IRS Form 8802 Instructions

U.S. taxpayers working in a foreign country may need to provide documentation to avoid double taxation by both the United States and that foreign country. This documentation comes in the form of a U.S. Letter of Residency Certification, also known as IRS Form 6166. Taxpayers request this residency certification on IRS Form 8802, Application for U.S. Residency Certification.

In this article, we’ll walk you through everything you need to know about obtaining a letter of residency certification. We’ll provide a step-by-step guide to the following:

- How to properly complete IRS Form 8802

- How to pay the user fee

- Other frequently asked questions

Let’s start by walking through this tax form itself.

Table of contents

How do I complete IRS Form 8802?

We’ll walk through this three-page tax form one step at a time. Let’s begin at the top.

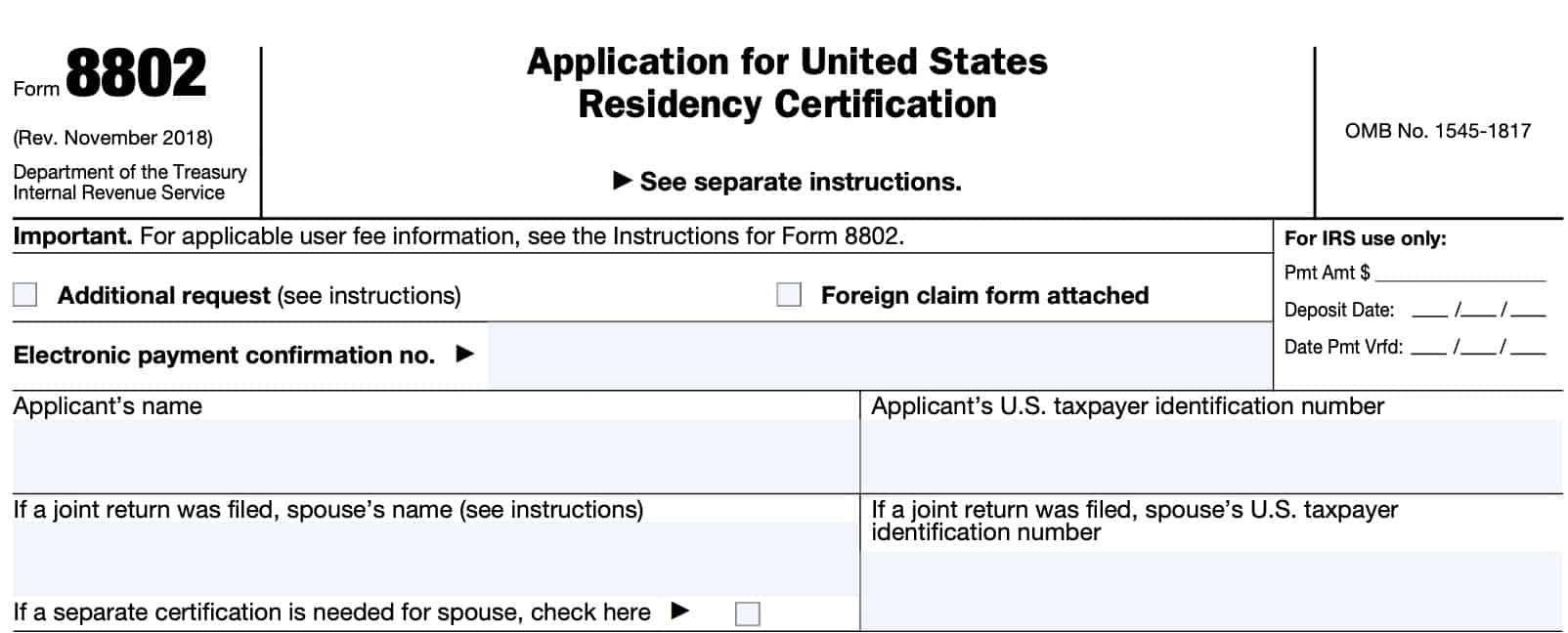

Top of the form

At the top of the form, there are two boxes:

- Additional request

- Foreign claim form attached

Let’s take a closer look at each box.

Additional request

Check this box if you are submitting IRS Form 8802 to request additional versions of IRS Form 6166 for a tax period for which the IRS has previously issued a Form 6166 to you. Additional requests on a separate Form 8802 will require a separate payment of the applicable nonrefundable user fee.

Foreign claim form attached

If you have included a foreign claim form sent to you by a foreign country as part of your application, check this box. The submission or omission of a foreign claim form will not affect your residency certification.

