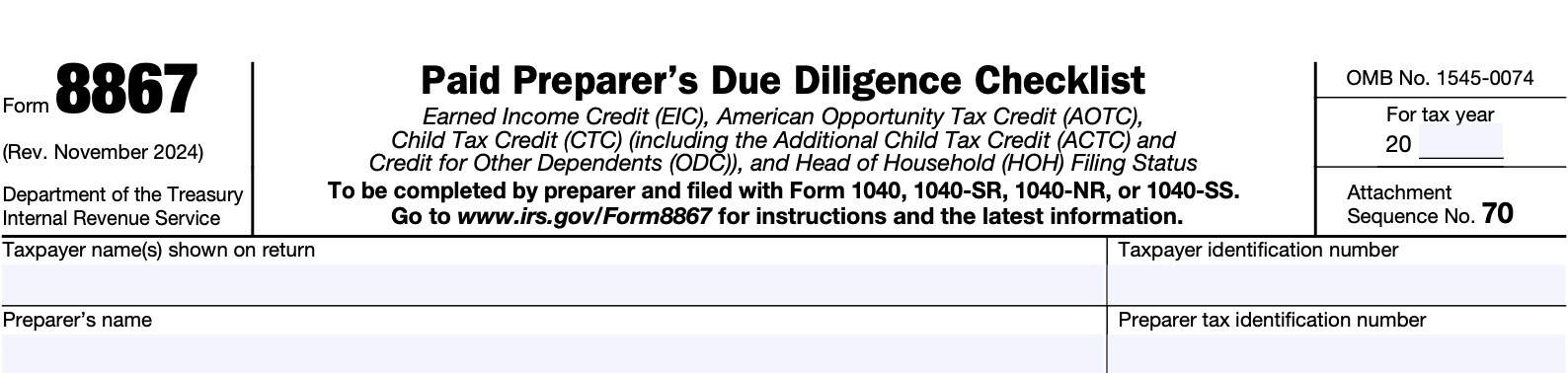

IRS Form 8867 Instructions

Because of fraudulent tax claims, the IRS has specific due diligence requirements for paid tax return preparers whose clients try to claim certain tax benefits. Part of these due diligence requirements involve filing IRS Form 8867, Paid Preparer’s Due Diligence Checklist, for taxpayers trying to claim any of the following:

- Earned income tax credit

- Child tax credit, including additional child tax credit or the credit for other dependents

- American Opportunity Tax Credit

- Head of household filing status

In this article, we’ll walk through everything you might need to know about IRS Form 8867, including:

- Step by step instructions your tax return preparer must follow

- Tax benefits impacted by IRS due diligence regulations

- Frequently asked questions

Let’s begin by going through IRS Form 8867, step by step.

Table of contents

IRS Form 8867 Instructions

IRS Form 8867 serves as a due diligence checklist for tax return preparers who need to ascertain a taxpayer’s eligibility for specific tax credits or for head-of-household filing status. Although most taxpayers will skip over this form when reviewing their income tax return, having a better understanding of these due-diligence questions might help produce more accurate tax returns.

In keeping with most articles on this site, this article will read as a set of instructions. Even if you’re not completing this tax form, this might help you to better understand why your tax return preparer can be particular about having sufficient information to claim a particular tax benefit.

Specifically, IRS Form 8867 covers due diligence requirements for the following:

- Earned income credit (EIC)

- American Opportunity Tax Credit (AOTC)

- Child Tax Credit (CTC)

- Additional Child Tax Credit (ACTC)

- Credit for Other Dependents (ODC)

- Head of household filing status (HOH)

There are 6 parts to this two-page tax form:

- Part I: Due Diligence Requirements

- Part II: Due Diligence Questions for Returns Claiming EIC

- Part III: Due Diligence Questions for Returns Claiming CTC/ACTC/ODC

- Part IV: Due Diligence Questions for Returns Claiming AOTC

- Part V: Due Diligence Questions for Claiming HOH

- Part VI: Eligibility Certification

Let’s start with the taxpayer information fields just above Part I.

Taxpayer information

You should see the following information:

- Tax year

- Taxpayer name(s) as shown on the federal tax return

- Taxpayer identification number

- Name of paid tax return preparer

- Preparer tax identification number (PTIN)

Everyone should review this information for accuracy. Let’s go to Part I.

