IRS Form 8992 Instructions

In 2017, the Tax Cuts and Jobs Act introduced new rules for reporting income from certain foreign companies. This led to the creation of the IRS Form 8992, U.S. Shareholder Calculation of Global Intangible Low-Taxed Income (GILTI).

In this article, we’ll walk you through everything you need to know about IRS Form 8992, including:

- How to complete IRS Form 8992

- Key concepts, such as GILTI,

- Frequently asked questions for U.S. shareholders of a CFC

Let’s start by walking through this new form, step by step.

Table of contents

How do I complete IRS Form 8992?

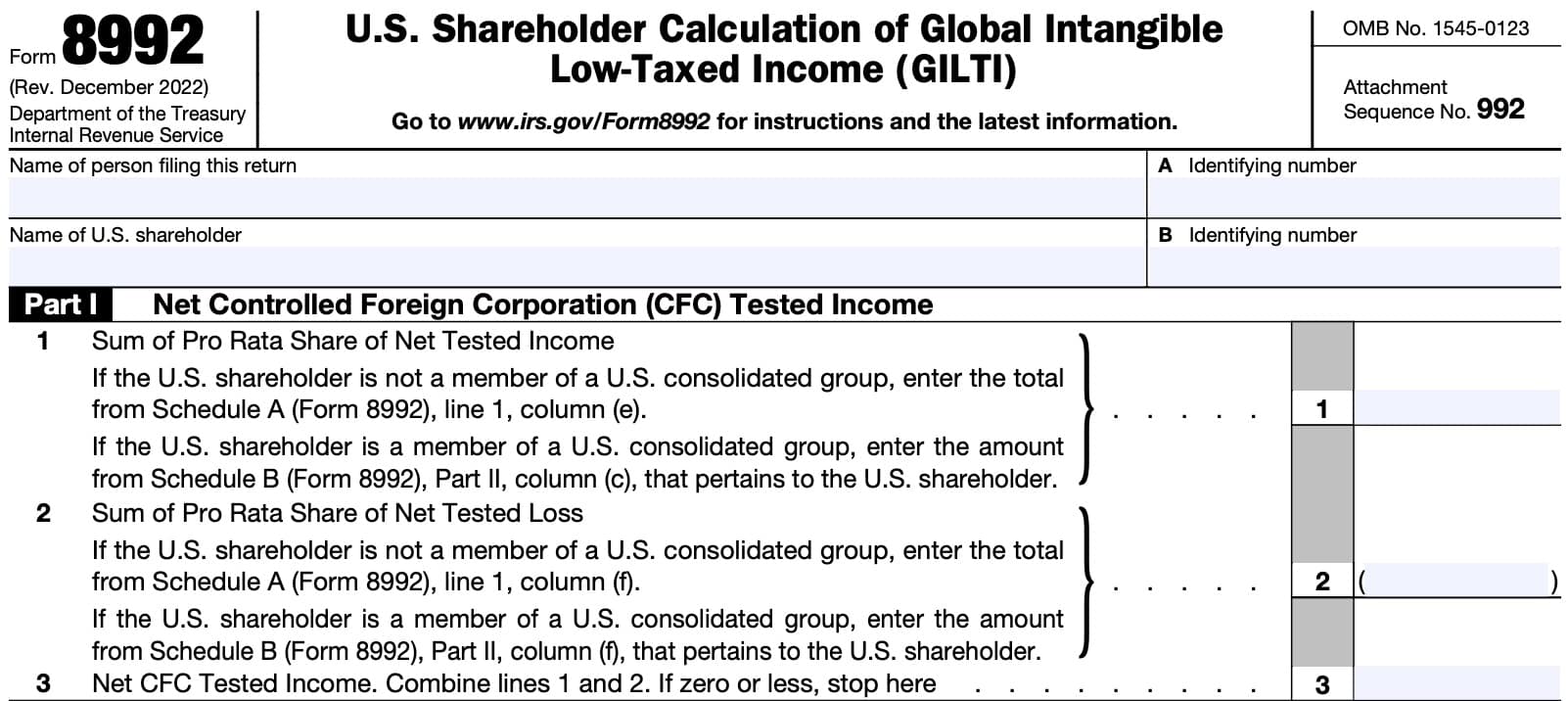

There are two parts to IRS Form 8992:

- Part I: Net Controlled Foreign Corporation (CFC) Tested Income

- Part II: Calculation of Global Intangible Low-Taxed Income (GILTI)

In addition, there are two schedules, one of which is required for completing the form itself:

- Schedule A: Schedule of Controlled Foreign Corporation (CFC) Information To Compute Global Intangible Low-Taxed Income (GILTI)

- Schedule B: Calculation of Global Intangible Low-Taxed Income (GILTI) for Members of a U.S. Consolidated Group Who Are U.S. Shareholders of a CFC

We’ll go through each part and schedule in depth. Let’s start at the top of the form with Part I of this tax form.

Part I: Net Controlled Foreign Corporation (CFC) Tested Income

At the top of the form, just before Part I, enter the person filing the income tax return as well as their identifying number. For individuals, the identifying number is their Social Security number.

For all other tax entities, the identifying number will be the employer identification number (EIN). Just below this field, enter the name of the U.S. shareholder and their identifying number.

In the case of a U.S. consolidated group, list the common parent as the person filing the tax return, then the EIN in the identifying number field. Leave the name of U.S. shareholder and corresponding identifying number field blank.

Line 1: Sum of Pro Rata Share of Net Tested Income

If the U.S. shareholder is not a member of a U.S. consolidated group, you will need to complete Schedule A (Form 8992), Columns (a) through (f).

If the U.S. shareholder is a member of a U.S. consolidated group, you’ll need to complete Schedule B (Form 8992), below.

From there, enter the total from either:

- Schedule A, Line 1, Column (e), or

- Schedule B, Part II, Column (c)

Line 2: Sum of Pro Rata Share of Net Tested Loss

Enter the appropriate amount, based upon whether the shareholder must complete Schedule A or Schedule B:

- Schedule A, Line 1, Column (f)

- Schedule B, Part II, Column (f)

Line 3: Net CFC Tested Income

Subtract Line 2 from Line 1, above. This represents your total net CFC tested income.

If the amount on Line 3 is greater than zero, complete Schedule A (Form 8992), columns (g) through (l).

