IRS Form 14135 Instructions

A taxpayer who receives a notice of federal tax lien (NFTL) can expect the Internal Revenue Service to place a tax lien on their property. This lien will stay in place until the taxpayer has paid the federal government the outstanding tax debt, plus penalties and interest. However, federal law does allow the Internal Revenue Service to discharge property from a federal tax lien if it’s in the government’s interest to do so. This article will walk you through using IRS Form 14135 to do just that.

Additionally, we’ll cover:

- Different ways you might get rid of a tax lien, even if you can’t fully pay your tax bill

- When you might consider discharging property from a federal tax lien

- How to request a certificate of discharge from a tax lien

Let’s start by going through Form 14135, step by step.

Table of contents

How do I complete IRS Form 14135?

Let’s break down this three-page application form, step by step.

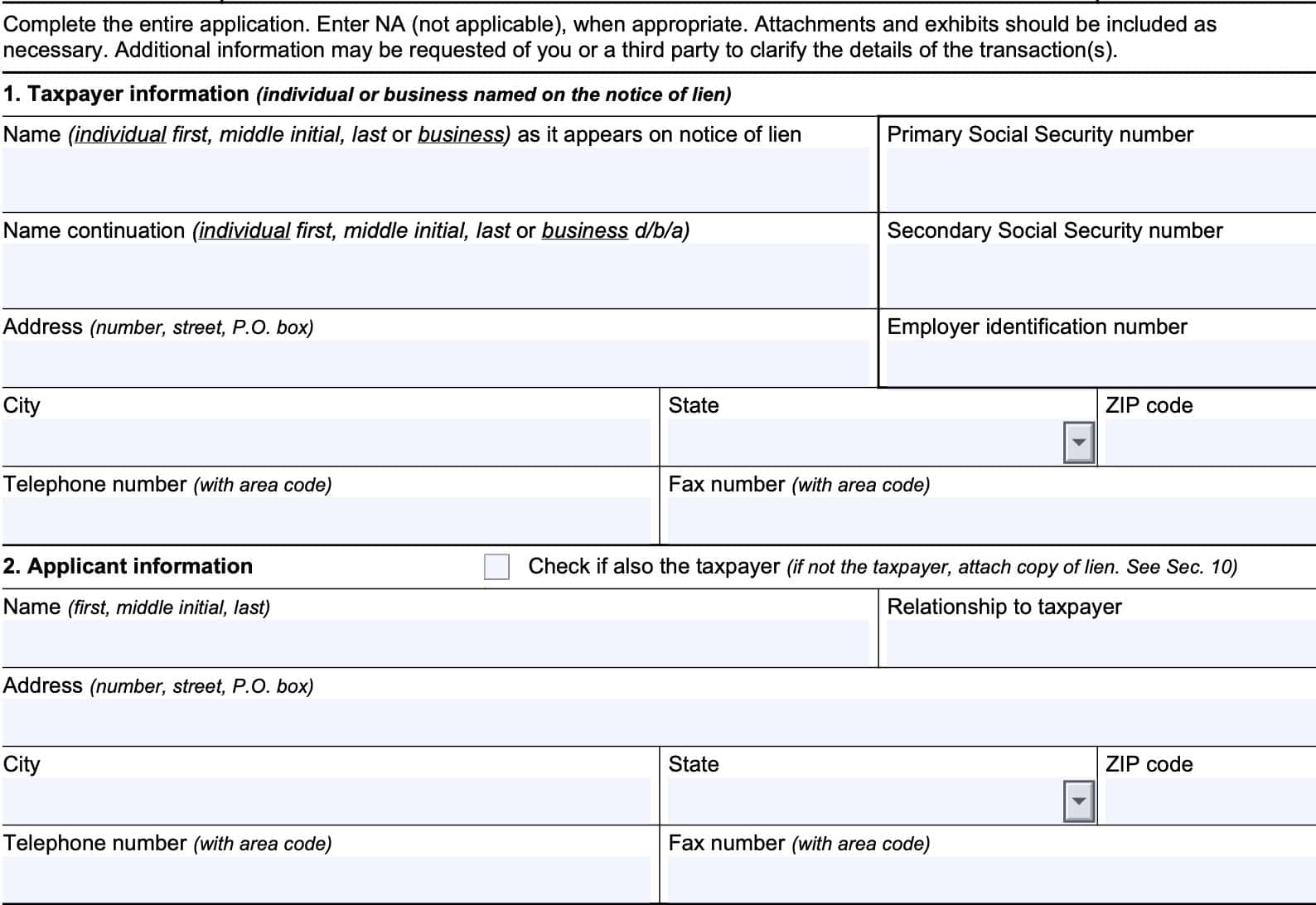

Line 1: Taxpayer information

The first step in this form is to enter the taxpayer’s personal information as it appears on the tax lien. If necessary, there is a second line for a spouse or other business name.

Enter the last 4 digits of the SSN, as appropriate, or the employer identification number (EIN). Complete the address information as it appears on the tax lien, including:

- Street number and street name

- City

- State

- Zip code

- Phone number

- Fax number (if applicable)

Line 2: Applicant information

Check the box if the applicant and taxpayer are the same person. If you are the applicant filing on the taxpayer’s behalf, then enter your information as indicated:

- Name

- Relationship to the taxpayer

- Address

- Telephone number

- Fax number

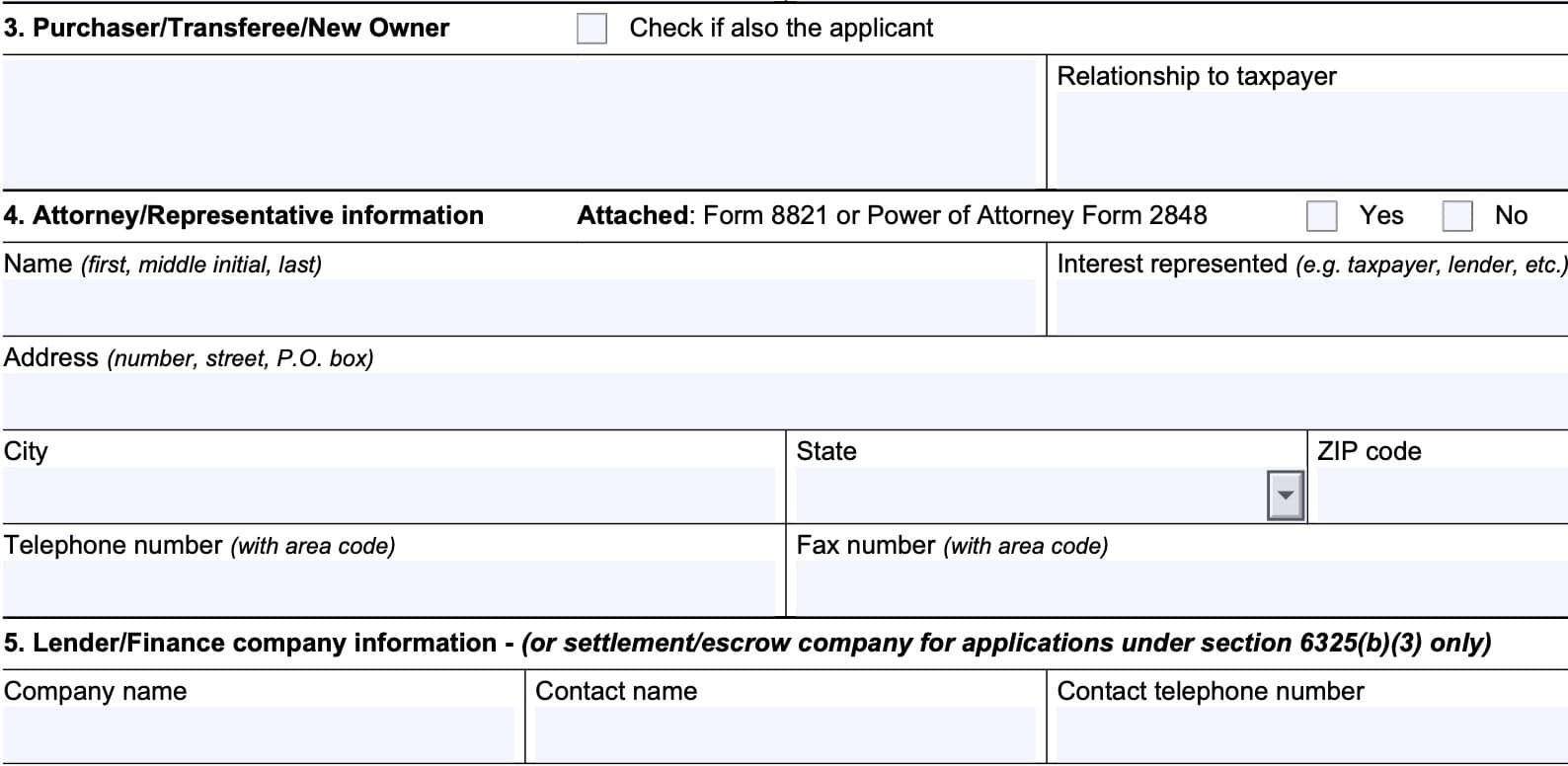

Line 3: Purchase/Transferee/New Owner

Check the box if you are also the applicant. If not, enter the name and relationship to the taxpayer.

Line 4: Attorney/Representative Information

If you’ve authorized someone access to your tax information on IRS Form 8821, or designated a power attorney using IRS Form 2848, select “Yes” and attach a copy of that form to this request and complete the rest of the field.

Otherwise, enter “No” and move on to Line 5.

Line 5: Lender/Finance Company Information

Enter the company name, as well as the contact information for the financial institution, mortgage lender, or other finance company involved in the potential transaction.

