IRS Form 8908 Instructions

In 2022, the federal government passed the Inflation Reduction Act, which extended the energy efficient home credit to cover qualified new energy efficient homes sold or leased after 2021 and before 2033. Additionally, the Inflation Reduction Act updated the Internal Revenue Code with increases to certain business tax credits for certain homes sold or leased after 2022. Eligible contractors and homebuilders can claim these credits by filing IRS Form 8908 with their income tax return.

In this article, we’ll cover everything you need to know about IRS Form 8908, including:

- How to complete IRS Form 8908

- Who can claim the energy efficient home credit

- Frequently asked questions

Let’s begin with an overview of the tax form itself.

Table of contents

How do I complete IRS Form 8908?

IRS Form 8908 contains 3 parts:

- Part I: Information About Your Qualified Homes

- Part II: Certifier Information

- Part III: Qualified Homes’ Addresses

Before we begin Part I, let’s go over the questions at the top of the form.

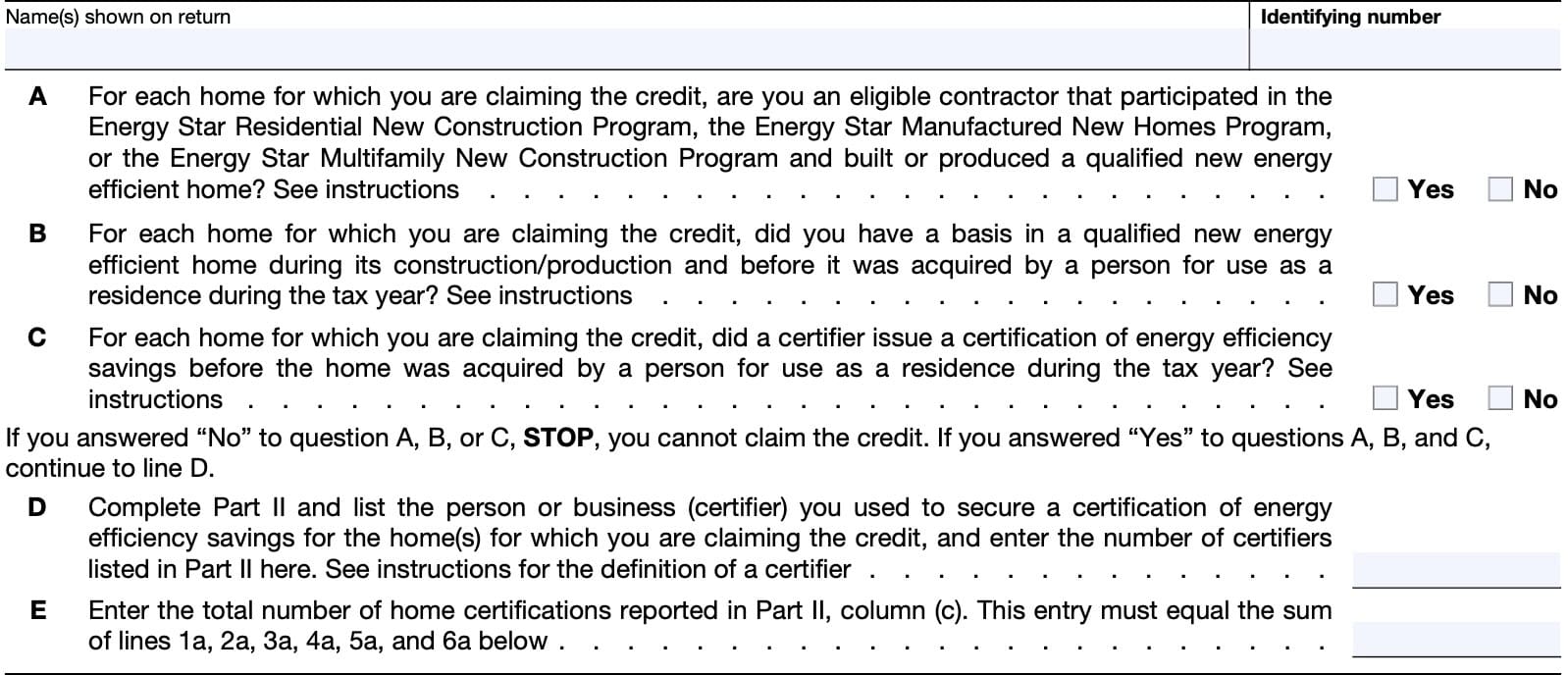

Top of IRS Form 8908

At the top of the form, you’ll see information fields for your name and identifying number, as shown on your tax return.

