IRS Form 56 Instructions

A fiduciary relationship is crucial in situations where the primary taxpayer is unable to handle his or her own financial or tax matters. The fiduciary duty is also important in cases where a government authority must grant permission for assets to be distributed, such as in bankruptcy proceedings or execution of a decedent’s estate. Taxpayers use IRS Form 56 to notify the IRS of a fiduciary relationship granted to another person or entity

This article will walk you through this tax form, including:

- When you should use Form 56

- When other tax forms are more appropriate

- How to complete and file IRS Form 56

Let’s start with step by step instructions on how to complete IRS Form 56.

Table of contents

How do I complete IRS Form 56?

There are 4 parts to this two-page tax form which we’ll walk through step by step:

- Part I: Identification

- Part II: Revocation or Termination of Notice

- Part III: Court and Administrative Proceedings

- Part IV: Signature

Let’s start with Part I.

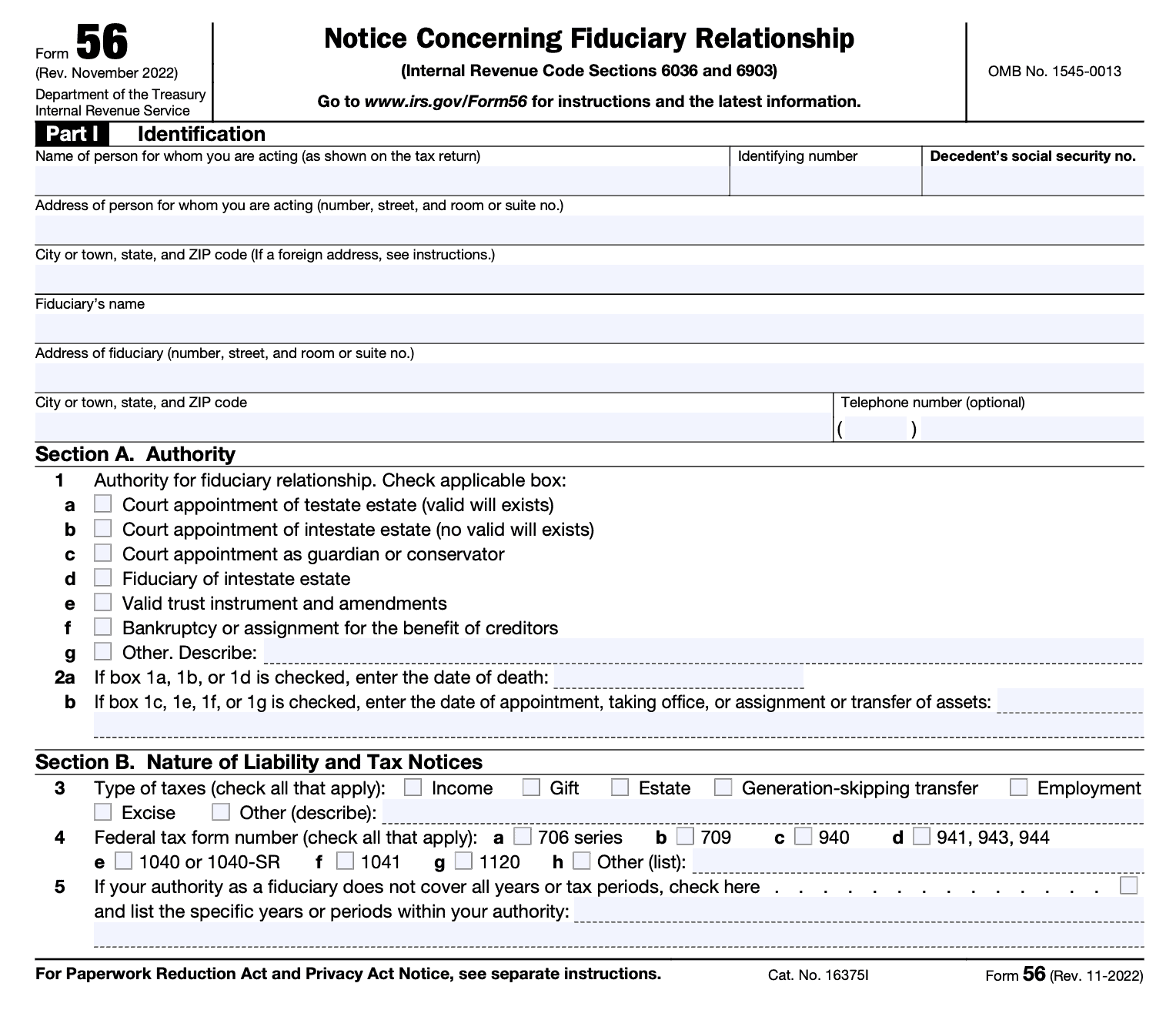

Part I: Identification

Aside from the identification fields at the top, there are also two sections to Part I:

- Section A: Authority

- Section B: Nature of Liability and Tax Notices

Let’s start with the identifying information.

