IRS Form 12153 Instructions

If the Internal Revenue Service has sent you a written notice of federal tax lien or a notice of intent to levy assets, then you may consider filing IRS Form 12153 to request a collection due process (CDP) hearing.

In this article, we’ll walk through everything you need to know about this tax form, including:

- Step by step instructions

- When you should consider filing IRS Form 12153

- Documentation requirements

- Frequently asked questions

Let’s start by taking a look at the form itself.

Table of contents

How do I complete IRS Form 12153?

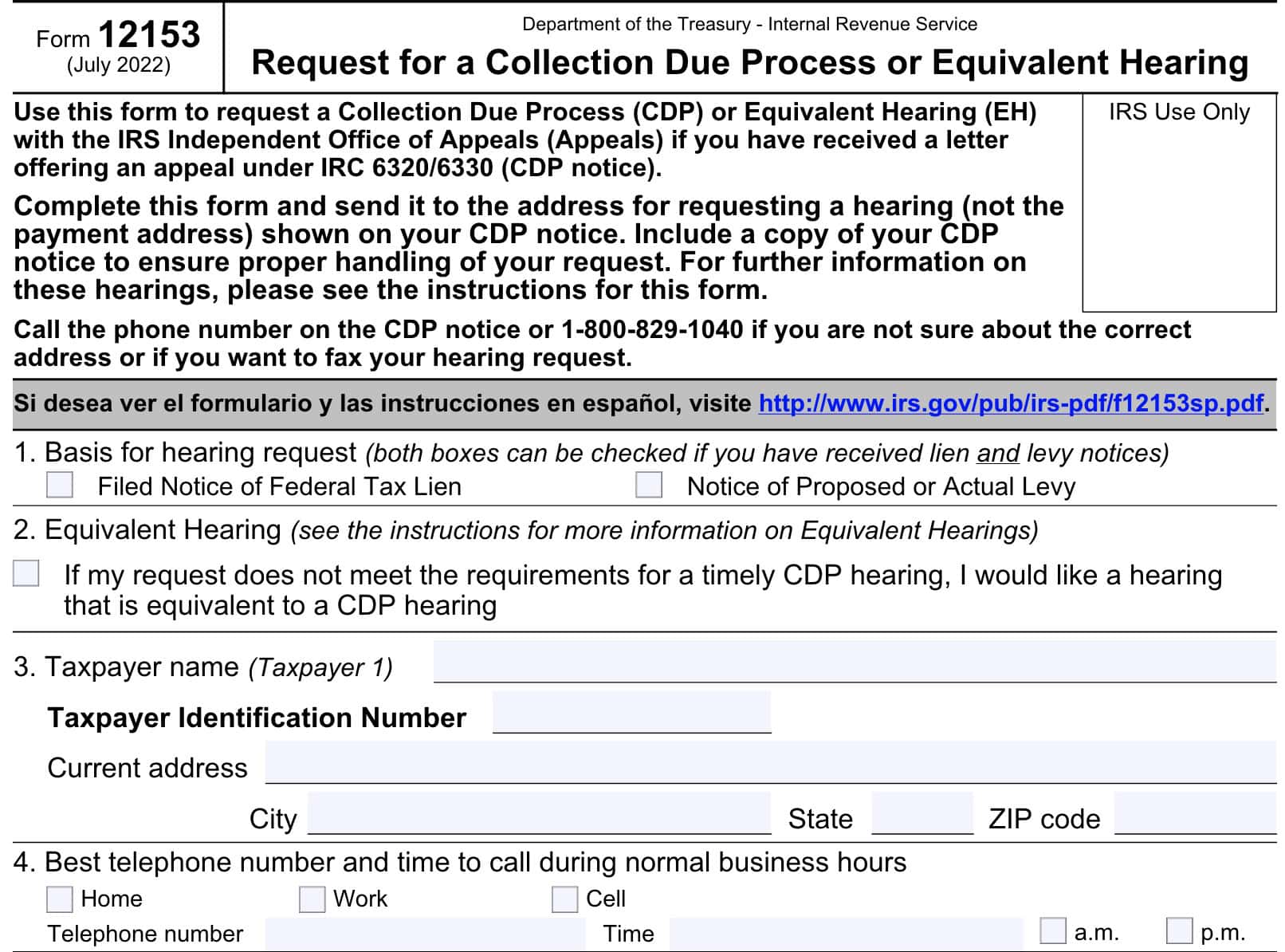

Let’s take a closer look at this two-page tax form, beginning with the information at the top of the form, just above Line 1.

