IRS Form 1128 Instructions

If you’re a taxpayer looking to change your tax year, you generally need to request approval from the Internal Revenue Service by filing IRS Form 1128.

In this article, we’ll walk through everything you need to know about this tax form, including:

- How to complete and file IRS Form 1128

- Specific requirements for each type of taxpayer entity

- Differences between automatic approval requests and ruling requests

Let’s start by going through this tax form.

Table of contents

How do I complete IRS Form 1128?

There are three parts to this tax form:

Let’s start at the top of Part I.

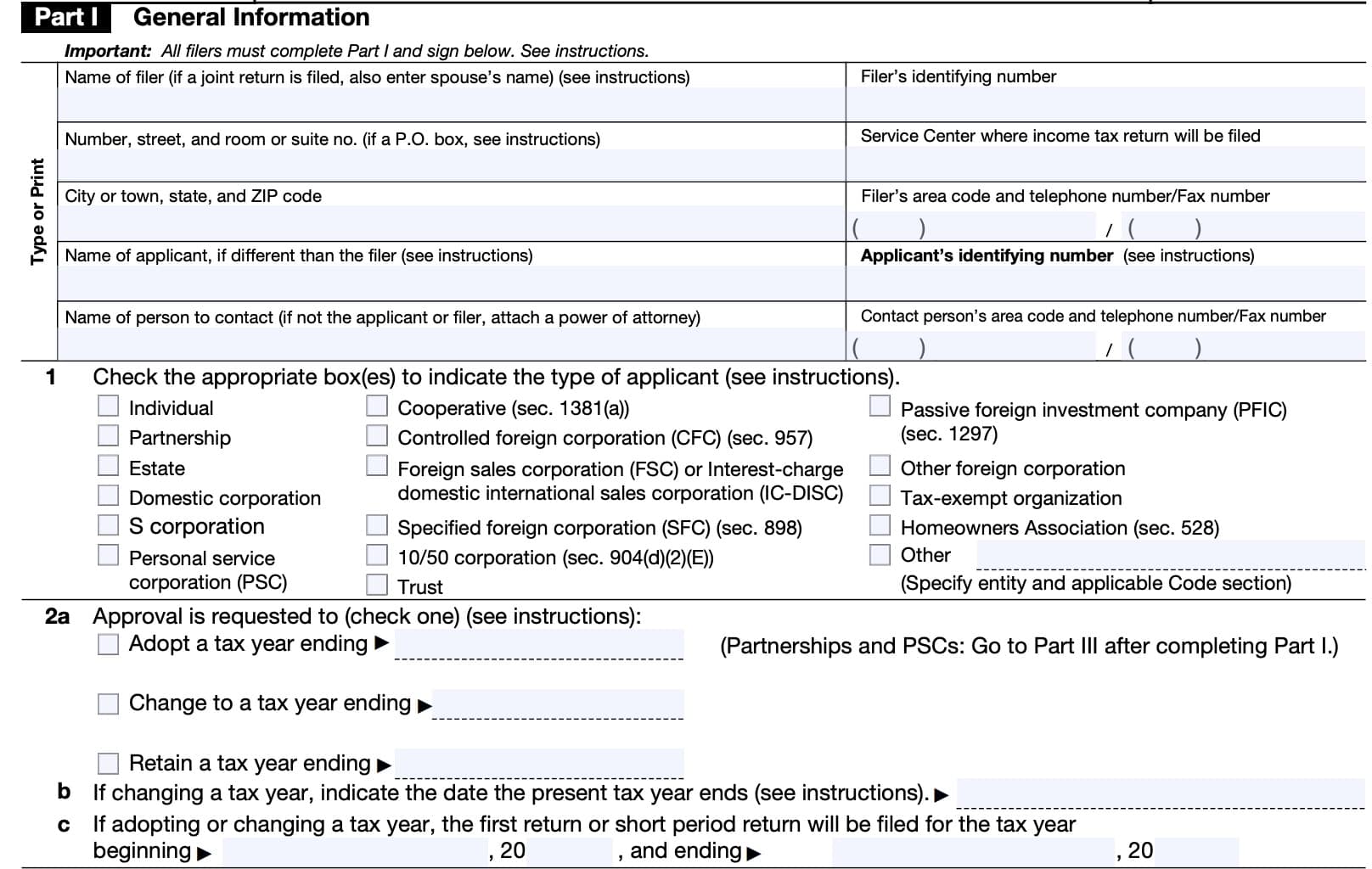

Part I: General Information

All filers must complete Part I, as well as the signature section at the end of Part I. Let’s start at the top, with the taxpayer information fields.

Taxpayer information

Let’s go over each line in this field, step by step.

Name of filer

In general, the filer of the form is the applicant. If you are filing a joint return, you will need to include

the names of both spouses.

If the applicant is a corporation, partnership, estate, trust, or tax-exempt organization, etc., enter the name of the entity or organization.

Filer’s identifying number

Individuals must enter their Social Security number (SSN) as the identifying number.

If filing a joint tax return, you should enter the SSN for both spouses, except if:

- One or both spouses are engaged in a trade or business, and

- IRS Form 1128 is being filed on behalf of the business

In this situation, enter the employer identification number (EIN) instead of SSNs. All other types of entities must enter an EIN.

Obtaining an EIN

If you are required to enter an EIN but you do not have one, you can apply online or by filing Form SS-4, Application for Employer Identification Number.

If you’ve already applied for an EIN but have not received it by the time you file this form, you may enter, ‘Applied For’ in the identifying number field.

Obtaining an SSN

If you are required to enter an SSN but you do not have one, you can apply by filing Form SS-5, Application for Social Security Card.

If you’ve already applied for an SSN but have not received it by the time you file this form, you may enter, ‘Applied For’ in the identifying number field.

Address

Enter the street address. If there is a suite, room, or office number, include that information after the street address.

For taxpayers with an address that the United States Postal Service (USPS) does not deliver mail to, you may enter a Post Office box number instead.

If the filer receives mail in care of a third party, such as an attorney or accountant, enter ‘C/O’ followed by the third party’s name and address.

Service center where tax return will be filed

Enter the service center location where you or the tax entity plan to file income tax returns.

Filer’s telephone number

Enter the telephone number for the filer.

Applicant’s information

In situations involving consolidated corporations, certain foreign corporations, Form 1128 may be filed on behalf of an applicant.

Consolidated corporations

For a consolidated group of corporations, enter the following:

- First line: Name and EIN of the parent corporation (as the filer)

- Fourth line: Name(s) and EIN(s) of member corporations (as applicants)

CFCs & 10/50 corporations

For CFCs and 10/50 corporations, enter the following:

- First line: Name and EIN of the controlling domestic shareholder(s), or common parent (as the filer)

- Fourth line: Name and EIN of the foreign corporation (as applicants)

Contact person

The contact person must be either authorized to sign IRS Form 1128, or the applicant’s authorized representative.