Identifying information

In this field, you’ll enter all applicable information about the taxpayer and the person assuming the fiduciary duty. This includes:

- Taxpayer’s name and identifying number

- You must file a separate Form 56 for each taxpayer

- If filing a decedent’s final tax return and you are the executor of the decedent’s estate, you must file a separate form for the decedent and the decedent’s estate

- Deceased taxpayer’s Social Security number, if applicable

- Street address, including city, state, and zip code

- If the mailing address is a P.O. Box, use this only if the post office does not deliver mail to the street address

- If the address is a foreign address, list city/town, province/state, and country. Do not abbreviate the country’s name

Section A: Authority

Check the appropriate box. Below are some key points:

Testate estate

This means that a valid will exists, and an appropriate court has authorized you to perform as a representative of the decedent’s estate. Attach current letters testamentary or a court certificate as proof of your court appointment.

List the decedent’s date of death in Line 2a.

Intestate estate

The decedent passed away without a valid will in place. Attach current letters testamentary or a court certificate as proof of your court appointment.

List the decedent’s date of death in Line 2a.

Guardianship or conservator

Check this box if if a court of appropriate jurisdiction has appointed you to serve over another person or entity as one of the following:

- Guardian

- Custodian

- Conservator

Enter the date of your appointment in Box 2b.

Fiduciary of intestate estate

Only check this box if:

- There are no court-appointed representatives for the decedent’s estate, and

- You are the sole person charged with the property of the decedent.

List the decedent’s date of death in Line 2a.

Valid trust instrument and amendments

Use this if you have been appointed as a trustee of a trust in a valid trust document.

Enter the date of your appointment in Box 2b.

Bankruptcy

Use this field if you are a bankruptcy trustee or assignee for the benefit of creditors.

Enter the date of your appointment in Box 2b.

Other

Describe the authority for the fiduciary relationship in the space provided.

Also, enter the date of your appointment in Box 2b.

Section B: Nature of Liability and Tax Notices

Use these fields to describe the following:

- Type of taxes that are part of your fiduciary responsibility (Line 3)

- Type of tax forms you expect to file in your fiduciary duty (Line 4)

- Specific tax years or periods within your authority (Line 5)

- If your fiduciary duty covers all tax periods, leave the box unchecked and the lines blank

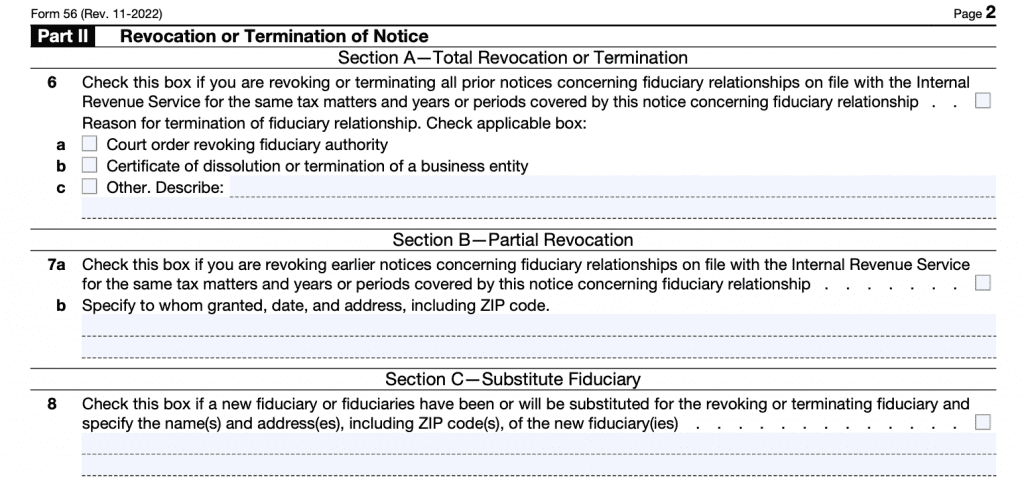

Part II: Revocation or Termination of Notice

Only complete Part II if revoking or terminating prior notices. Completing Section B or C does not relieve any new or substitute fiduciary of the requirement to give the IRS proper notice.

