IRS Form 8833 Instructions

If you’re a U.S. person living overseas, you may be required to report your income to both the U.S. government and the foreign country where you reside. In some cases, U.S. taxpayers may have the option of filing IRS Form 8833 to pay federal taxes at a reduced rate than they otherwise would pay under U.S. tax law and the laws of the foreign country in which they reside.

In this article, we’ll walk through everything you need to know about IRS Form 8833, including:

- How to complete IRS Form 8833

- Filing considerations

- Frequently asked questions

Let’s begin by going over this tax form, step by step.

Table of contents

How do I complete IRS Form 8833?

This one-page form appears relatively straightforward to complete. We’ll walk through this form, step by step. At the end of this section, we’ll discuss other filing considerations, such as where and how to file.

We’ve broken this form down into two parts:

Let’s start with the top of the form.

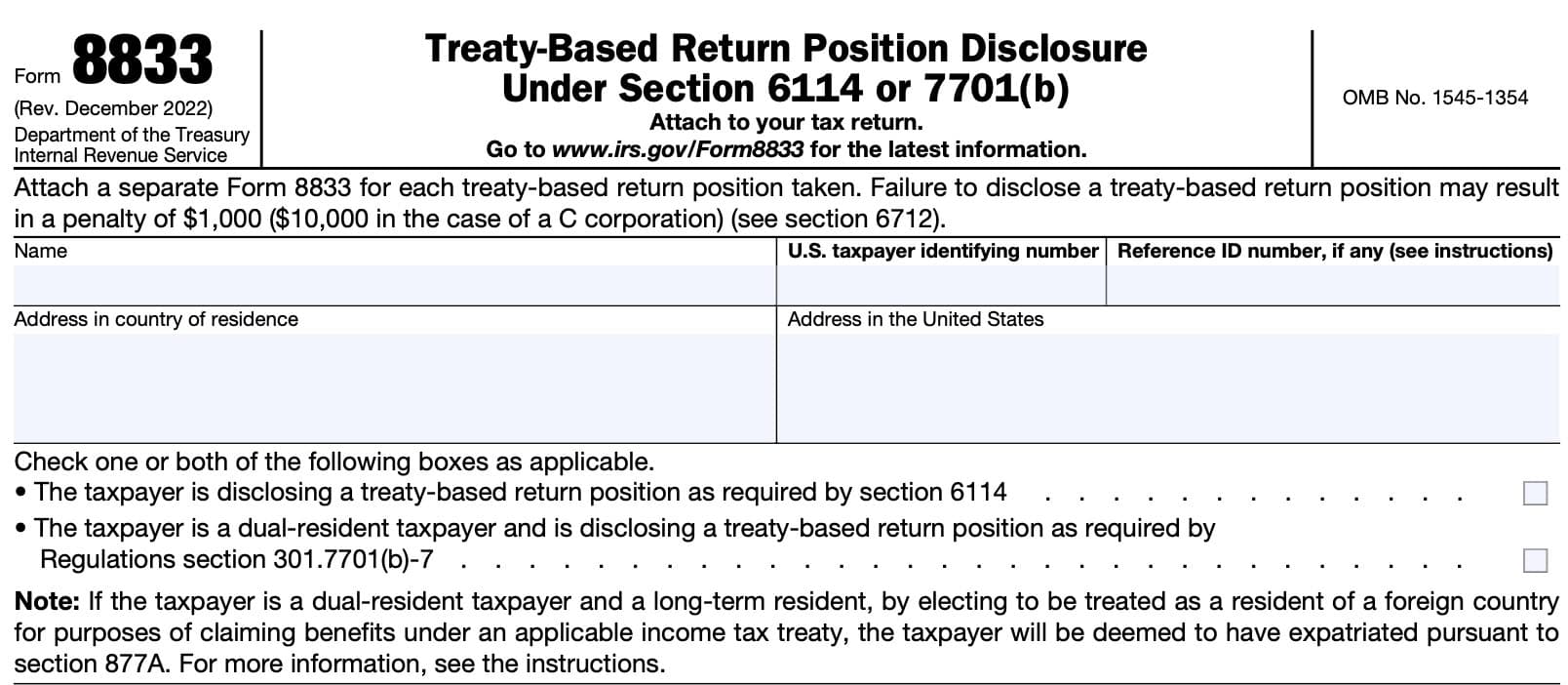

Taxpayer information

Before completing any taxpayer information, please note that the IRS expects taxpayers to attach a separate Form 8833 for each treat-based return position taken.