If your tax software does not automatically complete these fields, then do so and proceed to the first question.

For Questions A, B, and C, answer Yes or No. If you answer No to any of these questions, then stop. You cannot claim this tax credit.

Line A

For each home for which you are claiming the credit, are you an eligible contractor that participated in the

Energy Star Residential New Construction Program, the Energy Star Manufactured New Homes Program,

or the Energy Star Multifamily New Construction Program and built or produced a qualified new energy

efficient home?

Qualified New Energy Efficient Home

A qualified new energy efficient home is a dwelling unit located in the United States whose construction is substantially completed after August 8, 2005, and was acquired by another person on or before June 30, 2026, for use as a residence.

The home must be certified and meet certain energy saving requirements. Construction includes substantial reconstruction and rehabilitation.

Line B

For each home for which you are claiming the credit, did you have a basis in a qualified new energy

efficient home during its construction/production and before it was acquired by a person for use as a

residence during the tax year?

Check Yes if for each home you are claiming the credit, you had a basis in a qualified new energy efficient home during its construction/production and before it was acquired by a person for use as a residence during the tax year.

Line C

For each home for which you are claiming the credit, did a certifier issue a certification of energy efficiency savings before the home was acquired by a person for use as a residence during the tax year?

Check Yes if for each home you are claiming the credit, a certifier issued a certification of energy efficiency savings before it was acquired by a person for use as a residence during the tax year.

Line D

Complete Part II and list the person or business (certifier) you used to secure a certification of energy

efficiency savings for the home(s) for which you are claiming the credit, and enter the number of certifiers listed in Part II here.

Line E

Enter the total number of home certifications reported in Part II, column (c). This entry must equal the sum of Lines 1a, 2a, 3a, 4a, 5a, and 6a below.

