IRS Form 8853 Instructions

How do I complete IRS Form 8853?

There are three sections to this tax form:

- Section A: Archer MSAs

- Section B: Medicare Advantage MSA Distributions

- Section C: Long-term Care Insurance Contracts

You should complete all applicable fields, but most taxpayers will complete only one. We’ll go through each section in order.

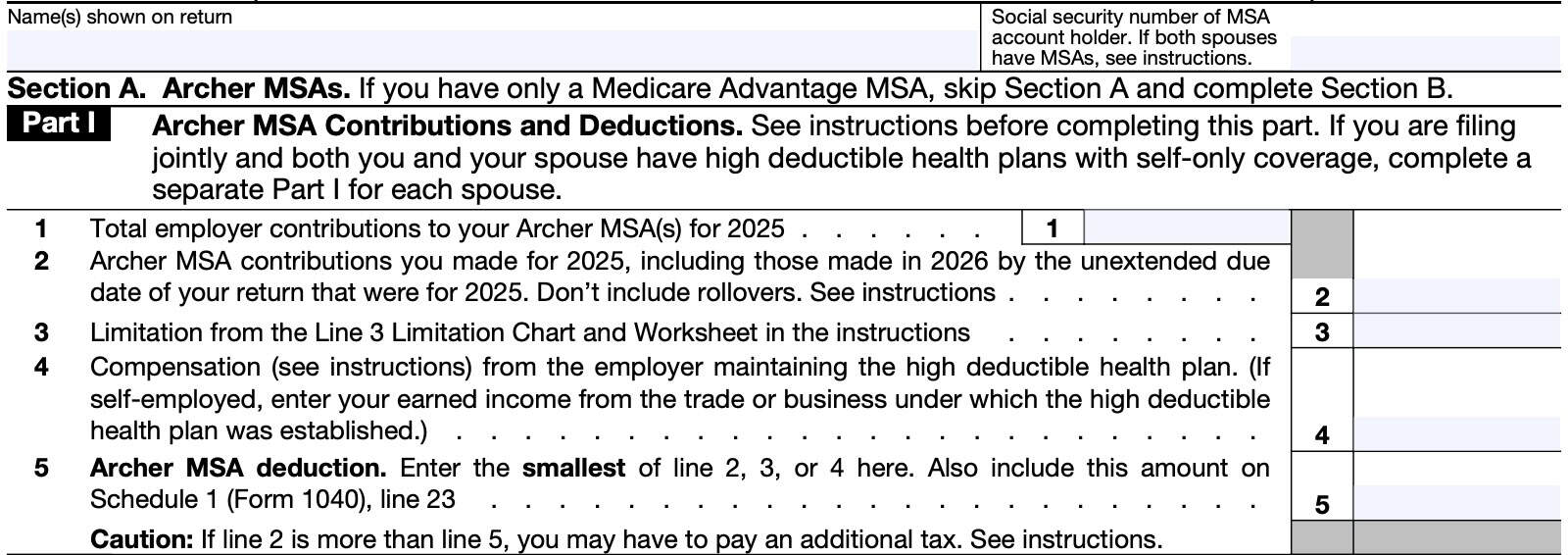

Section A: Archer MSAs

There are two parts to Section A:

- Part I: Archer Medical Savings Accounts contributions and deductions

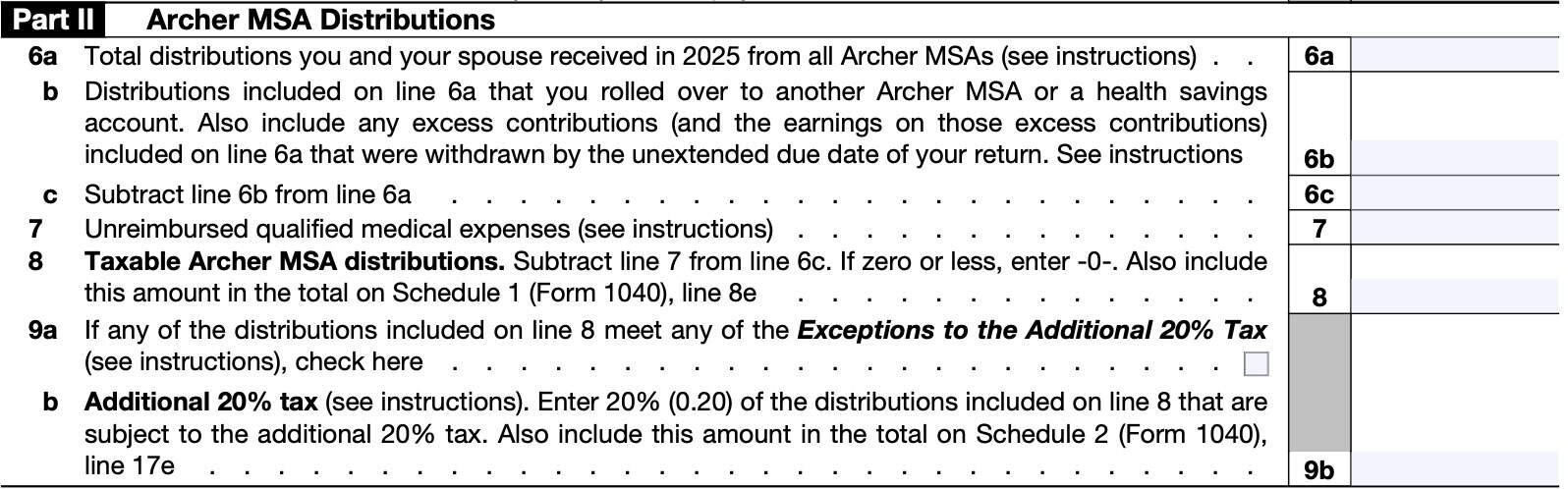

- Part II: Archer MSA distributions

We’ll start with Line 1.