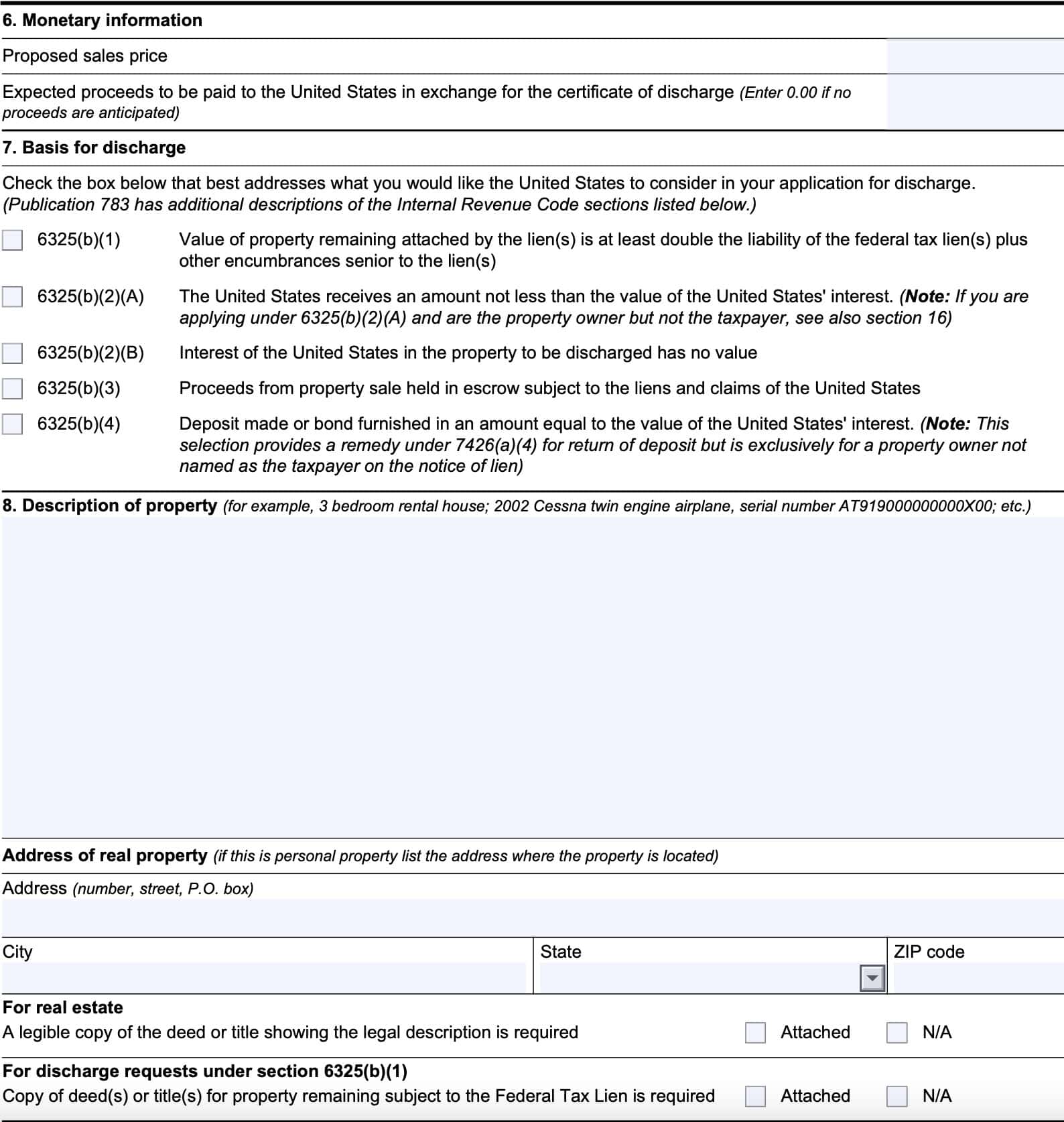

Line 6: Monetary information

Enter the proposed sales price, as well as expected proceeds of the sale that the U.S. government would receive at that sale price. If there are no expected proceeds due the federal government, enter N/A.

Line 7: Basis for discharge

Select the discharge basis that best suits your tax situation.

- IRC Section 6325(b)(1): Value of property remaining attached by the lien(s) is at least double the liability of the federal tax lien(s) plus other encumbrances senior to the lien(s)

- IRC Section 6325(b)(2)(A): The United States receives an amount not less than the value of the United States’ interest.

- Note: If you are applying under IRC 6325(b)(2)(A) and are the property owner but not the taxpayer, see also Section 16-Waiver.

- IRC Section 6325(b)(2)(B): Interest of the United States in the property to be discharged has no value.

- IRC Section 6325(b)(3): Proceeds from property sale held in escrow subject to the liens and claims of the United States.

- IRC Section 6325(b)(4): Deposit made or bond furnished in an amount equal to the value of the United States’ interest.

- Note: This selection provides a remedy under IRC 7426(a)(4) for return of deposit but is exclusively for a property owner not named as the taxpayer on the lien

Should the federal government disagree with your selection, the response letter will contain a detailed explanation.

Line 8: Description of property

Provide an accurate description of the property at hand.

For real estate, include the type of property. For example, 3-bedroom house; etc. Also list the property address.

When the property is personal property, include serial or vehicle numbers, as appropriate. For example, 2002 Cessna twin engine airplane, serial number AT919000000000X00; etc.

Attach a copy of the deed, if you have one, and select the appropriate box. If applying under IRC 6325(b)(1), check the “Attached” box. Attach copies of the titles or deeds for remaining property subject to the lien.

If you are not applying under 6325(b)(1), check the “NA” box.