If the IRS does not have an agreement with the foreign government to date stamp or otherwise process the form, the IRS will mail the foreign claim form back to you without processing the form.

Electronic payment confirmation number

Just below the two boxes for additional requests and foreign claims is a line for electronic payment confirmation. Once you have paid your user fee charge on the IRS’ electronic payment page, you should receive a confirmation number. Enter this number in the provided field.

Taxpayer information

Below the electronic confirmation field, enter the following required information:

- Taxpayer name

- Taxpayer identification number

- Spouse’s name & taxpayer identification number (if you previously filed a joint income tax return)

Additionally, there are a few minor notes that you want to keep in mind.

First, if your spouse needs a separate certification, check the applicable box.

Second, ensure that the information you enter here exactly matches the taxpayer information on the U.S. return filed for the tax period(s) for which certification will be based. If the IRS did not previously require you to file an income tax return, then enter this information exactly as it appears on the most recent documentation that you’ve previously sent to or received from the Internal Revenue Service.

Finally, if the taxpayer’s name has changed since the most recent IRS Form 8802 filing, then you must submit the Form 8802 and tax disclosure authorization under the taxpayer’s new name. In addition, you must submit documentation of the name change with the signed copy of Form 8802.

Examples of sufficient documentation include:

- Trust agreement documents

- Corporate charter

- Marriage or divorce documents

Let’s move on to Line 1.

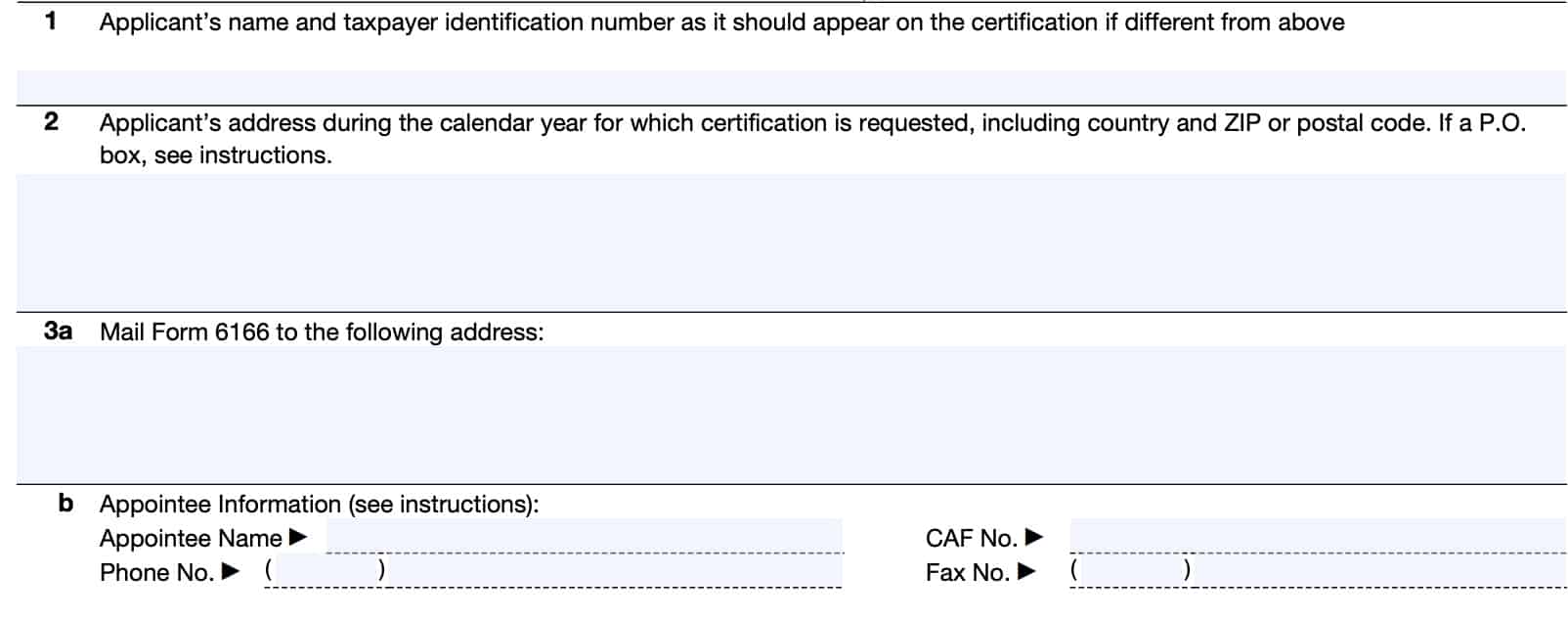

Line 1: Applicant’s name & TIN

Only complete Line 1 if the applicant’s name and taxpayer identification should appear on the certificate of residency, if it is different from the taxpayer information field, above.