Top of form

At the top of IRS Form 12153, there are some key pieces of information that every taxpayer should know.

Purpose of IRS Form 12153

Use this form to request a collection due process (CDP) or equivalent hearing (EH) with the IRS’ Independent Office of Appeals.

Let’s take a closer look at each.

Collection due process hearing

A CDP hearing is an opportunity to discuss alternatives to enforced collection and permits you to dispute the amount you owe if you have not had a prior opportunity to do so.

According to IRS Publication 1660, Collection Appeal Rights, a CDP hearing is available for any of the following:

- Notice of Federal Tax Lien Filing and Your Right to a Hearing under Internal Revenue Code 6320

- Final Notice – Notice of Intent to Levy and Notice of Your Right to a Hearing

- Notice of Jeopardy Levy and Right of Appeal

- Notice of Levy on Your State Tax Refund – Notice of Your Right to a Hearing

- Post Levy Collection Due Process (CDP) Notice

Your request for a CDP levy hearing, whether timely or equivalent, does not prohibit the IRS from filing a notice of federal tax lien.

You may appeal the results of a CDP decision in tax court. However, you must file your CDP request within a timely manner. You should have received a CDP notice, with a due date in order to make a timely request.

If, for some reason, you do not make a timely request for a CDP hearing, you can still request an equivalent hearing.

Equivalent hearing

An equivalent hearing is similar to a CDP hearing, with a few differences.

The collection period is not suspended

Generally, there is a 10-year time frame for the IRS to collect on outstanding tax debt. This is known as the collection statute expiration date, or CSED.

During a timely filed appeals request or CDP request, IRS collection action does not stop, nor does the IRS suspend the collection period.

Requesting an equivalent hearing does not prevent further enforcement action

Usually, the IRS will suspend collection activities for taxpayers who timely file a hearing request. However, this is not the case if a taxpayer requests an equivalent hearing because the CDP request was not made in a timely manner.

Decisions are final

Finally, any decisions made in an equivalent hearing are considered final and binding. Unlike a CDP hearing, a taxpayer does not have the right to appeal to the U.S. Tax Court in an equivalent hearing.

You must request an equivalent hearing within the following timeframe:

- Lien Notice: one year plus five business days from the filing date of the Federal Tax Lien.

- Levy Notice: one year from the date of the CDP levy notice.

How to file IRS Form 12153

Once you complete IRS Form 12153, you should send your completed form to the IRS address shown on your CDP notice. Make sure that you send your completed form to the address for requesting a hearing, not the payment address.

If you are not sure about the correct address, call the phone number listed on the CDP notice. If that does not work, you can call the IRS’ toll-free number at (800) 829-1040.

To fax your CDP hearing request, contact the IRS number in your IRS notice to ensure that you have the correct fax number.

You can request this form in spanish

Not all tax forms are available in languages other than English. However, if you wish to see a Spanish version of the form (and form instructions in Spanish), you can click the link provided.

For your convenience, we’ve also attached a Spanish version of the form below.

Let’s take a closer look at each line of IRS Form 12153.

Line 1: Basis for hearing

Check the appropriate box, based upon the reason for your hearing request:

- Filed Notice of Federal Tax Lien

- Notice of Proposed or Actual Levy

Let’s take a closer look at each:

Filed Notice of Federal Tax Lien

A filed notice of federal tax lien is a public notice to creditors. It notifies them that there is a federal tax lien that attaches to all your current and future property and rights to property.

In other words, a lien doesn’t actually take your property. However, it does inform creditors that the federal government has an interest in the property that the IRS placed a lien against.

