What Every Woman Should Know About Social Security: The Missing Parts

Many women experience economic challenges, especially in retirement. According to a recent Department of Labor study, women aged 65 years or older are “43% more likely than men to live on an income below the poverty level.” In fact, the Social Security Administration has published a guide, “What Every Woman Should Know About Social Security,” to help empower women on this important benefit.

Honestly, every person considering Social Security should read this guide, man or woman. But at 27 pages, it might be too dense for casual readers. Fortunately, there’s another SSA Publication: 5 Things Every Woman Should Know About Social Security.

While it’s shorter than the complete guide, there are some glaring omissions that you probably need to know about. We’ll cover this guide in more depth, specifically:

- What the Social Security Administration gets right in this 2-pager

- Crucial missing details that might be important for people to know

But first, a disclaimer.

Contents

Before you start

My highest recommendation is to discuss your financial needs with a Certified Financial Planner, who can cover Social Security planning as part of your entire financial plan. Likely, your planner uses a retirement planning software to help with your analysis. And in recent years, retirement planning software has made significant strides to include the complexities of timing Social Security benefits.

And like many financial mistakes, making the wrong Social Security decision can often be an irreversible decision. So its best to have someone to help you make your own decisions.

But if you’re determined to do this on your own, I’ve tried to curate some of the most important details below.

1. Nothing keeps you from receiving your own Social Security benefits

This is 100% true. If you’ve worked for at least 10 years, and accumulated at least 40 work credits, you may be entitled to Social Security benefits based on your own work history. Regardless of your spouse’s earnings history.

What the brochure covers

- You can claim Social Security as early as age 62

- Your Social Security benefits are based upon your 35 highest years of earnings

- You might be eligible for disability benefits if you worked for at least 5 of 10 prior years

- Your Social Security benefits might be reduced if you worked in a place where you didn’t have to pay Social Security taxes

What the brochure overlooks

There are a couple of key points that are easy to overlook here.

If you claim benefits early, you may be shortchanging yourself

You can claim retirement benefits as early as age 62. But people who claim early receive smaller pensions than those who wait. In fact, for each year after full retirement age that you delay claiming Social Security, your benefits increase by 8%.

The monthly payments for people who can afford to wait until age 70 to claim benefits can be about twice as much as people who decide to take Social Security at age 62.

And the reduced amount of your Social Security benefits can result in tens, or hundreds of thousands of dollars in lost Social Security benefits over the course of your lifetime.

You need to double check your earnings history

Your Social Security earnings history will determine how much your Social Security retirement benefits end up being. At least the highest 35 years of earned income history will.

And if, as part of your 35-year base, your employer made a mistake in reporting your earnings, this can directly impact your livelihood.

Fortunately, you can easily check this before claiming benefits by:

- Filing Form SSA 7050 to receive detailed earnings information, or

- Creating a free my Social Security account online

From there, you can evaluate your earnings, decide if they’re accurate, and take steps to correct any inaccuracies.

But even if your earnings are accurate, your Social Security payouts depend on another factor: your full retirement age. This, you should know.