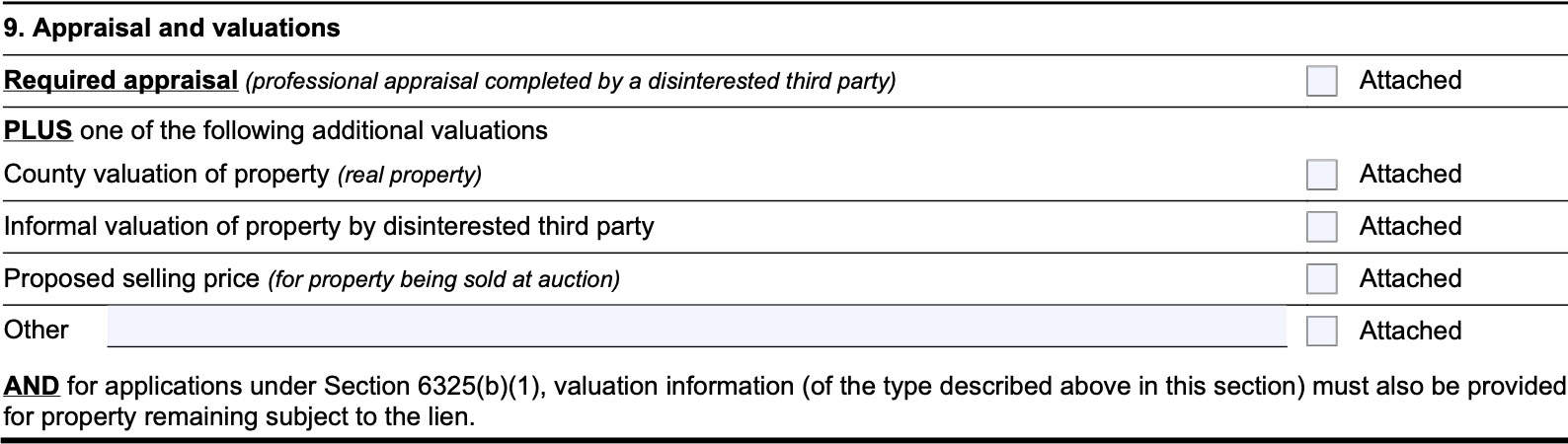

Line 9: Appraisal and valuations

If you have attached the required appraisal by a disinterested third party, check the “attached” box. This usually is a professional appraisal that provides:

- Neighborhood analysis

- Site description

- Description of the improvements

- Cost approach

- Comparable sales

- Definition of market value;

- Certification

- Contingent and limiting conditions

- Interior and exterior photos of the property

- Exterior photos of comparable sales used

- Comparable sales location map;

- Sketch of subject property showing room layout

- Flood map

- Appraiser’s qualifications

Also check the appropriate box when attaching one of the other required valuations:

- County valuation of property (for real property)

- Informal valuation of property by disinterested third party

- Proposed selling price, if being sold at auction

- Other approved valuation

Finally, for applications under Section 6325(b)(1), valuation information (of the type described above in this section) must also be provided for property remaining subject to the lien.

