IRS Form 8971 Instructions

In 2015, the Surface Transportation and Veterans Health Care Choice Improvement Act created an additional reporting requirement for taxable estates. Not only do executors of the estate above the basic exclusion amount have to file a federal estate tax return, they must also report the value of the property they distribute. The Internal Revenue Service created a new form, IRS Form 8971, to meet that new requirement.

In this article, we’ll walk through the basics of Form 8971, including:

- Who must file IRS Form 8971

- How to complete IRS Form 8971

- Applicable penalties for taxpayers

Let’s start with step by step instructions for IRS Form 8971.

Table of contents

How do I complete IRS Form 8971?

Both IRS Form 8971 and Schedule A are one-page documents. That said, we’ll go through each page step by step, starting with the form itself.

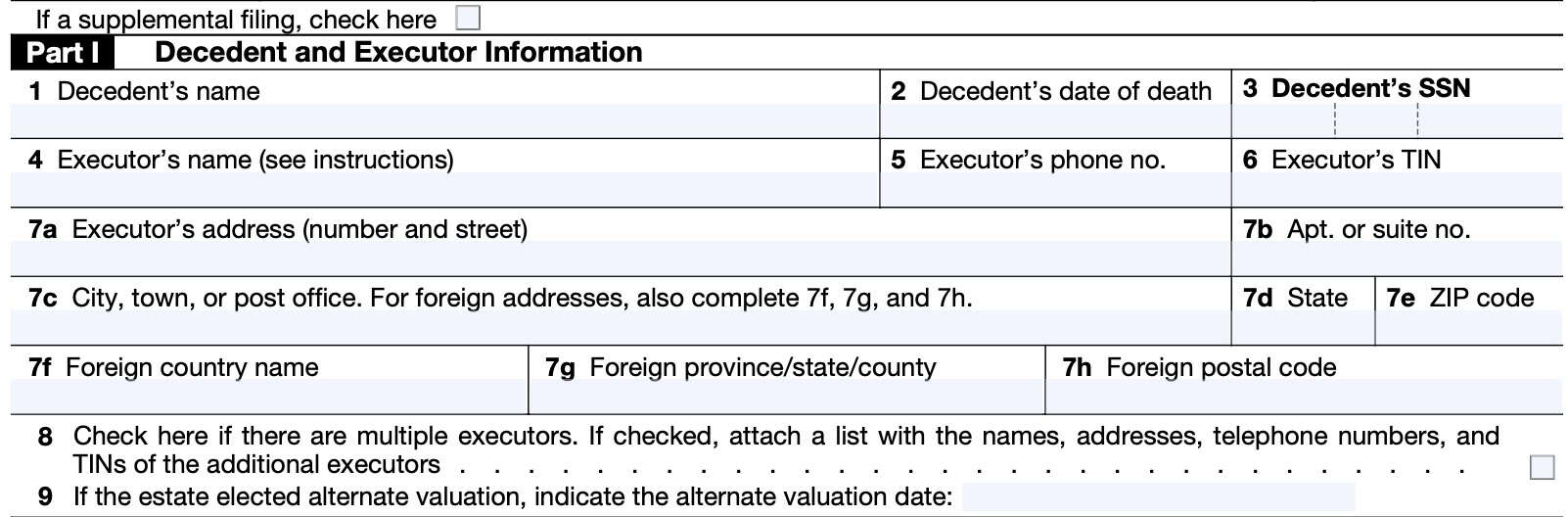

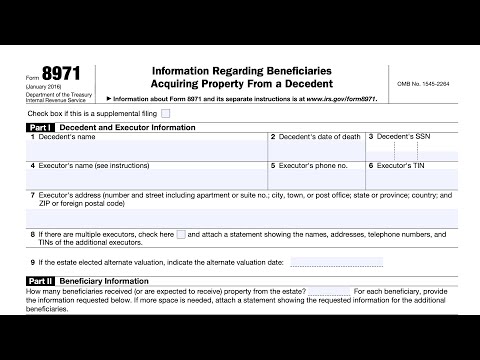

Form 8971

There are two parts to the form itself:

- Part I: Decedent and Executor Information

- Part II: Beneficiary Information

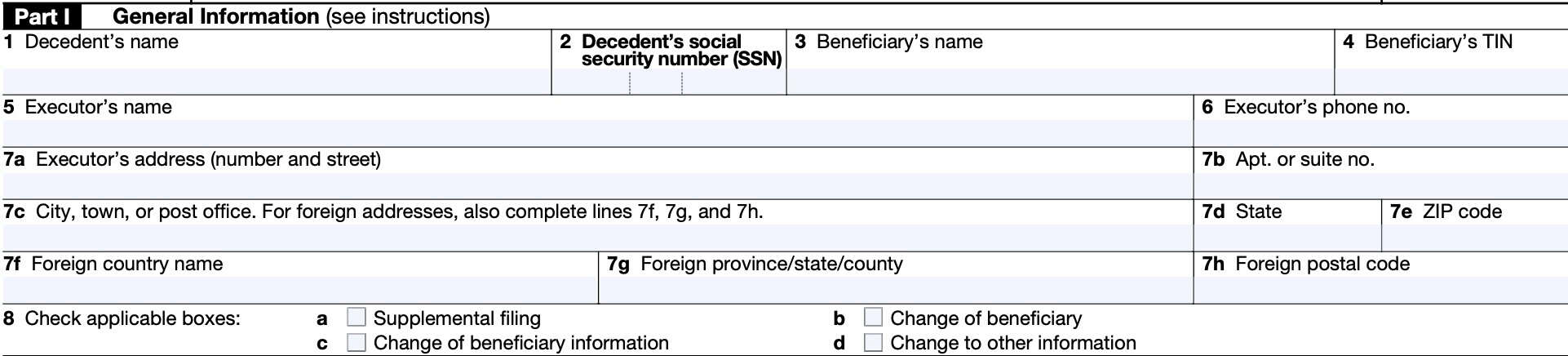

Let’s start at the top of Part I, beginning with Line 1.

Line 1: Decedent’s name

List the decedent’s name.

Line 2: Date of death

State the date of the decedent’s passing, as it appears on their death certificate and estate tax return

Line 3: Decedent’s SSN

If the decedent died without having a Social Security number, the executor of the estate may need to request one on the decedent’s behalf by filing SS-5, Application for a Social Security card.

There are several options to request form SS-5:

- Through the Social Security Administration’s website

- Calling the SSA at: 1-800-772-1213

Line 4: Executor’s name

In cases where there is more than one executor, enter the name of one executor, then follow the directions on Line 8, below.

Line 5: Executor’s phone number

Enter the phone number.

Line 6: Executor’s TIN

If there is more than one executor, provide only the TIN for the executor named in Line 4, then follow the instructions for Line 8, below.

Line 7: Executor’s address

For more than one executor, provide the address for the executor named in Line 4, then follow the Line 8 instructions. If the executor has recently moved, you may need to file IRS Form 8822 to report the change in address.

Line 8

Check the box if there are more than 1 executor of a decedent. Attach a statement showing the following information for the remaining executors:

- Executor name

- Address

- Telephone number

- TIN

Line 9: Alternate valuation date

If the estate elected alternate valuation, enter the alternate valuation date here.