If the contact person is not the filer or applicant, then attach a completed IRS Form 2848, Power of Attorney and Declaration of Representative to IRS Form 1128.

Line 1: Type of applicant

Check all boxes that apply. There may be more than one applicable box.

Line 2a

In Line 2a, check one of the following:

- Adopt a tax year ending on (insert preferred date)

- Change to a tax year ending on (insert preferred date)

- Retain a tax year ending on (insert preferred date)

If the requested year is a 52-53 week tax year, then describe the year. Examples could include:

- Last Saturday in December

- Saturday closes to December 31

A 52-53-week tax year must end on the date:

- That a specified day of the week last occurs in a particular month, or

- That day of the week occurs nearest to the last day of any month

Line 2b

If you are changing tax years, enter the date that the present tax year ends.

Line 2c

If adopting or changing a tax year, enter the beginning and ending dates for the tax year that the first federal income tax return or short tax period return will be filed.

A newly formed partnership or PSC that wants to adopt a tax year other than its required tax year must go to Part III after completing Part I.

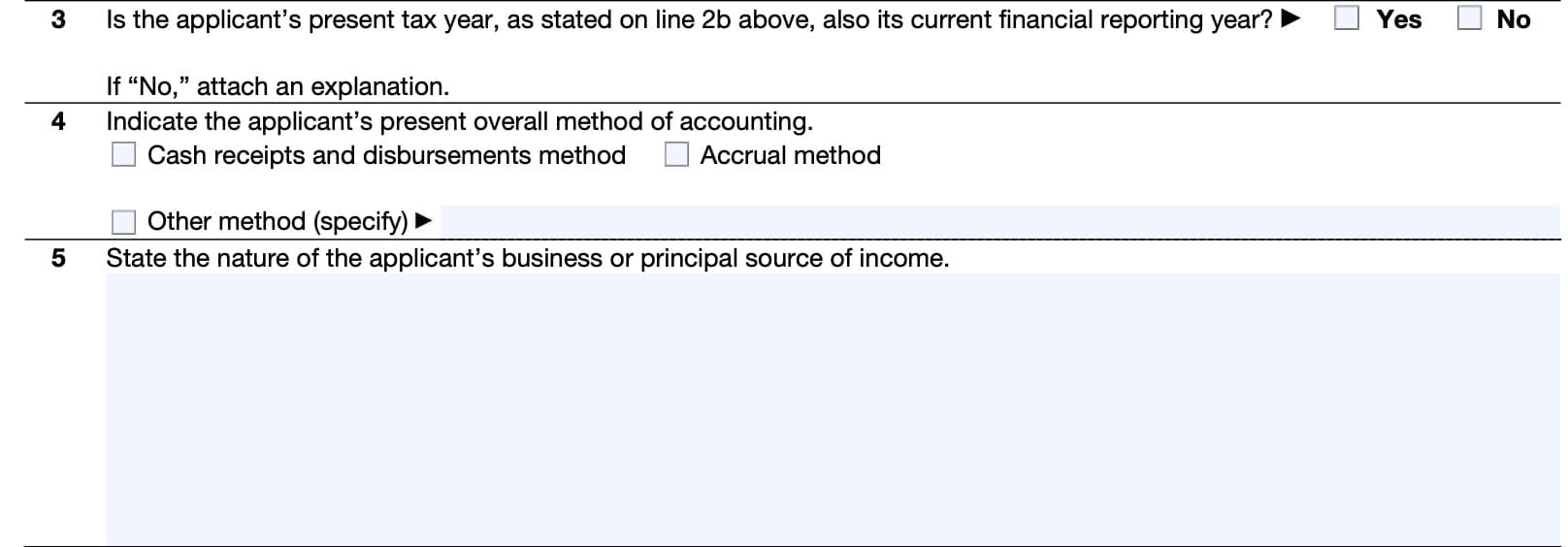

Line 3

Is the applicant’s present tax year, stated on Line 2b, also the current financial reporting year?

If not, attach a written explanation.

All attachments must include:

- Applicant’s name

- Applicant’s identifying number & address

- An indication that the statement is an attachment to IRS Form 1128

Line 4

Enter the applicant’s present accounting method:

- Cash receipts and disbursement method (known as the cash basis method)

- Accrual basis method

- Another method (specify the type of method in the space provided, such as the hybrid method)

Line 5

In Line 5, state the nature of the applicant’s business or primary source of income.

Part II: Automatic Approval Request

Part II is completed by applicants requesting an automatic change in tax year under one of the following IRS Revenue Procedures:

- Corporations: Revenue Procedure 2006-45, as modified by Revenue Procedure 2007-64

- Pass-through entities: Revenue Procedure 2006-46

- Individuals: Revenue Procedure 2003-62

- Tax exempt organizations: Revenue Procedure 76-10, as modified by:

There are 4 sections to Part II that correspond to each of the applicable revenue procedures:

- Section A: Corporations

- Section B: Partnerships, S Corporations, Personal Service Corporations, and Trusts

- Section C: Individuals

- Section D: Tax Exempt Organizations

Each taxpayer only needs to complete the section that corresponds to their status. But before proceeding to the applicable section, enter the Revenue Procedure that applies to this automatic approval request in the space provided above Section A.

Section A: Corporations

Rev. Proc. 2006-45 provides exclusive procedures for a C corporation to obtain automatic approval to change its annual accounting period under Internal Revenue Code Section 442 and Treasury Regulations Section 1.442-1(b).

A corporation complying with all the applicable provisions of this revenue procedure will be deemed to have established a substantial business purpose and obtained IRS approval for the accounting period change.

In Section A, corporations (not counting pass through entities or personal service corporations) will answer three Yes/No questions.

Line 1

Is the applicant a corporation (to include homeowners associations under IRC Section 528) that is:

- Requesting a change in tax year, and

- Allowed to use automatic approval rules under Section 4 of Revenue Procedure 2006-45 or its successor?