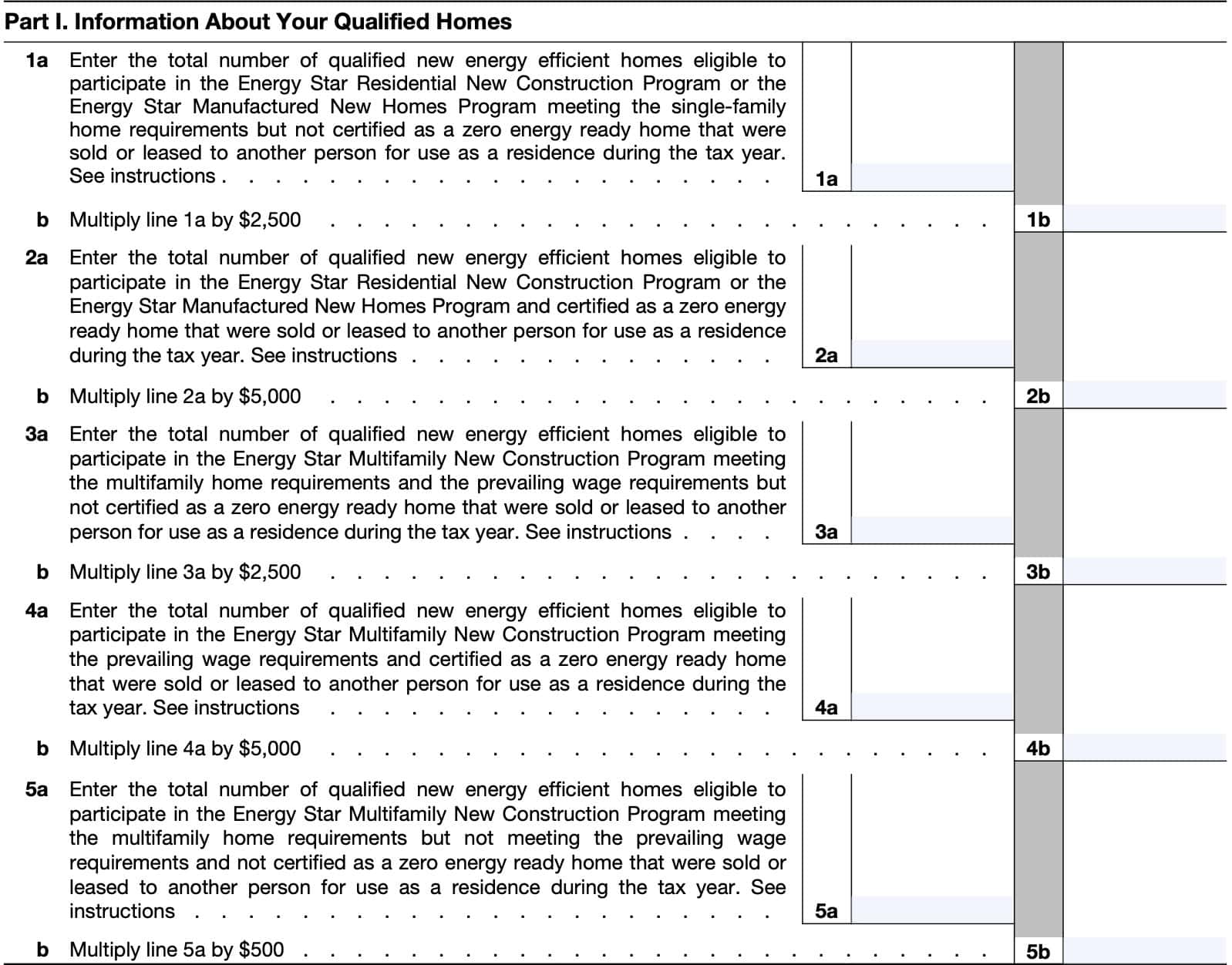

Part I: Information About Your Qualified Homes

Line 1: qualified new energy efficient homes that are not certified as zero energy ready

In Line 1a, enter the number of single-family homes sold or leased to another person for residential use that:

- Are eligible to participate in either of the following Energy Start programs:

- Energy Star Residential New Construction Program

- Energy Star Manufactured New Homes Program

- But have not been certified as zero energy ready homes

Energy Star Residential New Construction Program

The Energy Star Residential New Construction Program contains certain homebuilding requirements to improve a new home‘s energy efficiency and lower the home’s carbon footprint.

These requirements apply to the following dwelling types:

- Single family homes

- Duplexes

- Townhomes

Examples of additional Energy Star program requirements include:

- More energy-efficient air conditioning and heating

- Higher insulation requirements for walls, windows, and exterior doors

- Minimum energy standards for lighting and appliances

Depending on the new construction location, there may be additional state requirements to qualify.

The EnergyStar website contains additional information on specific Energy Star program requirements for qualified energy-efficient home construction.

Energy Star Manufactured New Homes Program

The Energy Star Manufactured New Homes Program contains certain homebuilding requirements to improve a manufactured home’s energy efficiency and lower the home’s carbon footprint vs an existing comparable home.

Depending on the new construction location, there may be additional state requirements to qualify.

The EnergyStar website contains additional information on required specifications for new manufactured home construction.

In Line 1b, multiply the number in Line 1a by $2,500. This represents your total tax credit amount for each new home that meets the Energy Star eligibility requirements.

Line 2: qualified new energy efficient homes that are certified as zero energy ready

In Line 2a, enter the number of homes built that meet the criteria outlined in Line 1 above, but also are certified as a zero energy ready home.

Zero energy ready homes

A zero energy ready home is a dwelling unit certified as a zero energy ready home under the Zero Energy Ready Home (ZERH) Program of the Department of Energy as in effect on January 1, 2023 (or any successor program determined by the Secretary of the Treasury).

The Department of Energy website contains more detailed information about applicable ZERH program requirements.

In Line 2b, multiply the number in Line 2a by $5,000. This represents your total tax credit for qualified new energy efficient homes certified as zero energy ready.

Line 3: Qualified new energy efficient multifamily new construction Homes

In Line 3a, enter the number of qualified energy efficient homes sold or leased during the taxable year that:

- Meet the Energy Star criteria for multi-family projects

- Meet the prevailing wage requirements, but

- Are not certified as a Zero Energy Ready Home

Homes that meet these energy efficiency requirements are eligible for a $2,500 credit in tax years 2023 through 2032.

In Line 3b, multiply the number in Line 3a by $2,500 and enter the result here.

What are prevailing wage requirements?

With respect to any qualified new energy-efficient homes, the prevailing wage requirements are that the eligible contractor shall ensure that any laborers and mechanics involved in the construction shall be paid wages at least equal to the prevailing rates for construction, alteration, or repair of a similar nature in the local area.

This requirement applies to anyone employed by the contractor, an authorized subcontractor, or other third-party contractor involved in the project. The Secretary of Labor determines the prevailing rates for localities.