A tax lien can impact your ability to obtain credit in the future. Also, if you sell your property, the tax lien will impact how much money you can receive upon the sale, since the lien must be paid off before you receive any of the remaining proceeds.

Notice of Proposed or Actual Levy

According to IRS Publication 594, the IRS Collection Process, a notice of proposed or actual levy is the notice that the IRS must send before actually seizing your property. Generally, there is at least a 30-day period between the date of the letter and the date that the IRS can actually take levy action.

The IRS may seize your property if you do not do one of the following:

- Pay your overdue taxes in full

- Including penalties and accrued interest

- Make other arrangements to satisfy your tax debt

- Request a hearing within a 30-day deadline stated in the levy notice.

If both a notice of federal tax lien and notice of proposed or actual levy apply, then you can check both boxes.

Line 2: Equivalent hearing

If your request does not meet the requirements for a timely CDP hearing, then you may request an equivalent hearing. For more specific information, see Equivalent Hearing, above.

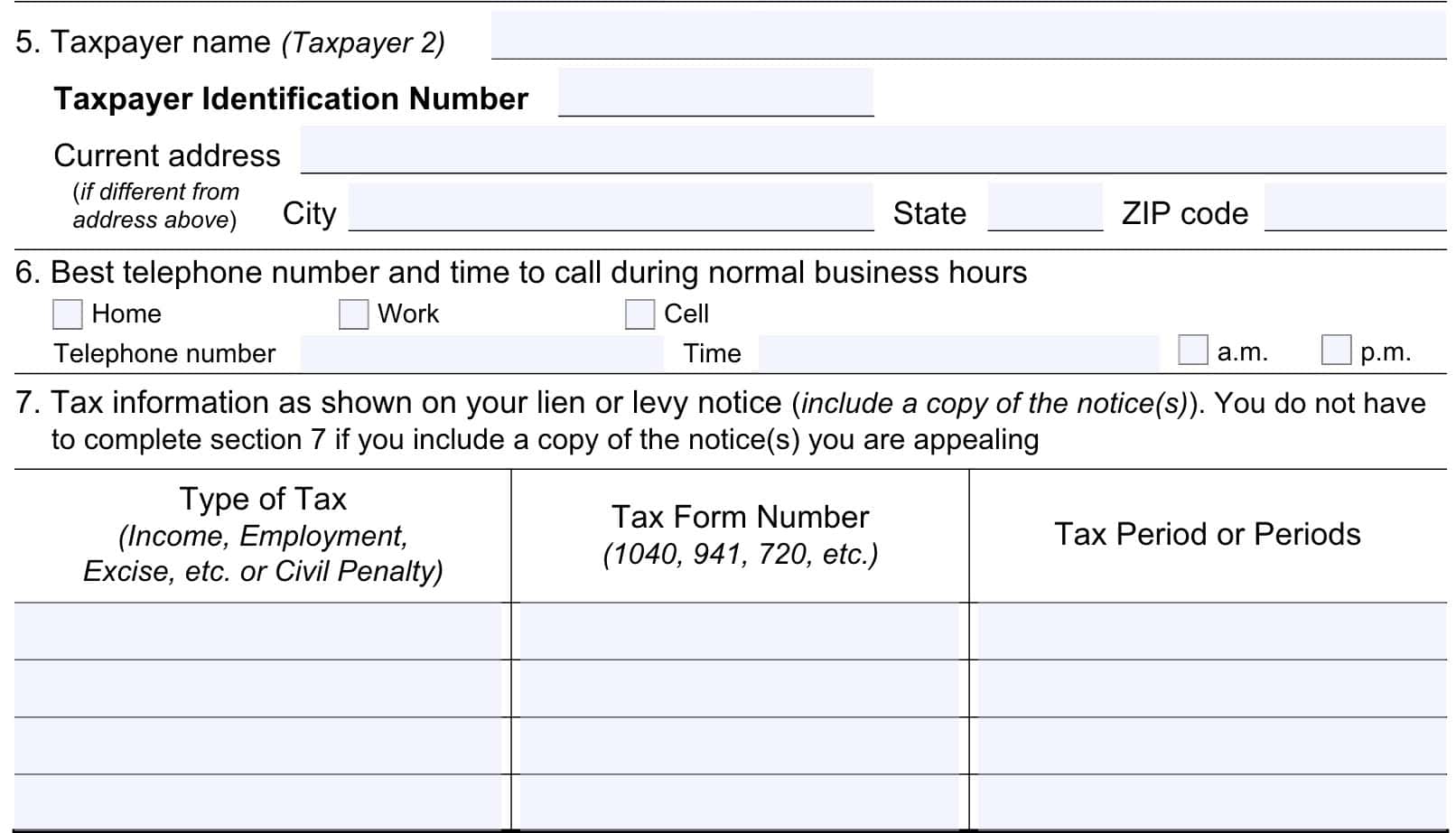

Line 3: Taxpayer information

Enter the following taxpayer information in Line 3:

- Taxpayer name

- Taxpayer identification number

- Social Security number

- Individual taxpayer identification number (ITIN)

- Employer identification number (EIN)

If there are two taxpayers (such as a married couple filing a joint return), then enter the information for the taxpayer that appears first on your income tax return.