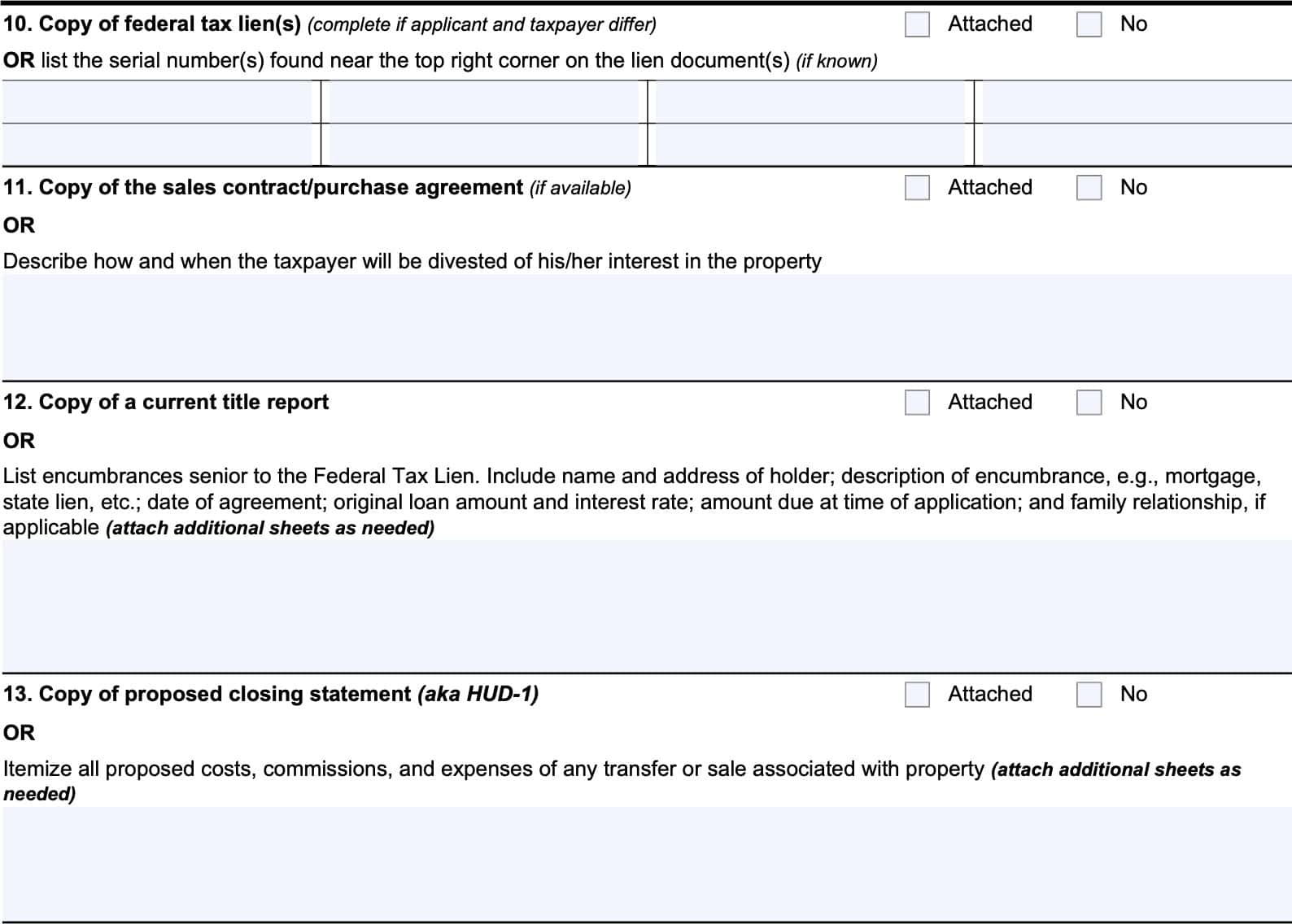

Line 10: Copy of Federal Tax Lien(s)

List the lien number(s) of any applicable federal tax lien or liens. Check the ‘Attached’ box if you’ve attached a copy. If you do not know the lien number, state, “Unknown.”

Line 11: Copy of sales contract/purchase agreement

Attach a copy of the purchase agreement. Also describe how the taxpayer named on the lien will be divested of their interest in the property or why they have no interest in the property.

Line 12: Copy of title report

Attach a copy of the title report. If you cannot, check ‘No” and use the provided space to list any liens or claims against the property and whether those claims are senior to the United States’ lien interest.

Include:

- Name and address of the lien holder

- Description of the claim

- Date of agreement

- Original loan and interest rate

- Amount due at application

- Whether there was a family relationship

Line 13: Copy of proposed closing statement

Select the ‘attached’ box if you plan to send a draft copy of the closing statement.

Otherwise, use the space provided to itemize all proposed costs, commissions, and expenses to refinance the property.