Automatic approval rules

A corporation is not allowed to use automatic approval rules if it:

- Has changed its annual accounting period at any time within the most recent 48-month period ending with the last month of the requested tax year

- Revenue Procedure 2006-45, Section 4.02(1) contains exceptions

- Has an interest in a pass-through entity as of the short period

- Revenue Procedure 2006-45, Section 4.02(2) contains exceptions

- Is a shareholder of an FSC or IC-DISC at the end of the short period

- Revenue Procedure 2006-45, Section 4.02(3) contains exceptions

- Is an FSC or IC-DISC

- Is an S corporation or attempts to make an S corporation election for the tax year immediately following the short period, unless the change is to a permitted tax year

- Is a personal service corporation (PSC)

- Is a CFC

- Revenue Procedure 2006-45, Section 4.02(8) contains exceptions

- Is a tax-exempt organization other than one exempt under:

- Is a cooperative association (under IRC Section 1381(a)) with a loss in the short period required to effect the change of accounting period, unless

- Patrons of the cooperative are substantially the same in the year before, short period, and in the year following the change

- Is a corporation leaving a consolidated group (Revenue Procedure 2007-64 contains details)

- Has a required tax year, unless the corporation is changing to the required tax year and is not otherwise described above.

the answer is Yes

If the answer to this question is Yes, then sign IRS Form 1128 and file the completed form at the address where the applicant’s income tax return is normally filed with:

Internal Revenue Service Center

Attention: Entity Control

Also attach a copy of the completed Form 1128 to the short period income tax return. Do not complete Part III.

If the answer is No

Go to Part III.

Line 2

Does the corporation intend to elect to be an S-corporation for the tax year immediately following the short period?

the answer is Yes

File Form 1128 as an attachment to IRS Form 2553.

the answer is No

Go to Line 3.

Line 3

Is the applicant a corporation requesting a concurrent change for a CFC, FSC or IC-DISC?

If a corporation’s interest in a pass-through entity, CFC, FSC, or IC-DISC (related entity) is disregarded under section 4.02(2) or 4.02(3) of Rev. Proc. 2006-45 because the related entity must change its tax year to the corporation’s new tax year (or, in the case of a CFC, to a tax year beginning one month earlier than the corporation’s new tax year), the related entity must change its tax year concurrently with the corporation’s change in tax year, under Rev. Proc. 2006-45.

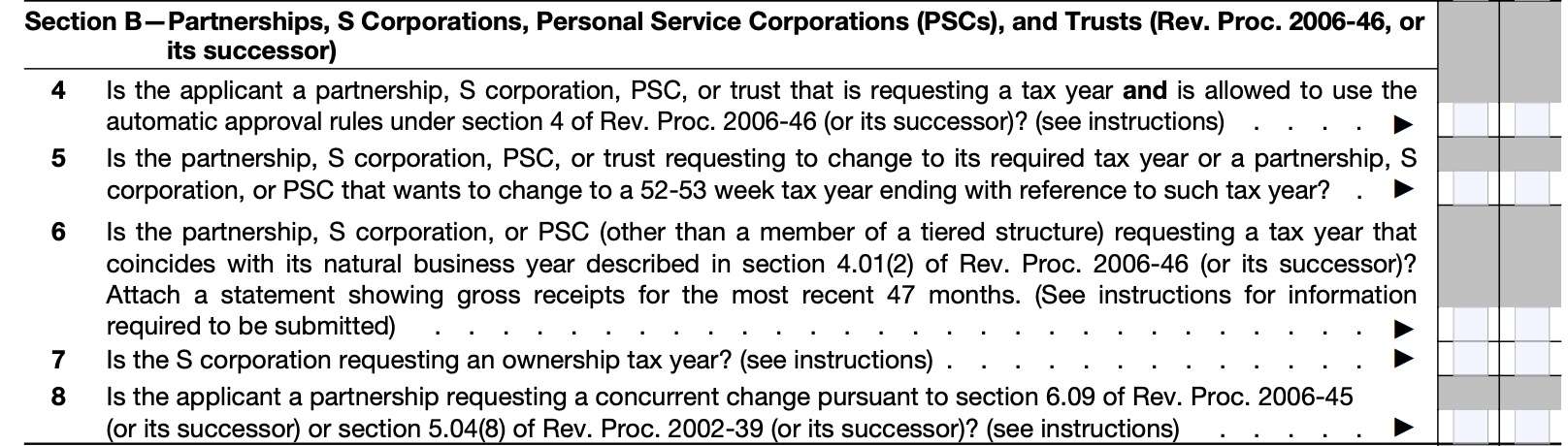

Section B: Partnerships, S Corporations, Personal Service Corporations, and Trusts

Revenue Procedure 2006-46 provides exclusive procedures for a partnership, S corporation, PSC, or trust within its scope to adopt, change, or retain its annual accounting period under

Revenue Procedure 2006-46 generally applies to trusts that are using an incorrect tax year and want to change to the required calendar tax year.

However, exceptions apply to the following:

- Trusts exempt from taxation under IRC Section 501(a)

- Charitable trusts described in IRC Section 4947(a)(1)

- Grantor trusts under Revenue Ruling 90-55

Line 4

Is the applicant a partnership, S corporation, PSC, or trust that is:

- Requesting a tax year, and

- Allowed to use automatic approval rules under Section 4 of Revenue Procedure 2006-46 or its successor?

Automatic approval rules

A partnership, S corporation, PSC or trust cannot use the automatic approval rules if the entity has changed its annual accounting period at any time within the most recent 48-month period ending with the last month of the requested tax year.

For this purpose, the following are not considered prior changes in an annual accounting method:

- A change to a required tax year or ownership tax year

- A change from a 52-53 week tax year to a non-52-53 week tax year that ends with reference to the same calendar month (or vice versa), or

- A change in accounting period by an S corporation or PSC in order to comply with common tax year requirements outlined in Treasury Regulations 1.1502-75(d)(3)(v) and 1.1502-76(a)

A partnership, S corporation, PSC, or trust cannot use the automatic approval rules under

Section 4 if any of the following apply:

- The entity is under examination, unless it complies with the procedures provided in Revenue Procedure 2006-46, Section 7.03(1)

- The entity is before an appeals office or a federal court with respect to any income tax issue and its annual accounting period is an issue under consideration by the appeals office or the federal court.

- On the date the partnership or S corporation would otherwise file its application, the partnership’s or S corporation’s annual accounting period is:

- An issue under consideration in the examination of a partner’s or shareholder’s federal income tax return, or

- An issue under consideration by an area office or by a federal court with respect to a partner’s or shareholder’s federal income tax return

Entities that are ineligible to use the automatic approval rules for one of the above reasons (not including change in accounting method) may still be able to use them if they apply the additional procedures outlined next.

Additional procedures

Additional procedures may apply that would allow an entity to use the automatic approval rules, provided they follow the corresponding guidance.