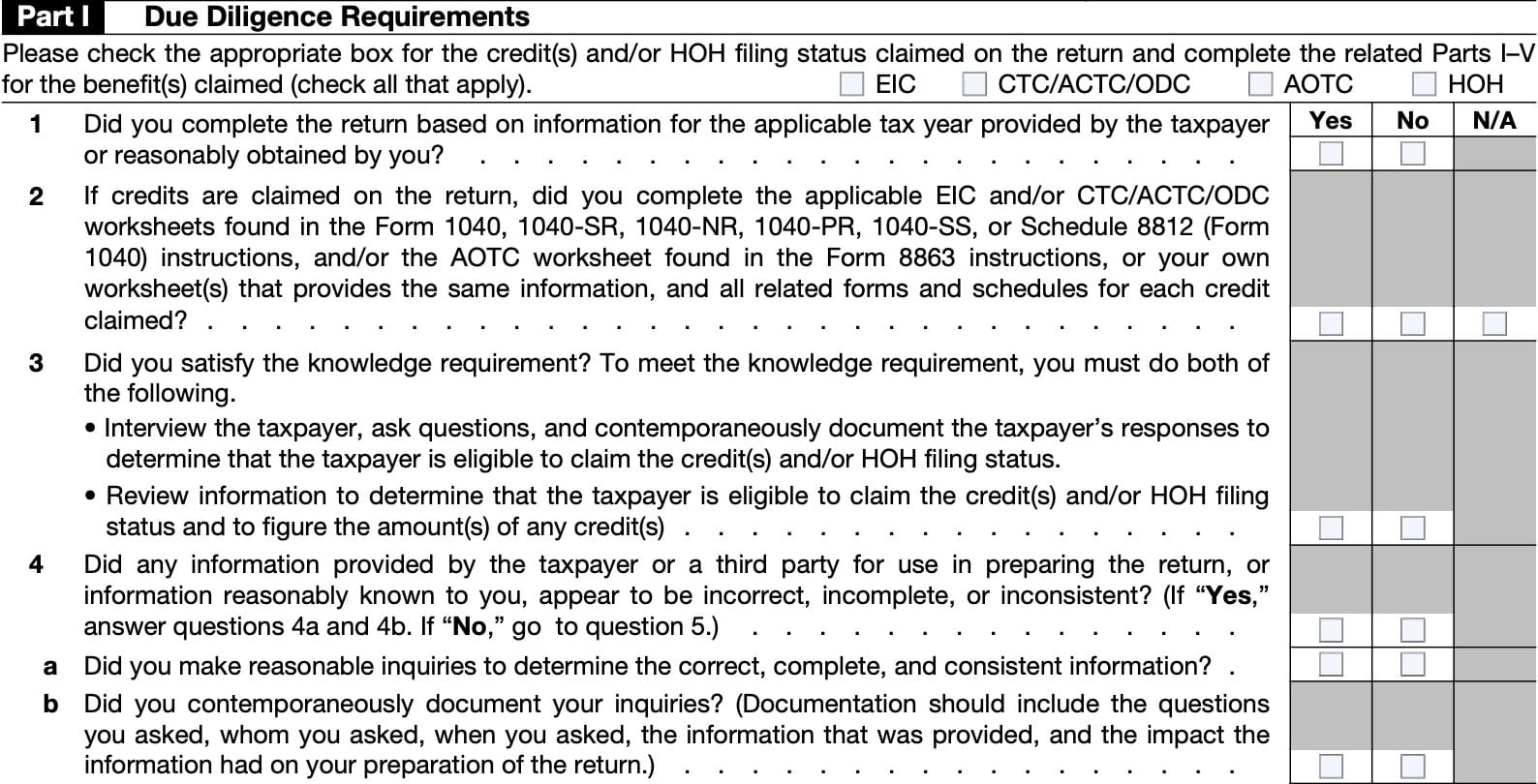

Part I: Due Diligence Requirements

In Part I, we’ll go over the due diligence rules that each paid tax return preparer must follow. All answers must be checked in the applicable box as one of the following:

- Yes

- No

- N/A (not applicable)

Let’s begin with the fields just above Question 1.

Above Question 1

You should see boxes for each of the tax credits and HOH filing status. The signing tax return preparer will have checked the appropriate box(es) and completed the corresponding parts of this tax form.

Question 1

Did you complete the return based on information for the applicable tax year provided by the taxpayer or reasonably obtained by you?

A tax return preparer should prepare the return based only on information related to the applicable tax year for which he or she is filing the return.