Line 1: Total employer contributions

Enter the total employer contributions made for you or your spouse for the given tax year for any Archer MSA.

You should see these contributions in Box 12 of Form W-2 with code R.

Line 2: Archer MSA contributions that you made during the tax year

Enter the total contributions you made to your Archer MSA in the tax year. Also include those contributions made from January 1 of the following tax year through the tax filing deadline.

For example, a taxpayer would include contributions made from January 1, 2026, through April 18, 2026, that were for 2025.

Note: If your employer made contributions (Line 1), and the number in Line 2 is not zero, you may have an excess contribution (see below).

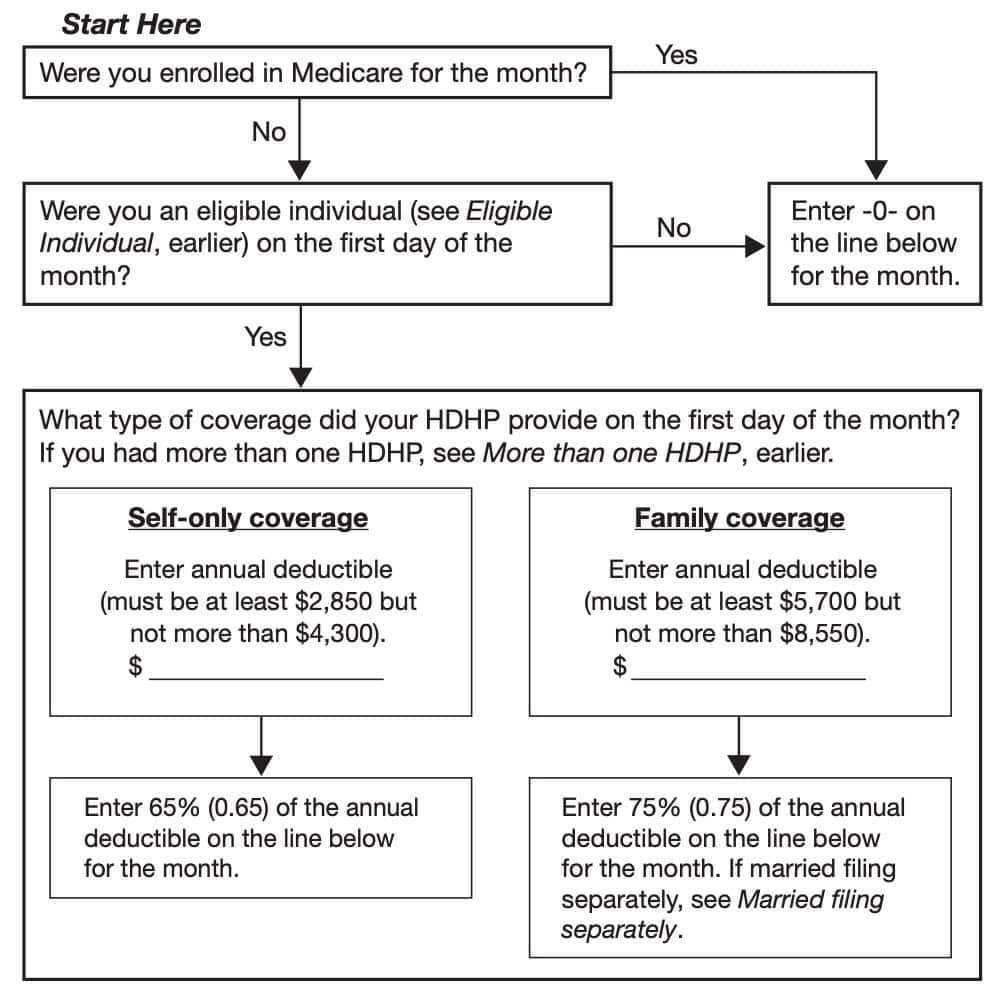

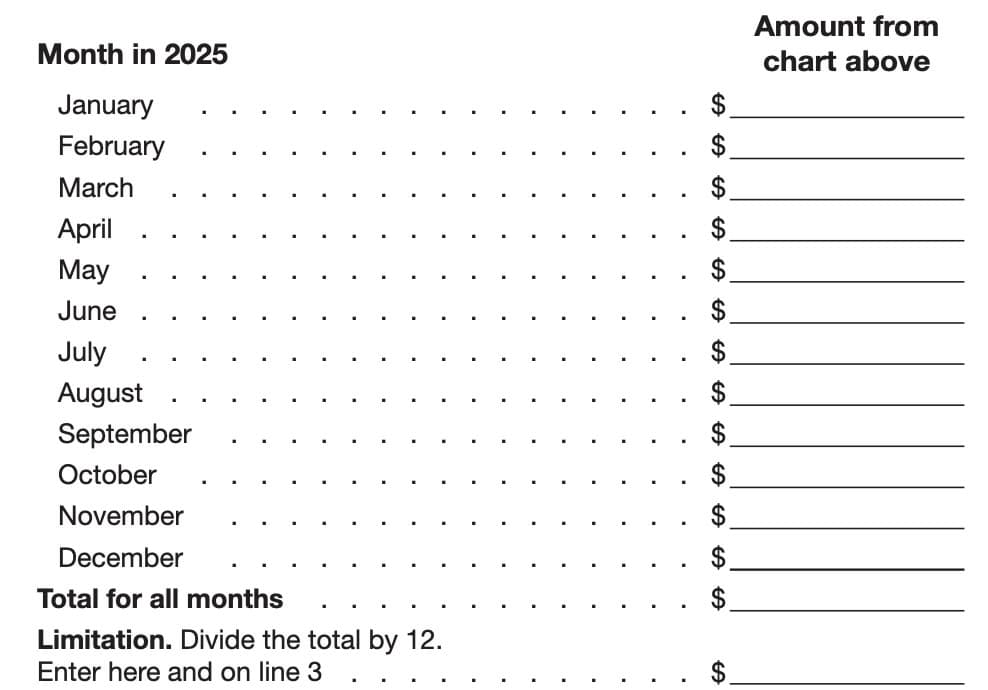

Line 3: Limitations

To calculate your contribution limitations, you must use the limitation chart and worksheet located in the form instructions (see below).

For each month, enter the appropriate amount, as determined by the chart. Combine all monthly totals, then divide this number by 12.

Enter the result on Line 3.

At the time of this update, the most current version of IRS Form 8853 was for the 2025 tax year. For the 2026 tax year, you should use the following figures:

| Self-only coverage | Family coverage | |

| Minimum annual deductible | $2,850 | $5,700 |

| Maximum annual deductible | $4,300 | $8,550 |

Line 4: Compensation

Compensation reported on Form W-2 includes the following:

- Wages & salaries

- Professional fees

- Other pay you receive for services you perform

- Sales commissions

- Commissions on insurance premiums

- Pay based on a percentage of profits, tips, and bonuses

Compensation also includes:

- Net earnings from self-employment

- Only for a trade or business in which your personal services are a material income-producing factor.

This is your income from self-employment minus expenses, which include the deductible part of self-employment tax.

Line 5: Archer MSA deduction

Enter the smallest of:

- Line 2

- Line 3

- Line 4

Carry this number over to Schedule 1, Line 23.

Excess contributions

To figure your excess contributions, subtract Line 5 from Line 2.

However, you can withdraw some or all of your excess contributions for the prior tax year, and they will be treated as if they hadn’t been contributed if:

- You make the withdrawal by the due date, including extensions, of your federal income tax return

