IRS Form 1098-C Instructions

Contributions of motor vehicles can be a great tax deduction for charitably inclined tax taxpayers who already itemize their tax deductions on income tax returns. But did you know that the donee organization must report each contribution of a qualified vehicle with a claimed value of over $500 to the Internal Revenue Service? This article will walk you through IRS Form 1098-C, so that you understand:

- What to expect from the charity for your vehicle donation

- IRS requirements for an allowable charitable deduction

- How to avoid key mistakes that could increase your income tax bill

Let’s start with walking step by step through this tax form so you can better understand it.

Table of contents

IRS Form 1098-C Instructions

Even if you are the donor, it’s worth understanding how this form works from the donee’s perspective. That way, you can better understand how the tax write-off works when you do your own taxes for the given tax year.

There are 3 identical copies of this form, which we’ll briefly discuss.

- Copy A: The donee organization submits the completed Copy A to the IRS, with a submittal document known as IRS Form 1096.

- Copy B: Given to the donor to submit with their federal income tax return

- Copy C: Given to the donor for their records

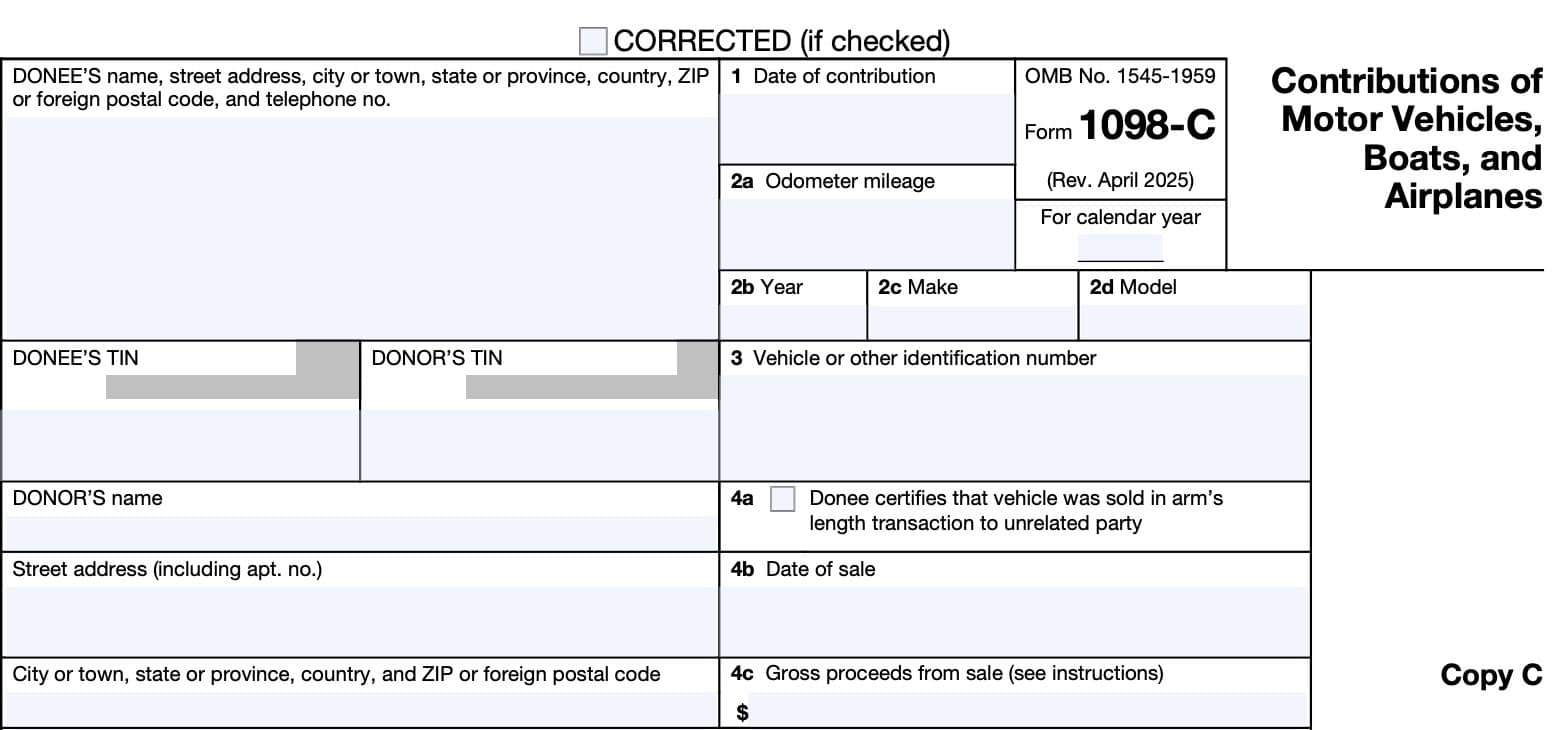

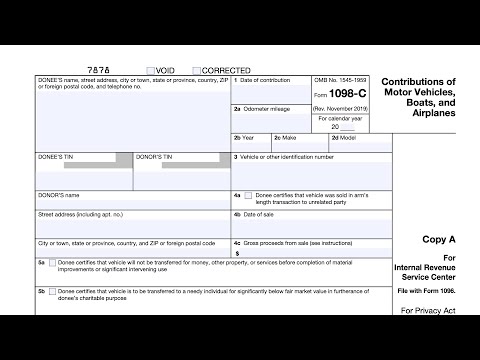

Let’s go through this form from the charity’s perspective. On the left-hand side of the form, there are information fields for both the donee and donor.

Donee’s information

This includes the name of the charitable organization, as well as the following contact information:

- Street address

- City or town

- State

- Country

- Zip code or postal code

- Telephone humber