If the amount on Line 3 is zero or negative, do not complete either Part II, below, or the rest of Schedule A. Instead, include the completed form and Schedule A with your income tax return.

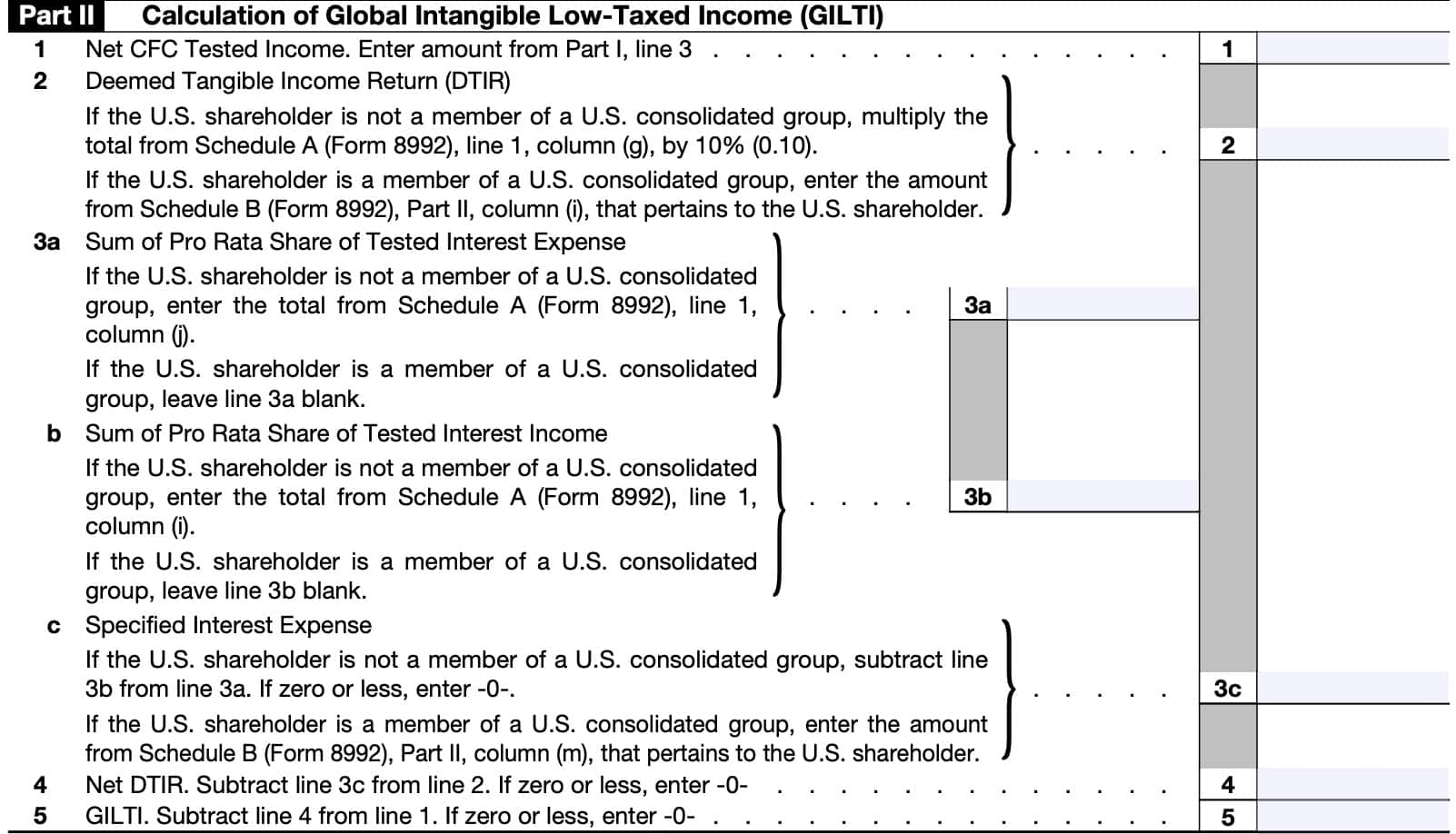

Part II: Calculation of Global Intangible Low-Taxed Income (GILTI)

In Part II, we’ll determine whether there is any GILTI income to report in the tax year.

Line 1: Net CFC Tested Income

Enter the amount from Part I, Line 3, above.

Line 2: Deemed Tangible Income Return

According to Internal Revenue Code Section 250, the term deemed intangible income means the excess, if applicable, of

- The deduction eligible income of the domestic corporation, over

- The deemed tangible income return of the corporation

The term deemed tangible income return means, with respect to any corporation, an amount equal to 10 percent of the corporation’s qualified business asset investment.

If the U.S. shareholder is not a member of a U.S. consolidated group

Multiply the total from Schedule A, Line 1, column (g), by 10% (0.10). Enter the result here.

If the U.S. shareholder is a member of a U.S. consolidated group

Enter the amount from Schedule B, Part II, column (i) pertaining to the U.S. shareholder.

Line 3a: Sum of Pro Rata Share of Tested Interest Expense

If The U.S. Shareholder Is Not A Member Of A U.S. Consolidated Group

Enter the total from Schedule A, Line 1, column (j).

If the U.S. shareholder is a member of a U.S. consolidated group

Leave Line 3a blank.

Line 3b: Sum of Pro Rata Share of Tested Interest Income

If The U.S. Shareholder Is Not A Member Of A U.S. Consolidated Group

Enter the total from Schedule A, Line 1, column (i).

If the U.S. shareholder is a member of a U.S. consolidated group

Leave blank.

Line 3c: Specified Interest Expense

If The U.S. Shareholder Is Not A Member Of A U.S. Consolidated Group

Subtract Line 3b from Line 3a. If the result is zero or less, enter ‘0.’ Otherwise, enter the result in Line 3c.

If the U.S. shareholder is a member of a U.S. consolidated group

Enter the amount from Schedule B, Part II, column (m) pertaining to the U.S. shareholder.

Line 4: Net DTIR

Subtract Line 3c from Line 2, then enter the result.

If zero or a negative number, enter ‘0.’

Line 5: GILTI

Subtract Line 4 from Line 1. If this results in zero or a negative number, enter ‘0.’

This represents the total global intangible low taxed income (GILTI) that you’ll enter as taxable income in your tax returns.

