IRMAA Frequently Asked Questions

We often receive IRMAA questions from clients and other people who visit our blog. Below are a few of the most common IRMAA questions we’ve answered from readers and clients.

As we see more questions, we will continue to update this page. If you have a question, please leave a comment below and we’ll do our best to answer it!

1. What is IRMAA?

IRMAA is also known as the income-related medical adjustment amount. Essentially, it’s a surcharge applied to Medicare premiums by the Social Security Administration for higher-income beneficiaries.

2. What parts of my Medicare premium are affected by IRMAA?

IRMAA applies to Medicare Parts B & D.

3. Do I have to worry about IRMAA before I start taking Medicare?

No. IRMAA only applies to Medicare beneficiaries.

4. Do I need to pay Part D IRMAA if I am not enrolled in Medicare Part D?

No. According to a December 10, 2010 Centers for Medicare & Medicaid Services (CMS) memorandum, if an individual does not have a Medicare prescription drug plan, that person should not be charged Part D IRMAA.

However, if that person disenrolled (either voluntarily or involuntarily) and has unpaid Part-D IRMAA from the outstanding balance, then that person might be responsible for the past due amount.

5. Who decides my IRMAA, and how do they calculate it?

The Social Security Administration (SSA) makes this determination. According to the SSA Program Operations Manual System (POMS) HI 01101.035-Initial IRMAA Determination Notices, the SSA makes these determinations based on IRS data (from your individual tax returns).

6. How do I pay IRMAA?

The SSA handles IRMAA payments in one of two ways:

- If you are taking Social Security and the amount of your check can cover your IRMAA charges, then the SSA will automatically deduct the IRMAA from your Social Security checks.

- If you are not yet taking Social Security, or the IRMAA charges exceed the amount of your check, then you will receive a bill for the unpaid IRMAA balance. This bill will come from either the Centers for Medicare & Medicaid Services or the Railroad Retirement Board, whichever applies to you.

7. Do I have to pay IRMAA even if I’m not taking Social Security?

If you are a Medicare participant and subject to IRMAA due to income, then you are required to pay IRMAA even if you are not taking Social Security.