Line 4: Telephone number

Select the best telephone number option:

- Home

- Work

- Cell

Enter the telephone number and the best time for IRS employees to call you.

Line 5: Taxpayer information

If applicable, enter the same information for the second taxpayer as you did in Line 3 for the first:

- Taxpayer name

- Taxpayer identification number

- Social Security number

- Individual taxpayer identification number (ITIN)

- Employer identification number (EIN)

Line 6: Telephone number

Select the best telephone number option:

- Home

- Work

- Cell

Enter the telephone number and the best time for IRS employees to

Line 7: Tax information as shown on your lien or levy notice

In this section, you should enter the tax information shown on your lien notice or levy notice. This includes the following information:

- Type of tax: What type of tax liability is your lien or levy notice about?

- Income tax

- Employment tax

- Excise tax

- Estate tax

- Tax form number: What type of tax return is involved? Below are some common examples:

- IRS Form 1040, U.S. Individual Income Tax Return

- IRS Form 1065, U.S. Return of Partnership Income

- IRS Form 1120-S, U.S. Income Tax Return for an S Corporation

- IRS Form 941, Employer’s QUARTERLY Federal Tax Return

- Tax period or periods: This can be a specific tax year or tax quarter. List all tax years or quarters that are on your notice.

If you wish to attach a copy of your notice or notices, you do not need to enter any information in Line 7.