Line 2: Applicant’s address

Enter the applicant’s address during the calendar year for which you are requesting certification. This address should include country & zip code or postal code.

The instructions for Form 8802warn taxpayers not to enter a P.O. box number or c/o address. The IRS might deny your application if you enter a post office box number or c/o address.

U.S. residents living outside the United States

If you are in any of the following categories for either the current year or prior year for which you request certification, you must submit a statement and documentation, as described below, with Form 8802.

- Dual residents: You are a resident of the United States and the treaty country for which you are requesting certification.

- Green card holders: You are either:

- A lawful permanent resident of the United States, or

- A U.S. citizen who filed IRS Form 2555 to claim the foreign tax credit.

- Bona fide residents: You are a bona fide resident of a U.S. possession.

Dual residents

If you are a dual resident, you must provide documentation to establish that you are a resident of the United States under the tie-breaker provision in the residence article of the tax treaty with the country for which you are requesting certification.

If you request certification for multiple foreign countries or foreign governments, you may need to verify this for multiple tax treaties.

Green card holders & Bona fide residents of a U.S. possession

If you are a green card holder or a bona fide resident of a U.S. possession, you must attach a statement and documentation to establish why you believe the federal government should certify you as a resident of the United States under the relevant treaty.

Under many U.S. treaties, U.S. citizens or green card holders who do not have a substantial presence, permanent home, or habitual abode in the United States during the tax year are not entitled to treaty benefits.

U.S. citizens or green card holders who reside outside the United States must examine the specific treaty to determine if they are eligible for tax benefits and U.S. residency certification under the terms of that treaty.

Green card holder involved in teaching or research activities

If you are a green card holder and are claiming income tax treaty benefits under a provision applicable to payments received in consideration of teaching or research activities, you must provide a specific penalties of perjury statement.

You can do this in Line 10, or by attaching a separate document to your completed form. See the IRS Form 8802 instructions for specific verbiage required for your penalty of perjury statement.

Exceptions

You do not need to attach the additional statement or documentation requested if you are a U.S. citizen or green card holder, and both of the following apply:

- You are requesting certification only for Bangladesh, Bulgaria, Cyprus, Hungary, Iceland, India, Kazakhstan, Malta, New Zealand, Russia, South Africa, Sri Lanka, or Ukraine; and

- The country for which you are requesting certification and your country of residence are two different countries

Line 3: Address to mail certificate of residency

The IRS will mail your certification of U.S. tax residency and any related correspondence either to:

- Yourself, or

- A third party that you designate in writing

If you provide an address on Line 3a, the IRS will use this address for all mail correspondence relating to your Form 6166 request. Otherwise, the IRS will mail Form 6166 to the address on Line 2.

If the mailing address entered on Line 3a is for a third party appointee, you must provide written authorization on Line 3b for the IRS to release the certification to the third party. You must provide the following additional information about your appointee:

- Appointee name

- Phone number

- CAF number

- CAF, known as Centralized Authorization File, is the IRS-managed records system that contains taxpayer powers of attorney and tax information authorization records. The IRS uses the CAF system to ensure safeguard taxpayer information.

- A CAF number is a unique nine-digit number. The IRS assigns a CAF number to each tax professional the first time he or she files for third-party authorization.