The information on Form 8867 should be for the year of the Form 1040, 1040-SR, 1040-NR, or 1040-SS that he or she is filing.

Election to use prior year earned income

Depending on the year, a client may be eligible to elect to use prior year earned income to figure the earned income tax credit (EIC) or American Opportunity Tax Credit (ACTC) if the client’s prior year income was more than the client’s earned income for the tax year being filed.

For a tax return in which the client properly elects to figure the EIC, ACTC, or both credits using prior earned income, the due diligence requirements set forth in Treasury Regulations apply to the preparer’s computation of earned income for 2 years.

The preparer’s computation of earned income for 2 years must include the following:

- The current tax year if the election requires that their prior tax year earned income be more than their current tax year earned income.

- The prior tax year to determine the earned income used to compute each credit claimed under the election.

If the taxpayer makes this election, answer “Yes” on Question 1. A preparer does not have to recompute the prior tax year earned income if the same preparer prepared that prior year tax return.

Question 2

If credits are claimed on the tax return, did you complete the applicable worksheets:

- EIC worksheet

- CTC/ACTC/ODC worksheets

- AOTC

Below is a brief summary of where each worksheet can be located.

EIC worksheet

For taxpayers making an EITC claim, you can find the appropriate EITC worksheet in the instructions for your applicable tax return:

- IRS Form 1040

- IRS Form 1040-SR

- IRS Form 1040-NR

- IRS Form 1040-SS

CTC/ACTC/ODC worksheets

Eligible taxpayers looking to claim one of these tax credits may find the appropriate worksheet in the Schedule 8812 instructions.

AOTC worksheet

For taxpayers looking to take the American Opportunity credit, you can find the AOTC worksheet in the IRS Form 8863 instructions.

Question 3

Did you satisfy the knowledge requirement?

IRS knowledge requirement

When determining a taxpayer’s eligibility to claim one of the above tax benefits, a paid tax return preparer, cannot use tax information that he or she knows, or has reason to know, to be incorrect. Additionally, the signing preparer must make reasonable inquiries if another reasonable and well-informed tax return preparer would conclude that the provided information is incorrect, inconsistent, or incomplete.

The IRS record-keeping requirements also require the tax preparer to maintain documentation about reasonable inquiries and the client’s answers to these questions.

A tax return preparer must know and understand the tax laws pertaining to each tax credit and/or HOH filing status claimed on a tax return. The preparer must use that knowledge to obtain relevant information and make reasonable inquiries about his or her client’s eligibility to claim any of these tax benefits.

Question 4

Did any information provided by the taxpayer or a third party appear to be:

- Incorrect

- Incomplete, or

- Inconsistent

If No, go to Question 5. Otherwise, go to Question 4a.

Question 4a

Did you make reasonable inquiries to determine the correct, complete, and consistent information?

Question 4b

Did you contemporaneously document your inquiries?

Based on the IRS’ record-keeping requirements, each tax preparer should maintain documentation pertaining to:

- Questions asked, specifically to whom, and when those questions were asked

- Information provided

- Impact of the client’s responses on the tax return

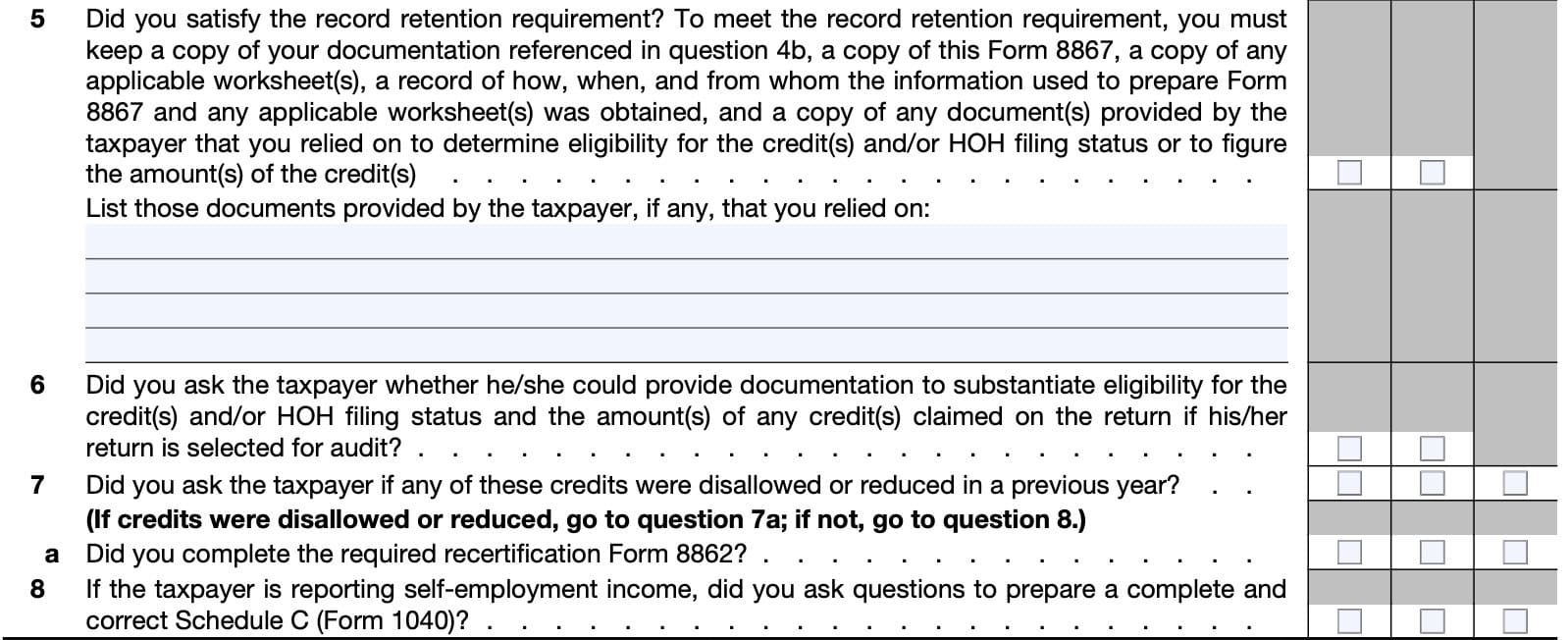

Question 5

Did you satisfy the record retention requirement? If so, list the documents that you relied upon, that the taxpayer provided.

IRS record retention requirements

The IRS requires preparers of federal income tax returns to adhere to certain document retention requirements. Specifically, a return preparer must keep:

- Copy of the documentation described in Question 4b

- A copy of the completed Form 8867

- Copies of applicable worksheets

- Records of how, when, and from whom any information used to prepare Form 8867 was obtained

- Including applicable worksheets

- Copies of supporting documents provided by the taxpayer to:

- Determine eligibility for credits or HOH filing status

- Calculate the amount(s) of applicable tax credits

A tax preparer must keep those records for 3 years from the latest of the following dates:

- The tax return’s due date (not including extensions).

- The date the return was filed

- For a signing tax return preparer electronically filing the return

- The date the return was presented to the taxpayer for signature

- For a signing tax return preparer filing the return in paper format

- The date you submitted to the signing tax return preparer the part of the return for which you were responsible

- If you are a nonsigning tax return preparer).

A tax preparer who has previously requested documents from the taxpayer to substantiate eligibility for a tax credit or HOH filing status as part of exercising due diligence does not need to request those documents again.

Examples of required documentation

According the IRS instructions, the following lists may satisfy certain due diligence criteria for specific questions related to a tax credit or HOH filing status. However, this list is not all-inclusive, and the IRS does not specifically require any of these documents to demonstrate eligibility for the related tax benefit.

Residency of a qualifying child

- School records or statement

- Landlord or a property management statement

- Health care provider statement

- Medical records

- Childcare provider records

- Placement agency statement

- Social service records or statement

- Place of worship statement

- Indian tribal official statement

Disability of a qualifying child

- Statement of medical doctor

- Statement of other health care provider

- Statement of social services agency or program statement

Schedule C

- Business license

- Forms 1099

- Records of gross receipts provided by taxpayer

- Taxpayer’s summary of income

- Records of expenses provided by taxpayer

- Summary of expenses provided by taxpayer

- Bank statements to show income and expenses

Question 6

Did you ask the taxpayer whether he/she could provide documentation to substantiate the following, in the case the Internal Revenue Service selects his or her tax return for a tax audit:

- Eligibility for the credit(s) and/or HOH filing status, and

- The amount(s) of any credit(s) claimed on the return

Check the appropriate box.

Question 7

Did you ask the taxpayer if any of these tax credits were disallowed or reduced in a previous tax year? If one or more tax credits was previously disallowed or reduced, go to Question 7a.