For more detail, the Internal Revenue Service has posted guidance through Notice 2022-61, 2022-52 I.R.B. 560.

Line 4: Homes eligible for Energy Star and certified as Zero Energy

In Line 4a, enter the number of qualified energy efficient homes sold or leased during the calendar year that:

- Meet the Energy Star criteria for multi-family projects

- Meet the prevailing wage requirements, but

- Are certified as a Zero Energy Ready Home

In Line 4b, multiply the number in Line 4a by $5,000 and enter the result here.

Homes that meet these energy efficiency requirements are eligible for a $5,000 federal tax credit in tax years 2023 through 2032.

Line 5: Multifamily homes eligible for Energy Star, but not meeting prevailing wage requirements and not certified as Zero Energy

Homes that meet the Energy Star requirements but not the prevailing wage requirements may still qualify for a reduced amount of credit.

In Line 5a, enter the number of qualified energy efficient homes that are eligible to participate in the Energy Start Multifamily New Construction Program, but:

- Do not meet the prevailing wage requirements, and

- Are not certified as a Zero Energy Ready Home

In Line 5b, multiply the number in Line 5a by $500. Enter the total here.

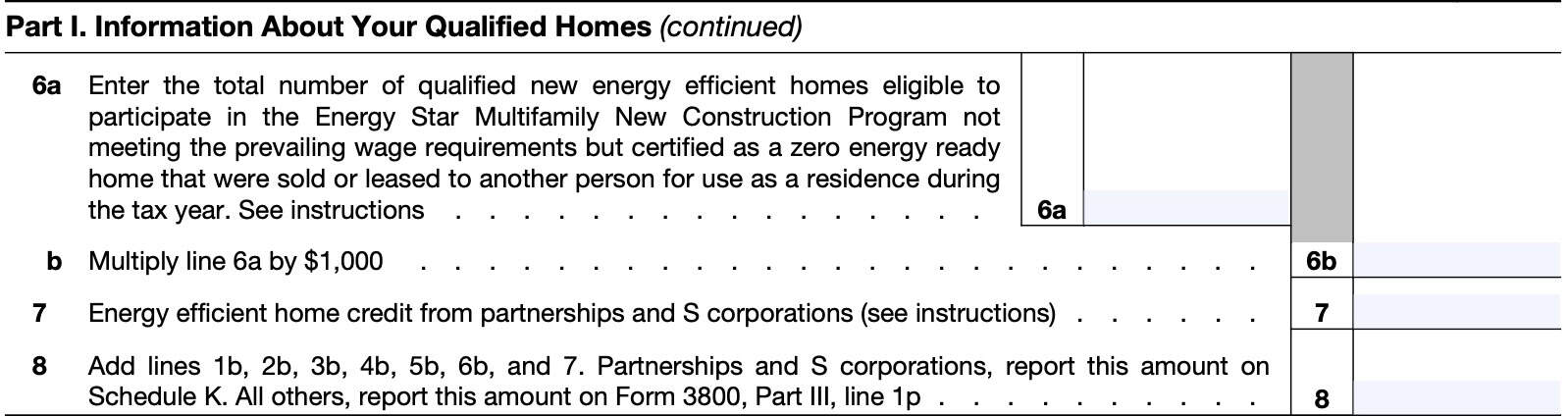

Line 6: Multifamily homes eligible for Energy Star, not meeting prevailing wage requirements but certified as Zero Energy

In Line 6a, enter the number of qualified energy efficient homes that are eligible to participate in the Energy Star Multifamily New Construction Program and:

- Do not meet the prevailing wage requirements, but

- Are certified as a Zero Energy Ready Home

In Line 6b, multiply the number in Line 6a by $1,000. Enter the total here.

Line 7: Energy efficient home credit from partnerships and S-corporations

For Line 7, partners and S-corporation shareholders will report any energy efficient home credits reported to them on their Schedule K-1.

Partnerships

For partners, these credits are reported on Schedule K-1 (Form 1065), Box 15, with reporting code ‘P.’

S corporations

S-corporation shareholders will find credits on their Schedule K-1 (Form 1120-S), Box 13, with reporting code ‘P.’

All other shareholders

All other filers figuring a separate credit on earlier lines also report the above credits on Line 7. Any taxpayer not using earlier lines to figure a separate credit can report the above credits directly on Part III of IRS Form 3800, Line 1p, as part of the general business credit.

Line 8: Total energy efficient home credit

Add the totals from Lines 1 through 7. Enter the total here.