Section A: Total revocation or termination

Check this box to completely revoke or terminate all prior notices regarding fiduciary relationships. Also check the appropriate box for termination.

Section B: Partial revocation

Use this to revoke earlier notices, but would like to specify the tax matters, tax years, or tax periods that you wish to revoke.

Section C: Substitute fiduciary

Check this box if a new fiduciary or fiduciaries have been or will be substituted. Specify the name(s) and address(es) of the new fiduciary or fiduciaries.

Even after you select this option, new fiduciaries still must have a Form 56 on file with the IRS.

Part III: Court and Administrative Proceedings

Only complete this part if you have been appointed a receiver, trustee, or fiduciary by a court or other governmental unit in a proceeding besides a bankruptcy proceeding.

Enter the following information:

- Name of court or agency and type of proceeding

- Date of proceeding

- Address of court or proceeding location

- Docket number

- Date and time of proceedings

Part IV: Signature

Part IV contains your signature, sworn under penalties of perjury, that this document is true, correct, and complete to the best of your knowledge.

What is IRS Form 56?

IRS Form 56, Notice Concerning Fiduciary Relationship, is the tax form that provides the Internal Revenue Service:

- Proper notification of the creation or termination of a fiduciary relationship under Internal Revenue Code (IRC) Section 6903

- Notice of qualification as executor or receive as required in IRC Section 6036

Which begs the question, “What is a fiduciary relationship?”

Examples of fiduciary relationships

The IRS website cites the following examples of fiduciaries:

- Administrators

- Conservators

- Designees

- Executors

- Guardians

- Receivers

- Trustees of a trust

- Trustees in bankruptcy proceedings

- Personal representatives

- Persons in possession of property of a decedent’s estate, or

- Debtors-in-possession of assets in any bankruptcy proceeding by order of the court

Difference between fiduciary and representative

Taxpayers must inform the IRS of the creation of a fiduciary relationship for a very important reason:

The role of a fiduciary assumes a much broader authority to perform duties on behalf of the taxpayer than someone who is simply an authorized representative of the taxpayer.

The IRS treats someone acting in a fiduciary capacity as if he or she were the actual taxpayer, not merely a personal representative or someone with power of attorney privileges. This means that the fiduciary has the rights and responsibilities (such as filing proper tax returns and paying taxes owed) of the actual taxpayer.

Conversely, an appointed representative may only have duties as specifically authorized by the taxpayer. A representative is not allowed to perform any function that the taxpayer has not explicitly authorized.

When do I NOT file IRS Form 56?

The IRS form instructions state that Form 56 is erroneously used in tax matters where different tax forms are more appropriate. Below are some of the more common examples when you should not file Form 56:

Do not use IRS Form 56 when updating an address

Instead, you should use one of the following IRS forms:

- IRS Form 8822: Change of Address

- IRS Form 8822-B: Change of Address, Responsible Party-Business

Using one of these forms is the proper way to notify the IRS of a change in address of the person listed on the tax form.

Do not use IRS Form 56 if you are an authorized representative of the taxpayer

Instead, you should file IRS Form 2848, Power of Attorney and Declaration of Representative. This form grants powers to represent the taxpayer in administrative matters before the IRS. However, the IRS does not treat the representative on Form 2848 as if he or she were the taxpayer.

By using Form 2848, the taxpayer can still dictate which duties their representative is authorized to perform.

Video walkthrough

Watch this instructional video to learn more about how to notify the IRS of your fiduciary relationship.

Are you tired of dreading tax season?

If you’re like most people, you push through the stress of filing, only to be hit with a bigger bill than expected—then put it all behind you until the same cycle repeats next year.

But what if you could change the game?

Tax planning puts you in control. It’s about being proactive, not reactive—taking small, smart steps throughout the year to reduce your tax burden, increase your savings, and keep more of your hard-earned money working for you.

Here’s what effective tax planning helps you do:

✅ Avoid the surprise of a high tax bill

✅ Understand how your income and decisions affect your taxes

✅ Strategically lower your tax liability over time

Ready to make smarter tax moves?

👉 Join my free weekly tax planning newsletter and get one actionable tip every week to help you reduce your taxes legally and effectively.

Start taking control—your future self will thank you.

Frequently asked questions

You should file this form with the Internal Revenue Service center or the IRS department who normally has jurisdiction over the taxpayer’s tax issues.

According to the IRS, a fiduciary is any person in a position of confidence acting on behalf of any other person. A fiduciary assumes the powers, rights, duties, and privileges of the person or entity on whose behalf he or she is acting.