- You don’t claim a deduction for the amount of the withdrawn contributions; and

- You also withdraw any income earned on the withdrawn contributions and include the earnings in “Other income” on your tax return for the year you withdraw the contributions and earnings

For employer excess contributions, if the excess wasn’t included in income on Form W-2, you must report it as “Other income” on your individual tax return. You can withdraw some or all of the excess employer contributions without penalty by following the guidelines for excess contributions, above.

Line 6: Total distributions

In Line 6a, include all distributions you and your spouse received in the tax year from all Archer medical savings accounts, as reported in Box 1 of Form 1099-SA.

In Line 6b, include all rollovers from an Archer MSA to another Archer MSA or HSA. This is generally considered a tax-free withdrawal, if performed correctly. Since improperly conducted rollovers can have significant tax consequences, you should refer to the form instructions for additional guidance or talk to your tax advisor.

For Line 6c, subtract Line 6b from Line 6a.

Line 7: Unreimbursed qualified medical expenses

In Line 7, include all Archer MSA distributions that were used for qualified medical expenses for household members, to include:

- Yourself

- Your spouse

- Dependents

- Someone who could be considered your dependent, but are not because of one or more of the following:

- The person filed a joint return

- The person had gross income of $5,200 or more

- You, or your spouse if filing jointly, are dependents of someone else

If you itemize your tax deductions on Schedule A, you cannot include the same medical expenses on both Schedule A and Form 8853, even though they may be tax deductible.

Line 8: Taxable Archer MSA distributions

Subtract Line 7 from Line 6c. If the number is zero or less, enter ‘0.’ Any positive number represents your taxable distribution. Enter this number on Schedule 1, Line 8e.

Line 9

In Line 9a, check the box if any distributions on Line 8 meet the criteria for exceptions to the additional 20% tax.

Exceptions to the additional 20% tax include distributions made after the account holder:

- Dies

- Becomes disabled

- Turns age 65

In Line 9b, multiply 20% by any amount included on Line 8 that does not meet the exceptions to the additional 20% tax. Include this number on Schedule 2, Line 17e.