If you do not disclose a treaty-based return position, the IRS may fine taxpayers up to $1,000. For C corporation taxpayers, this tax penalty may be $10,000.

Taxpayer name

Enter the taxpayer name as it appears on the taxpayer’s income tax return.

U.S. taxpayer identifying number

Enter the taxpayer identification number. This may be one of the following:

- Social Security number (SSN)

- Individual taxpayer identification number (ITIN)

- Employer identification number (EIN)

Reference ID number

If the taxpayer is a foreign corporation, enter any reference ID number assigned to the foreign corporation by a U.S. person with respect to which information reporting is required.

Common examples include the following tax forms:

- IRS Form 5471, Information Return of U.S. Persons With Respect To Certain Foreign Corporations

- IRS Form 5472, Information Return of a 25% Foreign-Owned U.S. Corporation or a Foreign Corporation Engaged in a U.S. Trade or Business

Address in country of residence

Enter the address information in the following order:

- City

- Province or state

- Country

Follow the country’s practice for entering postal codes. Do not abbreviate the name of the foreign country.

U.S. address

Enter your address as it appears in your tax records or on your tax return. This should include:

- Street number and name

- City, state, zip code

Boxes to check

Before moving onto Line 1, review the boxes just below the address fields. Below the taxpayer information fields, you may check one of several boxes:

- Taxpayer is disclosing a treaty-based return position as required by IRS Section 6114

- Taxpayer is a dual-resident taxpayer and disclosing a treaty-based return position as required by Regulations Section 301.7701(b)-7

- The taxpayer is a U.S. citizen, resident, or incorporated in the United States

You’ll note that if the taxpayer elects to be treated as a resident of a foreign country in order to claim treaty benefits, then that taxpayer will be considered an expatriate, per IRC Section 877A.

Check either of the boxes (or both) as applicable.

Taxpayer is disclosing a treat-based return position as required by Section 6114

According to the form instructions, Treasury Regulations Section 301.6114-1(b) further refines disclosure requirements from Internal Revenue Code Section 6114. Specifically, there are examples of the following situations:

- Situations where reporting is specifically required

- Exceptions from reporting

- Situations where reporting is required by Form 8833 instructions

Let’s take a closer look at each.

Situations where reporting is specifically required

Based on the instructions, taxpayers may need to check this box if any of the following conditions apply:

- A nondiscrimination provision of the treaty prevents the application of an otherwise applicable provision of the Internal Revenue Code,

- Other than with respect to making an election under IRC Section 897(i), which allows foreign corporations to be treated as domestic corporations;

- A treaty reduces or modifies the taxation of gain or loss from the disposition of a U.S. real property interest;

- A treaty reduces or modifies the branch profits tax (IRC Section 884(a)) or the amount of tax on excess interest (IRC Section 884(f)(1)(B));

- A treaty exempts from tax or reduces the rate of tax on dividends or interest paid by a foreign corporation that are U.S.-sourced under IRC Section 861(a)(2)(B) or Section 884(f)(1)(A)

- Certain situations in which a treaty exempts from tax or reduces the rate of tax on fixed or determinable annual or periodical (FDAP) income that a foreign person receives from a U.S. person

- That income effectively connected with a U.S. trade or business of a taxpayer is not attributable to a permanent establishment or a fixed base in the United States;

- That a treaty modifies the amount of business profits of a taxpayer attributable to a permanent establishment or a fixed base in the United States;

- That a treaty alters the source of any items of income or deduction (unless the taxpayer is an individual);

- That a treaty grants a credit for a foreign tax which is not allowed by the Code;

- That the residency of an individual is determined under a treaty and apart from the Code.