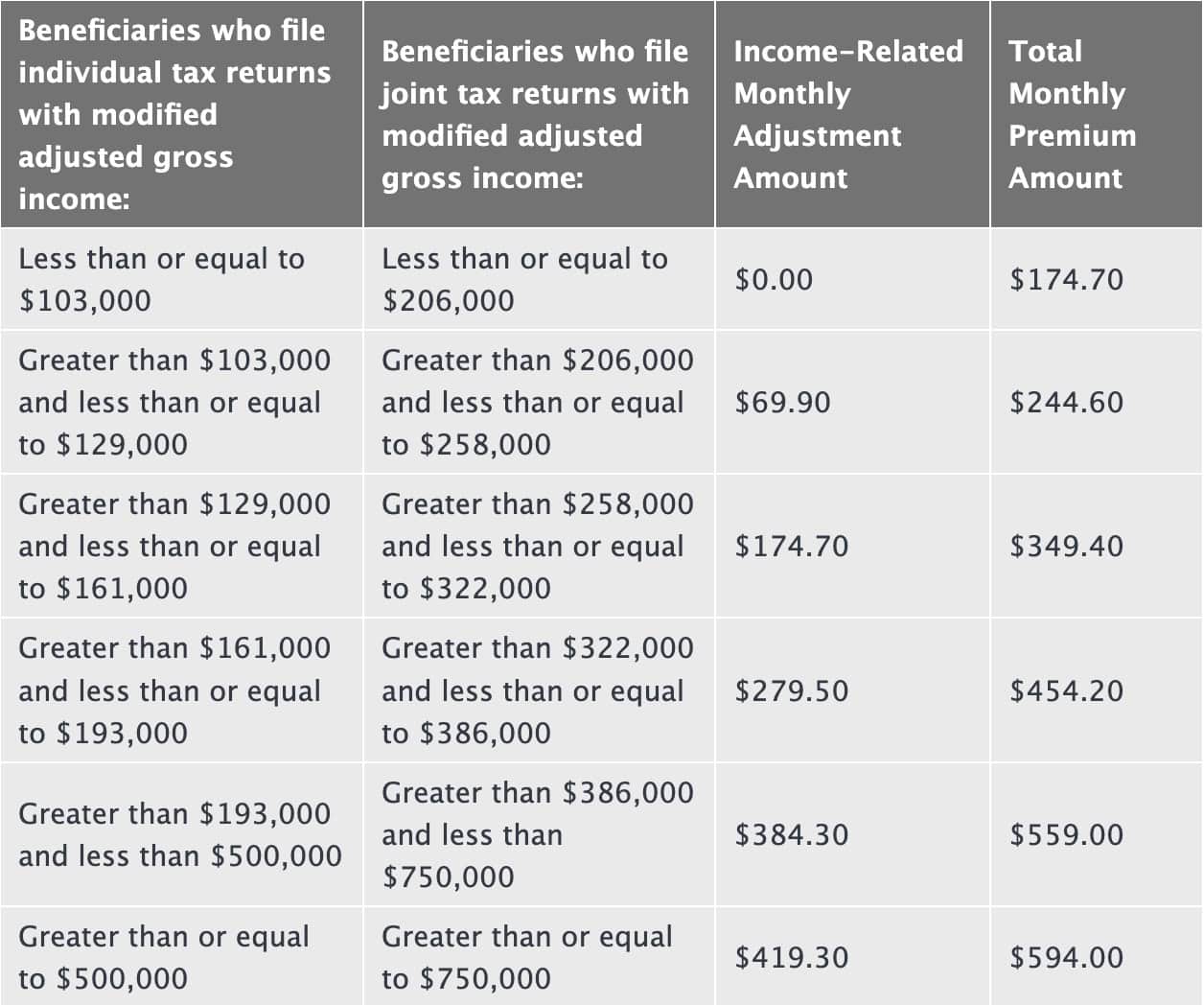

8. What are the IRMAA amounts for 2024?

The 2024 IRMAA surcharges will be calculated for most taxpayers using their 2022 MAGI (adjusted gross income plus municipal bond income). The 2024 IRMAA surcharges are as follows:

2024 Medicare Part B IRMAA

According to the Centers of Medicare and Medicaid Services, below is the 2024 Medicare Part B IRMAA schedule.

Standard premium: $174.70 (increased from $164.90 in 2023) per month.

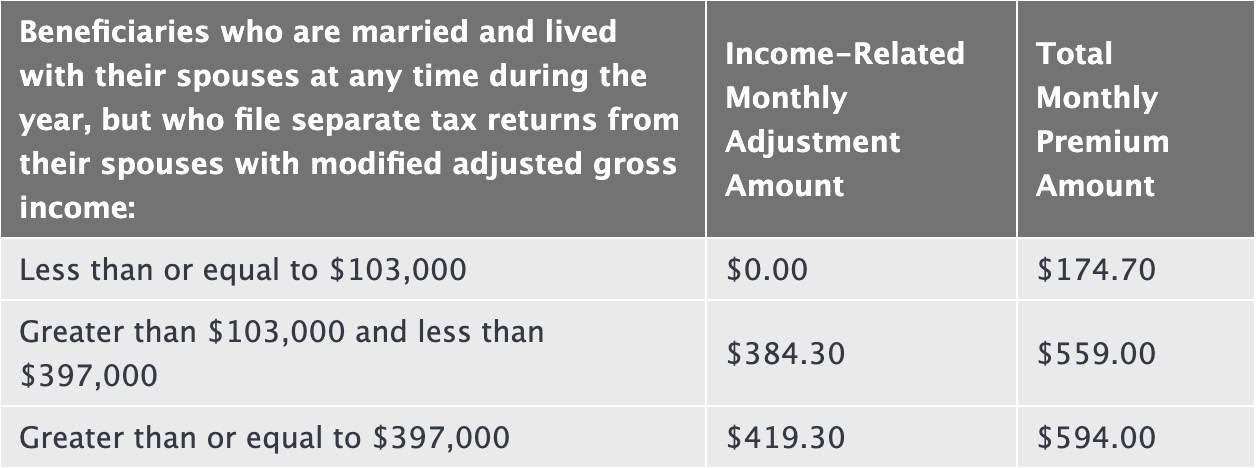

Here are the Part B premiums for married couples filing separate tax returns.

