- Corporations (excluding S corporations)

- At least $10 million in any single tax year, or

- $20 million in any combination of tax years

- For partnerships with only corporations (excluding S corporations) as partners (looking through any partners that are also partnerships):

- At least $10 million in any single tax year, or

- $20 million in any combination of tax years

- Whether or not any losses flow through to one or more partners

- For all other partnerships and S corporations

- At least $2 million in any single tax year, or

- $4 million in any combination of tax years,

- Whether or not any losses flow through to one or more partners or shareholders

- For trusts

- At least $2 million in any single tax year, or

- $4 million in any combination of tax years

- $50,000 in a single tax year if the loss arose from foreign currency transactions described in IRC Section 988(c)(1)

Section 165 loss

For purposes of the above threshold amounts, a Section 165 loss is adjusted for any salvage value and for any insurance or other compensation received. However, a section 165 loss does not take into account offsetting gains, other income, or limitations.

The full amount of a loss is taken into account in the year it was sustained. A Section 165 loss does not include any portion of a loss, attributable to a capital loss carryback or carryover from another year, that is treated as a deemed capital loss under IRC Section 1212.

You have participated in a loss transaction if your tax return reflects a Section 165 loss that equals or exceeds the applicable threshold amount.

If you are a partner, shareholder, or beneficiary of a pass-through entity (partnership, S corporation, or trust), you have participated in a loss transaction if your tax return reflects a Section 165 loss allocable to you from the pass-through entity (disregarding netting at the entity level) that equals or exceeds the applicable threshold amount.

For this purpose, a tax return is deemed to reflect the full amount of the Section 165 loss allocable to the taxpayer.

Transaction of interest

A transaction of interest is a transaction that is the same as or substantially similar to one of the types of transactions that the IRS has identified by notice, regulation, or other form of published guidance as a transaction of interest.

It is a transaction that the IRS and Treasury Department believe has a potential for tax avoidance or evasion, but for which there is not sufficient information to determine if the transaction should be identified as a tax avoidance transaction.

You have participated in a transaction of interest if you are one of the types or classes of individuals or entities identified as participants in the transaction in the published guidance describing the transaction of interest.

Line 3

If you checked either of the following boxes, enter the published guidance number for the listed transaction or transaction of interest:

- Line 2a: Listed transaction

- Line 2e: Transaction of interest

For listed transactions, identify the guidance as shown in Internal Revenue Notice 2009-59, or more recent IRS guidance.

Line 4

Enter the number of “same as or substantially similar transactions” reported on IRS Form 8886.

Do not report more than one transaction on this form unless the transactions are the same or substantially similar.

Substantially similar

A transaction is substantially similar to another transaction if it is expected to obtain the same or similar types of tax consequences and is either factually similar or based on the same or similar tax strategy.

Receipt of an opinion regarding the tax consequences of the transaction is not relevant to the determination of whether the transaction is the same as or substantially similar to another transaction.

Treasury Regulations Section 1.6011-4(c)(4) contains examples of substantially similar transactions.