Otherwise, go to Question 8, below.

Question 7a

Did you complete the required recertification IRS Form 8862?

Unless an exception applies, taxpayers will have to file IRS Form 8862, Information To Claim Certain Credits After Disallowance, if the IRS previously disallowed one or more tax credits due to negligence or prior fraudulent claims. This does not include a claim that was disallowed due to a math or clerical error.

Question 8

If the taxpayer is reporting self-employment income, did you ask questions to prepare a complete and correct Schedule C?

There are specific due diligence requirements that tax preparers must follow to ensure that self-employed individuals correctly report their self-employment income on Schedule C. You may find additional information on Schedule C and the EITC as part of the EIC tax return preparer toolkit on the IRS website.

Part II: Due Diligence Questions for Returns Claiming EIC

In Part II, we’ll cover specific due diligence questions for income tax returns claiming the earned income tax credit (EIC). If the tax return does not attempt to claim the EIC, you may skip Part II and proceed to Part III.

Question 9a

Have you determined that the taxpayer is eligible to claim the EIC:

- For the number of qualifying children claimed, or

- Without a qualifying child

If the taxpayer does not have a qualifying child, go to Question 10, below.

Qualifying child requirements

To qualify for the EITC, a qualifying child must:

- Have a valid Social Security number

- Meet all 4 tests for a qualifying child

- Age test

- Relationship test

- Residency test

- Cannot file a joint tax return except to get a tax refund on income taxes withheld from their paycheck

- Not be claimed by more than one person as a qualifying child

Question 9b

Did you ask the taxpayer if the child lived with the taxpayer for more than half of the tax year, even if the taxpayer has supported the child for the entire year?

Question 9c

Did you explain the tiebreaker rules about claiming the EIC when a child is the qualifying child of more than one person?

The IRS EIC tiebreaker rules help determine if a taxpayer may claim a child as a qualifying child for the EIC when the child meets the definition of a qualifying child for more than one person.

EIC tiebreaker rules

If, under these rules, the taxpayer may not claim a child as a qualifying child for the EIC, the taxpayer may be able to claim the EIC under the rules for a taxpayer without a qualifying child. If the taxpayer is not claiming the EIC for a child that is the qualifying child of more than one person, the tax preparer should check “N/A.”

- If only one of the persons is the child’s parent: The child is treated as the qualifying child of the parent.

- If the parents file a joint return together and can claim the child as a qualifying child: The child is treated as the qualifying

child of both of the parents. - If the parents do not file a joint return together but both parents claim the child as a qualifying child: The child is treated

as the qualifying child of the parent with whom the child lived for the longer period of time during the year.- If the child lived with each parent for the same amount of time, the child is treated as the qualifying child of the parent who had the higher adjusted gross income (AGI) for the year.

- If no parent can claim the child as a qualifying child: The child is treated as the qualifying child of the person who had the highest AGI for the year.

- If a parent can claim the child as a qualifying child but no parent does so: the child is treated as the qualifying child of the person who had the highest AGI for the year, but only if that person’s AGI is higher than the highest AGI of any of the child’s parents who can claim the child.