If the applicant is under examination, and has obtained the consent of the appropriate director to the change or retention of the applicant’s accounting method:

- The applicant must attach a statement from the director consenting to the change or retention to the completed application

- Applicant must also provide a copy of the application to the director as it is filed

- Must contain the name and phone numbers of the examination agent(s)

The applicant is before an appeals office and the annual accounting period is not an issue under consideration:

- The applicant must attach a separate statement certifying that the annual accounting period is not under consideration, to the best of the applicant’s knowledge

- The applicant must also provide a copy of the application to the appeals officer as it is filed

- Must contain the name and telephone number of the appeals officer

If the applicant is before a federal court and the annual accounting period is not an issue under consideration:

- The applicant must attach a separate statement certifying that the annual accounting period is not under consideration, to the best of the applicant’s knowledge

- The applicant must also provide a copy of the application to government counsel as it is filed

- Must contain the name and telephone number of the government counsel

If the answer is Yes

In a situation where the answer to Line 4 is ‘Yes,’ and the answers to the rest of Section B are ‘Yes,’

- Sign IRS Form 1128

- File your completed form with the IRS Center where you normally file your tax return, marked with ‘Internal Revenue Service Center, Attention: Entity Control‘

- Do not complete Part III

Go to Part III if the answer to Line 5, Line 6, or Line 7 is no.

If the answer is No

Do not complete Part III if the answer to the question on Line 4 is ‘No’ because the applicant (or a partner or shareholder) is:

- Under examination and has not obtained the appropriate director’s consent, or

- Before an appeals office or federal court and the annual accounting period is under consideration

If the answer is ‘No’ solely because of a prior change in accounting period, complete Section B, then proceed to Part III.

Line 5

Is the partnership, S corporation, PSC, or trust requesting to change to its required tax year or a partnership, S corporation, or PSC that wants to change to a 52-53 week tax year ending with reference to such tax year?

Answer ‘Yes’ or ‘No.’

Line 6

Is the partnership, S corporation, or PSC (other than a member of a tiered structure) requesting a tax year that coincides with its natural business year described in Section 4.01(2) of Revenue Procedure 2006-46 (or its successor)?

If so, attach a statement showing gross receipts for the most recent 47 consecutive months.

Natural business year

A partnership, S corporation, electing S corporation, or PSC establishes a “natural business year” under Rev. Proc. 2006-46 by satisfying the “25-percent gross receipts test.”

The applicant must supply its gross receipts for the most recent 47 months (or for any predecessor) to compute the 25-percent gross receipts test.

The IRS Form 1128 Instructions contain additional information on how to compute the 25% gross receipts test.

Line 7

Is the S corporation requesting an ownership tax year? Indicate ‘Yes’ or ‘No.’

For an S corporation, an “ownership tax year” is the tax year other than a calendar year that, as of the first day of the first effective year, constitutes the tax year of one or more shareholders (including any shareholder that concurrently changes to such tax year) holding more than 50 percent of the corporation’s issued and outstanding shares of stock.

Line 8

Is the applicant a partnership requesting a concurrent change pursuant to either:

- Revenue Procedure 2006-45, Section 6.09, or

- Revenue Procedure 2002-39, Section 5.04(8)

Answer ‘Yes’ if the partnership is a related entity that must concurrently change its tax year as a term and condition of the approval of the taxpayer’s request to change its tax year.

Section C: Individuals

Line 9

Is the applicant an individual requesting a change from a fiscal year to a calendar year?

If the answer to this question is “Yes,” and the restrictions of Section 4.02 of Revenue Procedure 2003-62 (or its successor) do not apply:

- Sign IRS Form 1128

- File your completed form with the IRS Center where you normally file your tax return, marked with ‘Internal Revenue Service Center, Attention: Entity Control‘

- Do not complete Part III

If the answer is ‘No,’ go to Part III.

Section D: Tax Exempt Organizations

Line 10

Is the applicant a tax-exempt organization requesting a change?

If the answer to this question is ‘Yes,’ and the organization is either a:

- Section 501(a) organization to which Revenue Procedure 85-58 Section 3.03 applies, or

- Central organization to which Revenue Procedure 76-10 applies

Sign IRS Form 1128, send the completed form to the IRS center where you normally file your tax return, marked: ‘Internal Revenue Service Center, Attention: Entity Control.’

Part III: Ruling Request

Part III is completed only by applicants requesting to adopt, change, or retain a tax year that cannot use the automatic procedures listed in Part II.

There are 8 sections to Part III:

- Section A: General Information

- Section B: Corporations

- Section C: S Corporations

- Section D: Partnerships

- Section E: Controlled Foreign Corporations (CFCs)

- Section F: Tax-exempt Organizations

- Section G: Estates

- Section H: Passive Foreign Investment Companies

All applicants must complete Section A, below, as well as any other section that applies to them. Below is a quick reference point to understand which sections are required:

| If the applicant is… | Complete only |

| A C corporation (other than 10/50 or CFC) | Sections A & B, plus any other applicable section |

| An S corporation | Sections A & C |

| A partnership | Sections A & D |

| An estate | Sections A & G |

| An individual | Section A only |

| A CFC or 10/50 corporation | Section A & E |

If Part III is required, file Form 1128 and the appropriate user fee with the IRS National Office.

Mail Form 1128 to:

Internal Revenue Service

Associate Chief Counsel (Income Tax and Accounting)