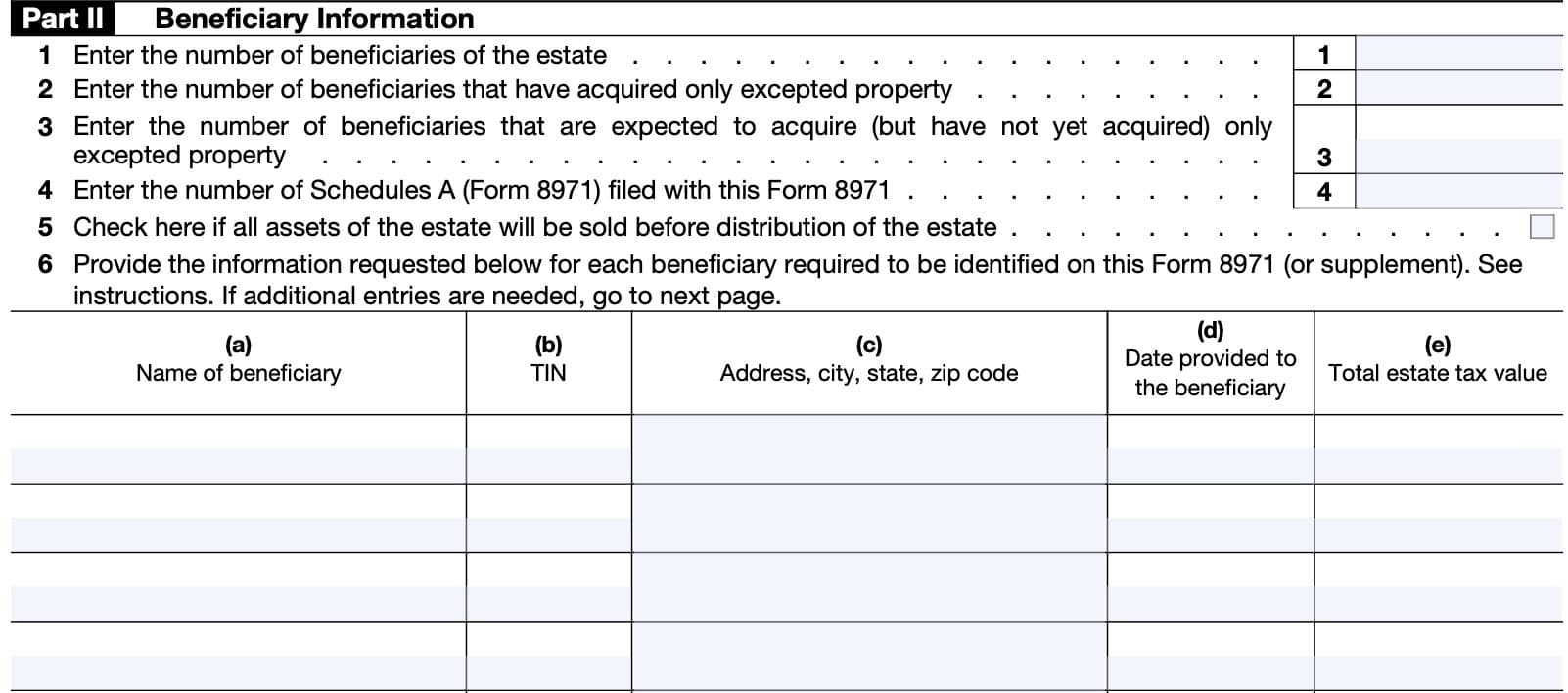

Part II

Part II lists the number of beneficiaries who received property, or who are expected to receive property from the decedent’s estate.

Before entering the beneficiary information, there are several lines to complete.

Line 1

Enter the number of beneficiaries of the estate.

Line 2

Enter the number of beneficiaries that have acquired only excepted property.

Excepted property

Excepted property includes the following:

- United States dollars

- United States dollar-denominated demand deposits;

- Certificates of deposit denominated in United States

- Cash collateral denominated in United States dollars held by a third party to secure a liability (such as a deposit of purchase money or a security deposit);

- Money market shares in a mutual fund

- Life insurance proceeds on the life of the decedent payable in a lump sum in United States dollars;

- Federal, state, and local tax refunds and other refunds payable in United States dollars;

- Notes that are forgiven in full by the decedent upon the decedent’s death, whether or not denominated in United States dollars;

- Household and personal effects for which an appraisal is not required under Section 20.2031-6(b) of the Estate Tax Regulations;

- Property that, prior to distribution from the estate or the decedent’s revocable trust, is completely sold, exchanged, or otherwise disposed of in one or more transactions that are recognition events for federal income tax purposes

- Other property having an initial basis that is not in any way determined with regard to or derived from the property’s fair market value for federal estate tax purposes

- Bonds to the extent that they are redeemed by the issuer for United States dollars prior to being distributed to a beneficiary so that any resulting gain or loss is recognized by the estate;

- Property included in the gross estate of a beneficiary who died before the due date of the Information Return; and

- Any other property that is identified as excepted property in published guidance in the Federal Register or in the Internal Revenue Bulletin

Line 3

Enter the number of beneficiaries who are expected to acquire only excepted property, but have not yet done so.

Line 4

Enter the number of Schedules A filed with this form.

Line 5

Check this box if all estate assets will be sold before distribution.

Line 6

Provide the requested information for each beneficiary required to be identified on this form. If you need additional pages, you may use them.

For each beneficiary, you’ll need to list:

- Column A: Beneficiary’s name

- Column B: Beneficiary’s TIN

- If you do not have the TIN, enter “Requested”

- Column C: Beneficiary’s full address, including city, state, and zip code

- Column D: Date that Schedule A was provided to the beneficiary

- Column E: Total estate tax value

If you do not have a beneficiary’s TIN, you must request it from the beneficiary. If you’ve requested a beneficiary’s TIN but have not received it at the time of filing, you must file a supplemental 8971 and corresponding Schedule A once the beneficiary provides their TIN to you.