Individual shareholders will enter this amount on the proper ‘other income’ line from IRS Schedule 1 (if filing Form 1040) or a comparable line on other noncorporate tax returns.

Corporate shareholders will report GILTI income on the appropriate line of Schedule C of their IRS Form 1120, or a comparable line for other corporate returns.

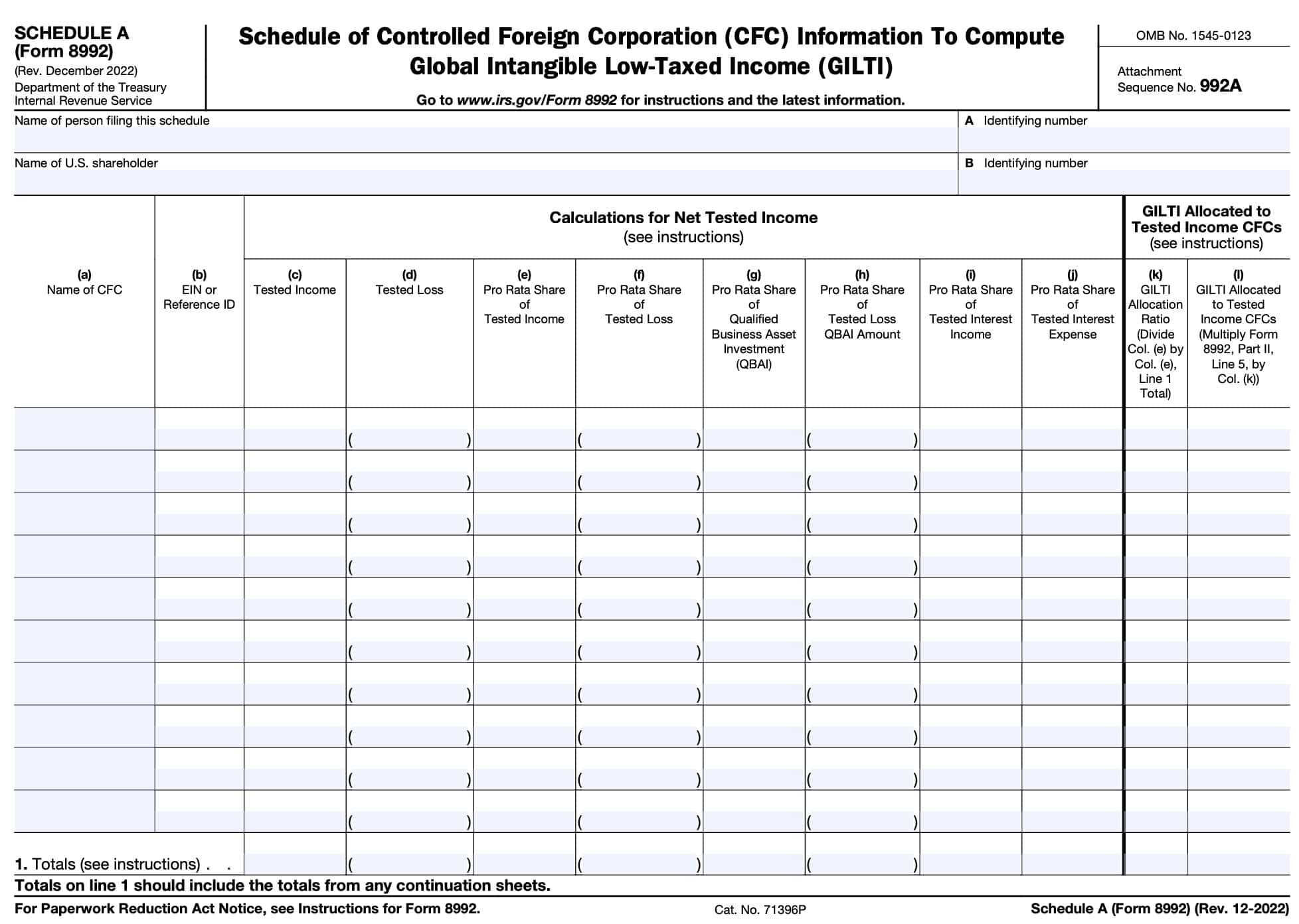

Schedule A: Schedule of Controlled Foreign Corporation (CFC) Information To Compute Global Intangible Low-Taxed Income (GILTI)

In the case of a U.S. shareholder that is not a member of a U.S. consolidated group, the U.S. shareholder of a CFC files Schedule A (Form 8992).

Schedule A allows U.S. shareholders of any CFC to report pro rata share of amounts for each CFC from each CFC’s IRS Form 5471, Schedule I-1. This helps to determine:

- The U.S. shareholder’s GILTI inclusion amount,

- Any GILTI inclusion amount allocated to CFCs

If a U.S. shareholder does not file a Schedule I-1 (Form 5471) for a CFC that is part of its GILTI computation, the U.S. shareholder will still need to provide amounts with respect to each CFC as if the U.S. shareholder filed Schedule I-1 for that CFC.

At the top of Schedule A, ensure that the names and identifying numbers for each person or U.S. shareholder are the same as at the top of IRS Form 8992.

Let’s go through each column so we can fully understand the required information for each CFC.

Column (a): Name of CFC

Enter the name of the CFC in column (a).

If the name of any of the CFCs being reported has changed within the past 3 years, include the prior name(s) in parentheses after the current name.

Column (b): EIN or Reference ID

If the CFC has an EIN, then enter the applicable EIN.

If the foreign company does not have an EIN, you must enter a reference ID number that uniquely identifies the CFC. Do not enter “FOREIGNUS” in column (b) in lieu of a reference ID number.

Note that if a U.S. shareholder is required either Schedule A or Schedule B with respect to a CFC, then the reference ID number from IRS Form 5471 must match the reference ID number in Schedule A or Schedule B for that same CFC.

Column (c): Tested Income

In column (c), enter the U.S. dollar amount of tested income, if any, for each CFC listed in column (a).

You’ll find the tested income figure on Line 6 of IRS Form 5471, Schedule I-1, for each CFC.

Column (d): Tested Loss

In column (d), enter the U.S. dollar amount of tested loss, if any, for each CFC listed in column (a).

You’ll find the tested loss figure on Line 6 of IRS Form 5471, Schedule I-1, for each CFC.