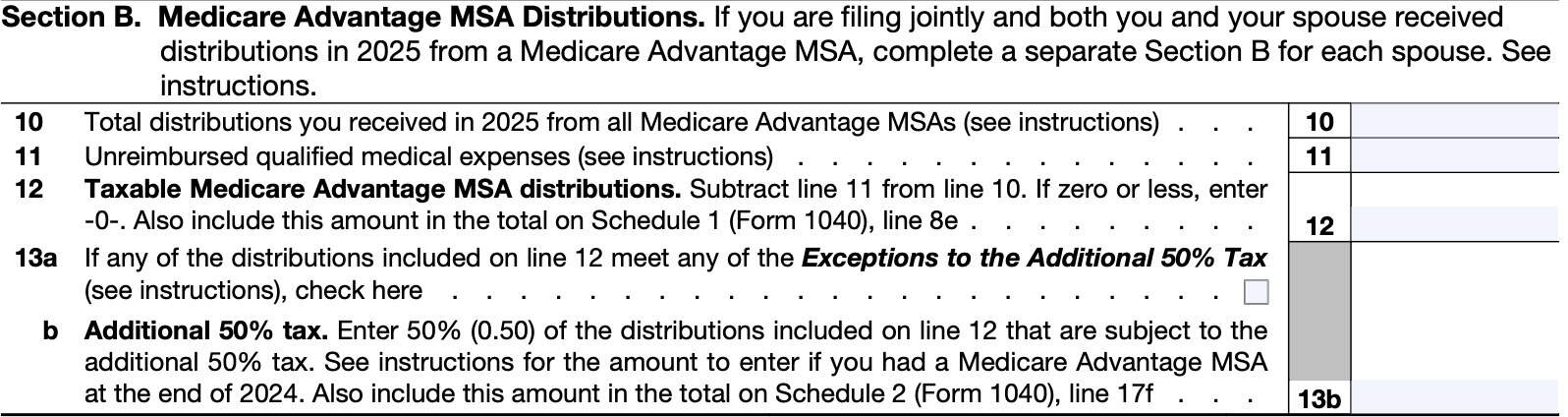

Section B: Medicare Advantage MSA Distributions

Complete Section B if you (or your spouse, if filing jointly) received distributions from any Medicare Advantage medical savings accounts in the current taxable year.

If both you and your spouse received distributions, you will need to:

- Complete Form 8853, Section B for each spouse

- Enter “Statement” across the top of each Section B

- Fill in the name and Social Security number for each spouse

- Add the totals of Lines 10-13b on each form and enter the combined total into the combined Form 8853

Line 10: Total Medicare Advantage MSA distributions

Enter the total distributions you received in the tax year from all Medicare Advantage MSAs. These amounts should be shown in Box 1 of IRS Form 1099-SA.

Line 11: Unreimbursed qualified medical expenses

Enter the total Medicare Advantage MSA distributions used for qualified medical expenses. If you itemize tax deductions, you cannot include the medical expenses on both Form 8853 and Schedule A.

You must select one or the other. Generally, including medical expenses on Form 8853 is more tax-efficient, but you should consult with your tax professional about your specific tax situation.

Line 12: Taxable Medicare Advantage MSA distributions

Subtract Line 11 from Line 10. If the number is zero or less, enter ‘0.’ Any positive number represents your taxable distribution. Enter this number on Schedule 1, Line 8e.

Line 13

In Line 13a, check the box if any distributions on Line 12 meet the criteria for exceptions to the additional 50% tax.

Exceptions to the additional 50% tax include distributions made after the account holder:

- Dies

- Becomes disabled

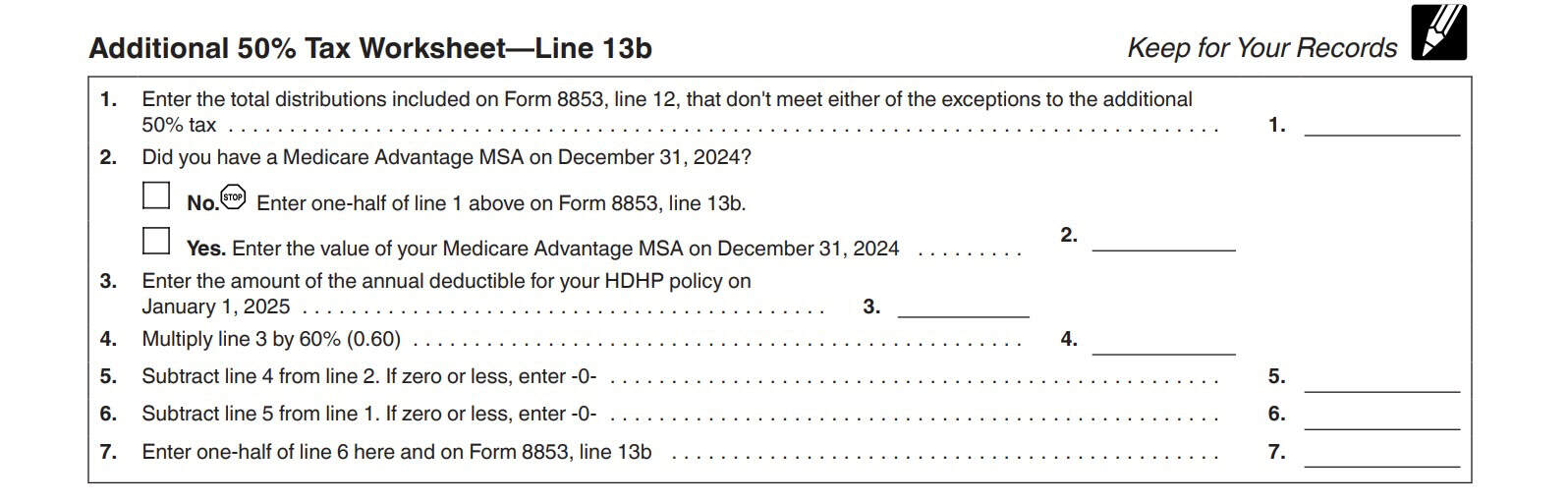

In Line 13b, multiply 50% by any amount included on Line 12 that does not meet the exceptions to the additional 50% tax. Include this number on Schedule 2, Line 17f.