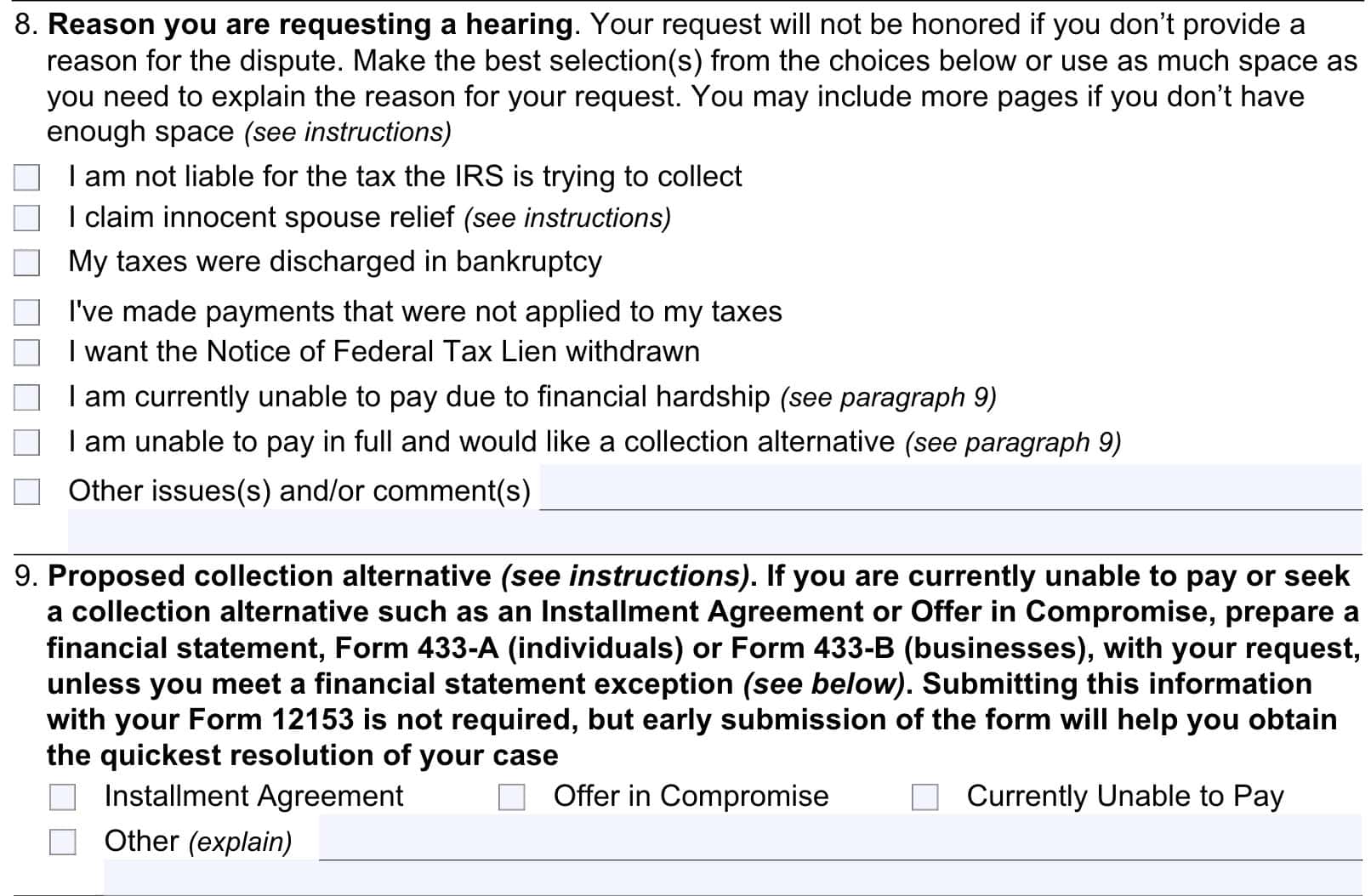

Line 8: Reason you are requesting a hearing

Check the box or boxes that apply to your situation. Let’s take a closer look at each of the options.

I am not liable for the tax the IRS is trying to collect

You can generally raise a disagreement about the amount of tax you owe if you:

- Did not receive a deficiency notice for the tax liability, or

- Have not had another prior opportunity for Appeals, or for a court to consider your disagreement

A deficiency notice is a notice that explains why you owe taxes. A deficiency notice should give you the right to challenge in court, within a certain time frame, the additional tax that the IRS says you owe.

Appeals may remove all or part of the tax penalties on unpaid taxes if you have a reasonable cause for not paying or not filing on time.

I claim innocent spouse relief

If you believe that your spouse is the only person that should be responsible for the tax liability, then you may be eligible for innocent spouse relief. You must file IRS Form 8857 to request innocent spouse relief.

My taxes were discharged in bankruptcy

You may have received a prior bankruptcy discharge and your taxes were not excepted from the discharge.

Even if your taxes were discharged, your pre-bankruptcy property may remain subject to a tax lien if:

- The property was excluded from the bankruptcy filing, or

- The IRS filed the notice of the lien before the bankruptcy

I’ve made payments that were not applied to my taxes

Select this option if you disagree with the amount the IRS says you have or have not paid. If you want to check your tax balance online, and you’ve already set up an account with the Internal Revenue Service website, you can check before your hearing.