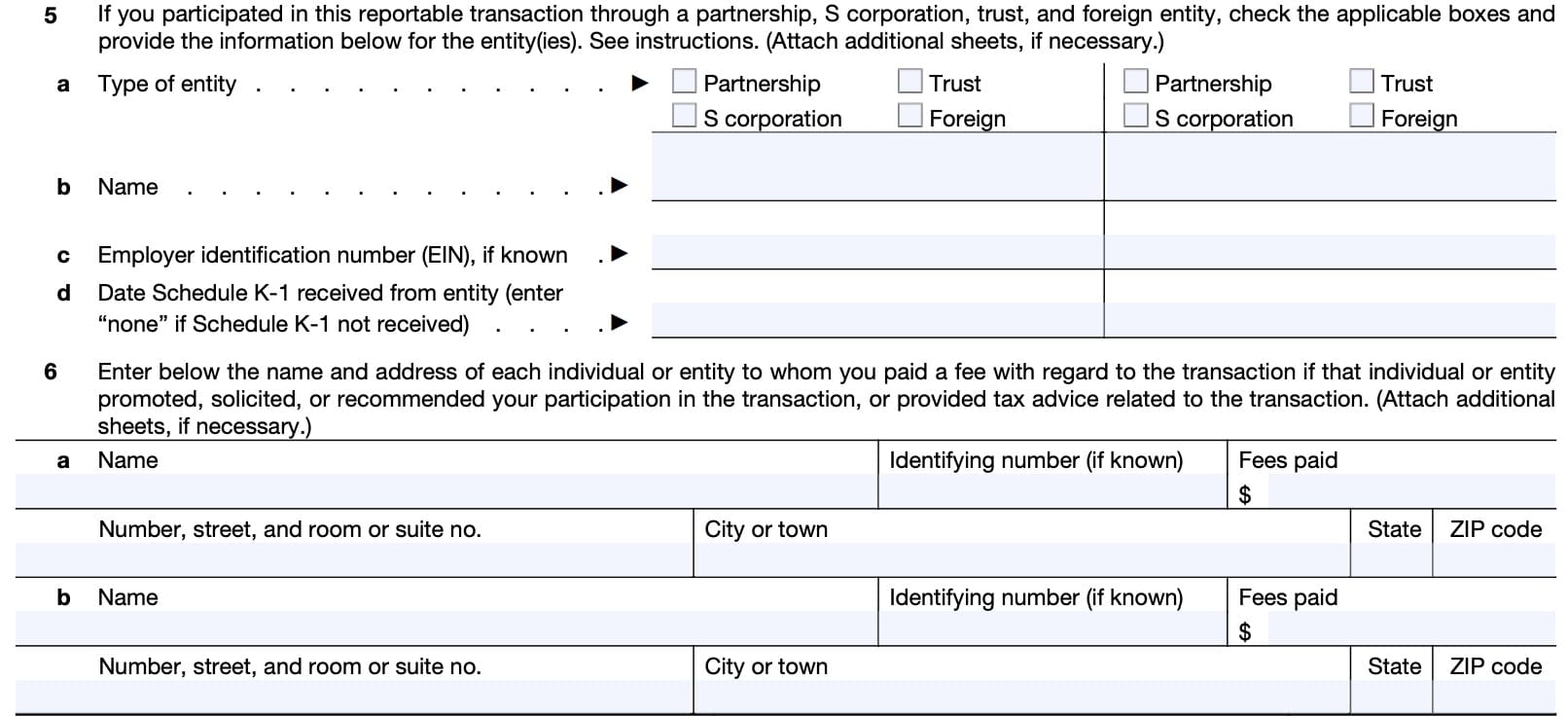

Line 5

If you participated in the transaction through other entities, complete Line 5.

In Line 5a, indicate the type of entity from the following:

- Partnership

- Trust

- S corporation

- Foreign entity

On Line 5b, enter the complete name of the entity.

For Line 5c, enter the entity’s employer identification number, if known.

In Line 5d, enter the date you received the Schedule K-1 from the reporting entity, or ‘none’ if you never received a Schedule K-1.

For reporting more than one entity, use a separate column for each entity. If you are reporting more than two entities, then attach additional sheets.

Line 6

In Line 6, enter the following information for each individual or entity that you paid a fee to:

- Name

- Address

- Social Security number or EIN

- Fees paid

Enter this information for each individual or entity who:

- Promoted, solicited, or recommended that you participate in the reported transaction, or

- Provided tax advice related to the tranasction

When reporting fees, applicable fees include fees for the following:

- Tax strategy

- Tax advice

- Analyzing the transaction

- Transaction implementation

- Documenting the transaction

- Tax return preparation in excess of reasonable preparation fees

You are also treated as paying fees to an advisor if you know or should know that an amount you paid will be paid indirectly to the advisor, such as through a referral fee or fee-sharing arrangement. However, a fee does not include amounts paid to a person, including an advisor, in that person’s capacity as a party to the transaction.