Use the Additional 50% Tax Worksheet located in the Form 8853 instructions to assist in this calculation.

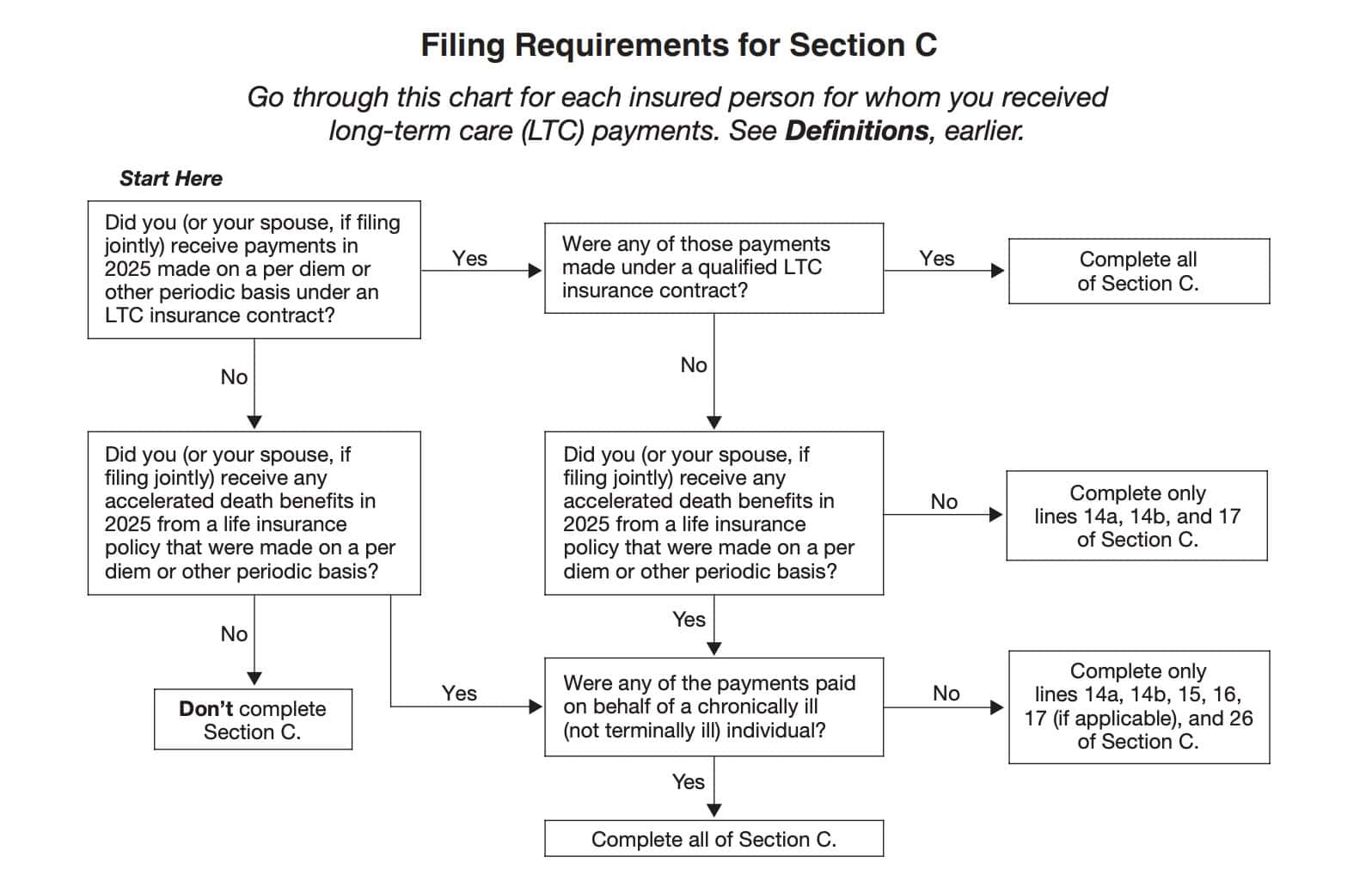

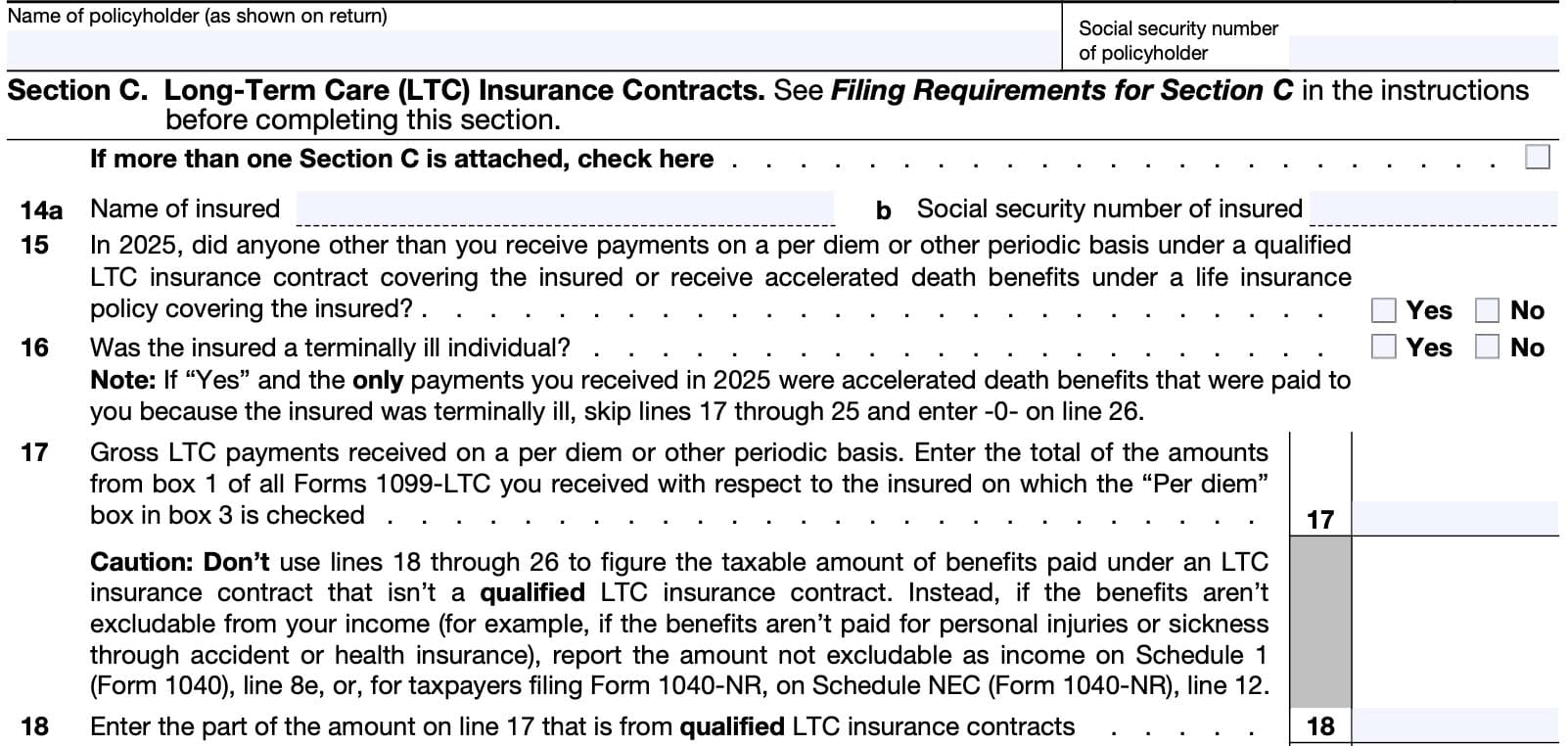

Section C: Long-Term Care (LTC) Insurance Contracts

The IRS form instructions contain a flowchart to help taxpayers determine whether they need to complete Section C. To help you determine whether you should complete Section C, this flowchart is provided below.

Before entering any information in Lines 14-26, be sure to include the name and SSN of the policyholder as shown on the tax return.

Line 14

Enter the name (Line 14a) and Social Security number (Line 14b) of the insured.

Line 15

If anyone other than the taxpayer received payments on a per diem basis or other periodic basis under a qualified LTC insurance contract, check “Yes.” Otherwise, check “No.”

If there are multiple payees for the mentioned long-term care insurance benefits, you should refer to the form instructions for additional details.

Line 16

Was the insured a terminally ill person? If yes, check the terminally ill box. If you check “Yes,” and the only payments that you received were accelerated death benefits paid because the person was terminally ill, skip Lines 17 through 25 and enter ‘0’ on Line 26.

Otherwise, proceed to Line 17.

Line 17: Gross LTC payments

Enter the total reported on Box 1 for all Forms 1099-LTC regarding the insured for which the ‘per diem’ box in Box 3 is checked.

Line 18: Gross LTC payments from qualified insurance contracts

From Line 17, enter the amount of payments that came from qualified LTC contracts.