Attention: CC:PA:LPD:DRU

P.O. Box 7604

Ben Franklin Station

Washington, DC 20044-7604

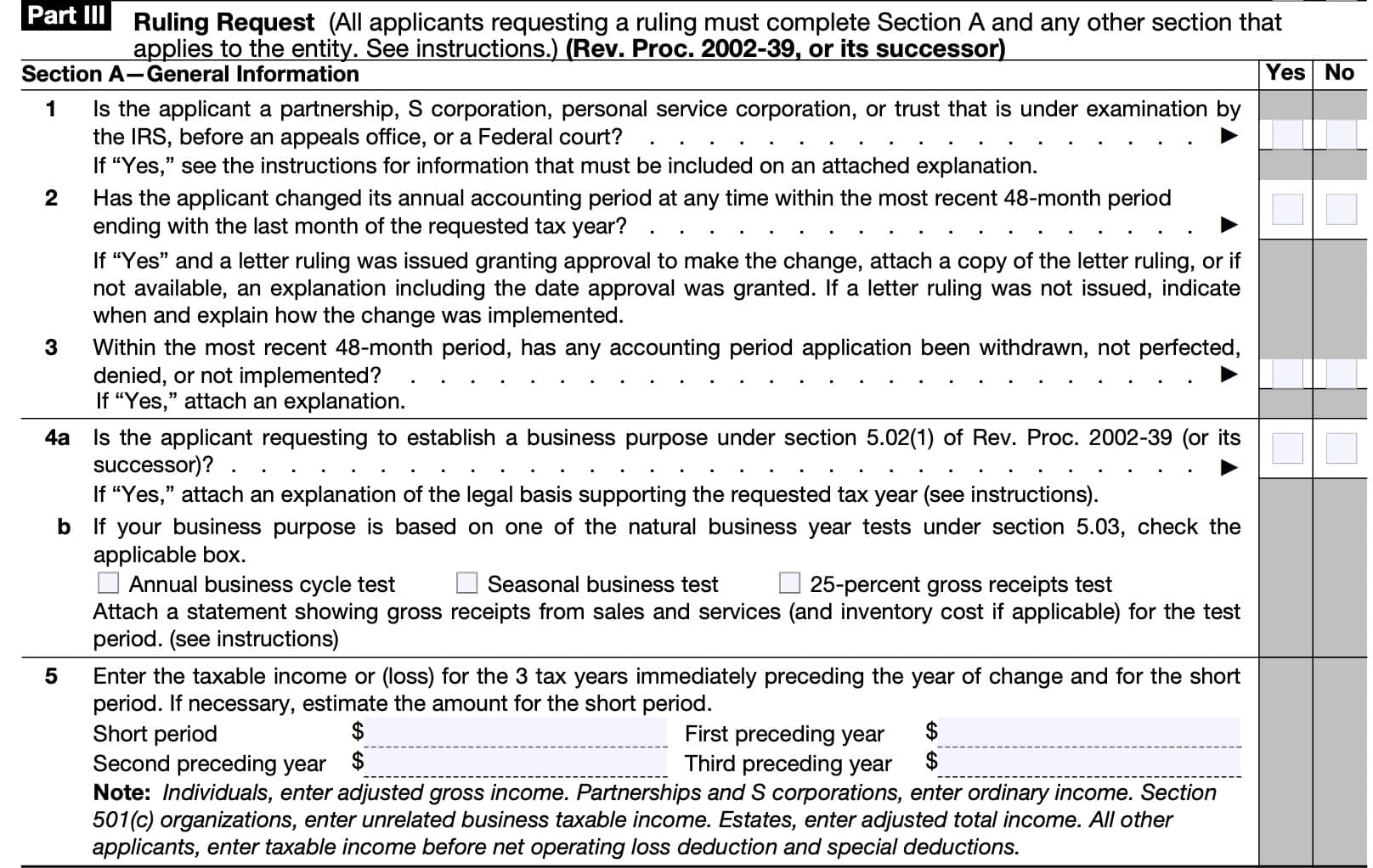

Section A: General Information

Line 1

Is the applicant a partnership, S corporation, personal service corporation, or trust that is under examination by the IRS, before an appeals office, or a Federal court?

If so, then you must follow the additional procedures outlined below.

If the applicant is under examination, and has obtained the consent of the appropriate director to the change or retention of the applicant’s accounting method:

- The applicant must attach a statement from the director consenting to the change or retention to the completed application

- Applicant must also provide a copy of the application to the director as it is filed

- Must contain the name and phone numbers of the examination agent(s)

The applicant is before an appeals office and the annual accounting period is not an issue under consideration:

- The applicant must attach a separate statement certifying that the annual accounting period is not under consideration, to the best of the applicant’s knowledge

- The applicant must also provide a copy of the application to the appeals officer as it is filed

- Must contain the name and telephone number of the appeals officer

If the applicant is before a federal court and the annual accounting period is not an issue under consideration:

- The applicant must attach a separate statement certifying that the annual accounting period is not under consideration, to the best of the applicant’s knowledge

- The applicant must also provide a copy of the application to government counsel as it is filed

- Must contain the name and telephone number of the government counsel

Line 2

Has the applicant changed its annual accounting period at any time within the most recent 48-month period ending with the last month of the requested tax year?

If the answer is ‘Yes’ and a letter ruling was issued that approves the change, then you must attach a copy of the letter ruling. If the letter ruling is not available, attach a written explanation including the date that the IRS granted approval.

If a letter ruling was not issued, indicate when and how the change was implemented in a separate statement.

Line 3

Within the most recent 48-month period, has any accounting period application been withdrawn, not perfected, denied, or not implemented?

If you answer ‘yes,’ attach an explanation.

Line 4a: Is the applicant requesting to establish a business purpose under Revenue Procedure 2002-39, Section 5.02(1), or its successor?

As applicable, attach an explanation of the legal basis supporting the requested tax year. Include all authority supporting the requested year, such as statutes, regulations, etc. Also, include all relevant facts and circumstances that may establish a business purpose.

Line 4b

If your business purpose is based on one of the natural business year tests under Section 5.03, check the applicable box:

- Annual business cycle test

- Seasonal business test

- 25% gross receipts test

Also, attach a statement showing gross receipts from sales and services (and inventory cost, if applicable), for the test period.

If the request is to establish a natural business year under the annual business cycle test or seasonal business test rules, you must provide gross receipts from sales or services for:

- Each month in the requested short period, and

- Each month of the three immediately preceding tax years

If the request is to establish a natural business year under the 25% gross receipts test rules, then you must supply gross receipts for the most recent 47 months.

Line 5

In the space provided, enter the taxable income or loss for the short period and the three tax years immediately preceding the short period.

Enter the following, based upon your taxpayer status:

- Individual taxpayers: Use adjusted gross income (AGI)

- Partnerships & S corporations: Use ordinary income

- Section 501(c) organizations: Use unrelated business taxable income

- Estates: Use adjusted total income

- All other applicants: Use taxable income before net operating loss (NOL) deduction and special deductions