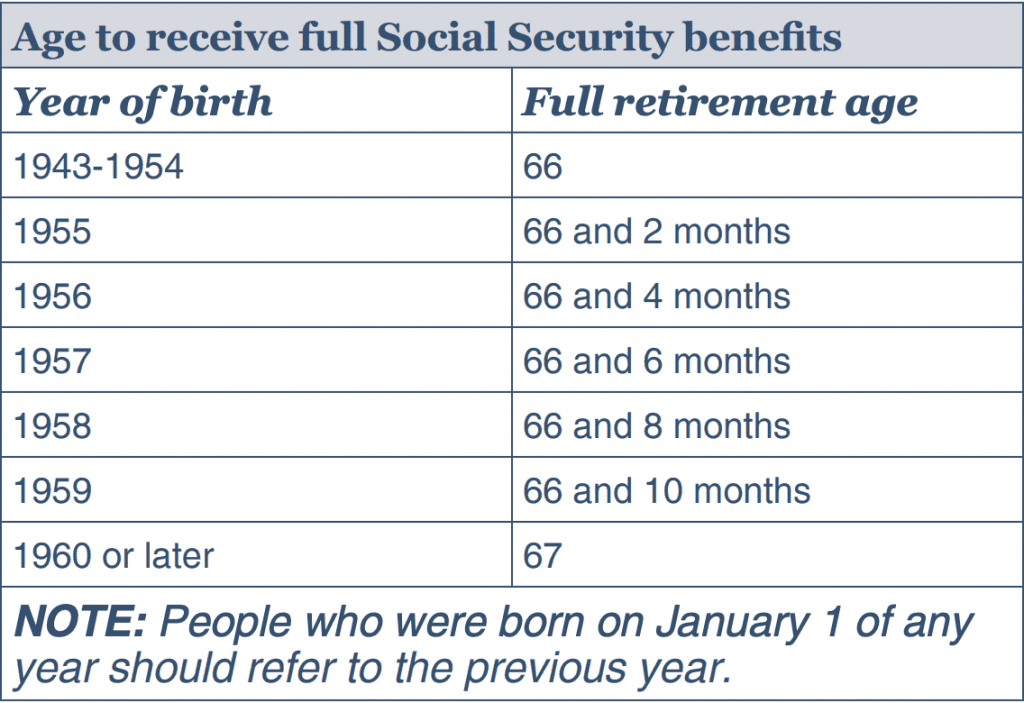

You should know your full retirement age

Full retirement age (FRA) is the age in which the applicant may file for, and receive, their full benefit. This sounds intuitive, but in the 21st Century, that FRA has slowly moved up from age 66. For people born in 1960 or later, FRA is age 67.

And this has a direct impact on both:

- The amount you’re penalized for claiming early benefits

- The amount of delayed credits you receive for waiting until age 70

Below is a full table of precise full retirement age based upon your year of birth.

So a person born in 1960 who decides to claim at age 62 will penalized for withdrawing 5 years early. Conversely, a person born in 1950 who also claimed at age 62 would only be penalized for withdrawing 4 years early.

So the younger you are, the more early withdrawals will hurt you.

Filing early can be the gift that keeps on killing you

In addition to receiving lower benefits for life, your annual cost-of-living adjustments (COLA) won’t go as far. This is because the percentage applies to a smaller number. Year over year.

For example, let’s look at two people, Mary and Sarah. Both decide to file for benefits this year. Mary is entitled to $2,000 per month, while Sarah is entitled to $1,500 per month.

Next year, the SSA announces a 2% COLA adjustment, which amounts to the following new entitlements:

- Mary: $2,040 ($40 per month more than last year)

- Sarah: $1,530 ($30 per month more than last year)

This doesn’t seem like that much. But here’s what that simple difference might look like over 10, 20, and 30 years:

- Year 0: $500/month ($2,000 minus $1,500)

- Year 1: $510/month ($2,040 minus $1,530)

- Year 10: $609.50/month

- Year 20: $742.97/month

- Year 30: $905.68/month ($3,622.72 minus $2,717.04)

In other words, the deficit between Sarah and Mary has grown from $500 per month to over $900 per month.

Note: If you think that 30 years is too long for planning purpose, please keep in mind that most retirement plans assume that you live until age 100. This is completely possible.

2. There is no marriage penalty or limit to benefits paid to a married couple

What the brochure covers

Unlike certain parts of the tax code, there is no penalty for a married couple looking to claim benefits. And there is no limit to the amount of benefits a married couple may claim.

If each spouse passes the Social Security earnings test (at least 10 years of covered work history), then each is entitled to their own retirement benefit, based upon their own work history.

What the brochure overlooks

How a married couple can decide on claiming benefits

Just because you can take your own benefit doesn’t necessarily mean that you should (see #3 below). So how do you determine whether one spouse should claim their own Social Security benefit, or claim a spousal benefit?

Fortunately, your financial planner can run multiple scenarios and put them side by side. From there, you can determine which claiming strategy has the highest lifetime value, and you can decide for yourself.

Those scenarios include comparing multiple benefits, if you’re entitled to them.

3. If you’re due two benefits, you’re generally paid the higher rate,

not both

What the brochure covers

As a spouse, if you are eligible for benefits on either:

- Your own work record and

- Your spouse’s work record

But not both. In most cases, you may be required to apply for both benefits. From there, the Social Security system will automatically choose the higher amount.

If you are a spouse with no work record or a low entitlement on your own record, you might be eligible for up to one-half of your spouse benefits. Most working spouses receive their own record because it’s more than 1/2 of their spouse’s benefit.