Column (e): Pro Rata Share of Tested Income

Enter your pro rata share of the tested income listed in column (c), as determined under Treasury Regulations Section 1.951A-1(d)(2)).

Column (f): Pro Rata Share of Tested Loss

Enter your pro rata share of the tested loss listed in column (d), as determined under Treasury Regulations Section 1.951A-1(d)(2)).

If the net CFC tested income from Part I, Line 3, was positive, complete columns (g) through (l).

Otherwise, you are finished with IRS Form 8992 and may file your completed form with your tax return.

Column (g): Pro Rata Share of Qualified Business Asset Investment (QBAI)

In column (g), enter your pro rata share of the U.S. dollar amount of QBAI, as

determined under Treasury Regulations Section 1.951A-1(d)(3). You’ll find this amount on Line 8 from Schedule I-1, Form 5471, for each tested income CFC.

If you have a tested loss for a particular CFC, do not make an entry for that CFC in this column. See

Treasury Regulations section 1.951A-3(b).

Column (h): Pro Rata Share of Tested Loss QBAI Amount

Enter your pro rata share of the tested loss QBAI amount of any tested loss CFC.

The tested loss QBAI amount of a tested loss CFC is the amount reported on Schedule I-1 (Form 5471), line 9c, that the tested loss CFC would have had if it were instead a tested income CFC.

For additional guidance, see Treasury Regulations Sections 1.951A-4(b)(1)(i) and 1.951A-4(b)(1)(iv).

Column (i): Pro Rata Share of Tested Interest Income

Enter your pro rata share of the amount of tested interest income from Schedule I-1 (Form 5471), Line 10c, for each CFC.

Column (j): Pro Rata Share of Tested Interest Expense

Enter your pro rata share of the amount of tested interest expense. You’ll find this on Line 9d, Schedule I-1, IRS Form 5471, for each CFC.

Column (k): GILTI Allocation Ratio

Before completing column (k), enter the totals (including amounts from any Schedule A Continuation Sheet(s)) of columns (c) through (j) on Line 1 for each column. From there, complete Part I and Part II on IRS Form 8992.

Then, for each CFC with an amount in column (e), divide that amount by the total on Line 1, column (e). Enter the result here to four decimal places.

Column (l): GILTI Allocated to Tested Income CFCs

For each CFC with an amount in column (e), multiply the column (k) ratio for that CFC by the GILTI amount located in Part II, Line 5. Enter the result in column (l) in whole dollars only.

This information is used in completing the following schedules on IRS Form 5471 for each of the foreign companies:

- Schedule J, Accumulated Earnings and Profits (E&P) of CFC

- Schedule P, Previously Taxed Earnings and Profits of U.S. Shareholder of Certain Foreign Corporations

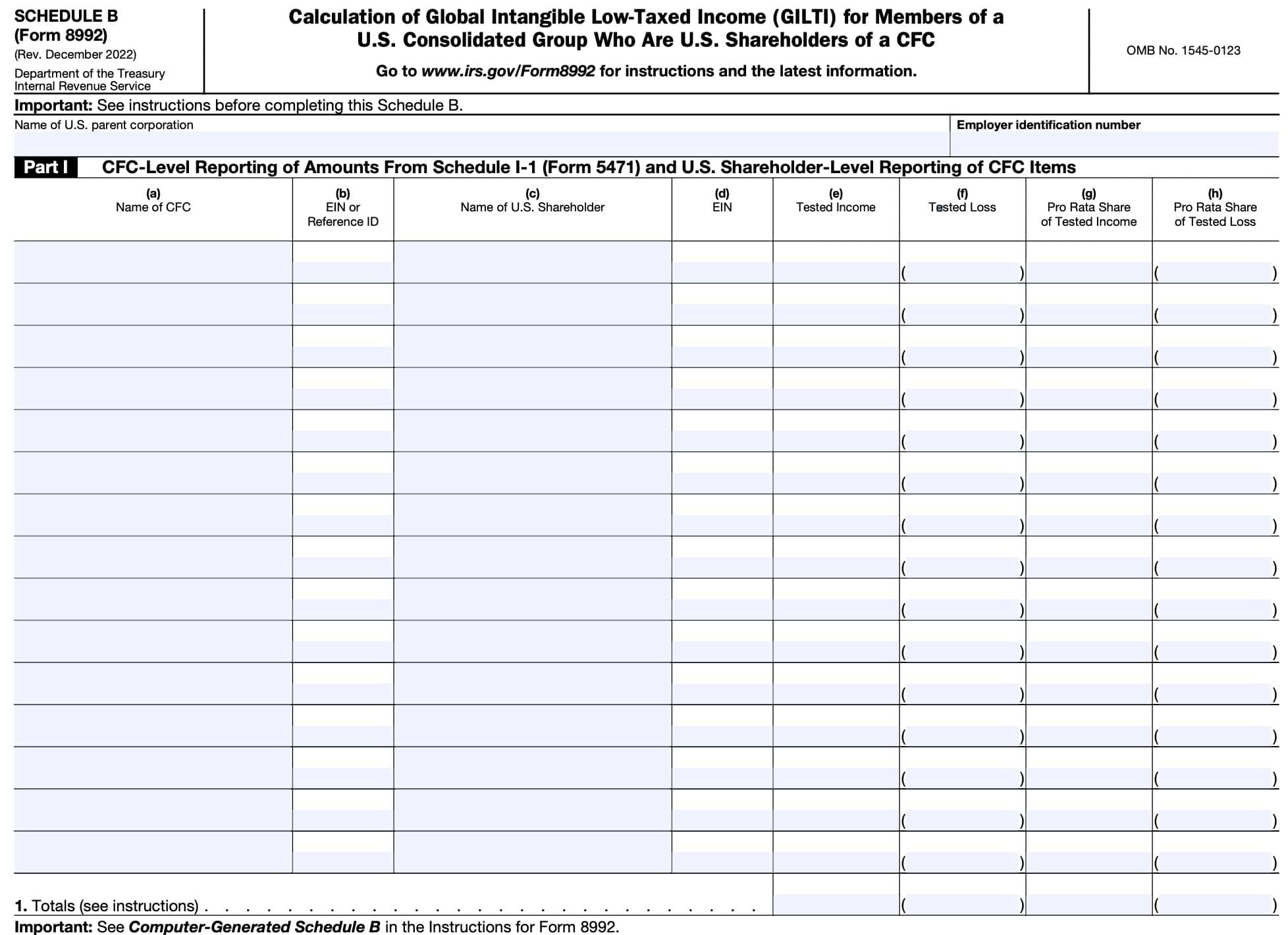

Schedule B: Calculation of Global Intangible Low-Taxed Income (GILTI) for Members of a U.S. Consolidated Group Who Are U.S. Shareholders of a CFC

Complete a single Schedule B for all members of the U.S. consolidated group that are U.S. shareholders of a CFC.