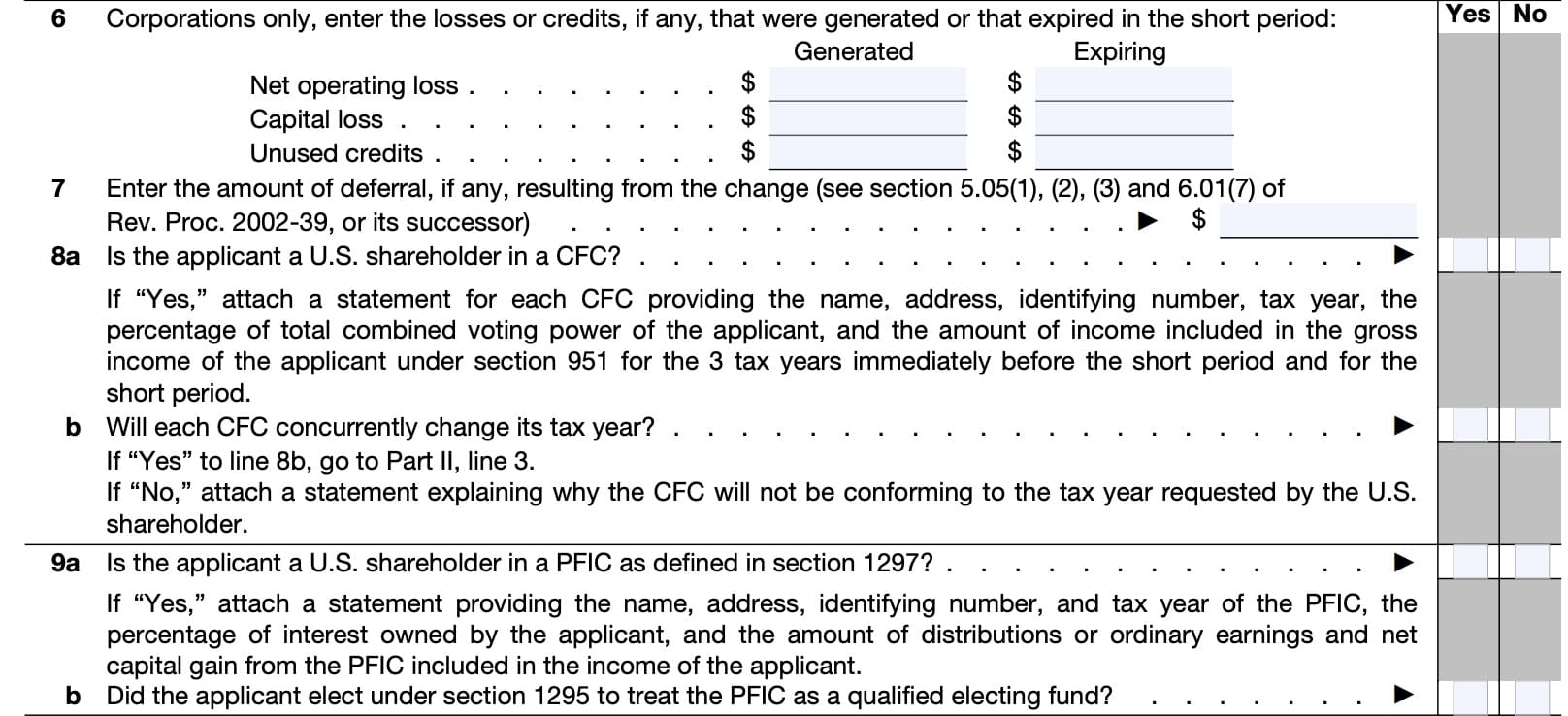

Line 6

Only corporations need to complete Line 6. Enter losses or credits that were either generated or that expired in the short period:

- Net operating loss

- Capital loss

- Unused credits

Line 7

Enter the amount of tax deferral, if applicable, that resulted from the change.

Line 8a

Is the applicant a U.S. shareholder in a CFC?

If ‘Yes,’ attach a statement for each CFC that provides:

- Name

- Address

- Identifying number

- Tax year

- Percentage of applicant’s total combined voting power

- Amount of income included in the gross income under Section 951 for the short period and the three years immediately preceding the short period

Then go to Line 8b. Otherwise, go to Line 9a.

Line 8b

Will each CFC concurrently change its tax year? If the answer is ‘Yes,’ go to Part II, Line 3. If not, attach a statement that explains why the CFC will not conform to the tax year requested by the shareholder.

Line 9a

Is the applicant a U.S. shareholder in a passive foreign investment company (PFIC) as defined in IRC Section 1297?

If so, attach a statement with the following information:

- Name, address, identifying number, and tax year of the PFIC

- Percentage of interest owned by the applicant

- Amount of distributions or earnings and net capital gain included in the applicant’s income

Line 9b

Did the applicant elect under IRC Section 1295 to treat the PFIC as a qualified electing fund?

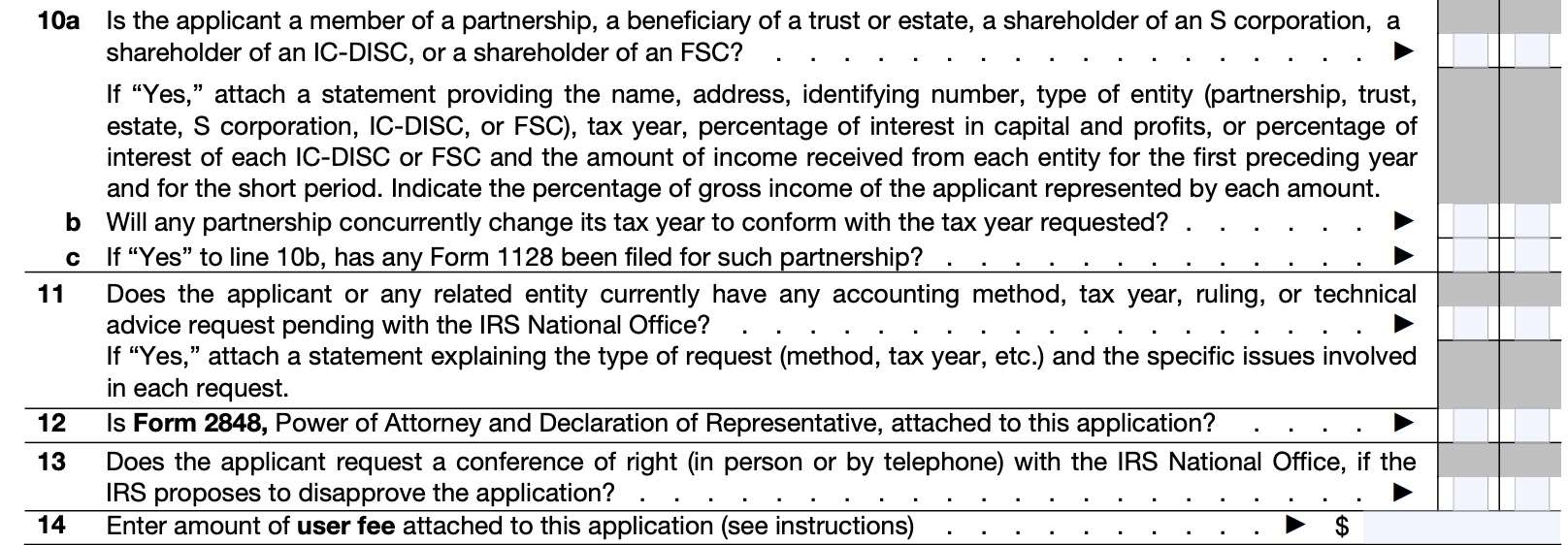

Line 10a

Is the applicant any of the following:

- Member of a partnership

- Trust or estate beneficiary

- Shareholder of an existing S corporation

- Shareholder of an IC-DISC

- Shareholder of an FSC

If so, attach a statement with the following:

- Name, address, identifying number, and type of entity

- Tax year

- Percentage of interest in capital & profits, or percentage of interest and the amount of income received for the first preceding year and the short period

Indicate the percentage of applicant’s gross income by each amount.

Line 10b

Will any partnership concurrently change its tax year to conform with the requested tax year?

Line 10c

If the answer to Line 10b is ‘Yes,’ has the partnership filed IRS Form 1128?