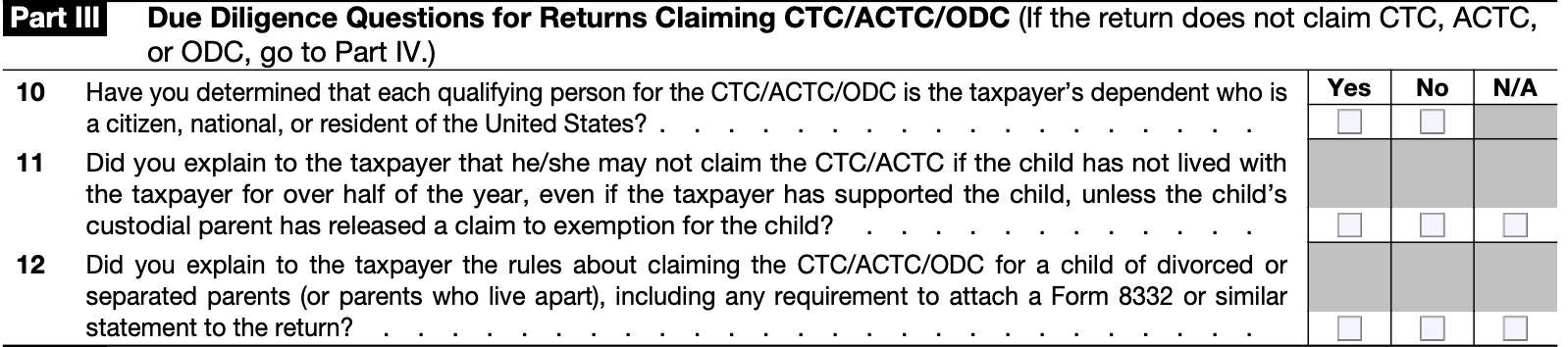

Part III: Due Diligence Questions for Returns Claiming CTC/ACTC/ODC

In Part III, we’ll cover specific due diligence questions for income tax returns claiming one of the following tax credits:

- Child tax credit (CTC)

- Additional child tax credit (ACTC)

- Credit for other dependents (ODC)

If the tax return does not attempt to claim any of these credits, you may skip Part III and proceed to Part IV.

To claim any of these tax credits, a taxpayer must meet all of the eligibility requirements, regardless of the answers to Question 12.

Question 10

Have you determined that each qualifying person for the CTC/ACTC/ODC is the taxpayer’s dependent who is a citizen, national, or resident of the United States?

Question 11

Did you explain to the taxpayer that he/she may not claim the CTC/ACTC if the child has not lived with the taxpayer for over half of the year, even if the taxpayer has supported the child, unless the child’s custodial parent has released a claim to exemption for the child?

Question 12

Did you explain to the taxpayer the rules about claiming the CTC/ACTC/ODC for a child of divorced or separated parents (or parents who live apart)? This includes the requirement to attach a completed copy of IRS Form 8332, Release/Revocation of Release of Claim to Exemption for Child by Custodial Parent, or similar documentation, to the tax return.

Part IV: Due Diligence Questions for Returns Claiming AOTC

In Part IV, we’ll cover specific due diligence questions for income tax returns claiming the American Opportunity Tax Credit (AOTC). If the tax return does not attempt to claim the AOTC, you may skip Part IV and proceed to Part V.

Question 13

Did the taxpayer provide substantiation for the credit?

This can include documents such as:

- A taxpayer’s copy of the tuition statement, IRS Form 1098-T, issued by the higher education institution

- Receipts for the qualified tuition and related expenses

A taxpayer must meet all of the eligibility criteria to claim the AOTC, even if the tax return preparer answers ‘Yes’ to Question 13.

Part V: Due Diligence Questions for Claiming HOH

In Part V, we’ll cover specific due diligence questions for income tax returns claiming head of household tax filing status. If the tax return does not attempt to claim HOH status, you may skip Part V and proceed to Part VI.

Question 14

Have you determined that the taxpayer was unmarried or considered unmarried on the last day of the tax year and provided more than half of the cost of keeping up a home for the year for a qualifying person?

Taxpayers must meet all of the criteria to claim head of household filing status, even if you check ‘Yes’ to Question 14. IRS Publication 501 contains additional information about HOH filing requirements.