Certain amounts from Schedule B are carried over to the consolidated group’s Form(s) 8992. A separate Form 8992 is completed for each of the U.S. shareholders of CFCs. Additionally, a

consolidated Form 8992 is completed for the consolidated group as a whole.

The Schedule B and the consolidated Form 8992 are filed with the consolidated group’s income tax return.

How to complete Schedule B

Use the following steps to complete Schedule B:

Step 1

Complete 1 Schedule B for all members of the consolidated group that are U.S. shareholders of a CFC as follows:

- Complete Schedule B, Part I, columns (a) through (h), based upon the instructions for Part I, below.

- Enter the totals for columns (e) through (h) on Line 1 for each column.

- Column (e) and column (f) should not reflect items from any CFC more than once, even if the CFC is listed more than once

- If the Line 1 total for Part I, column (h) exceeds the Line 1 total for column (g), stop. Do not complete the rest of Schedule B. Proceed directly to Step 3, below.

- If the Line 1 total for Part I, column (g) exceeds the amount for column (h), then complete Part I, columns (i) through (n), as instructed below.

- Enter the totals for columns (i) through (n) on Line 1 of those columns.

- Skip columns (o) and (p) for now. Do not complete unless instructed to do so later.

- Complete all columns of Schedule B, Part II, as outlined below.

Step 2

Complete a separate copy of IRS Form 8992 to perform GILTI calculations for each U.S. shareholder of any CFC, as listed in Schedule B, Part II. Use the instructions on the front of Form 8992 to determine the GILTI inclusion amount for each U.S. shareholder of a CFC.

Step 3

Complete a consolidated Form 8992, as follows:

- If the Schedule B, Line 1 total for Part I, column (h), equals or exceeds the Column (g) amount:

- If the Schedule B, Line 1 total for Part I, column (h), is less than the Column (g) amount:

- For each line on Form 8992, aggregate the amounts from the corresponding line for all Forms 8992 completed for each U.S. shareholder listed in Step 2

- Enter the total on the corresponding line of the consolidated Form 8992

- File the consolidated IRS Form 8992 with the U.S. consolidated group’s federal income tax return for the taxable year.

- Complete Schedule B, Part I, columns (o) and (p), as outlined below.

- Do not file the Forms 8992 that you completed for each U.S. shareholder. Keep them for your records in case of an examination.

Part I: CFC-Level Reporting of Amounts from Schedule I-1 and U.S. Shareholder-Level Reporting of CFC Items

In Part I, complete columns (a) through (n) as outlined below. If otherwise instructed in Step 3, you may need to complete columns (o) and (p).

Column (a): Name of CFC

In column (a), list all CFCs, an interest in which is owned by any member of the consolidated group.

If more than one member of the consolidated group owns an interest in the same CFC, list the CFC on multiple lines, using a separate line for each member that owns an interest in the CFC. Be sure to note the name and EIN of the member that is a U.S. shareholder of the CFC in column (c) and column (d).

On each line, enter the name of the CFC in column (a).

If the name of any of the CFCs being reported on Schedule B has changed within the past 3 years, include the prior name(s) in parentheses after the current name.

Column (b): EIN or Reference ID number

If the CFC has an EIN, then you must enter that EIN in column (b).

If the CFC does not have an EIN, you must enter a reference ID number that uniquely identifies the CFC. This reference ID number must match that of the CFC listed in other areas of the tax return, such as IRS Form 5471.

Column (c): Name of U.S. Shareholder

For each CFC listed in column (a), enter the name of each U.S. shareholder that owns an interest in that CFC, within the meaning of IRC Section 958(a).

Column (d): EIN

For each U.S. shareholder listed in column (c), enter the EIN of the U.S. shareholder.

Column (e): Tested income

For each CFC listed in column (a), enter the U.S. dollar amount of tested income from IRS Form 5471, Schedule I-1, Line 6.

For each CFC listed in column (a), enter the column (e) amount on the corresponding line of the U.S.

shareholder’s applicable IRS Form 1118, Schedule D, Part I, column 6, for that CFC. This should be in the Form 1118 being completed for either of the following income categories, as applicable:

- Passive category income

- General category income

Column (f): Tested loss

For each CFC listed in column (a), enter the U.S. dollar amount of tested loss, if any, from IRS Form 5471, Schedule I-1, Line 6.

Column (g): Pro rata share of tested income

For each CFC listed in column (a) and the U.S. shareholder listed in column (c), enter the U.S. shareholder’s pro rata share of the CFC’s tested income, as determined under Treasury Regulations Section 1.951A-1(d)(2)).

For each CFC listed in column (a), enter the column (g) amount on the corresponding line of the U.S.

shareholder’s applicable IRS Form 1118, Schedule D, Part I, column 5, for that CFC.

Column (h): Pro rata share of tested loss

For each CFC listed in column (a) and the U.S. shareholder listed in column (c), enter the U.S. shareholder’s pro rata share of the CFC’s tested loss listed in column (f).