Just below this, the donee will include their tax identification number (TIN).

Donor’s information

The donee also includes the same information for the donor:

- Tax identification number

- For most donors, this is the donor’s Social Security number

- Donor’s name

- Donor’s address

Box 1

In Box 1, the donee will mark the date of the contribution.

Box 2

If the donation is a car, the mileage information goes into Box 2a. Year, make, and model of the vehicle go into Box 2b, Box 2c, and Box 2d, respectively.

If the donation is a plane or boat, the IRS does not require mileage information from the vehicle’s odometer.

Pro tip: The odometer reading should be in miles, not kilometers. If your donated vehicle’s odometer is in kilometers, make sure the donee made the proper conversion. The IRS instructions recommend using the following conversion:

1 kilometer = 0.62137 miles

Box 3: Vehicle identification number

Box 3 should contain the vehicle identification number, or VIN.

For a car or truck, this is a 17-digit number that might appear in a couple of places on the vehicle. On a boat, this number is 12 characters in length and is usually found on the starboard transom. For aircraft, the identification number is 6 digits and is located on the aircraft’s tail.

Box 4

The items in Box 4 contain information about a sale of the vehicle in question.

Box 4a, if checked, is the donee’s certification that the vehicle was sold in an arm’s length transaction to an unrelated party. In other words, if checked, then the donor’s charitable deductions for this contribution likely cannot exceed the amount in Box 4c, below.

Box 4b indicates the date of sale, while Box 4c should reflect the gross proceeds from the sale. The IRS form instructions specifically tell donees not to include any fees or expenses incurred in Line 4c.