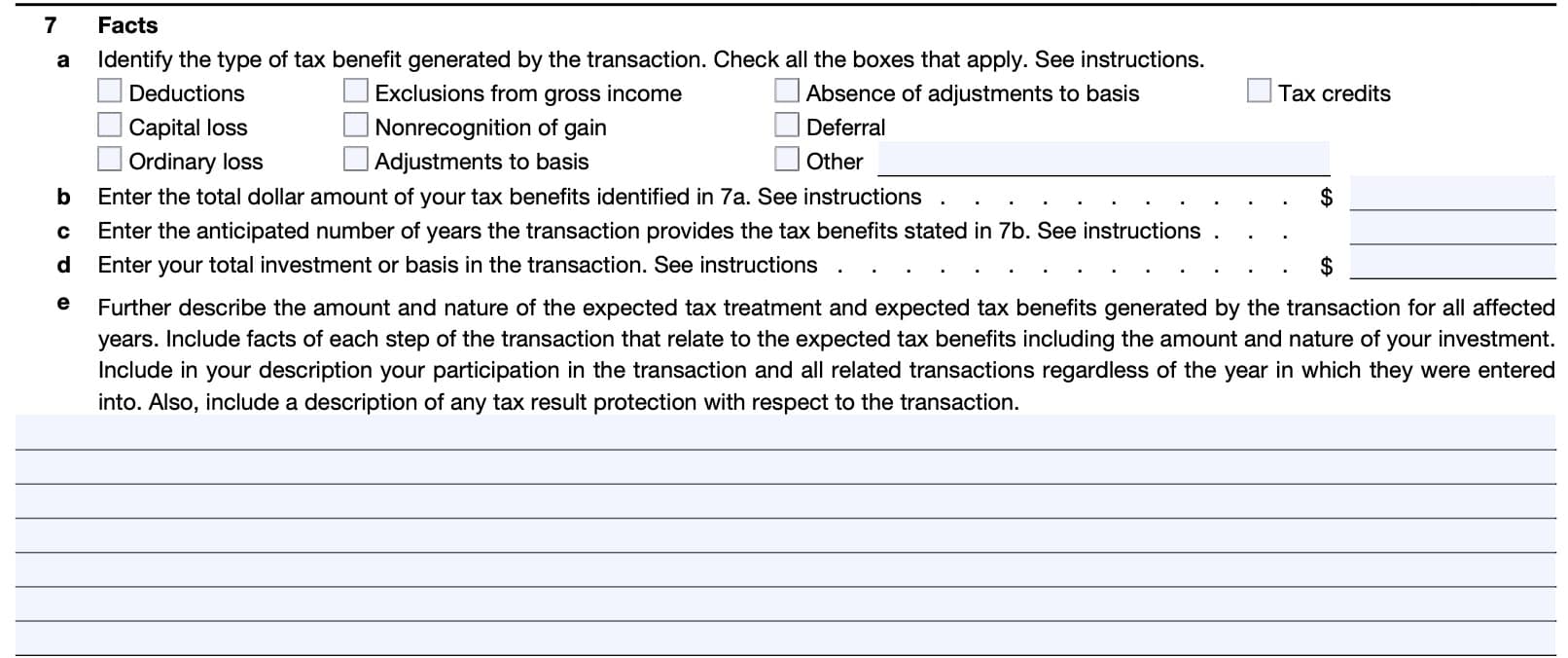

Line 7: Facts

In Line 7, you’ll enter the facts surrounding the transaction.

Line 7a

In Line 7a, indicate the type of potential tax benefits that the transaction generated. If the transaction generated more than one tax benefit, check all applicable boxes.

You may choose from the following tax benefits:

- Tax deductions

- Capital loss

- Ordinary loss

- Exclusions from gross income

- Nonrecognition of gain

- Adjustments to basis

- Absence of adjustments to basis

- Deferral

- Tax Revenue

- Other

Check the “Other” box for tax benefits not specifically identified by a box, then identify the tax benefits in the space provided.