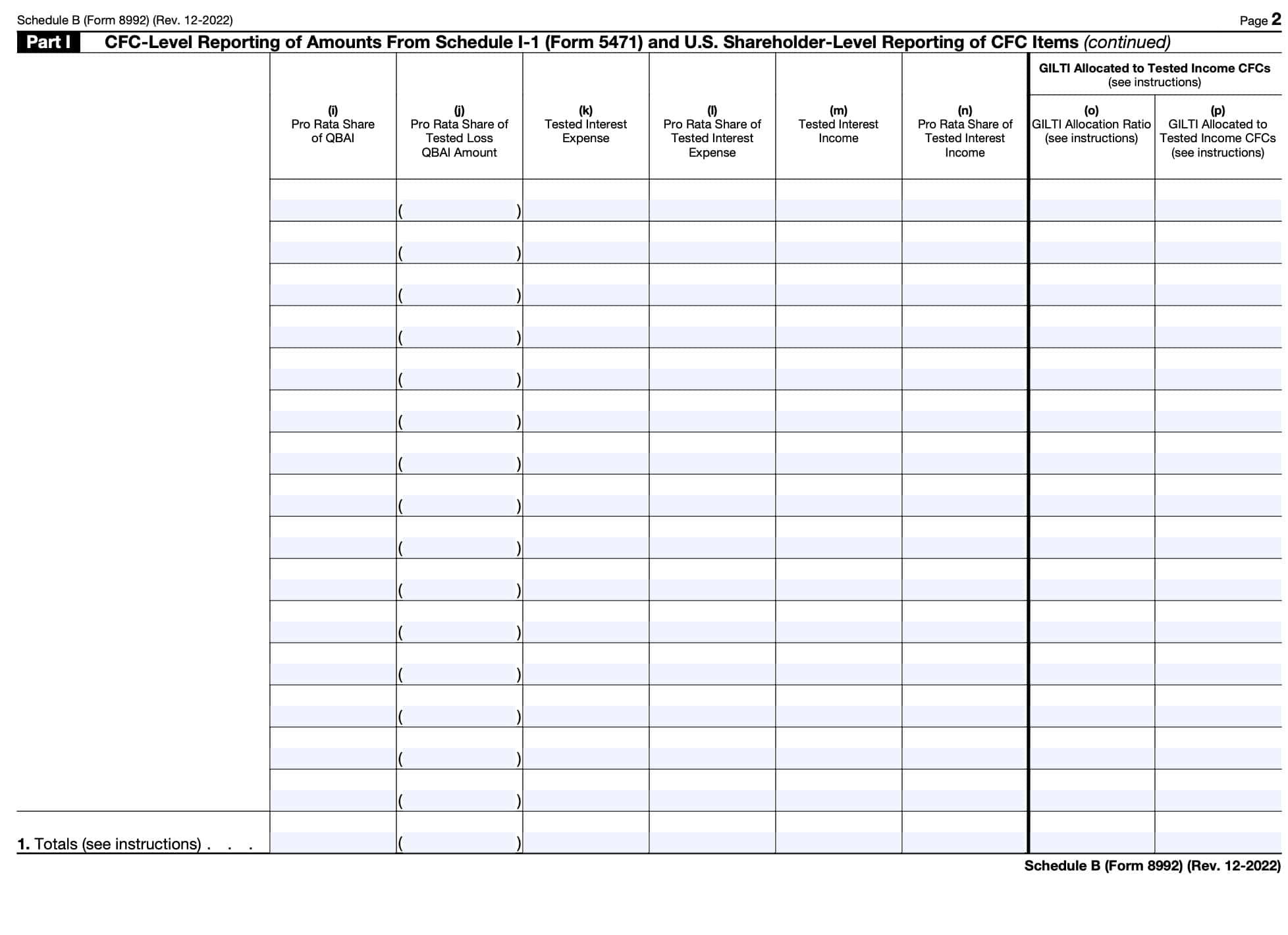

Column (i): Pro rata share of QBAI

For each tested income CFC listed in column (a) and the U.S. shareholder listed in column (c), enter the CFC shareholder’s pro rata share of the tested income CFC’s QBAI from Line 8 of that CFC’s Schedule I-1.

If you have a tested loss for a particular CFC, no entry should be made for that CFC in column (i).

Column (j): Pro rata share of tested loss QBAI amount

For each line where there is a U.S. shareholder listed in column (c) that owns an interest in a tested loss CFC listed in column (a) of that line, enter the U.S. shareholder’s pro rata share of the tested loss QBAI amount of the CFC.

The tested loss QBAI amount of a tested loss CFC is an amount equal to 10% of the QBAI from

IRS Form 5471, Schedule I-1, Line 9c, that the tested loss CFC would have had if it were instead a tested income CFC.

Column (k): Tested interest expense

For each CFC listed in column (a), enter the U.S. dollar amount of tested interest expense, if any, from IRS Form 5471, Schedule I-1, Line 9d.

Column (l): Pro rata share of tested interest expense

For each CFC listed in column (a) and the U.S. shareholder listed in column (c), enter the U.S. shareholder’s pro rata share of the CFC’s tested interest expense listed in column (k).

Column (m): Tested interest income

For each CFC listed in column (a), enter the U.S. dollar amount of tested interest income, if any, from IRS Form 5471, Schedule I-1, Line 10c.

Column (n): Pro rata share of tested interest income

Only complete column (n) if required.

For each CFC listed in column (a) and the U.S. shareholder listed in column (c), enter the U.S. shareholder’s pro rata share of the CFC’s tested interest income listed in column (m).

Column (o): GILTI Allocation Ratio

For each CFC listed in column (a), that has an amount in column (e), and the U.S. shareholder listed in column (c), divide the Part I, column (g), amount for that U.S. shareholder by the Part II, column (c), amount for that U.S. shareholder.

Enter the result to four decimal places. IRC Section 951A(f)(2) contains additional information.

Column (p): GILTI Allocated to Tested Income CFCs

For each CFC listed in column (a), that has an amount in column (e), and the U.S. shareholder listed in column (c), multiply the GILTI allocation ratio for that CFC, column (o), by the amount of the U.S.

shareholder’s GILTI inclusion amount from Form 8992, Line 5.

Enter the result in whole dollars only.

Line 1

Enter the totals for Part I, columns (e) through (p) on Line 1.