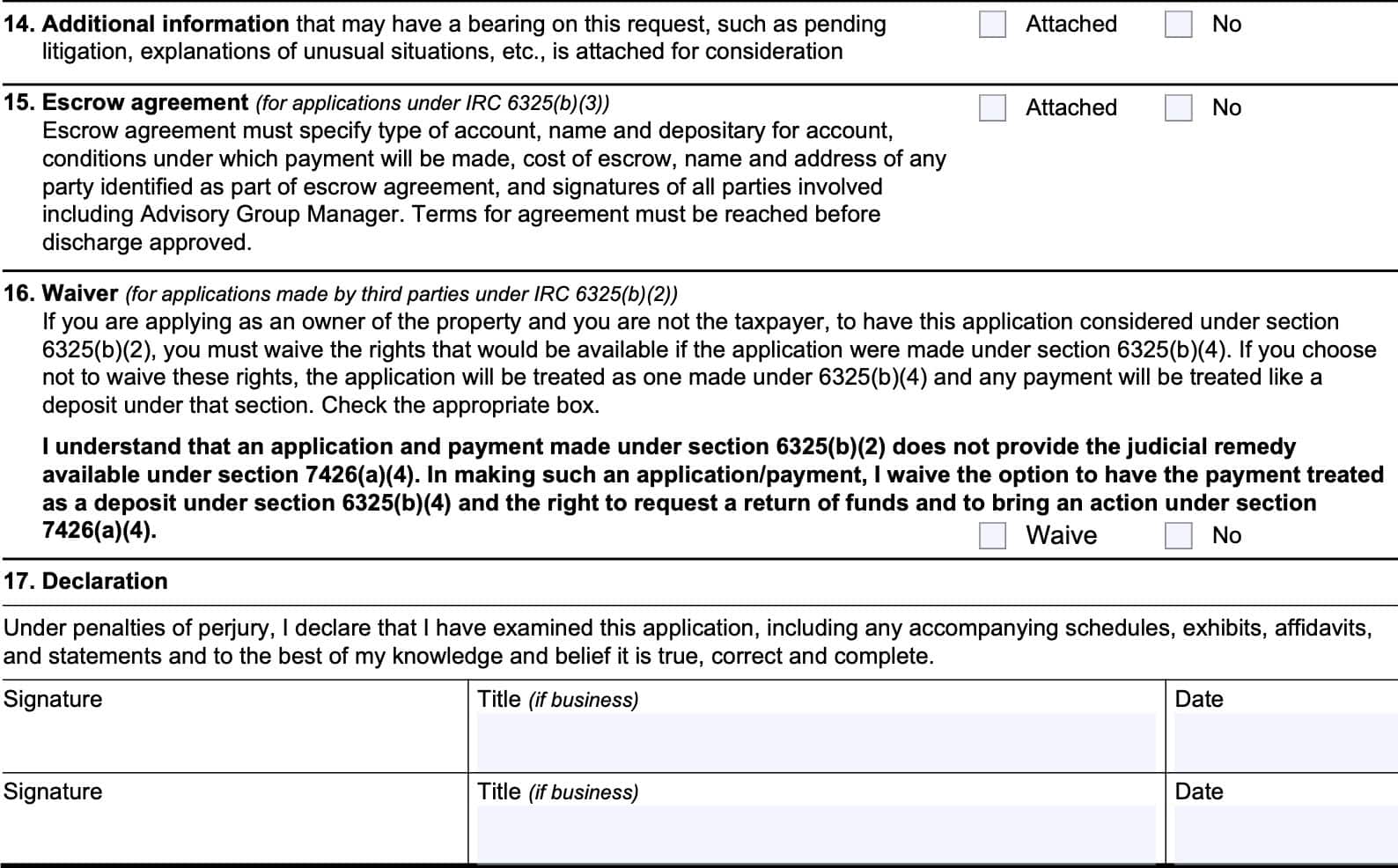

Line 14: Additional information

If there is additional information, select “Yes” and attach to this form. Additional information might include one or more of the following:

- Pending litigation

- Written explanation of extenuating circumstances

- Affidavits

- Court documents

- Other legal documents

Line 15: Escrow agreement

This only pertains to applications under Section 6325(b)(3). If attaching an escrow agreement, it must contain:

- Type of escrow account

- Name and depositary for account

- Conditions under which payment will be made

- Escrow costs

- Name and address of all parties identified in the escrow agreement

Line 16: Waiver

This part applies only under the following circumstances:

- You are filing IRS Form 14135 under IRC Section 6325(b)(2)(A)

- You are the property owner, but not liable for the underlying tax debt

By checking the “Waive” box you are waiving the option to have the payment treated as a deposit under Section 6325(b)(4), which has the accompanying right to request a return of funds and to bring an action under Section 7426(a)(4).

If you check the “no” box, your application will automatically be considered under 6325(b)(4) which provides for return of deposited funds and a court challenge under IRC Section 7426(b)(4).

Line 17: Declaration

In Line 17, you (and your spouse, if applicable) will sign and date the form. Please note that this attestation is made under the penalty of perjury.

Ways that a taxpayer may get rid of a federal tax lien

According to the Internal Revenue Service, the best way to completely rid yourself of a federal tax lien is to completely pay off your IRS debt. The IRS website states that an IRS lien release occurs within 30 days of full payment of all federal taxes, plus any tax penalties and interest.

However, the IRS recognizes certain instances where it might be in the best interest of the taxpayer and the federal government to reduce the impact of a tax lien if a federal lien release is not feasible. There are three alternative options that the IRS offers, provided that they serve the best interests of both the government and the taxpayer.

Withdrawal of a tax lien

IRC Section 6323(j) states that the federal government may withdraw notice of a federal tax lien under one or more of the following circumstances:

- The IRS or the Treasury Secretary determines that the lien notice was premature or otherwise not filed according to established procedures

- The taxpayer has entered into a direct debit installment agreement with the IRS

- Withdrawal of the lien notice will actually facilitate collection of the tax, or

- With the consent of the Taxpayer Advocate or at the Taxpayer Advocate’s recommendation that a tax lien withdrawal would be in the federal government’s best interest

We’ve written extensively on how to obtain a tax lien withdrawal by filing IRS Form 12277.