This is not a complete list of required situations. You may need to refer to Treasury Regulations Section 301.6114-1(b) for official taxtrea guidance.

Exceptions from reporting

Reporting requirements may be waived in the following taxpayer situations:

- A treaty reduces or modifies the taxation of income derived by an individual from dependent personal services, pensions, annuities, social security, and other public pensions, as well as income derived by artists, athletes, students, trainees, or teachers;

- That a Social Security Totalization Agreement or Diplomatic or Consular Agreement reduces or modifies the income of a taxpayer;

- That a treaty exempts a taxpayer from the excise tax imposed by IRC Section 4371,

- Only if certain conditions are met

- For example, the taxpayer has entered into an insurance excise tax closing agreement with the IRS

- That a treaty exempts from tax or reduces the rate of tax on FDAP income, if the beneficial owner is an individual or governmental entity;

- If a partnership, trust, or estate has disclosed a tax treaty position that the partner or beneficiary would otherwise be required to disclose;

Treasury Regulations Section 301.6114-1(c) contains additional information about exceptions.

Situations where reporting is required by Form 8833 instructions

According to the form instructions, the following amounts specifically require a treaty-based

return disclosure on Form 8833:

- Dual-resident corporations: Amounts that are received by a corporation that is a resident under the domestic law of both the United States and a foreign treaty jurisdiction

- Multiple tax treaties: Amounts that are received by a corporation that is a resident of both:

- The jurisdiction whose treaty is invoked, and

- Another foreign jurisdiction that has an income tax treaty with that treaty jurisdiction.

- Revenue Ruling 2004-76 applies,

- Amounts that are received by a foreign collective investment vehicle that is a contractual arrangement and not a person under foreign law.

- Example 7 of Treasury Regulations Section 1.894-1(d)(5).

- Amounts that are received by a foreign interest holder in a domestic reverse hybrid entity, as stated in Treasury Regulations Section 1.894-1(d)(2).

Taxpayer is a dual-resident taxpayer and is disclosing a treaty-based return position as required by Regulations Section 301.7701(b)-7

An alien individual is a dual-resident taxpayer if that individual is considered to be a resident of both the United States and another country under each country’s tax laws.

If you are an individual who is a dual-resident taxpayer and you choose to claim treaty benefits as a resident of the foreign country, you are treated as a nonresident alien in figuring your U.S. income tax liability for the part of the tax year you are considered a dual-resident taxpayer.

If you are eligible to be treated as a resident of the foreign country pursuant to the applicable income tax

treaty and you choose to claim benefits as a resident of such foreign country, you must file Form 1040-NR, U.S. Nonresident Alien Income Tax Return, with Form 8833 attached.

Expatriated taxpayers

According to the IRS, if you are a dual-resident taxpayer and a long-term resident (LTR) and you are filing this form to be treated as a resident of a foreign country for purposes of claiming benefits under an applicable U.S. income tax treaty, you will be deemed to have terminated your U.S. residency status for federal income tax purposes.

This means that you may be subject to tax under IRC Section 877A, and you must file IRS Form 8854, Initial and Annual Expatriation Statement.

The federal government considers you to be an LTR if you were a lawful permanent U.S. resident for 8 of the previous 15 tax years ending with the year you file Form 8833. IRS Pub. 519, U.S. Tax Guide for Aliens contains more details.

The taxpayer is a U.S. citizen, resident, or incorporated in the United States

Check this box if you are a U.S. citizen or resident, or if your tax entity is incorporated in the United States.