Line 7

Add all amounts from Column (e). Enter the total here.

Line 8

Enter the total from Column (e) for any additional Parts II attached to this form.

Line 9

Add Line 7 and Line 8. This total must match the total from all Schedules A, Part II, Line 4, Column (h).

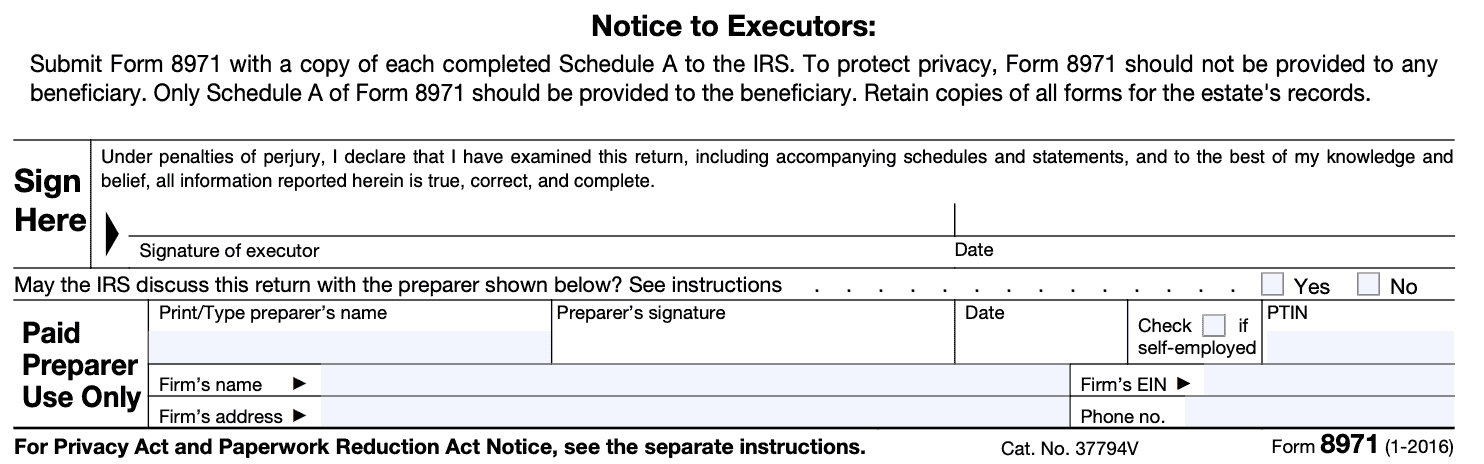

Notice to Executors

Executor’s signature and date goes in the taxpayer’s signature block.

Do not provide a copy of the complete form to any beneficiary, as it contains confidential information about the other beneficiaries.

If using a paid preparer, selecting Yes to the IRS question about discussing this return only authorizes the preparer to discuss information on this form with the IRS. It does not authorize the preparer to represent the decedent’s estate in any manner.

To authorize your tax preparer’s authorization, you must complete and attach IRS Form 2828, Power of Attorney and Declaration of Representative to this form. When completing the declaration, the executor’s name, not the decedent’s name, goes on Line 1 of the form.

Schedule A

Schedule A contains two parts as well. The first part, General Information, will contain much of the information located in the form itself.

At the top of the form, check the box if this is a supplemental Schedule A.

Line 1: Decedent’s name

Same as Line 1 on the form itself.

Line 2: Date of death

Same as Line 2 on the form itself.

Line 3: Beneficiary’s name

As outlined in Part II of the form.

Line 4: Beneficiary’s TIN

As outlined in Part II of the form.

Line 5: Executor’s phone number

Same as Line 5 on the form itself.

Line 6: Executor’s TIN

Same as Line 6 on the form itself.

Line 7: Executor’s address

Same as Line 7 on the form itself.