Subordination of a tax lien

Federal law allows the IRS to subordinate their tax lien so that another creditor may move ahead of the IRS in position. This may be particularly helpful for taxpayers who are looking to refinance their mortgage, but have been consistently paying their tax debt.

IRC Section 6325(d) states that the federal government may subordinate a federal tax lien under one of the following circumstances:

- The taxpayer has made an additional payment equal to the amount of the lien or interest to which the certificate subordinates the lien of the United States

- The federal government believes that subordinating the tax lien will help the taxpayer continue to pay down their tax liability

IRS Publication 784 contains additional information on how a taxpayer may request tax lien subordination. Additionally, we’ve written an extensive guide on how to use IRS Form 14134 to obtain a certification of subordination of federal tax lien.

Discharge of property

A tax lien discharge does not absolve the taxpayer of the unpaid back taxes they still owe. However, it removes the government’s legal claim to the property from the taxpayer’s property itself.

A lien discharge might be a good idea for taxpayers with a lien on real property, such as a primary residence, that they are trying to refinance. Another situation might be when trying to replace personal property, such as a car, but the lien prevents the taxpayer from doing so.

However, the IRS website indicates that a discharge of property might be the best option if you are trying to sell the property, while subordination might be a better option for refinancing.

When might I be able to obtain a certificate of discharge of property from a tax lien?

Internal Revenue Code Section 6325(b) authorizes the discharge of property secured by a federal tax lien under one of the following circumstances:

- Fair market value of the property secured by the lien is at least twice the amount of the lien and all other debts associated with the property

- Most applicable to real property in a rising real estate market

- Lien has been partially satisfied, and/or the federal government determines that their interest in the specific piece of property has no value

- The property is sold and the available funds are held in a separate account that the U.S. government has the same priority over the funds as with the property

- Taxpayer either:

- Makes a payment equivalent to the amount secured by the lien

- Furnishes a bond acceptable to the federal government for the amount secured by the lien

Let’s further discuss how to use Form 14135 to obtain a certificate of discharge of property.

Five ways the government can grant lien discharge

There are five references of the federal law under which the IRS can grant lien subordination:

- IRC 6325(b)(1): a discharge may be issued under this section if the value of the taxpayer’s remaining property encumbered by the federal tax lien is equal to at least twice the amount of the federal tax liability secured by the lien and any encumbrance entered into before the IRS filed its public notice of the lien

- IRC 6325(b)(2)(A): a discharge may be issued under this provision when the tax liability is partially satisfied with an amount paid that is not less than the value of the United States’ interest in the property being discharged.

- IRC 6325(b)(2)(B): a discharge may be issued under this provision when it is determined that the government’s interest in the property has no value.

- IRC 6325(b)(3): a discharge may be issued under this provision if an agreement is reached with the IRS allowing the property to be sold.

- IRC 6325(b)(4): an IRS tax lien discharge will be issued under this provision to a third party who owns the property if a deposit is made or an acceptable bond provided equal to the government’s lien interest in the property.

Technically, the IRS may discharge an estate tax lien under Internal Revenue Code Section 6325(c). However, the taxpayer must submit IRS Form 4422, which is outside the scope of this article.

Video walkthrough

Watch this instructional video for step by step guidance on completing Form 14135.

Frequently asked questions

The IRS will issue a discharge certificate when it determines that it is in the government’s interest to do so. Discharging a property secured by a tax lien might make sense when the taxpayer may be able to resolve their tax problems through the sale of the property.

IRS Form 14135, Application for Certificate of Discharge of Property from Federal Tax Lien, is the tax form that a taxpayer might use when requesting that a specific property be removed from a tax lien. Obtaining an IRS lien discharge certificate might be the preferred approach for individual taxpayers looking to sell their property. In most cases, sale of property will be contingent on obtaining a discharge certificate.

Where can I find IRS Form 14135?

You may obtain a copy of IRS Form 14135 as a PDF file from the IRS website or by downloading a copy below.