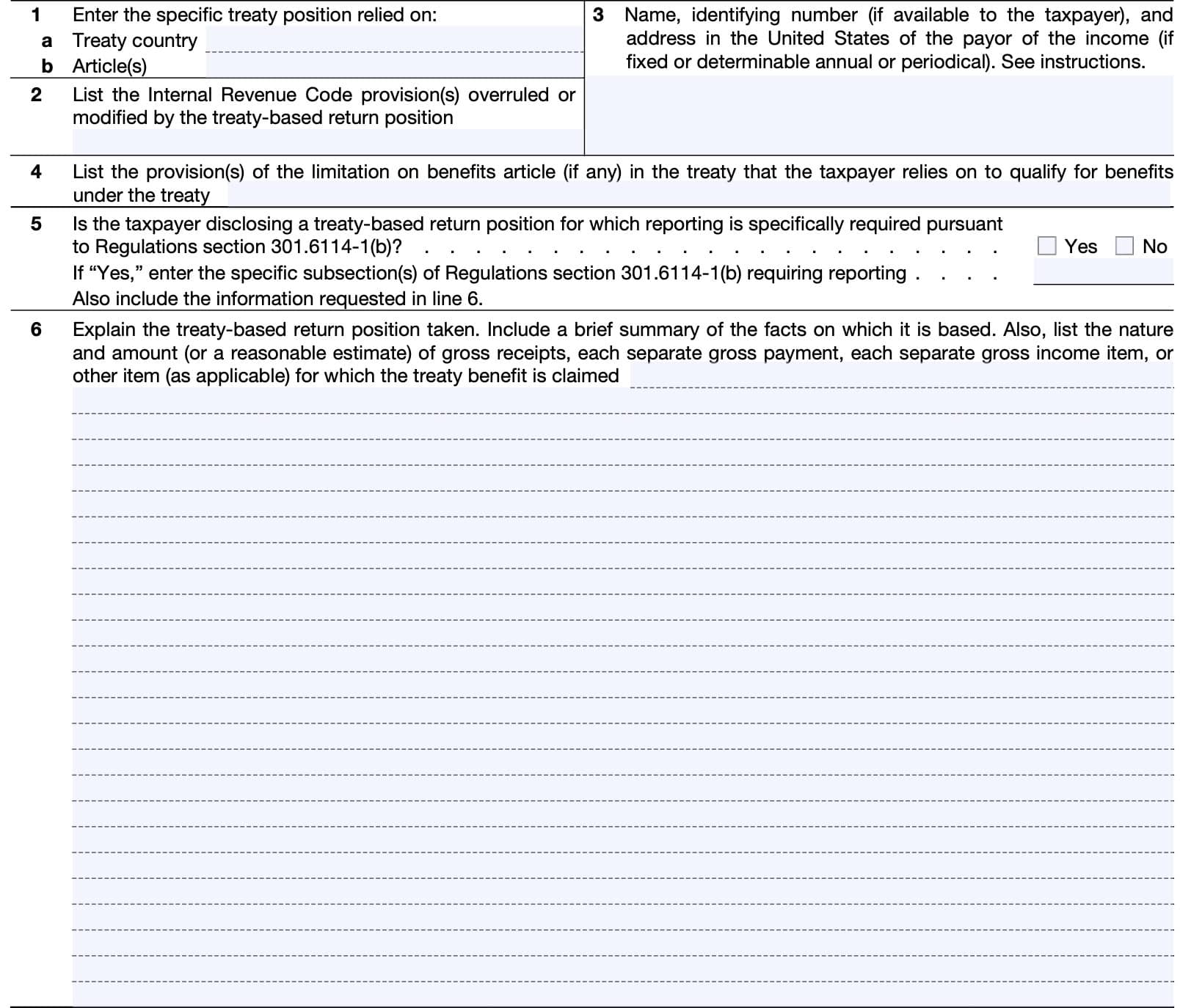

Treaty information

Although not marked on the form, this section contains necessary information about the treaty, the position the taxpayer chooses to take, and the Code Section that the treaty overrules.

Line 1: Specific treaty

Enter the treaty country in Line 1a. For Line 1b, list the article or articles that the treaty position relies upon.

Line 2: IRC provision overruled

List the provisions that the treaty-based return position either overrules or modifies.

Line 3: FDAP income payor

List the name, ID number (if available), and address of the payor for the FDAP income declared. If there is more than one position, or more than one source of income declared, you may need to file a separate form for each.