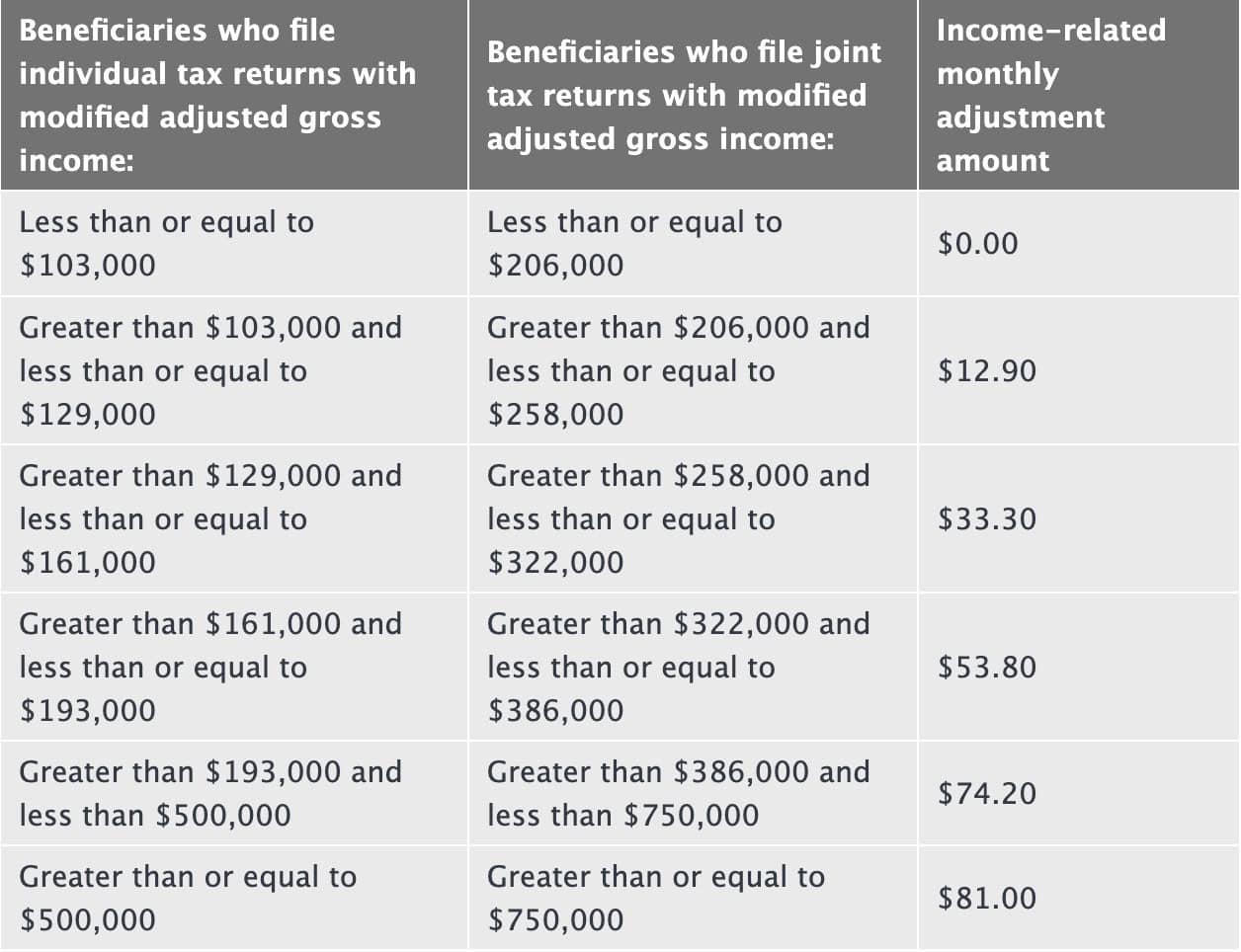

2024 Medicare Part D IRMAA

According to the Medicare website, below is the 2024 schedule for Part D IRMAA.

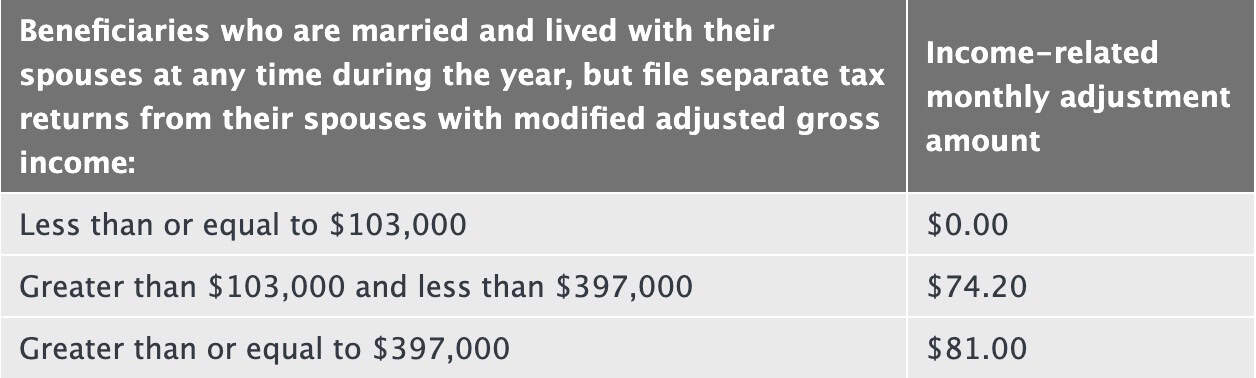

Here are the Part D premiums if you’re married filing a separate tax return.

