IRS Form 8586 Instructions

Certain taxpayers who invest in low-income housing may be able to take a tax credit to lower their tax liability using IRS Form 8586, Low Income Housing Credit.

In this article, we’ll walk through this tax form, including:

- How to complete IRS Form 8586

- Important information about the low income housing credit

- Frequently asked questions

Let’s start with a walkthrough of the tax form itself.

Table of contents

How do I complete IRS Form 8586?

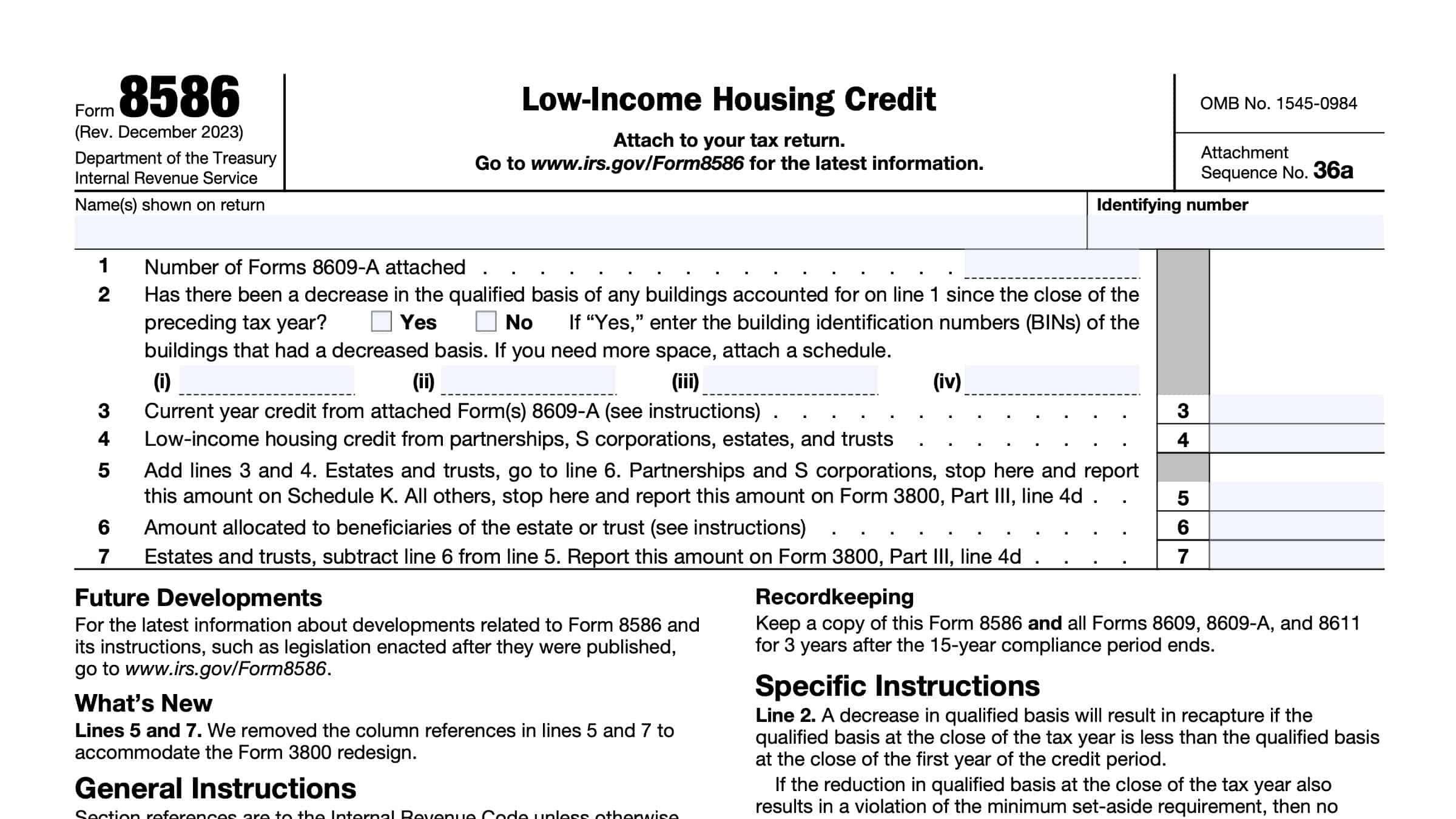

This one-page tax form is relatively straightforward. Let’s start at the top with the taxpayer information field.

Taxpayer information

Enter the taxpayer name as it appears on the federal income tax return. Under the identifying number field, enter the appropriate taxpayer identification number.

This could be an employer identification number (EIN) for pass-through entities such as trusts, estates, S corporations, or partnerships. For individual taxpayers, this will likely be a Social Security number (SSN) or individual taxpayer identification number (ITIN).