Line 7b

In Line 7b, enter the total dollar amount of the tax benefits you identified in Line 7a. This should include all expected tax benefits over the entire anticipated life of the transaction.

Line 7c

Enter the approximate number of years that you expect the tax benefits to last.

Line 7d

Enter your total investment or basis in the transaction. This is the total amounts you paid related to the transaction that includes:

- Cash

- Fair market value (FMV) of property or services transferred or acquired

- Adjustments to basis

- Valuation of notes, obligations, shares, or other securities

Line 7e

In Line 7e, provide more detail about the expected tax treatment and benefits for all affected years.

Describe each step of the transaction, including all information known to you. Include in your description other parties to the transaction and, if known,

- Assumptions of liabilities or other obligations

- Satisfaction of liabilities or obligations

- Sales of property or interests in property

- Formation and dissolution of entities

- Agreements between or among parties to the transaction

Describe any tax result protection with respect to the transaction. This term includes insurance company and other third-party products commonly described as tax result insurance.

When describing amounts involved, include the following:

- Cash

- FMV of property or services transferred or acquired

- Adjustments to basis

- Valuation of notes, obligations, or other securities

If known, describe, the relationship between the steps of the transaction and how each step relates to why the transaction is reportable. Your description should include the relevance, if known, of any party (including but not limited to participants in the transaction) listed in Line 8.

Describe the economic and business reasons for the transaction and its structure. Describe market or business conditions creating the tax benefit(s) or consequence(s) and the transaction’s financial reporting, if known.

If you checked Box 2b, explain how your disclosure of information concerning the transaction was limited, either by contract or verbal agreement, and the nature and extent of the disclosure limitations.

Treasury Regulations Section 1.6011-4(b)(3) contains more details.

If you checked Box 2c, describe the terms of the contractual protection.

See Treasury Regulations Section 1.6011-4(b)(4) for more details.

If you checked Box 2d, explain how you calculated the basis of the asset for which there was a loss.