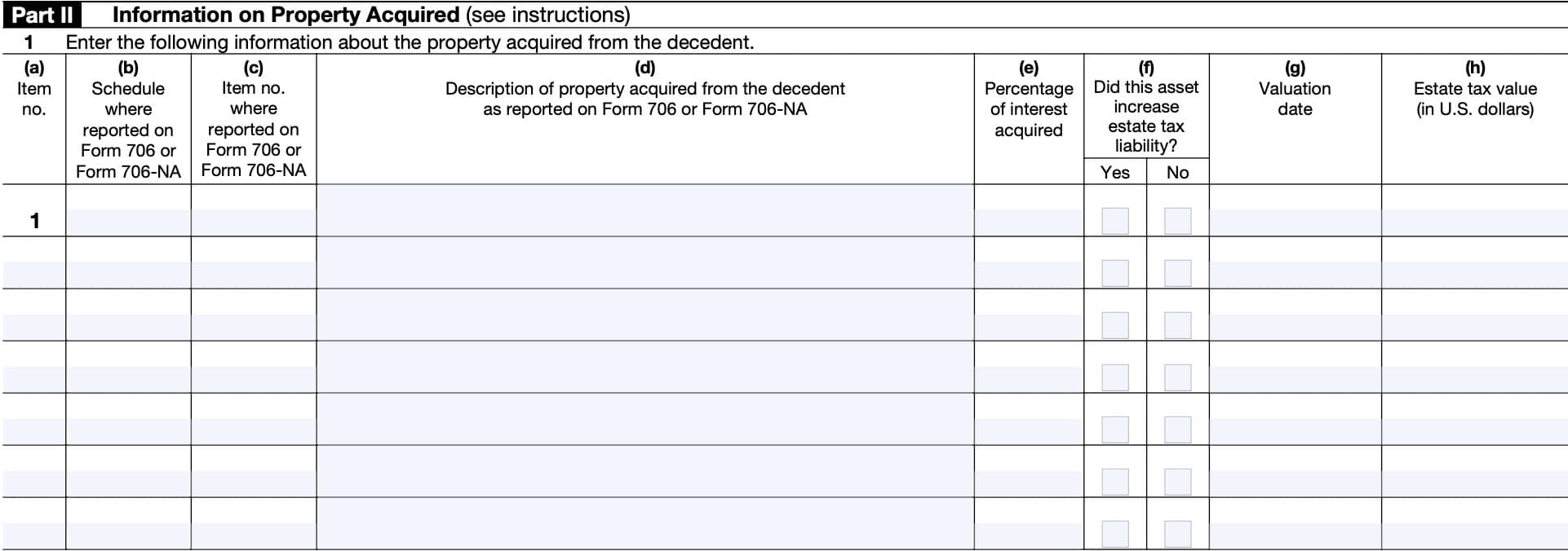

In Part 2 of Schedule A, list each item that has been distributed, or that you expect to distribute to the specified beneficiary. If you need to use additional pages, the form has a continuation page on the back. When using the continuation page, be sure to list the total number of pages, and specify the number of that particular page (example: Page 3 of 7).

Column A: Item number

Number each item received by the beneficiary. Carry this numbering convention through each continuation page, as necessary.

Column B: Property description

In Column B, enter the same description that the executor used for the property on the Form 706 or Form 706-NA. Include in Column B the schedule and item number where the property was reported on Form 706 or Form 706-NA, as applicable.

If the beneficiary acquired a partial interest in the property, indicate the interest acquired in Column B.

For additional information on description requirements, see the instructions for IRS Form 706 or Form 706-NA.

Column C

Enter “Y” only if:

- Estate taxes were generated and

- The asset contributed to the estate tax

As a standard rule, any property that qualifies for either of the following will not generate estate tax, meaning that ‘N’ would be appropriate:

- Marital deduction under IRC Section 2056 or through a qualified domestic trust under Section 2056A, or

- Charitable deduction under Section 2055

Column D: Valuation date

Generally, this is the date of the decedent’s date, unless an alternate valuation date was indicated in Line 9.

Column E: Estate tax value

List the value reported on the estate tax return. The value reported in column E should be the fair market value as of the decedent’s date of death or any alternate valuation date used for the estate tax return.

This value should not reflect any change in asset value since the decedent’s death.

Who must file IRS Form 8971?

As a general rule, all estate executors who must file a federal estate tax return must also file Form 8971. This includes both IRS Form 706 for U.S. citizens and residents as well as IRS Form 706-NA for nonresident aliens.