Line 1: Number of Forms 8609-A attached

In Line 1, enter the number of IRS Forms 8609-A that are attached to IRS Form 8586. Taxpayers use IRS Form 8609-A, Annual Statement for Low-Income Housing Credit, to

- Annually report compliance with low-income housing provisions, and

- Calculate the low-income housing credit

Once you’ve entered the number of forms in Line 1, proceed to Line 2.

Line 2

Has there been a decrease in the qualified basis of any buildings accounted for on Line 1 since the end of the previous year? Answer Yes or No.

If the answer is ‘Yes,’ then enter the building identification numbers (BINs) of the buildings that had a decreased basis. Attach a schedule if you need more space.

Decrease in qualified basis

A decrease in qualified basis will result in recapture if the qualified basis at the close of the tax year is less than the qualified basis at the close of the first year of the credit period.

If the reduction in qualified basis at the close of the tax year also results in a violation of the minimum set-aside requirement, then no credit is allowable for the year.

For more information about the minimum set-aside requirement, see the instructions for IRS Form 8609, Low-Income Housing Credit Allocation and Certification.

Line 3: Current year credit from attached Form(s) 8609-A

For each building, the amount of their low-income housing credit is calculated on a separate Form 8609-A. Attach a copy of each completed form to IRS Form 8586.

In Line 3, enter the total amount of the credit you calculated for the current tax year.

Line 4: Low-income housing credit from partnerships, S corporations, estates, and trusts

In Line 4, enter the part of the credit that you may have received from pass-through entities. This could be from any of the following:

- Partnerships

- S-corporations

- Estates & trusts

Line 5

Add Line 3 & Line 4. Enter the result here.

For estates & trusts, go to Line 6, below.

Partnerships and S-corporations should stop here and report this amount on Schedule K.

All other taxpayers stop here. Report this amount as part of the general business credit on IRS Form 3800, Line 4d.

Line 6: Amount allocated to beneficiaries

Enter the total part of the credit allocated to beneficiaries of the trust or estate.

You will need to properly allocate the low-income housing credit on Line 5 between the estate or trust and the beneficiaries. To do this, allocate each portion of the credit in the same proportion as income was allocated.

Enter the beneficiaries’ share on Line 6.

Line 7

For estates and trusts, subtract Line 6 from Line 5. Enter the result in Line 7 as well as on IRS Form 3800, Line 4d.

Video walkthrough

Watch this instructional video to learn more about claiming the low-income housing tax credit using IRS Form 8586.

Do you use TurboTax?

If you use TurboTax, and you’re completing this tax form for the first time, you might be ready to try TurboTax Federal Premium instead of the free or deluxe versions. TurboTax Federal Premium comes in two offerings, DIY or Live Assisted.

Do it yourself

To learn more about using TurboTax Federal Premium’s DIY option, click here.

Live Assisted

If you feel more comfortable having a tax expert guide you for the first time through this new form (or any other new forms), get started here.

Ready to hand the reins over to someone else completely? Go here to learn more about TurboTax’s Live Assisted Full Service offering!

About the low income housing credit

This investment credit cannot exceed the amount allocated to the building. Internal Revenue Code Section 42(h)(1) contains further details.

The low-income housing credit can only be claimed for residential rental buildings in low-income housing projects that meet one of the minimum set-aside tests. You can find more information about the set-aside tests in the IRS Form 8609 instructions.

Except for buildings financed with certain tax-exempt bonds, taxpayers may not take a low-income housing credit on a building if it has not received an allocation from the housing credit agency. No allocation is needed when 50% or more of the aggregate basis of the building and the land on which the building is located is financed with certain tax-exempt bonds.

However, the owner must still obtain Form 8609 from the appropriate housing credit agency. All applicable items should be completed, and there should be a BIN assigned.

Recapture of the low-income housing credit

There is a 15-year compliance period during which the residential rental building must continue to meet certain requirements.

If, as of the close of any tax year in this period, there is a reduction in the qualified basis of the building from the previous year, you may have to recapture a part of the credit you have taken.

Similarly, you may have to recapture part of the credits taken in previous years upon certain dispositions of the building or interests therein, unless you follow the procedures to prevent recapture. You can find additional guidance for recapture and building dispositions in the IRS Form 8609-A instructions.

If you must recapture credits, use IRS Form 8611, Recapture of Low-Income Housing Credit.

Frequently asked questions

No. As a component of the general business credit, this is a nonrefundable tax credit. This means that you can reduce your tax liability to zero, but this credit cannot create a tax refund.

You may take the low-income housing credit for each new qualified low-income building you place into service after 1986. You may take this nonrefundable tax credit over a 10-year credit period.

Not necessarily. Taxpayers who are not a pass-through entity, and whose only source of this credit is from pass-through entities, may claim this credit directly on IRS Form 3800.

Where can I find IRS Form 8586?

You can find the latest versions of IRS forms like IRS Form 8586 on the IRS website. For your convenience, we’ve attached the latest version to this article as an Adobe Acrobat file.