For partnerships and S corporations, report this amount on Schedule K.

All other taxpayers should report this number on IRS Form 3800, Line 1p.

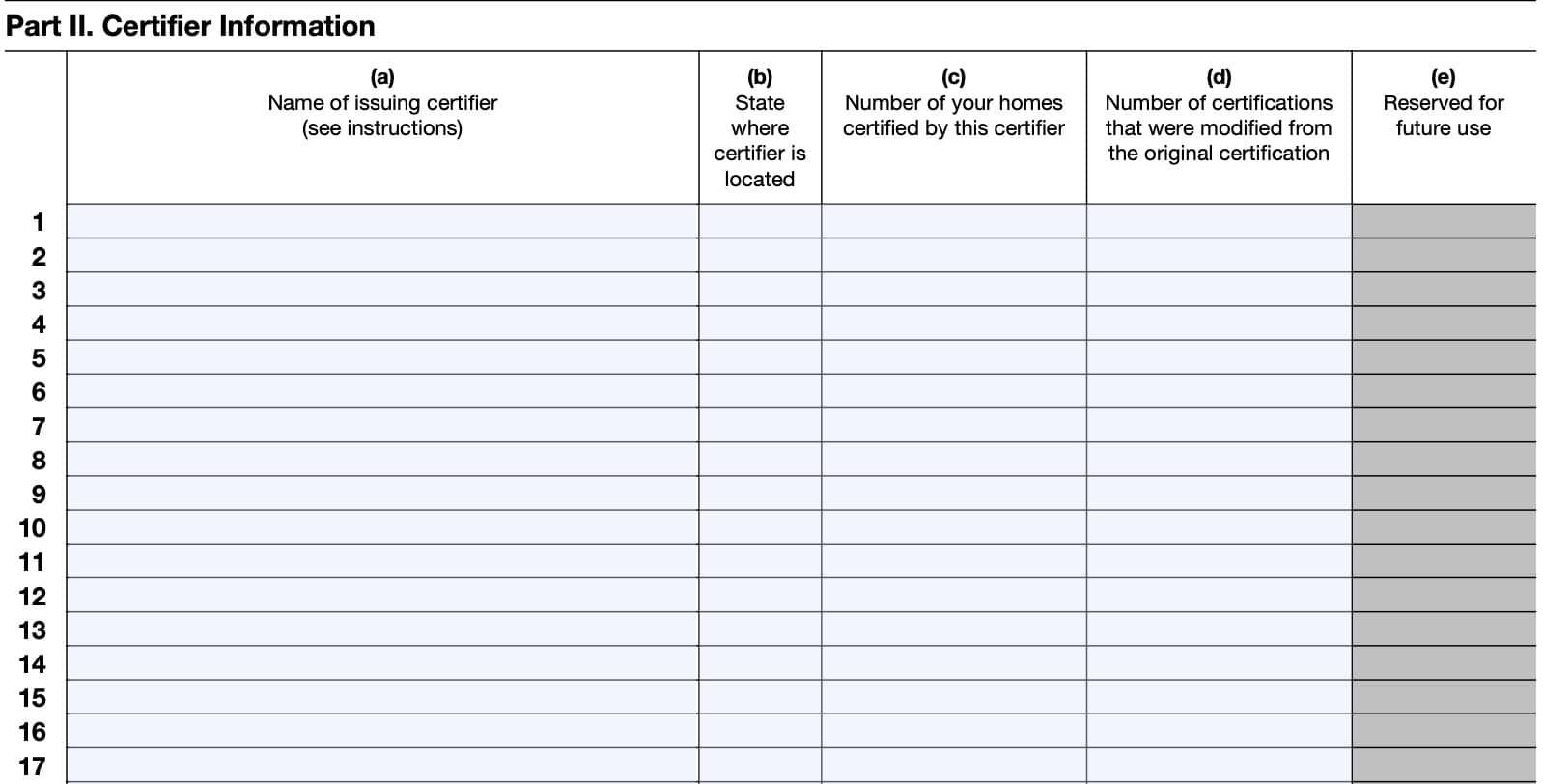

Part II: Certifier Information

Complete Part II for each certifier as follows:

Column (a): Name of issuing certifier

Enter the name of the person or business (certifier) that issued the energy efficient savings certification.

Add the total number of different certifiers shown in Lines 1 through 38 and enter in item D at the top of the form.

Column (b): State where certifier is located

Enter the two-letter state abbreviation where the certifier is located.