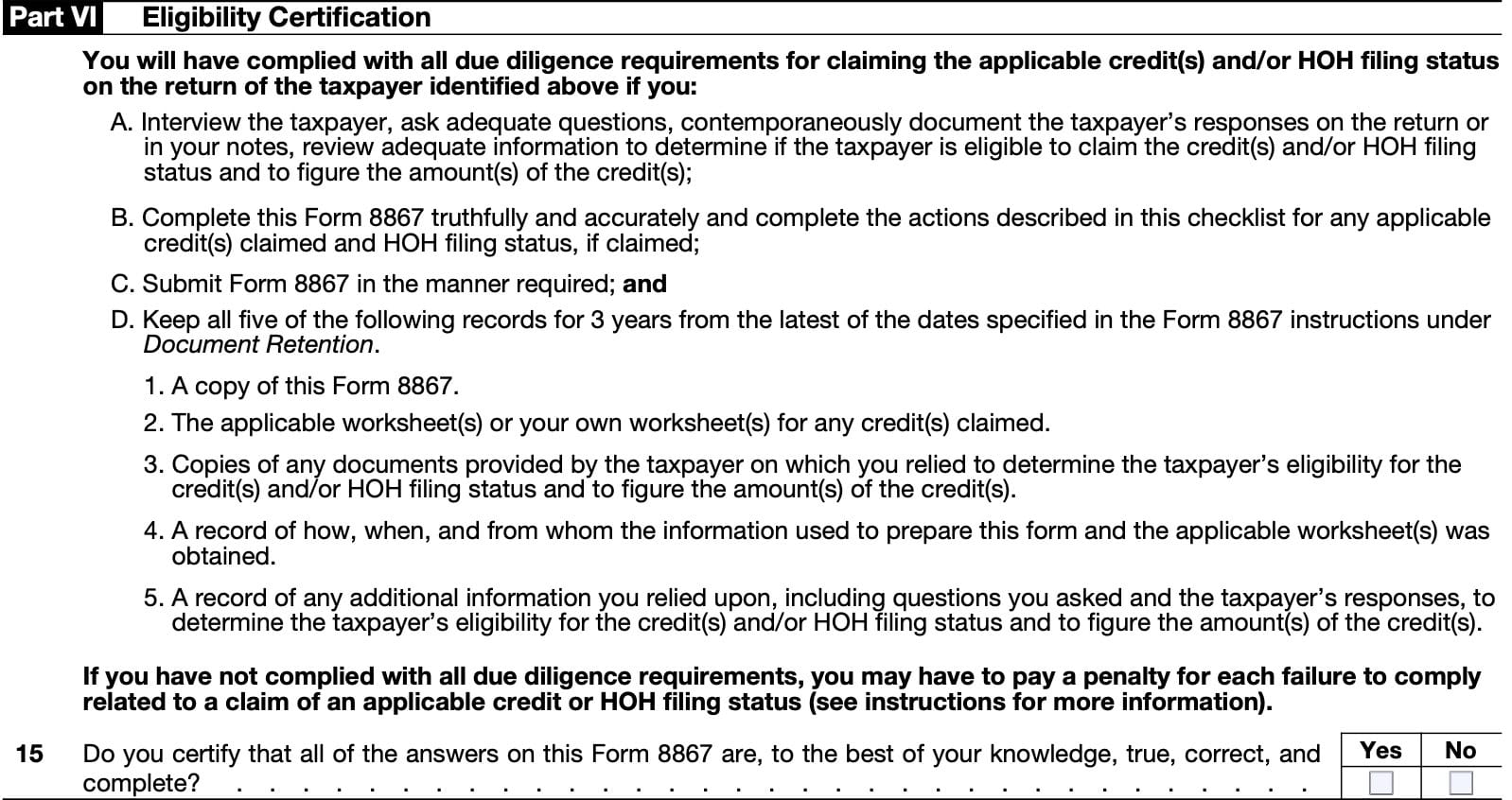

Part VI: Eligibility Certification

In part VI, the tax preparer ascertains that he or she has complied with all of the due diligence regulations and requirements for claiming the applicable tax credits and head of household filing status.

Question 15

Do you certify that all of the answers on this Form 8867 are true, correct, and complete, to the best of your knowledge?

Due diligence penalties

Failure to meet the due diligence requirements for claiming the EIC, the CTC/ACTC/ODC, the AOTC, and/or HOH filing status could result in a $635 (amount for a return or claim for refund filed in 2026) penalty for each failure. If a paid tax preparer fails to meet the due diligence criteria for a taxpayer claiming all of these tax benefits, that preparer could face a maximum penalty of $2,540 for that income tax return.

Video walkthrough

Watch our instructional video for more details about what your tax professional might ask you when completing IRS Form 8867.

Frequently asked questions

The purpose of IRS Form 8867, Paid Preparer’s Due Diligence Checklist, is to ensure that the practitioner has considered all applicable eligibility criteria for certain tax credits for each return prepared. This includes the Earned Income Credit, American Opportunity Tax Credit, Child Tax Credit, and Head of Household filing status.

A paid tax return preparer cannot ignore the implications of any information given or known to the preparer. The preparer must also make additional reasonable inquiries, if a reasonable and well-informed tax return preparer, knowledgeable in the law, would conclude the information furnished appears incorrect, inconsistent or incomplete.

The IRS requires tax preparers to maintain copies of Form 8867 for 3 years after the tax return due date, filing date, date the return was submitted for taxpayer’s signature, or the date that the return was submitted to a signing tax return preparer (if the preparer was not a signing preparer), whichever is later.

Where can I find IRS Form 8867?

You can find IRS Form 8867 on the IRS website. For your convenience, we’ve included the latest copy of Form 8867 here, in this article.