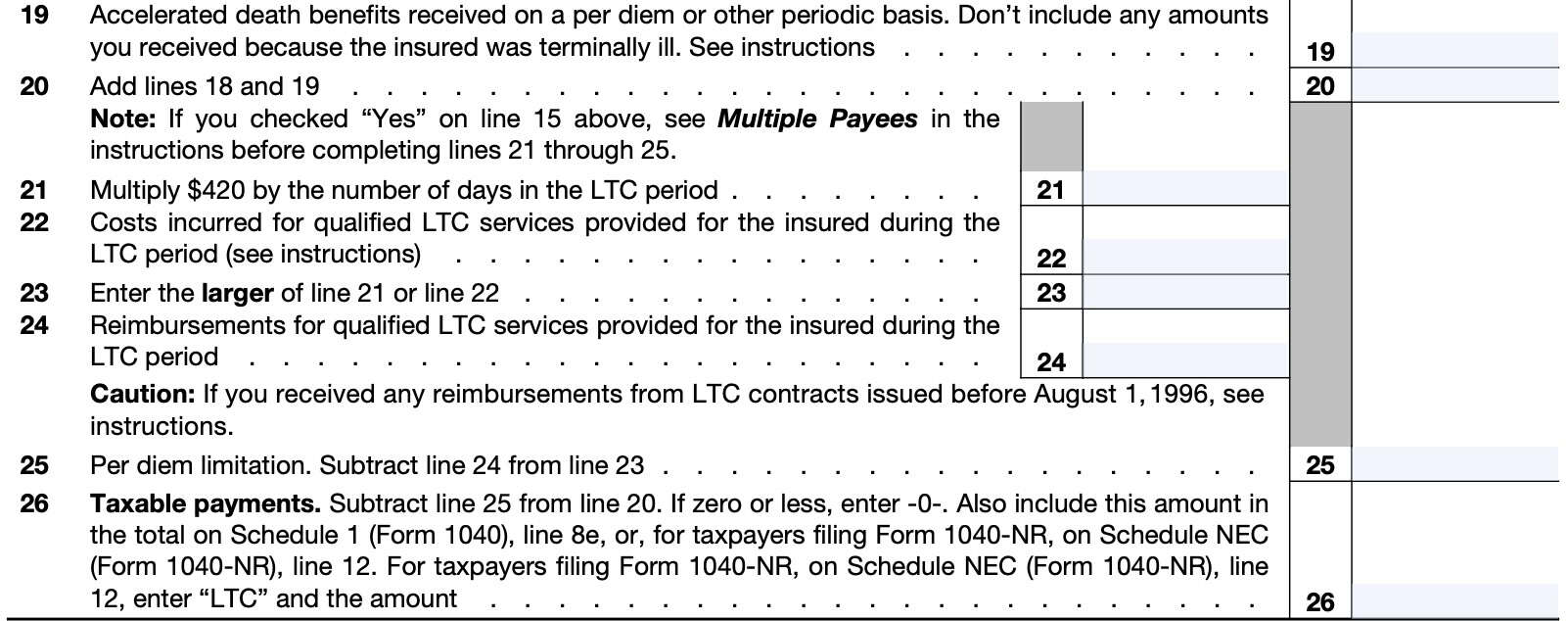

Line 19: Accelerated death benefits received on a per diem or other periodic basis

Enter the total accelerated death benefits you received with respect to the insured listed on Line 14a. These amounts are generally shown in Box 2 of Form 1099-LTC.

Include only amounts you received while the insured was a chronically ill individual. Don’t include amounts you received while the insured was a terminally ill individual.

Chronically ill individual vs. terminally ill individual

According to the form instructions, a chronically ill individual is someone who has been certified by a licensed health care practitioner as:

- Being unable to perform at least two activities of daily living (ADL) without substantial assistance from another individual due to a loss of functional capacity

- ADLs include the following:

- Eating

- Toileting

- Transferring

- Bathing

- Dressing

- Continence

- Must be for at least 90 days

- ADLs include the following:

- Requiring substantial supervision to protect the individual from threats to health and safety due to severe cognitive impairment.

An individual must have been certified within the past 12 months as meeting this condition. Additionally, the individual must be re-certified every 12 months.

Conversely, a terminally ill individual is any individual who has been certified by a physician as having an illness or physical condition that can reasonably be expected to result in death within 24 months of the date of certification.

Line 20

Add Lines 18 and 19. Enter the total in Line 20.

Line 21

Multiply the number of days in the LTC period by $420.

Line 22: Costs incurred for qualified LTC services for the insured during the LTC period

Qualified LTC services are the following necessary services required to treat a chronically ill individual who is under a plan of care as prescribed by a licensed health care professional:

- Diagnostic

- Preventive

- Therapeutic

- Curing

- Treating

- Mitigating

- Rehabilitative

- Maintenance

- Personal care

Line 23

Enter the larger of:

- Line 21

- Line 22

Line 24: Reimbursements for qualified LTC services provided during the LTC period

Enter the reimbursements you received or expect to receive through insurance or otherwise for qualified LTC services provided for the insured for LTC periods in the tax year.

Box 3 of Form 1099-LTC should indicate if payments were made on a reimbursement basis.

Line 25: Per diem limitation

Subtract Line 24 from Line 23.

Line 26: Taxable payments

Subtract Line 25 from Line 20. If zero or less, enter ‘0.’

If Line 26 results in a positive number, enter this number on one of the following, as applicable:

- Schedule 1 (Form 1040), Line 8e

- Schedule NEC, (Form 1040-NR)

- Enter “LTC” and the amount

What is an Archer MSA?

IRS Publication 969, Health Savings Accounts and Other Tax-Favored Health Plans, defines the Archer MSA as a tax-exempt trust or custodial account that you set up with a U.S. financial institution (such as a bank or an insurance company) in which you can save money exclusively for future medical expenses.