I want the Notice of Federal Tax Lien withdrawn

For the filing of a Notice of Federal Tax Lien (NFTL) against your property, you can choose one of the following lien resolutions:

- Withdrawal

- Subordination

- Release

- Discharge

Let’s take a closer look at each of these options, and the required tax form that should accompany your request. In each case, if there is additional documentation to complete, you should include that additional documentation with your hearing request.

Lien Withdrawal

When you request a withdrawal of the NFTL, you are asking the IRS to remove the NFTL information from public records because you believe the NFTL should not have been filed in the first place.

To request a lien withdrawal, you should complete IRS Form 12277, Application for Withdrawal of Filed Form 668(Y), Notice of Federal Tax Lien.

Lien Subordination

When you request a subordination, you are asking the IRS to make a Federal Tax Lien secondary to a non-IRS lien.

This might be an option for someone who cannot or does not want to remove their IRS liens, but who may need to subordinate a tax lien for personal purposes, such as a house refinance. The IRS will consider lien subordination when it improves a taxpayer’s ability to pay their tax debt, such as using the proceeds from refinancing a home as part of a payment plan.

To request lien subordination, complete IRS Form 14134, Application for Certificate of Subordination of Federal Tax Lien.

Lien Release

You can get a federal tax lien released if you pay your taxes in full or complete the terms of an accepted Offer-in-Compromise.

Lien Discharge

When you request a discharge, you are asking the IRS to remove a federal tax lien from a specific property.

To request a lien discharge, file IRS Form 14135, Application for Certificate of Discharge of Federal Tax Lien.

I am currently unable to pay due to financial hardship

If applicable, check this box. You can see more information about financial hardships in Line 9, below.

I am unable to pay in full and would like a collection alternative

If you want to discuss a collection alternative, then you should complete Line 9 and complete the appropriate collection information statement, as outlined below:

- IRS Form 433-A, Collection Information Statement for Wage Earners and Self-Employed Individuals

- IRS Form 433-B, Collection Information Statement for Businesses

Submitting this information with your Form 12153 is not required. However, you may find that this should provide the quickest resolution of your case.

Other issues(s) and/or comment(s)

If you wish to point out tax issues not already identified, or make additional comments, include them in the space provided. If you do not have enough space, you may include additional pages

Line 9: Proposed collection alternative

You may enter one of the following:

- Installment agreement

- Offer in Compromise

- Currently unable to pay

- Other

Let’s take a closer look.

Installment agreement

An installment agreement allows taxpayers to pay their tax bill in full, including penalties and interest, by setting up a payment plan over an agreed to time period. This might be an option for those with a large bill, but one that they can pay in monthly installments.

You can apply for an installment agreement on the IRS website or by filing IRS Form 9465, Installment Agreement Request. The IRS does not require collection information statements for installment agreement applications placed through the IRS website.

Offer in Compromise

In an offer-in-compromise, the IRS agrees to accept one or more tax payments for less than the amount of tax that you may owe, according to your tax balance.

You may apply for an offer in compromise on the IRS website or by filing IRS Form 656, Offer in Compromise.

You must submit a financial statement with your offer in compromise unless the offer-in-compromise is based upon Doubt as to Liability.

Currently unable to pay

You may not be able to pay due to job loss, illness, reasonable expenses that exceed income, etc.

Appeals may consider freezing collection action until your circumstances improve. Interest and applicable penalties will continue to accrue on your tax liability.

Other

If you have another option, outline that option in the space provided.