9. What can I do if I don’t agree with my IRMAA determination?

There are several reasons you might not agree with the IRMAA determination. The SSA provides clear online guidance in the case of two of them.

IRMAA determination based upon IRS tax information that is incorrect.

This could be based upon either an amended tax return for the year that was used for the IRMAA determination, or it could be based upon an IRS error. In either case, the beneficiary will be expected to provide proof, through one of the following:

- An amended tax return

- A letter from the IRS documenting the factual data the IRS actually received & the erroneous information that the IRS provided to the SSA

- A transcript from the IRS with new information and a copy of the filed tax return for the tax year the error occurred.

For more information on using corrected or updated tax information to determine IRMAA, you can refer to the POMS HI 01120.050-Use of Corrected IRS Tax Data or contact the SSA office.

A recent life event has had (or is expected to have) significant impact to your income.

The SSA recognizes 8 life-changing events that may be used to reduce or eliminate IRMAA:

- Death of a spouse

- Marriage

- Divorce or annulment

- Work reduction

- Work stoppage

- Loss of income-producing property

- Loss of employer pension

- Receipt of settlement payment from a current or former employer

If one or more of those events occurred, you may be able to request a reconsideration of your IRMAA based upon that event. For that to occur, you would fill out Form SSA-44, Medicare Income-Related Monthly Adjustment Amount-Life Changing Event and provide the requested documentation.

This is not an appeal. It is a request for the SSA to come to a new determination based upon information that they could not have assumed from your tax return.

Appeal

If neither of these routes is effective in helping you, you can always appeal to the Office of Medicare Hearings and Appeals. Before your appeal, you must have requested a reconsideration of the IRMAA determination.

For more information, you can contact the SSA or start with the OMHA Medicare Part B Premium Appeals website.

10. What is SSA-44 and how does it affect my IRMAA?

As mentioned above, SSA-44 is the form you can use to request a new determination based upon life changes that have impacted your finances.

To help you, we’ve written a step-by-step guide to walk you through the SSA-44.

11. I received my IRMAA determination letter, but then I retired. Can I ask Social Security to change my IRMAA?

Retirement is one of the 8 life-changing events that the SSA would consider when making a new IRMAA determination. To do this, you would follow the instructions on the SSA-44.

To learn more about Form SSA 44, watch this instructional video.

12. Can Roth conversions help me avoid IRMAA?

When done as part of a deliberate Roth conversion strategy designed to reduce required minimum distributions (RMDs), Roth conversions can help you reduce or avoid IRMAA.

However, each taxpayer’s situation is different. There are many factors that might determine your taxable income, not just IRA distributions.

Some of these factors (not all of them) might include:

- How much municipal bond income you receive (Line 2a on your Form 1040)

- Whether you receive pension income

- Other sources of income (part-time job, spousal income, etc).

- Charitable contributions: Charitable contributions can help decrease your taxable income, especially qualified charitable distributions (QCDs). QCDs are charitable distributions that you can make directly from your IRA to the qualified charity of your choice. QCDs can count against your RMD, and still not count as taxable income.

- Capital gains-There are two types of capital gains worth considering

- Investments with low-basis, high capital gains-This might be stocks or mutual funds that you’ve accumulated over the years, either through an employer, family inheritance, or on your own.

- Capital gains distributions-This might be in mutual funds with high turnover. Even if you don’t sell the mutual fund, the mutual fund manager may issue distributions at the end of the year based upon capital gains that the mutual fund has accumulated.

To see how Roth conversions might help you reduce or avoid IRMAA, you should talk to your tax professional or financial advisor.

13. It looks like the SSA used 3 year old information to calculate my IRMAA even though I have a more recent tax return on file. What can I do?

It appears that this is a common occurrence. In fact, it’s common enough for the SSA procedure manual to have its own section that outlines what to do:

To summarize, this is the process by which the SSA office should verify the taxpayer’s more recent return, and use that information to re-run the IRMAA calculation.

For example, a past client asked about her 2021 IRMAA, which was calculated using 2018 tax return information, even though she and her husband had filed a 2019 tax return.

This should not require an SSA-44, because this is not considered a life-changing event. This is a completely different procedural matter that requires a different process to resolve it.

Update: Recently, a client had this conversation with the SSA on this very matter. It appears that something in the SSA’s system is automatically generating a lot of these notices, which the SSA is trying to get fixed.