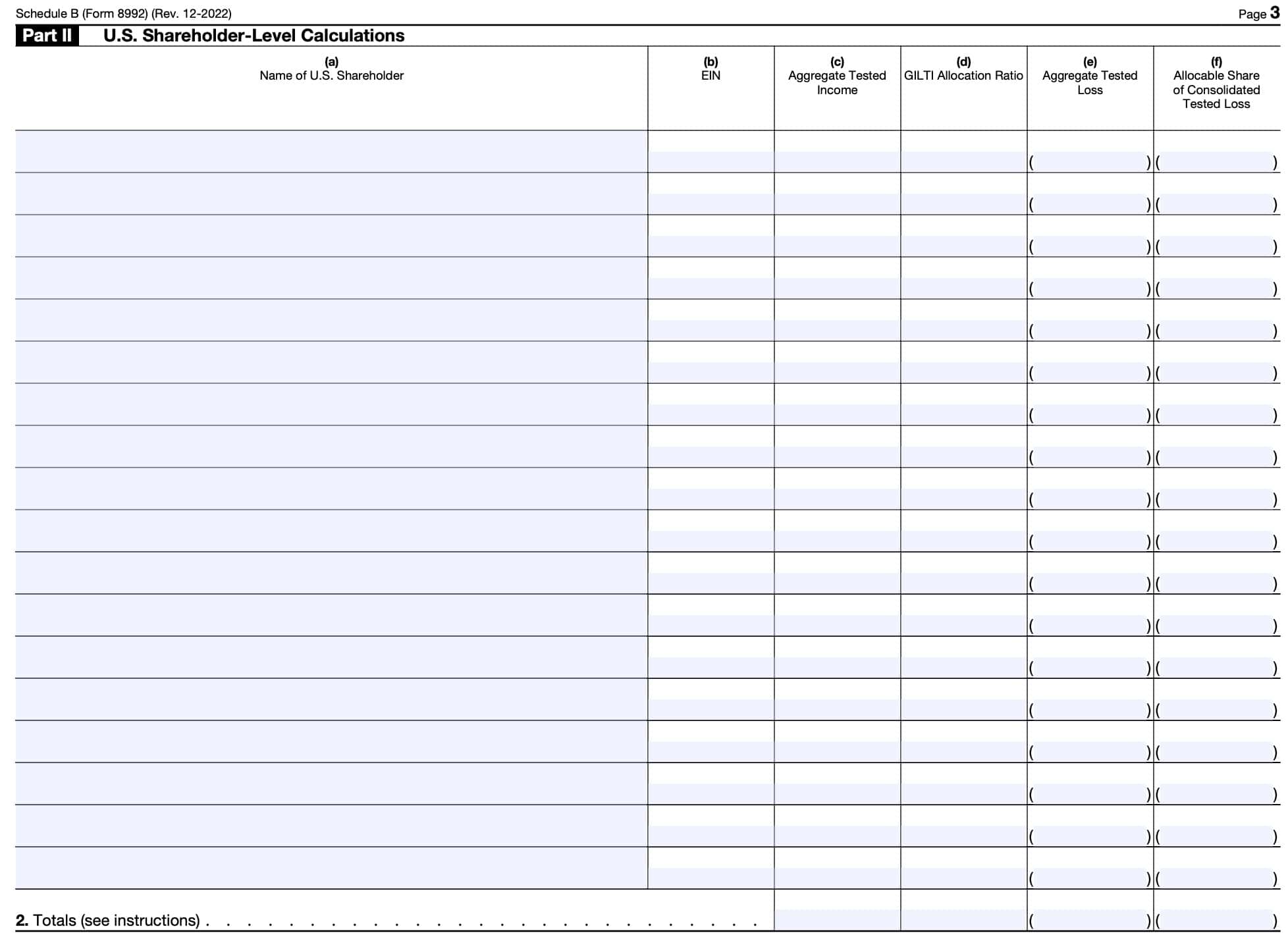

Part II: U.S. Shareholder-level calculations

Column (a): Name of U.S. Shareholder

For each U.S. shareholder listed in Part I, coludmn (c), enter in column (a), the name of each such shareholder, using a single line for each such U.S. shareholder.

Column (b): EIN

Enter the EIN of each U.S. shareholder listed in Part II, column (a).

Column (c): Aggregate tested income

For each U.S. shareholder listed in column (a), enter the sum of all amounts entered in Part I, column (g) with respect to that U.S. shareholder.

In other words, in Part II, column (c), sort and then sum the pro rata share of tested income amounts listed in Part I, column (g), by U.S. shareholder.

Each U.S. shareholder listed in Part II, column (a), will enter their Part II, column (c), amount on their Form 8992, Part I, Line 1.

Column (d): GILTI allocation ratio

For each U.S. shareholder listed in column (a), divide the column (c) amount for that U.S. shareholder by the total amount shown on Part II, Line 2d, column (c).

The GILTI allocation ratio computed here in Part II, column (d), is in accordance with Treasury Regulations Section 1.1502-51(e)(10). This differs from the GILTI allocation ratio computed in Part I, column (o), which accords with the rules of IRC Section 951A(f)(2).

Column (e): Aggregate tested loss

For each U.S. shareholder listed in Part II, column (a), enter the sum of all amounts

entered in Part I, column (h), with respect to that U.S. shareholder.

In other words, in Part II, column (e), sort and then sum the pro rata share of tested loss amounts listed in Part I, column (h), by U.S. shareholder.

Column (f): Allocable share of consolidated tested loss

For each U.S. shareholder listed in Part II, column (a), multiply the GILTI allocation ratio entered in Part II, column (d), with respect to that U.S. shareholder by the total amount shown on Part II, Line 2, column (e).

Each U.S. shareholder listed in Part II, column (a), will enter their Part II, Column (f), amount on their Form 8992, Part I, Line 2.