The publication goes on to cite the following tax benefits of an Archer MSA:

- You can claim a tax deduction for contributions you make even if you don’t itemize your deductions on Schedule A

- The interest or other earnings on the assets within an Archer MSA are tax-free

- Distributions may be tax free if you pay qualified medical expenses

- Generally, qualified medical expenses are unreimbursed medical expenses that could otherwise be deducted on Schedule A of your income tax return

- Insurance premiums are not considered qualified medical expenses unless they are for one of the following:

- Long-term care insurance policy

- Health care continuation coverage

- Health care coverage while receiving unemployment compensation under federal or state law.

- The contributions remain in your Archer MSA from year to year until you use them

- An Archer MSA is ‘portable,’ so it stays with you if you change employers or leave the work force

In other words, these benefits sound almost exactly like what you would see for a health savings account (HSA). In fact, these benefits are listed identically in the IRS publication for both HSAs and Archer MSAs!

So that begs the obvious question…

Why did HSAs replace Archer MSAs?

Simply put, they’re more user-friendly. In contrast to an Archer MSA, HSAs have:

- Higher contribution limits

- More employers are eligible to participate

- Archer MSAs were only open to self-employed individuals and businesses with 50 or fewer employees

- HSAs allow both employers and employees to contribute to the account each year, subject to the annual contribution limit

- Archer MSAs only allow one or the other, but not both

However, the primary drawback of HSAs is the requirement to maintain their health insurance through a high deductible health plan, or HDHP, in order to contribute to the account each year. This precludes taxpayers who register for Medicare.

This tiny loophole is one big reason why Archer MSAs are still around. Specifically, a form of MSA known as the Medicare Advantage MSA.

What is a Medicare Advantage MSA?

IRS Publication 969 states that a Medicare Advantage MSA (MA MSA) is “an Archer MSA designated by Medicare to be used solely to pay the qualified medical expenses of the account holder.” To qualify for a Medicare Advantage MSA, an account holder must:

- Be enrolled in Medicare

- Have an HDHP that meets the Medicare guidelines

Contrary to an HSA, which precludes all health plans that are not an HDHP, a Medicare Advantage MSA specifically allows the enrollee to participate in both Medicare and a qualifying HDHP. However, this requirement does preclude certain taxpayers who might receive health care outside of an HDHP, such as:

- Veterans or retired military who receive benefits through TRICARE or the Department of Veterans Affairs

- Medicaid recipients

- Retired federal employees who receive health care through Federal Employees Health Benefits Program (FEHBP)

- People with outside coverage through their employer

The Medicare website contains additional information on MA MSAs. This includes a full list of requirements for joining a Medicare Advantage MSA.

Now, let’s turn our focus to the tax form itself.

What is IRS Form 8853?

IRS Form 8853, Archer MSAs and Long-Term Care Insurance Contracts, is the tax form that taxpayers can use to report transactions within their Archer MSA or Medicare Advantage MSA. This includes:

- Report Archer MSA contributions

- Including employer contributions to your Archer MSA account

- Calculate your Archer MSA deduction

- Report distributions from Archer MSAs or Medicare Advantage MSAs during the tax year

- Report taxable payments from long-term care (LTC) insurance contracts, or

- Report taxable accelerated death benefits from a life insurance policy

Video walkthrough

Watch this instructional video to learn how to go through Form 8853, step by step.

Are you tired of dreading tax season?

If you’re like most people, you push through the stress of filing, only to be hit with a bigger bill than expected—then put it all behind you until the same cycle repeats next year.

But what if you could change the game?

Tax planning puts you in control. It’s about being proactive, not reactive—taking small, smart steps throughout the year to reduce your tax burden, increase your savings, and keep more of your hard-earned money working for you.

Here’s what effective tax planning helps you do:

✅ Avoid the surprise of a high tax bill

✅ Understand how your income and decisions affect your taxes

✅ Strategically lower your tax liability over time

Ready to make smarter tax moves?

👉 Join my free weekly tax planning newsletter and get one actionable tip every week to help you reduce your taxes legally and effectively.

Start taking control—your future self will thank you.

Frequently asked questions

IRS Form 8853 is the tax form that taxpayers can use to report transactions within their Archer MSA or Medicare Advantage MSA. This includes:

According to the IRS, taxpayers must file Form 8853 if they:

-Made contributions to an Archer MSA (including employer contributions)

-Acquired an interest in an Archer MSA or Medicare Advantage MSA from a decedent

-Received payments under a long term care insurance contract or accelerated death benefits from a life insurance policy on a per diem basis in the tax year

-Received Archer MSA or Medicare Advantage MSA distributions in the tax year.

IRS Publication 969 states that a Medicare Advantage MSA (MA MSA) is “an Archer MSA designated by Medicare to be used solely to pay the qualified medical expenses of the account holder.”

Where can I find IRS Form 8853?

You can find IRS Form 8853, along with other free tax forms, on the Internal Revenue Service website. For your convenience, the most current version of this form is available below in PDF format.

Related tax articles

This tax form is one of the fillable tax forms provided by the Internal Revenue Service, to help taxpayers reduce their tax preparation costs. To see more forms like this, visit our free fillable tax forms page, where you’ll also find articles like this.

Unlike the IRS, our articles contain step by step instructions for each tax form, as well as video walkthroughs. You can also check out all of our videos by subscribing to our YouTube channel!