You can apply for a widow’s rate if your spouse dies before you.

What the brochure overlooks

How to put all this together

Deemed filing represents another layer of complexity to Social Security planning.

Deemed filing came about because of the revocation of ‘file and suspend,’ and restricted applications. These were Social Security claiming strategies created by loopholes in the Social Security Act. Unfortunately, these loopholes were closed in 2015 and are largely unavailable to new filers.

Because of this, both spouses need to evaluate their situations to see what might be the best situation for them. In addition to deemed filing, here are some other factors that might come into play:

- Outside cash flow or income

- Size of retirement accounts (which may determine required minimum distribution size and IRMAA surcharges)

- Longevity and life expectancy of each spouse

Two common filing strategies

When working with clients, I ran hundreds of Social Security projections. After these loopholes closed, many of the highest outcome came in one of two ways:

- Both spouses wait until age 70 and collect maximum benefits

- Lower earning spouse files based on own record at FRA, then claims spousal benefit at age 70

Again, your financial advisor might be able to run the numbers and see which one serves you best.

4. If you’re divorced and were married at least 10 years, you may be eligible on your ex’s Social Security record

What the brochure covers

Divorced women who were married at least 10 years may be eligible for Social Security based on their ex-spouse’s work record. This only applies if they are:

- Unmarried and

- Not entitled to a higher benefit on their own record when they become eligible for Social Security

Some women sign divorce decrees relinquishing their rights to Social Security on their ex’s record. Those clauses in divorce decrees are rarely enforced.

Any benefits paid to a divorced spouse DO NOT reduce payments made to the ex or any payments due the ex’s current spouse.

Generally, the same payment rules apply to divorced wives and widows as to current wives and widows. That means most divorced women collect their own Social Security while the ex is alive, but

they can apply as a surviving spouse and collect survivor benefits when their ex-spouse passes away.

What the brochure overlooks

How nasty divorce negotiations can get

Anyone who has gone through a combative divorce can sympathize with a newly single woman who signs an additional clause just to get the divorce decrees finalized. In honesty, claiming benefits on based upon the service record of your ex-spouse generally doesn’t trigger anything significant because:

- There is ZERO impact to your ex-spouse’s pension, and

- It’s highly unlikely that your ex will even know when you apply for benefits

But the SSA really undersells this point. Especially given the context of many nasty divorces.

If you’re a survivor of domestic violence, the SSA may help

This might be of cold comfort to victims who are (rightfully) skeptical of ‘help’ from others, but the SSA is a powerful institution.

For example, many survivors have to change their identity to hide from their ex-spouse, who is now stalking them. Under the right circumstances, the SSA can help you change your identity, to include assigning you a new Social Security number.

You can find more information under their guide for New Social Security Numbers for Domestic Violence Victims.

5. When your spouse (or ex) dies, you may be due a widow’s benefit

What the brochure covers

A widow is eligible for between 71 percent (at age 60) and 100 percent (at full retirement age) of what the spouse was getting before they died.

The SSA must pay your own retirement benefit first, then supplement it with whatever

extra benefits you are due as a widow. This will bring your Social Security benefit amount up to the widow’s rate.

The SSA also can pay you a $255 lump sum payment if you were living with your

spouse when they died. As an aside, I wrote an in-depth guide about how to claim the lump sum death benefit.

If you made more money than your spouse, (or ex-spouse) then they might be due a survivors benefit rate on your record, if you die before they do.

What the brochure overlooks

You don’t earn delayed retirement credits.

When filing for retirement benefits, most people understand that filing as late as age 70 can result in increased retirement benefits. That’s between 3 or 4 years after full retirement age. After reaching age 70, there is no additional benefit to delaying.

When filing for survivor benefits, there is no additional benefit to delaying beyond full retirement age. This means that when you reach FRA, it is in your best interest to file for survivor benefits, even if you end up waiting until age 70 to claim your own benefits.

You’re probably better off if your higher-earning spouse delays benefits until age 70.

Not only does this positively impact your spouse’s COLA adjustments (as mentioned earlier), but you end up with his (or her) higher pension as a survivor.

So the higher pension ends up being the better fit over two lifetimes.

Conclusion

Overall, the SSA does a great job of providing all the content you need to make the right Social Security decisions. However, they do a mediocre job of providing this content in a user-friendly format.

If you have any questions, please feel free to reach out and email me!