Line 11

Does the applicant or any related entity currently have any of the following requests pending with the IRS National Office:

- Accounting method

- Tax year

- Ruling

- Technical advice

If so, attach a statement explaining the type of request and the specific issues involved.

Line 12

Have you attached IRS Form 2848 to this application?

Line 13

Does the applicant request a conference of right with the IRS National Office, if the IRS proposes to disapprove the application? This can be by phone or in person.

Line 14: User fee

Enter the amount of the user fee enclosed with this application. The most recent update to the list of IRS user fees can be found on the IRS web site.

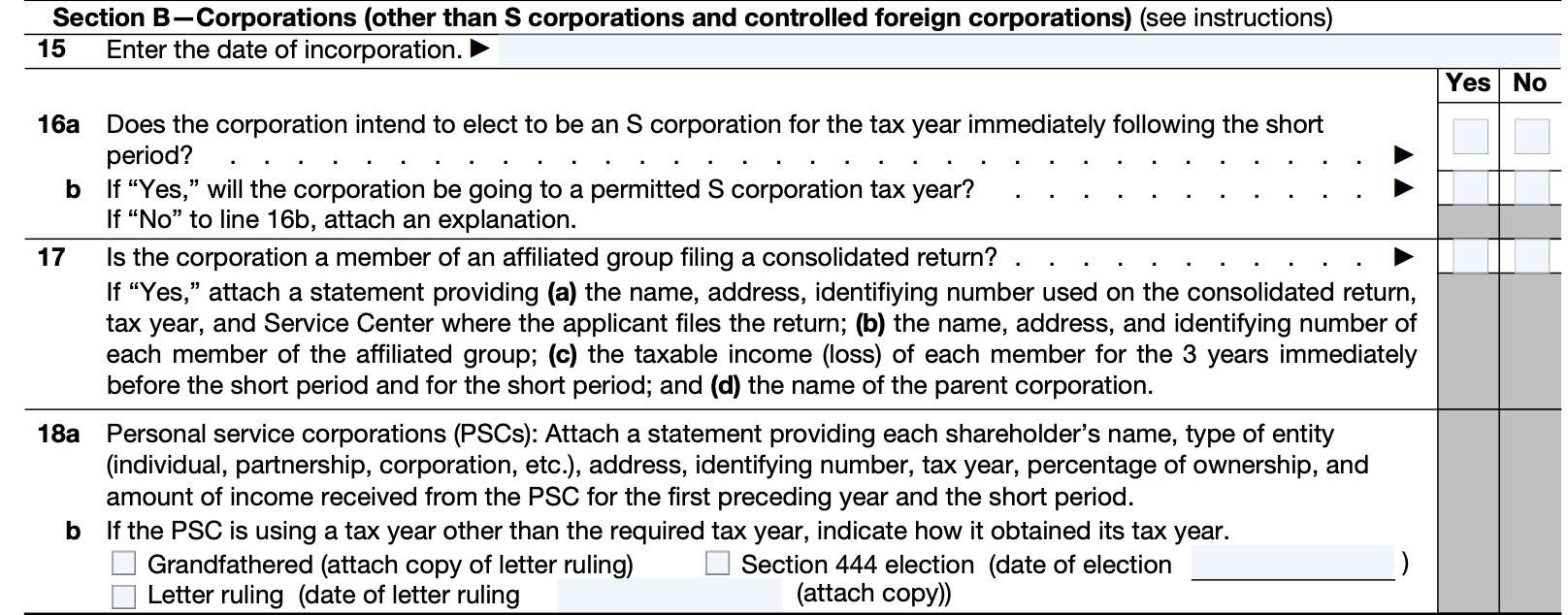

Section B: Corporations

Corporations must complete this section and any other section in Part III that applies to that particular entity.

For example, a Passive Foreign Investment Company (PFIC) completes Section B and attaches the

statement required by Section H.

Tax exempt organizations complete Section B and Section F.

CFCs and 10/50 corporations do not complete Section B.

Line 15: Date of incorporation

Enter the date that the company was incorporated.

Line 16

In Line 16a, answer the following question: “Does the corporation intend to elect to be an S corporation for the tax year immediately following the short period?”

If so, answer the following question in Line 16b: “Will the corporation be going to a permitted S corporation tax year?”

If the answer to this question is ‘No,’ attach a written explanation.

Line 17

Is the corporation a member of an affiliated group filing a consolidated tax return? If so, attach a statement that provides the following information:

- Name, address, identifying number used on the return, tax year, and IRS center where the return is filed

- Name, address, and identifying number of each member of the affiliated group

- Each member’s income or loss for the short tax year and for the three tax years immediately prior

- Parent corporation’s name

Line 18: Personal Service corporations only

Attach a statement that provides:

- Each shareholder’s name

- Type of entity

- Address

- Identifying number

- Tax year

- Ownership percentage

- Amount of income received during the short period and the prior year

If the PSC is using a year other than the required year, indicate how it obtained the current tax year:

- Grandfathered (attach a copy of the ruling)

- Section 444 (date of election)

- Letter ruling (date of ruling)

Section C: S Corporations

An S corporation must have a permitted tax year unless it has elected under IRC Section 444 to have a tax year other than the required tax year.

A permitted tax year is:

- A tax year that ends on December 31, or

- Any other tax year if the corporation can establish a business purpose to the IRS’ satisfaction

- Deferral of income to shareholders is not considered as a business purpose

If any S corporation shareholder is applying for a corresponding change in tax year, that shareholder must file a separate Form 1128 to get advance approval to change its tax year.

Line 19

Enter the date of the S corporation election in Line 19.

Line 20

Is any shareholder applying for a corresponding change in tax year? If so, each shareholder must separately file Form 1128 to obtain this approval.

Line 21

If the S corporation is using a year other than the required year, indicate how it obtained the current tax year:

- Grandfathered (attach a copy of the ruling)

- Section 444 (date of election)

- Letter ruling (date of ruling)

Line 22

Attach a statement that provides the following information:

- Each shareholder’s name

- Type of shareholder

- Address

- Identifying number

- Tax year

- Ownership percentage

- Amount of income each shareholder received for the short period and the preceding tax year

Section D: Partnerships

A partnership must obtain advance approval from the IRS to adopt, change, or retain a tax year unless it:

- Is not required to file IRS Form 1128, or

- Meets one of the automatic approval rules discussed in Part II, Section B, earlier