Those filing requirements depend largely on the basic exclusion amount for federal estate tax purposes. Below are the basic exclusion amounts by tax year.

| Tax Year | Exclusion amount (per person) | Exclusion amount (per married couple) |

| 2025 | $13,990,000 | $27,980,000 |

| 2026 | $15,000,000 | $30,000,000 |

However, Form 8971 isn’t always required when filing an estate tax return. Here are the cases in which the executor of the estate does not have to file:

- The gross estate plus adjusted taxable gifts is less than the basic exclusion amount, as previously mentioned

- The executor filed estate tax-related forms other than Form 706 or Form 706-NA

- IRS Form 706-CE: Certification of Payment of Foreign Death Tax

- IRS Form 706-GS: Generation-Skipping Transfer Tax Return for Distributions

- IRS Form 706-QDT: U.S. Estate Tax Return for Qualified Domestic Trusts

- The estate tax return is filed solely to make an allocation or election respecting the generation-skipping transfer tax (GSTT); or

- The estate tax return is filed solely for portability election of the deceased spousal exclusion amount (DSUE).

- Also known as the marital deduction

While not all estates must file IRS Form 8971, it’s still important to know when to file or not. Because the associated penalties can be steep.

What penalties apply if I don’t file Form 8971?

There are multiple penalties that the IRS may impose on estates that do not properly file, depending on the circumstances. Each penalty may be imposed without respect to the other penalties.

Failure to file correct Form 8971 by the due date

Under IRC Section 6721, the IRS may impose a penalty for failure to file a correct Form 8971 by the due date. This penalty applies to the following:

- Failure to file on time

- Failure to include all information required to be shown on the form or schedule

- Failure to include correct information on the form or schedule, or

- Failure to file a correct supplemental Form 8971 and/or Schedule A by the due date

The severity of the penalty depends on how late the return is, or how long it takes to file the correct return. A taxpayer may qualify for a reduced maximum penalty if the gross annual receipts for the most recent 3 tax years were $5 million or less.

There are also limited exceptions if there is reasonable cause, or an inconsequential error or omission. However, errors related to the following are never considered inconsequential:

- Taxpayer identification number (TIN)

- Beneficiary’s name

- Value of the asset received from the estate

- Beneficiary’s address

Returns correctly filed within 30 days

For returns filed correctly within 30 days of the due date of Form 8971, the penalty is $50 per form, up to a maximum penalty of $532,000 per year ($186,000 for taxpayers eligible for reduced maximum penalties). This includes all required Schedules A.

Returns correctly filed after 30 days

For returns filed correctly after 30 days of the due date, the penalty is $2600 per Form 8971, up to a maximum penalty of $3,193,000 per year ($1,064,000 for taxpayers eligible for reduced maximum penalties). This includes all required Schedules A.

Failure to provide proper Schedules A to each designated beneficiary by the due date

IRC Section 6722 authorizes the IRS to impose a penalty if the executor of the estate does not give a copy of every Schedule A to each beneficiary before the filing deadline. The penalties are the same as the applicable penalties under IRC Section 6721, above.

Intentional disregard of filing requirements

If the IRS determines that failure to file or provide Schedule A is caused by intentional disregard of filing requirements, it may impose a minimum penalty of $530 per required form or schedule. There is no maximum penalty.

Penalty for inconsistent filing

IRC Section 6662 authorizes the IRS to impose a 20% accuracy-related penalty on beneficiaries who report basis in property that is inconsistent with the amount on the Schedule A.

Now that we understand the penalties involved in not properly filing this form on time, let’s move on to how to complete the form.

Video walkthrough

Watch this instructional video to learn more about how to complete IRS Form 8971.

Frequently asked questions

IRS Form 8971 is the tax form that the executor of an estate must use to report the final estate tax value of property of that estate. This information return reports the values from the decedent’s gross estate to both the IRS and to each beneficiary receiving property from the estate.

By receiving a copy of this tax form, each beneficiary of an estate can better understand the new basis of property that they inherit. This helpful information can help those beneficiaries make better decisions on such property because they can understand the capital gain tax impact. This form also provides the IRS better transparency to ensure taxpayers don’t misrepresent the final value of inherited property.

The executor must file IRS Form 8971, with all Schedules A, with the IRS no later than the earlier of: 30 days after the estate tax return’s due date or 30 days after the estate tax return is actually filed. At the time of filing, the executor must also provide each beneficiary with his or her separate Schedule A.

Where can I find IRS Form 8971?

As with other tax and information forms, you may find IRS Form 8971 on the IRS website. For your convenience, we’ve included the most recent version of IRS Form 8971 and Schedule A for download at the bottom of this article.