Where to find additional information

For more information, individuals should consult Section 871(a) and Treasury Regulations Section 1.871-7(b) and (c). Foreign corporations should see Section 881(a) and Treasury Regulations Section 1.881-2(b) and (c).

Line 4: Provisions cited

In Line 4, name the specific test in the Limitations on Benefits (LOB) article that’s met. The IRS website contains an LOB table, with a summary of the various tests for each treaty.

If you have made a request with the U.S. competent authority for a discretionary determination, and that request is still pending, you may not claim benefits, unless the treaty or technical explanation specifically states otherwise.

Line 5

Select the appropriate box.

If ‘Yes,’ Enter the subsection of Regulations Section 301.6114-1(b) that is pertinent to your treaty-based return position and proceed to Line 6.

If ‘No,’ simply proceed to Line 6.

Line 6

Unless specifically waived under Treasury Regulations Section 301.6114-1(c), all taxpayers taking a treaty-based return position must include all requested information.

If applicable, explain:

- Why this position meets the LOB test identified on Line 4

- Basis for meeting any special requirements

- Amount of the income affected by the treaty claim

Filing considerations

In this section, we’ll cover some additional filing considerations about IRS Form 8833.

How do I file IRS Form 8833?

When filing your tax return, such as Form 1040-NR or Form 1120-F, you should attach all completed copies of Form 8833 to your tax return.

Normal filing timelines apply, as this form is due with your completed tax return.

If you do not need to file a tax return

If you do not have to file a tax return, you must file IRS Form 8833 at the IRS Service Center where you would normally file a return.

Who must fill out IRS Form 8833?

The form instructions maintain a long list of situations in which a taxpayer may be required to file this form. However, the instructions state that this is not an all-inclusive list.

Let’s take a closer look at situations in which a taxpayer must file this tax form.

A provision of the treaty prevents the application of a tax code provision that would otherwise apply.

The exception to this is the election of a foreign corporation to be treated as a domestic corporation as outlined under IRC Section 897(i). This does not necessitate filing Form 8833.

The treaty impacts the tax treatment of real estate sales

If a treaty reduces or modifies the taxation of gains or losses from the disposition of a U.S. real property interest, then the taxpayer must file.

The treaty modifies branch profits tax or taxes on excess interest

Generally speaking, a foreign company with branches in the United States must pay a 30% tax on any excess income produced by US branches, but not reinvested in them. Under Section 884, this includes:

- The profits themselves

- Excess interest earned on the profits

If a treaty reduces or modifies this tax, then the taxpayer must file.

The treaty reduces taxes on certain dividend or interest income

If a tax treaty reduces the income tax liability for dividend and interest income paid by a foreign corporation, but U.S.-sourced, the taxpayer must file. The following code provisions apply, and will provide more specific detail:

- IRC Section 861(a)(2)(B): Certain dividends from a foreign corporation

- IRC Section 884(f)(1)(A): Interest on profits excluded from branch profits tax

The treaty reduces certain fixed, determinable, annual, periodical (FDAP) income

This is the section that might apply to most individual taxpayers.

It maintains that anyone who receives FDAP income may be required to file this form if their treaty position lowers their tax bill.

What is FDAP income?

The IRS considers all sources of income to be FDAP income, unless it’s specifically excluded. FDAP stands for the following:

- Fixed when paid in amounts that are known ahead of time

- Determinable when there is a basis for figuring out how much is paid, and

- Periodic if paid from time to time.

- Does not have to be annual, or even at regular intervals

Types of FDAP

- Compensation for personal services

- This might include commissions and gross proceeds from performances

- Dividends

- Interest

- Original issue discount

- Pensions and annuities

- Alimony

The IRS website maintains a list of all income sources, then describes the treatment of each. We’ll touch base on some particulars of other sources of FDAP.

Social Security benefits

The IRS considers U.S. source FDAP to include 85% of any U.S. Social Security benefit (or the Social Security equivalent part of a Tier 1 railroad retirement benefit). Some international amoutax treaties exclude Social Security income.