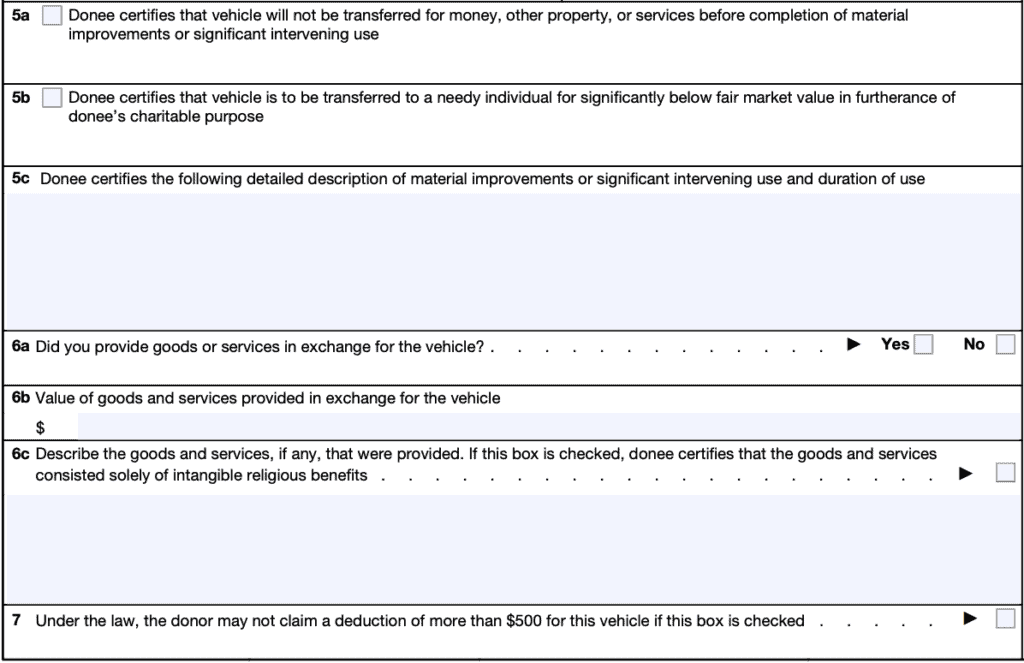

Box 5a

If this box is checked, this indicates that the charitable organization does not intend to sell or transfer the vehicle without either material improvements or significant intervening use.

Material improvements are improvements that improve the vehicle’s condition in a way that greatly increases the value of that vehicle.

Significant use is not an exact definition. According to the IRS website, examples of significant use might include providing transportation on a regular basis for a significant period of time or significant use directly relating to training in vehicle repair.

The donee should not check this box if the vehicle’s value is under $500.

Box 5b

If the donee has checked this box, this means that the donee intends to transfer the vehicle to a needy individual for much lower than the vehicle’s fair market value. The organization might do this because it directly supports the organization’s charitable purpose of relieving the poor and distressed or underprivileged who are in need of a means of transportation.

The donee should not check this box if the vehicle’s fair value is $500 or less.

Pro tip: If this box is checked, then the donor’s tax deduction is not limited to the amount in Box 4c, above.

Box 5c

If completed, Box 5c will contain the charitable organization’s description of future improvements or intended significant use of the donated vehicle. If the fair value is $500 or less, this box might be empty.

Box 6a

If checked, this indicates that the charitable organization provided goods and services in exchange for the donated vehicle.

Box 6b

Box 6b contains the approximate value of any goods and services rendered in exchange for the vehicle, as marked in Box 6a. The IRS requires all donee organizations to give a good faith estimate of goods and services exchanged for donations. This includes intangible religious benefits, as well as any goods or services that the organization may provide in a year other than the current year.

Pro Tip: You may be able to check this information in IRS Publication 561, Determining the Value of Donated Property, to verify accuracy.

Box 6c

This box, if completed, contains the organization’s description of goods and services exchanged for the vehicle. If the donee has checked the box in this section, this means that the donee certifies the goods and services consisted solely of intangible religious benefits.

An intangible religious benefit is one that:

- An organization provides organized exclusively for religious purposes and

- Which generally is not sold in a commercial transaction outside the donative context

Box 7

If checked, the donor may not claim a deduction that exceeds $500.

Filing IRS Form 1098-C

For tax entities who must file this tax form with the Internal Revenue Service, the IRS requires certain paper versions of information returns to be accompanied by IRS Form 1096, Annual Summary and Transmittal of U.S. Information Returns.