The IRS treats someone acting in a fiduciary capacity as if he or she were the actual taxpayer, not merely a personal representative or someone with power of attorney privileges. This means that the fiduciary has the rights and responsibilities (such as filing proper tax returns and paying taxes owed) of the actual taxpayer. Conversely, an appointed representative may only have duties as specifically authorized by the taxpayer. A representative is not allowed to perform any function that the taxpayer has not explicitly authorized.

Generally, the IRS recommends filing Form 56 when creating or terminating a fiduciary relationship. Specifically, receivers in receivership hearings or assignees for the benefit of creditors, should file Form 56 within 10 days of meeting with the Advisory Group Manager for the IRS center with jurisdiction over the taxpayer.

Where can I find IRS Form 56?

You can find this form on the IRS website. For your convenience, the most current version is available for download at the end of this article.

i was on disability and they put my mom in hospice she made a will out which i still have. ic cannot even remember the address of the courthous in reno.all i can remember is i showed them the death certificate and the will on a monday and they told me to pay like eighteen dollars. i do not remember getting any papers. and the next day flew into nyc from reno so i called the irs and said i am the benefiary and they told me that records are archived and do not go that far back so we cannot tell you if your mother took her Rmd I belive that is alie. i remember they gave me no documents when i gave the clerk the 18 dollars should i enclose ac opy of the will. i went to aa tax clinic and she paid no taxes but i do not remeber if she paid an rmd.that means i am responsible. noone at wells fargo 11 years ago told me about this. form. i called wells fargo to ask them if she took theRmd and they said they do not keep records that old.i am computer illiterate got shoulder injury from covid vaccine from the idiot pharmacist at walgreens. i am now a cripple and homebound another conundrum/have tardive dystonia should i go to local irs office i hate this Internet world. i have no documents just will.ineed to know if she took her rmd the irs knows.

I’m sorry you’re going through this ordeal. As the beneficiary of your mother’s estate, you should be able to obtain information about your mother’s tax history, as well as other pertinent tax information. Here is a link to the IRS website, which should contain more information to help you out. Specifically, there is a link to an IRS page that will tell you if you need to file a tax return for your mother or not (Do I need to file a tax return), and there is a page that points out considerations when doing so (How Do I File a Deceased Person’s Tax Return).

I wish you the best of luck.

https://www.irs.gov/pub/irs-utl/decedent-tax-guide.pdf

Hello,

I watched your video and read through your article above.

I need some direction regarding Form 56. Only regarding Part 1 Identification. Should be simple, yet having some issues with the IRS.

Form #1-Form 56 for the personal/individual and their personal SS#. I have listed there last known/living address according to the death certificate. I have listed the fiduciary’s name and their address.

Form #2-Form 56 for “The Estate” Jane A. Doe Estate-Identifying Number=EIN 00-1234567 Decedent’s Social Security #=000-00-0000.

Now what address do I put? The Fiduciary’s address or the still the decedents address?

On the Form 56 (Form 2) that has “Estate” on it and the EIN do the address’s need to match?

I was told yes the form that goes to the IRS the address’s need to match but what I think I am understanding from the IRS is different. I am so confused!

Another question. Do I also need to send along a 8822 form with these two F56 forms?

I received a letter back from the IRS stating “The requested fiduciary is already reflected on both the decedent’s individual (SSN) account and their estate (EIN) account, but both accounts need an address change. Please complete Form 8822, Change of Address, for the SSN account and Form 8822-B, Change of Address or Responsible Party-Business, for EIN account. Use the same old and new addresses as on Form 56.”

I hope I am making sense! Please help!

Thank you.

Melissa

It seems that the IRS is instructing you to file IRS Form 8822 (for the individual) and IRS Form 8822-B (estate) to reflect that the tax accounts have changed from the old address (presumably the decedent’s address) to the fiduciary’s address. If you’re already listed as the fiduciary, then you might not need to file Form 56 again.

Below are links to some additional info on Fom 8822 and Form 8822-B:

IRS Form 8822, Change of Address

Article: https://www.teachmepersonalfinance.com/irs-form-8822-instructions/

Video: https://youtu.be/s95SrGoFMoI

IRS Form 8822-B, Change of Address or Responsible Party, Business

Article: https://www.teachmepersonalfinance.com/irs-form-8822-b-instructions/

Video: https://youtu.be/rxG-TBidBP4

Thank you Forrest. Do I have to fill out two F-56 forms? One with the decedent’s name, address, and social security number and one with the decedent’s name along with the word ESTATE after their name and their EIN number and SS#, to identify the individual and the estate separately?

Or does one form take care of that?

Thank you.