IRS Publication 901, U.S. Tax Treaties, contains a complete list of income tax treaties that exempt U.S. Social Security benefits from U.S. income tax.

Capital gains

Capital gains are subject to varying types of treatment, based upon:

- Source of income

- Length of residency in the United States

Refer to the IRS website for more specific details.

Installment payments

Income can be FDAP income whether it is paid in a series of repeated payments or in a single lump sum. The IRS example states that $5,000 in royalty income would be FDAP income whether paid in:

- 10 payments of $500 each, or

- 1 payment of $5,000

Insurance proceeds

If an insured nonresident alien surrenders a life insurance policy, or receives income at the policy’s maturity, the proceeds are considered FDAP income to the extent they exceed the policy’s cost.

Certain payments, such as accelerated death benefits or payments received as part of a viatical settlement contract, might not be taxable. IRS Publication 525, Taxable and Nontaxable Income, contains more detail.

Income connected with a U.S. trade or business, but not attributable to a source in the United States

If income is effectively connected with a U.S. trade or business of a taxpayer, but is not attributable to a permanent establishment or a fixed base in the United States, the taxpayer must file IRS Form 8833.

The treaty modifies profits attributable to U.S. sources

If a treaty modifies the amount of business profits of a taxpayer attributable to a permanent establishment or a fixed base in the United States, the taxpayer must file IRS Form 8833.

The treaty makes certain alterations

This includes:

- Altering the source of an item of income or deduction

- Granting a foreign tax credit otherwise not allowed under the Internal Revenue Code

- Determining an individual’s residency for tax purposes

If any of the above situations apply, the taxpayer must file.

Video walkthrough

Are you tired of dreading tax season?

If you’re like most people, you push through the stress of filing, only to be hit with a bigger bill than expected—then put it all behind you until the same cycle repeats next year.

But what if you could change the game?

Tax planning puts you in control. It’s about being proactive, not reactive—taking small, smart steps throughout the year to reduce your tax burden, increase your savings, and keep more of your hard-earned money working for you.

Here’s what effective tax planning helps you do:

✅ Avoid the surprise of a high tax bill

✅ Understand how your income and decisions affect your taxes

✅ Strategically lower your tax liability over time

Ready to make smarter tax moves?

👉 Join my free weekly tax planning newsletter and get one actionable tip every week to help you reduce your taxes legally and effectively.

Start taking control—your future self will thank you.

Frequently asked questions

IRS Form 8833, Treaty-Based Return Position Disclosure Under Section 6114 or 7701(b), is the tax form that individual and corporate taxpayers must complete when taking a treaty-based position that results in a reduction of tax on their U.S. tax return.

U.S. tax law requires U.S. taxpayers to report worldwide income to the U.S. government. Taxpayers can use a treaty-based return position to claim tax treaty benefits to override an Internal Revenue Code provision on a U.S. tax return if they meet the requirements of that particular tax treaty.

According to Treasury Regulations Section 301.7701(b)-7(a)(1), an individual who is considered a resident of the United States pursuant to the internal laws of the United States and also a resident of a treaty country pursuant to the treaty partner’s internal laws.

No. If a taxpayer elects to use a tax treaty to lower their U.S. tax liability, then they are subject to all applicable sections of that treaty. Also, if you claim an income tax treaty benefit as a resident of a treaty country, the United States will consider you to be a nonresident alien for income tax purposes.

The due date of IRS Form 8833 should be the same as the due date for your original tax return.

Where can I find IRS Form 8833?

You may find IRS Form 8833 on the Internal Revenue Service website. For your convenience, we’ve attached the latest copy of this tax form here, in our article.

Related tax articles

This tax form is one of the fillable tax forms provided by the Internal Revenue Service, to help taxpayers reduce their tax preparation costs. To see more forms like this, visit our free fillable tax forms page, where you’ll also find articles like this.

Unlike the IRS, our articles contain step by step instructions for each tax form, as well as video walkthroughs. You can also check out all of our videos by subscribing to our YouTube channel!