Check out our step-by step instructional guide for more information on how to submit your information return with IRS Form 1096.

What is IRS Form 1098-C used for?

Any charitable organization that receives qualified vehicle donations must report each donation of a vehicle where the claimed value of that vehicle is $500 or more. The donee organization reports the donation on IRS Form 1098-C, Contributions of Motor Vehicles, Boats, and Airplanes.

As the form’s name indicates, Form 1098-C isn’t used for reporting only car donations. The charity must use this to report the donation of any qualified vehicle for a charitable purpose.

What is a qualified vehicle?

According to the IRS instructions, a qualified vehicle can be any of the following:

- Any motor vehicle manufactured primarily for use on public streets, roads, and highways

- Any boat

- Any airplane

However, a qualified vehicle does not include any vehicles held primarily for sale, such as the inventory of a car dealer or boat dealer.

But the donee organization completes this form, not the donor. This ensures that a series of checks and balances exists so that donors don’t get into trouble for improperly claiming this tax deduction. But the form is only required in certain situations.

When is IRS Form 1098-C required?

The 1098-C form is only required when the claimed value of the donated vehicle exceeds $500. According to the tax law, a contemporaneous written acknowledgement is required within 30 days of the vehicle’s donation. Without this written acknowledgement, the donor cannot legally claim a deduction of more than $500.

What is a contemporaneous written acknowledgment?

Internal Revenue Code Section 170 requires that a charitable organization sends written acknowledgement within 30 days of either the date of sale or date of contribution for each charitable contribution of a motor vehicle, airplane or boat. The donee organization may use Copy B of the 1098-C Form as written acknowledgement.

However, the IRS instructions also state that charitable organizations should not file Form 1098-C if the claimed value is $500 or less. They may do so, by providing the donor with Copy C only. In this case, the donee organization must check Box 7 on the form itself.

Video walkthrough

Watch this instructional video to learn more about Form 1098-C.

Are you tired of dreading tax season?

If you’re like most people, you push through the stress of filing, only to be hit with a bigger bill than expected—then put it all behind you until the same cycle repeats next year.

But what if you could change the game?

Tax planning puts you in control. It’s about being proactive, not reactive—taking small, smart steps throughout the year to reduce your tax burden, increase your savings, and keep more of your hard-earned money working for you.

Here’s what effective tax planning helps you do:

✅ Avoid the surprise of a high tax bill

✅ Understand how your income and decisions affect your taxes

✅ Strategically lower your tax liability over time

Ready to make smarter tax moves?

👉 Join my free weekly tax planning newsletter and get one actionable tip every week to help you reduce your taxes legally and effectively.

Start taking control—your future self will thank you.

Frequently asked questions

Any charitable organization who receives a qualified vehicle must file IRS Form 1098-C with the IRS and provide a copy to the donor within 30 days of either the date of sale or date of donation.

A charitable organization must file Form 1098-C within 30 days of the sale of a donated vehicle or 30 days of receipt of the vehicle.

Internal Revenue Code Section 6720 imposes penalties on any donee organization that is required under section 170(f)(12) to furnish an acknowledgment to a donor if the donee organization knowingly fails to furnish an acknowledgment or furnishes a false acknowledgment.

As a taxpayer, you may include an electronic copy B with your tax return, if your tax preparation software allows this to be submitted electronically. Otherwise, you may need to send a paper version of Copy B to the IRS, along with IRS Form 8453, U.S. Individual Income Tax Transmittal for an IRS e-File Return.

If you are the taxpayer and donor, you do not have to file Form 1098-C with your tax return if you do not intend to claim the deduction. For example, if your tax preparer informs you that you would be better off claiming the standard deduction than itemizing deductions on Schedule A, then you do not need to file this form.

Where can I find IRS Form 1098-C?

This tax form is available on the IRS website in PDF format. For your convenience, we’ve included the most recent version of this form at the bottom of our article.