Column (c): Number of your homes certified by this certifier

Enter the total number of homes certified by this certifier.

Add the total number of home certifications shown in lines 1 through 38 and enter in item E at the top of the form.

Column (d): Number of certifications that were modified from the original certification

Enter the number of certifications that were modified from the original certification.

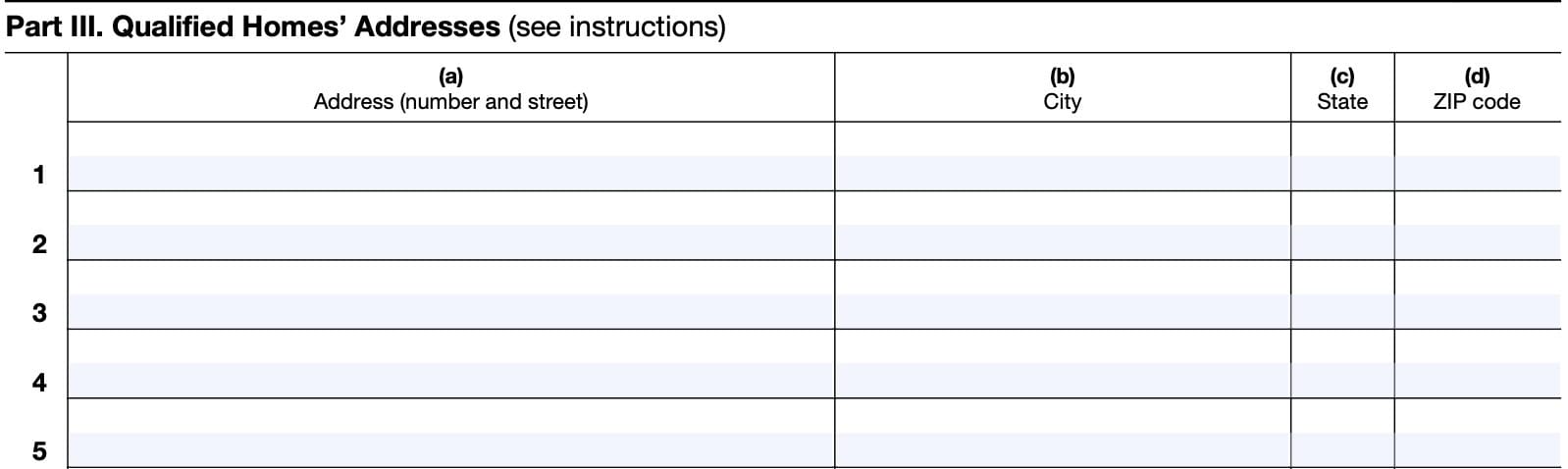

Part III: Qualified Homes’ Addresses

For each qualified home, enter the following information:

- Column (a): Address (including street name and number)

- Column (b): City

- Column (c): State

- Column (d): Zip code

Video walkthrough

Watch this instructional video to learn more about claiming the energy efficient home credit with Form 8908.

Frequently asked questions

For tax years 2023 through 2032, the energy efficient home credit total credit amount ranges from $500 to $5,000 per qualified home. Qualified homes that meet Zero Energy Home Ready requirements and multiple family homes that meet prevailing wage requirements can qualify for higher credits.

Wage requirements mandate that all contractors involved in the new home construction pay their employees wages at a rate at least equal to that of the prevailing rates in the given locality. The Secretary of Labor determines prevailing rates for this requirement.

A qualified new energy efficient home is a dwelling unit located in the United States, whose construction is substantially completed after August 8, 2005, and sold or leased to another person after 2005 but before June 30, 2026, for use as a residence. The home must be certified and meet certain energy savings requirements. Construction includes substantial reconstruction and rehabilitation.

No. This tax credit is specifically for eligible contractors for each qualified energy efficient home sold or leased to another person during the tax year for use as a residence.

Where can I find IRS Form 8908?

As with any other IRS form, you may find Form 8908 on the IRS website. For your convenience, we’ve enclosed the latest version in this article.

Related tax articles

This tax form is one of the fillable tax forms provided by the Internal Revenue Service, to help taxpayers reduce their tax preparation costs. To see more forms like this, visit our free fillable tax forms page, where you’ll also find articles like this.

Unlike the IRS, our articles contain step by step instructions for each tax form, as well as video walkthroughs. You can also check out all of our videos by subscribing to our YouTube channel!