Two different SSA employees told her that in the interim, the best way to resolve this is to:

- Contact the SSA office to inform them of this.

- Resubmit the SSA-44 form. If possible, put the form to the attention to the person/department you discussed this with.

Your mileage may vary. We will update this post as warranted.

14. Are Medicare IRMAA payments tax-deductible?

IRMAA payments may be tax deductible as a medical expense on your income tax return, if you itemize deductions on Schedule A.

Generally speaking, you may only deduct medical expenses on Schedule A to the extent that those medical expenses exceed 7.5% of your adjusted gross income (AGI). However, there may be many tax situations in which you are better off taking the standard deduction, even if you do have medical expenses exceeding that threshold.

For more details, you should discuss your tax situation with your tax professional or financial advisor.

15. Does Social Security count towards IRMAA?

Yes, and no.

Only the taxable portion of Social Security is applied towards IRMAA thresholds. Lower income taxpayers generally receive either:

- 100% tax-free Social Security (paying taxes on 0% of their Social Security income), or

- 50% tax-free Social Security (paying taxes on the other 50% of their Social Security income)

Usually, Social Security recipients in either of these two situations do not face IRMAA surcharges, unless a significant tax event happens.

At the highest ends of the tax picture, Social Security beneficiaries are only taxed on 85% of their Social Security. So the 15% of tax-free Social Security does not count towards IRMAA calculations for those taxpayers.

Conclusion

If you have an IRMAA question that we didn’t answer, please email us and let us know.

We had high income in 2021 (based on the sale of an asset), so my husband paid a lot of IRMAA in 2023. We never appealed the IRMAA charges. Will Social Security refund us the overpayment of IRMAA once they receive and process the data in our 2022 and 2023 returns?

If the sale of the asset was voluntary, and there were no other life-changing events (LCEs) that would qualify for a reduction/elimination of IRMAA, then I don’t think you would be able to retroactively receive a determination (and lower the IRMAA paid in 2023).

With that said, your 2024 IRMAA determination would be based on your 2022 tax return, so your Medicare premiums should have reverted back to normal. Here are links to the article and video I produced about Form SSA-44, which is the form you can look at to see if there are any other qualifying circumstances regarding your IRMAA situation:

Article: https://www.teachmepersonalfinance.com/ssa-44-instructions/

Video: https://youtu.be/YRGMQ2bMrdA

I am a widow of almost 4 years and suddenly owe 5,000 dollars plus 349 a month due to Irma. I am subject to the WEP/GPO in my state so lost all social security of my husband’s when he passed after 49 years of marriage because I was a teacher. My income increased because of distributions I had to take due to his Vanguard account doing well. I appealed and was denied. Should I appeal again and if so on what basis?

I’m sorry to hear about this, but I’m not sure there are a lot of options here. IRA distributions are not considered to be a life-changing event. However, you may consider filing Form SSA-44 based upon your husband’s passing, if you meet the other criteria.

Below are links to an article and video about Form SSA-44.

Article: https://www.teachmepersonalfinance.com/ssa-44/

Video: https://youtu.be/YRGMQ2bMrdA

I retired at 62, and started taking medicare at 65. I’m already paying an IRMAA surcharge on my Medicare Part B premium, and on my prescription drug plan premium, thru an automated deduction from my bank account to cover premium and IRMAA. Now, I’m 70 and started receiving Social Security. The social security letter said my SS payment will be reduced by an IRMAA related to my prescription drug plan. This sounds redundant, am I being charged twice for the IRMAA related to my prescription drug plan? What do I need to change to avoid paying this IRMAA twice?

If I understand this correct, it seems that you’ve been paying IRMAA on your Part B premiums for the past 5 years, and now that you’re on Part D (prescription plan), the SSA is applying IRMAA to your Part D premiums.

If that’s the case, there’s not really much that you can do. The Part D premium IRMAA surcharges are different from the Part B surcharges. However, the IRMAA tiers for each surcharge is identical. So if you’re paying Part B IRMAA, you’ll be paying Part D IRMAA at the same tier level.

If this was not your intended question, please let me know.

I’ve been under IRMA thresholds, but plan to sell some stock (take gains).

How do I handle this? Just wait and they’ll hit me in 2 years?

Can you clarify this question? Are you trying to avoid IRMAA, or is there another goal here?

Based on the below information (from your email), IRMAA for your 2026 year would not be imposed until 2028.

2025 income $200,000

2026 income $250,000 (IRMA required)

2027 income $200,000

2028 income $200,000

If IRS is looking 2 years back, the IRMA required charges required for 2026 won’t be imposed on me till 2028? Because in 2027 they are looking at 2025 income?