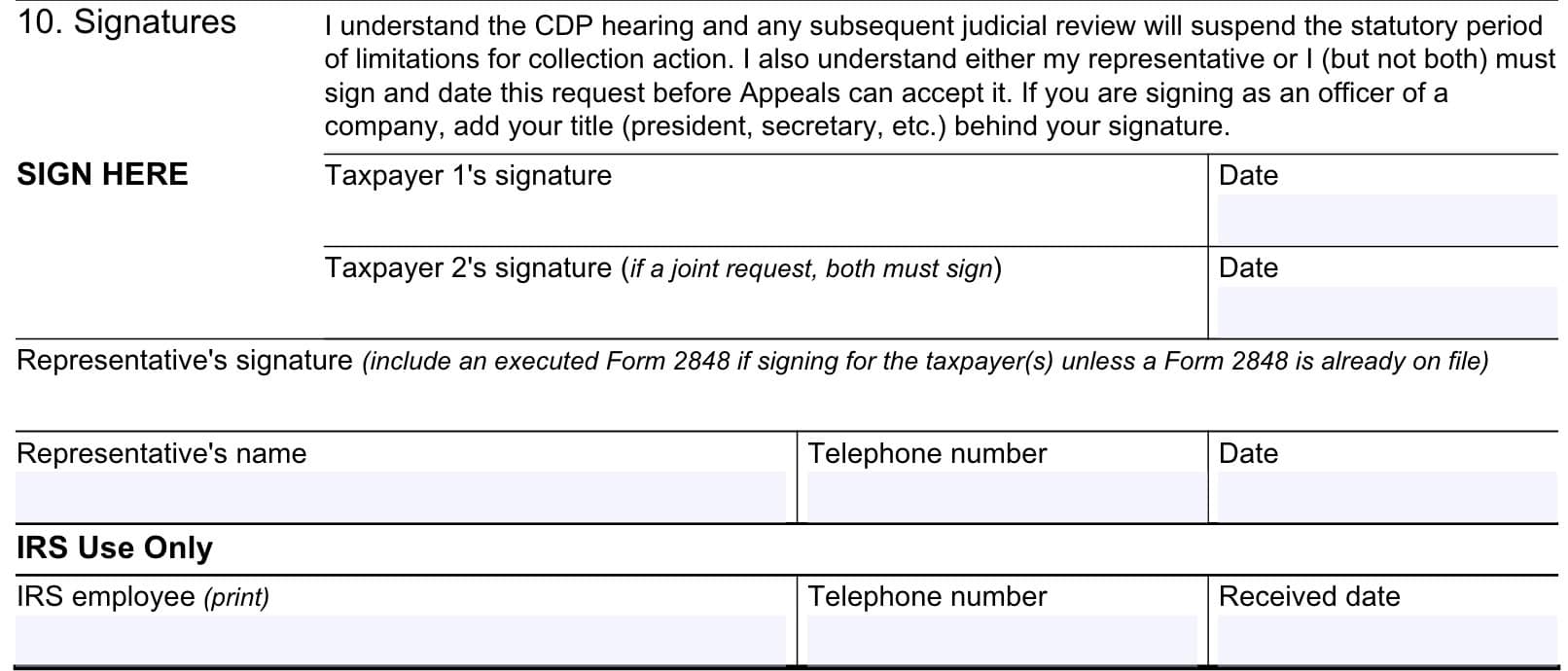

Line 10

At the bottom of the form, provide your dated signature, which states that you understand the following:

- The CDP hearing and subsequent judicial reviews will suspend the statutory period of limitations for collection action

- Either you or your representative must sign and date your request before the IRS office of appeals will accept it.

For joint requests, both spouses must sign.

If you have appointed a representative, you must also include a completed copy of IRS Form 2848, Power of Attorney and Declaration of Representative, unless it is already on file with the IRS.

Video walkthrough

Frequently asked questions

Taxpayers may use IRS Form 12153 to request a collection due process (CDP) hearing. This may be an option for taxpayers facing a tax lien, tax levy, or other IRS tax collection actions.

The collection due process (CDP) and the collection action program (CAP) cover slightly different parts of the IRS collections process. CAP generally results in a quicker appeals decision and is available for a broader range of collection actions. However, you cannot go to court if you disagree with the CAP decision.

You may appeal the results of a CDP hearing to judicial review by the U.S. Tax Court. However, taxpayers may not appeal the results of an equivalent hearing, if the taxpayer did not submit the hearing request in time for a CDP review.

Where can I find IRS Form 12153?

The IRS provides electronic copies of tax forms on the IRS website. For your convenience, we’ve included the latest version of IRS Form 12153 (in English and in Spanish), here in this article.