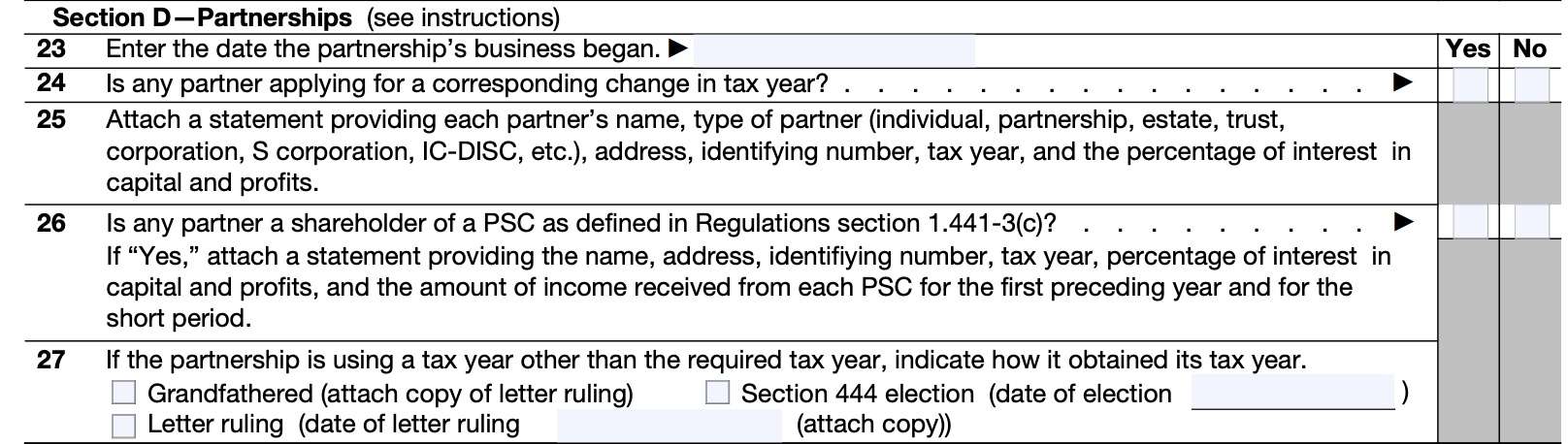

Line 23

Enter the beginning date of the partnership’s business. This would be considered the first date that a business transaction resulted in a tax consequence, such as incurring an expense or receiving income.

Line 24

Is any partner applying for a corresponding tax year change?

Partners must also get separate advance approval to change their tax years.

Line 25

Attach a statement providing the following information about each partner:

- Name

- Type of entity

- Address

- Identifying number

- Tax year

- Percentage of interest in capital and profits

Line 26

Is any partner a PSC shareholder as defined in Treasury Regulations Section 1.441-3(c)?

If so, attach a statement that includes:

- Partner name & address

- Identifying number

- Tax year

- Percentage of interest in capital and pofits

- Amount of income received from each PSC for the short period and first preceding year

Line 27

If the partnership is using a year other than the required year, indicate how it obtained the current tax year:

- Grandfathered (attach a copy of the ruling)

- Section 444 (date of election)

- Letter ruling (date of ruling)

Section E: Controlled Foreign Corporations (CFCs)

Line 28

For CFCs, attach a statement for each U.S. shareholder that contains:

- Name

- Address

- Identifying number

- Tax year

- Percentage of total value & total voting power

- Amount of income included in gross income under IRC Section 951 for the short period and 3 tax years immediately preceding the short period

Section F: Tax-exempt Organizations

Line 29

Indicate the type of organization:

- Corporation

- Trust

- Other (specify)

Line 30

Indicate the date of organization

Line 31

Enter the Internal Revenue Code section makes the organization exempt.

Line 32

Is the organization required to file an annual return on any of the following:

- IRS Form 990

- IRS Form 1120-C

- IRS Form 990-PF

- IRS Form 990-T

- IRS Form 1120-H

- IRS Form 1120-POL

Line 33

Enter the date that the IRS granted the tax exemption and attach a copy of the letter ruling granting the tax exemption. If the letter ruling is not available, attach an explanation.

Line 34

For private foundations, is the foundation terminating its status under IRC Section 507?

Section G: Estates

Line 35

Enter the date that the estate was created.

Line 36a

Attach a statement that provides the following information for each beneficiary and each person who may be an interested party of any part of the estate:

- Name

- Identifying number

- Address

- Tax year

Line 36b

Based on the adjusted total income entered in Part III, Section A, Line 5, attach a statement showing the following information for each beneficiary for the short period and 2 tax years immediately preceding it:

- Distribution deduction

- Taxable amounts

Section H: Passive Foreign Investment Companies

Line 37

For passive foreign investment companies, attach a statement providing the following information for each U.S. shareholder:

- Name

- Address

- Identifying number

- Ownership percentage

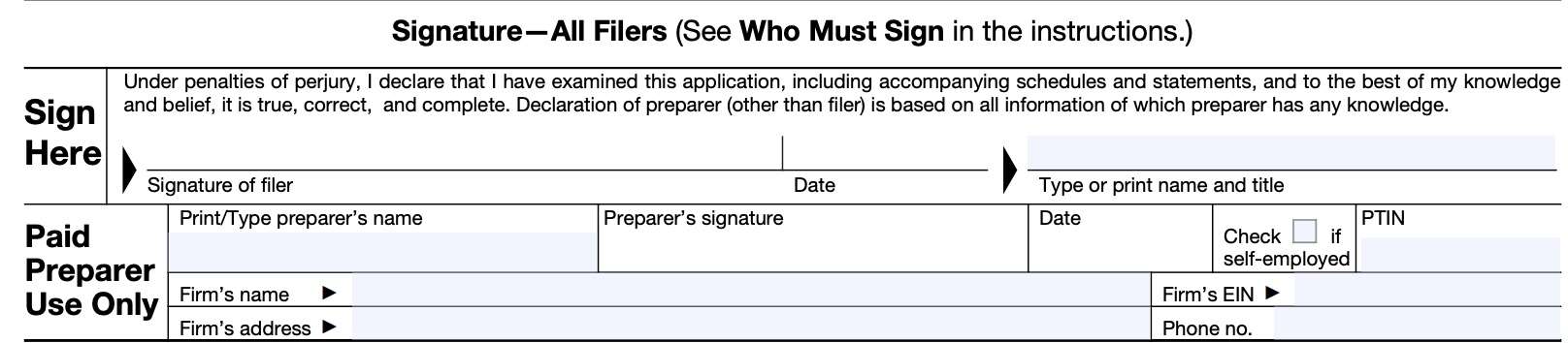

Signature section

Here, the filer will sign and date the form, under penalty of perjury. If using a paid tax preparer, the tax preparer will complete their part of the field as well.

Video walkthrough

Frequently asked questions

Tax entities must file IRS Form 1128 must be filed by the due date of the tax return for the first effective year, not including extensions.

If applying under automatic approval rules, you may file with the IRS center that normally processes your tax return. If you must complete a ruling request in Part III, you must file IRS Form 1128 with the IRS National Office. Exempt organizations send their ruling request to the Ogden IRS office.

This article was tremendously helpful. Thanks so much.