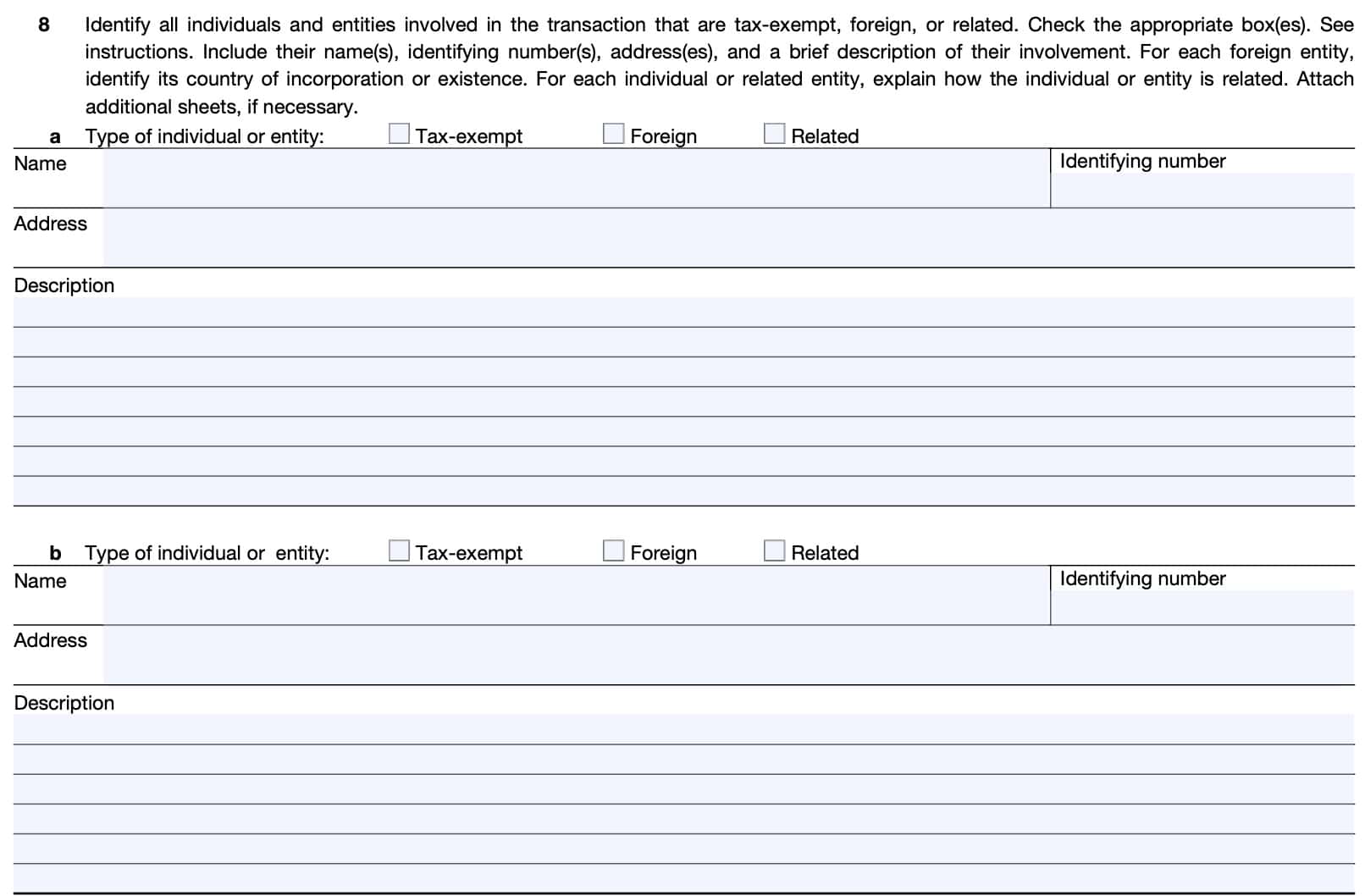

Line 8

In Line 8, you will list all individuals and entities in the transaction. Specifically, list all of the following entities and check the appropriate box(es):

- Tax-exempt entities

- Foreign entities

- Related entities

Attach additional sheets where appropriate. Provide all information, including the name, EIN or SSN, and address, if known.

Include a brief description of each listed individual’s and each entity’s involvement in the transaction.

Provide the country of incorporation or existence for each foreign entity, if known.

Video walkthrough

Watch this instructional video, where we complete Form 8886 step by step, to disclose a reportable transaction.

Frequently asked questions

In general, the term “prohibited tax shelter transaction” means listed transactions, transactions with contractual protection, or confidential transactions. With regard to prohibited transactions, tax-exempt entities are subject to additional reporting requirements.

IRS Form 8886, Reportable Transaction Disclosure Statement, is the tax form that taxpayers use to report certain transactions to the Internal Revenue Service. Certain transactions are deemed to be reportable when they include potential tax benefits the taxpayer would not normally be entitled to.

Taxpayers should attach Form 8886 to their federal income tax return or information return, including amended returns, for each tax year in which they participated in a reportable transaction.

Where can I find IRS form 8886?

You may find a copy of Form 8886 on the IRS website. For your convenience, we’ve enclosed the latest copy of the form in this article.

Related tax articles

This tax form is one of the fillable tax forms provided by the Internal Revenue Service, to help taxpayers reduce their tax preparation costs. To see more forms like this, visit our free fillable tax forms page, where you’ll also find articles like this.

Unlike the IRS, our articles contain step by step instructions for each tax form, as well as video walkthroughs. You can also check out all of our videos by subscribing to our YouTube channel!

Why didn’t the website open

I’m not sure why you experienced this. I just tried to open the article that this comment appears on, and everything seems to be working fine.