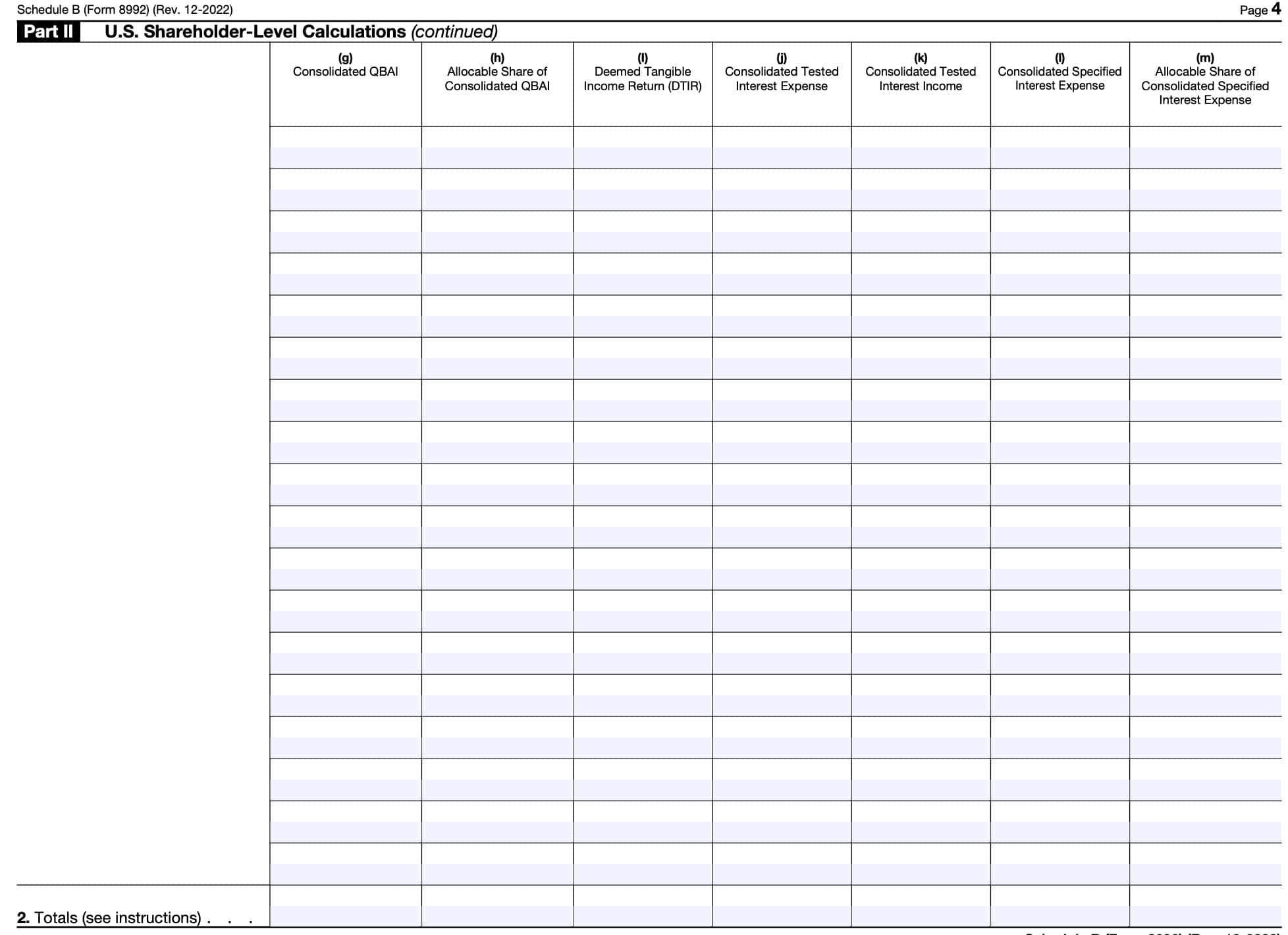

Column (g): Consolidated QBAI

For each U.S. shareholder listed in Part II, column (a), enter the sum of all amounts entered in Part I, column (i), with respect to that U.S. shareholder.

In other words, in Part II, column (g), sort and then sum the pro rata share of QBAI amounts listed in Part I, column (i), by U.S. shareholder.

Column (h): Allocable share of consolidated QBAI

For each U.S. shareholder listed in Part II, column (a), multiply the GILTI allocation ratio entered

in Part II, column (d), with respect to that U.S. shareholder by the total amount shown on Line 2, column (g).

Column (i): Deemed tangible income return (DTIR)

For each U.S. shareholder listed in Part II, column (a), multiply the Part II, column (h), amount by 10% (0.10).

Each U.S. shareholder listed in Part II, column (a), will enter their Part II, column (i), amount on their Form 8992, Part II, Line 2.

Column (j): Consolidated tested interest expense

For each U.S. shareholder listed in Part II, column (a), enter the sum of all amounts entered in Part I, column (l), with respect to that U.S. shareholder.

In other words, in Part II, column (j), sort and then sum the pro rata share of tested interest expense amounts listed in Part I, column (l), by U.S. shareholder.

Column (k): Consolidated tested interest income

For each U.S. shareholder listed in Part II, column (a), enter the sum of all amounts entered in Part I, column (n), with respect to that U.S. shareholder.

In other words, in Part II, column (k), sort and then sum the pro rata share of tested interest income amounts listed in Part I, column (n), by U.S. shareholder.

Column (l): Consolidated specified interest expense

For each U.S. shareholder listed in Part II, column (a), leave column (l) blank. However, on Line 2

(Totals) for column (l), subtract the total amount shown on Part II, Line 2, column (k), from the total amount shown on Part II, Line 2, column (j).

If the result is zero or less, enter ‘0.’

Column (m): Allocable share of consolidated specified interest expense

For each U.S. shareholder listed in Part II, column (a), multiply the GILTI allocation

ratio entered in Part II, column (d), with respect to that U.S. shareholder by the total amount shown on Part II, Line 2, column (l).

Each U.S. shareholder listed in Part II, column (a), will enter their Part II, column (m), amount on their Form 8992, Part II, Line 3c.

Line 2

For Line 2, enter the totals of the following columns:

Video walkthrough

Watch this instructional video to learn more about calculating GILTI using IRS Form 8992.

Frequently asked questions

IRS Form 8992 helps U.S. shareholders of a CFC calculate the amount of global intangible low-taxed income (GILTI) includible in gross income. In simple terms, GILTI is the part of your foreign company’s profits that the U.S. government thinks should be taxed in the U.S., because those profits are considered “easily moved” or “intangible” (like earnings from patents, software, or services).

Some taxpayers may be eligible for a tax deduction under IRC Section 250.

You need to file Form 8992 if you’re a U.S. person who owns part of a foreign company that’s controlled by U.S. shareholders. This is called a controlled foreign corporation or CFC.

This usually means you own 10% or more of the foreign company’s stock. If that company earned profits during the year, the IRS may require you to report and pay U.S. tax on a portion of those earnings — even if you didn’t receive a cash payment.

Taxpayers file IRS Form 8992 with their regularly scheduled tax return. If you file as part of a group of companies that share one U.S. tax return, you use a special schedule for consolidated filers. The deadline is the same as your normal tax return deadline, including any extensions you file.

Where can I find IRS Form 8992?

You can find this new form on the IRS website. For your convenience, we’ve enclosed the latest version as a PDF form on this article, just below.