Melissa

Melissa,

According to the form instructions, a decedent’s estate is a taxable entity separate from the decedent that comes into existence at the time of the decedent’s death. Further in the instructions, they tell you to create 2 forms

“if you will be filing the decedent’s final Form 1040 and are the executor/administrator of the decedent’s estate, file one Form 56 entering the name of the decedent as the person for whom you are acting and file one Form 56 entering the name of the estate as the name of the person for whom you are acting.”

If you complete the forms as you outlined above, you should be all right.

Can you share where exactly the Form 56 should be mailed to? I can’t find an address to do this to save my life.

According to the form instructions: “File Form 56 with the Internal Revenue Service Center where the person for whom you are acting is required to file tax returns.”

With that understanding, the IRS website contains specific filing addresses for each type of tax return (i.e. 1040, 1120, 941, etc). This link gives an overview, then provides links to specific pages containing ‘Where to file’ information based upon the type of tax return:

https://www.irs.gov/filing/where-to-file-paper-tax-returns-with-or-without-a-payment

Could you please clarify about the type of taxes and forms to check in sections B3 and B4, on the two forms 56, one for decedent’s final 1040 (lets call that instance A) and the form 56 for the court appointed executor (lets call that instance B) when selecting type of taxes and forms to be filed, such as 1041, 706. Will the gov expect all forms checked to actually be filed, if it turns out they are not required, such as form 1041, form 706, estate tax return, and should generation-skipping transfer be checked on the form 56 for the estate, if the will leaves real estate to a grandchild? Are you required to file a form 706 as well in that case? (and no such generation skipping transfer was made while the deceased was alive?)

For “Instance A” should section B3 check just Income, and is it also OK to check gift even if no gift tax form is ultimately filed, but perhaps it needs to be checked to later request, by an other applicable method, the decendent’s history of gifts reported. Also in “Instance A”, would Estate be checked in sec. B3, or only in “Instance B”? If filing for an extension of any of the tax forms should that be noted in sec. B4- h other? Should an extension for the estate tax be filed, even if it turns out it isn’t required to be filed? Can you get an extension for filing the form that reports generation-skipping transfer of real property that occurs via the decedent’s will? Is it reported in the year the decedent died or in the following year that the actual transfer of the deed to the grandchild occurs?

Also in Sec. A, Authority when only checking Sec.1a -Court appt. of testate estate (valid will exists), is it only necessary to check 2a and enter date of death? or should 2b the date of appt. as the executor also be checked?

With the above Authority selected, then in Part III is the probate court Court name and address entered, and for “date proceeding initiated”, is it the date the petition was submitted to the court for formal probate of a will plus appointment of personal representative (as they call the executor now in MA), same date for both, or should it be the date the will and personal representative (aka executor) were actully appointed, called the “Decree and Order on Petition”? or should appt date go in boxes for date and time? Note: The date of the decree and order on petition and the date letters authority issued to the executor being the same, with no “Time” listed on the doc, just the date. It being all procedural by the probate office without an actual hearing with external input conducted, there having been no objections.

Also in Instance A on the form 56 for decedent’s final 1040. Can I enter only decedent’s social security number? Does the court appointed executor have to enter their own SS # too? In Instance B for the estate name, its estate EIN and decendent’s SS#, from what I gather.

Thank you for your help.

This is a lot, and I’m not sure that I have enough information to guide you here. I’ll outline some basic points to consider below:

1. Do you need to file Form 56 for a decedent’s final return? You might not have to. Here’s a link to the IRS page with more information: https://www.irs.gov/individuals/file-the-final-income-tax-returns-of-a-deceased-person

2. Would the government expect you to file tax returns simply because you’re the court appointed executor? Not necessarily. For most estates, particularly under the estate tax threshold, Form 706 is not required. Form 1041 is generally only required in cases where the estate is complicated enough to have significant amounts of income, or the income is retained based upon the directions of the estate or trust, or if assets will be retained for an extraordinary amount of time. Most estates are distributed quickly enough to not warrant filing Form 1041.

My general advice is that if the estate is complicated enough to warrant a Form 706 or Form 1041, you should hire a tax professional to prepare these returns. The estate (or if a trust is created, then the trust) would be able to pay for the costs of tax preparation, as well as associated accounting or legal costs.

In Section A of the Form 56, you would check Line 1a, then enter the date of death in 2a. You do not need to enter anything in 2b unless you checked Line 1c, 1e, 1f, or 1g. If you completed Section A as the executor or PR, then I don’t believe you need to complete Part III.

I’m sure that there’s a question that I missed here, but in most situations, many of these questions aren’t applicable (i.e. most estates where assets are distributed relatively quickly-1 year or less). If there are still questions that apply, please let me know.