- Telephone number

- Fax number

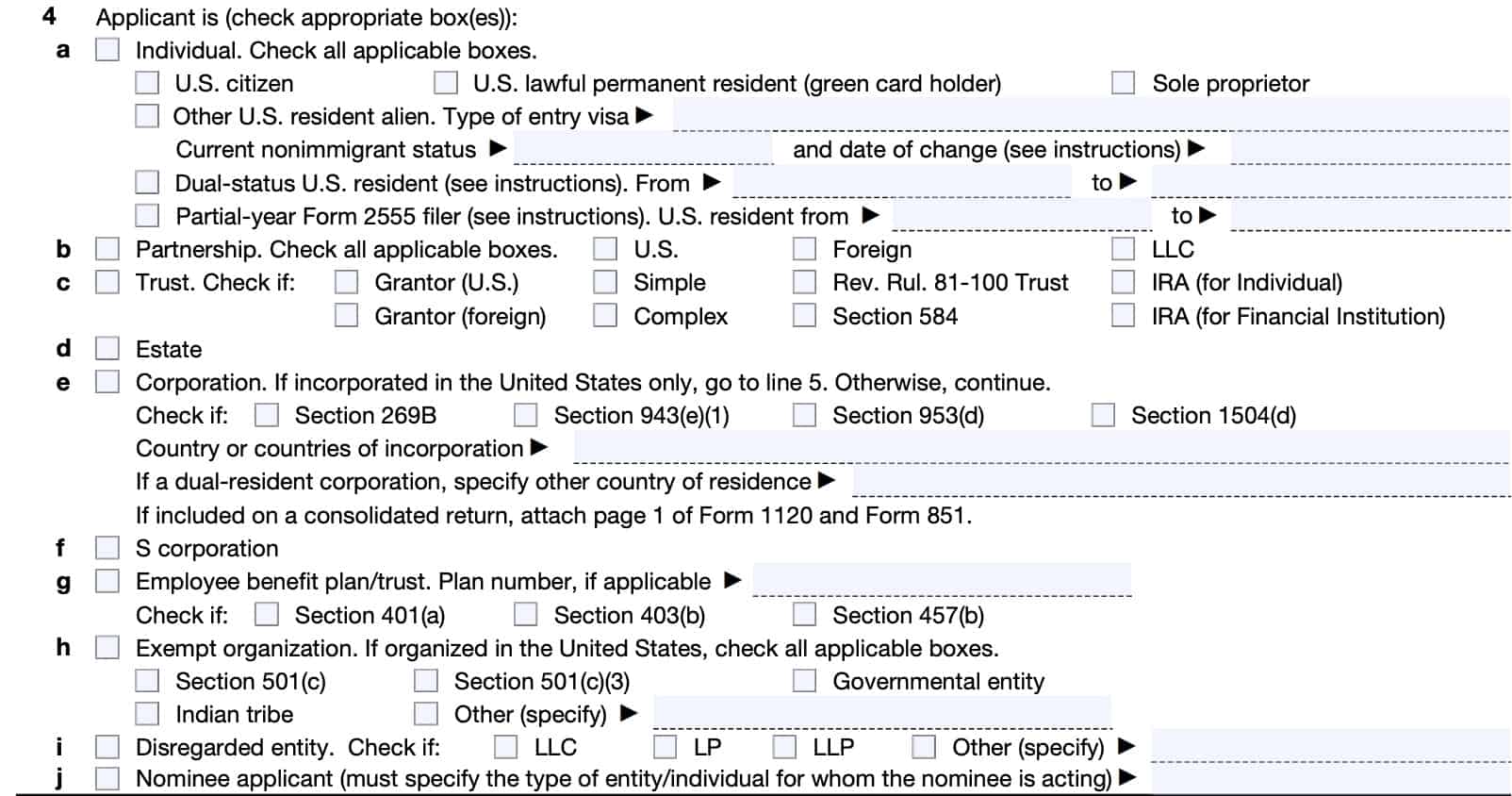

Line 4: Applicant information

In Line 4, check any of the boxes, as applicable, then follow the instructions provided for each box.

- Line 4a: Individual

- Line 4b: Partnership

- Line 4c: Trust

- Line 4d: Estate

- Line 4e: Corporation

- Line 4f: S corporation

- Line 4g: Employee benefit plan or trust

- Line 4h: Exempt organization

- Line 4i: Disregarded entity

- Line 4j: Nominee applicant

Line 4a: Individual

Individual taxpayers should check all of the applicable boxes below, then follow the specified instructions.

- U.S. citizen

- U.S. lawful permanent resident (green card holder)

- Other U.S. resident alien

- Dual-status U.S. resident

- Partial-year Form 2555 filer

- Sole proprietor

Green card holder

If you are a resident alien with lawful permanent resident status who recently arrived in the United States and you have not yet filed a U.S. income tax return, you should provide a copy of your current Form I-551.

Instead of a copy of your green card, you can attach a statement from U.S. Citizenship and Immigration Services (USCIS) that gives the following information:

- Alien registration number

- Date and port of entry

- Date of birth

- Classification

IRS Publication 519, U.S. Tax Guide For Aliens, contains more information to help determine your U.S. resident status for federal tax purposes.

Other U.S. resident alien

An individual who is not a lawful permanent resident of the United States but who meets the “substantial presence test” under Internal Revenue Code Section 7701(b) is a resident alien for purposes of U.S. taxation.

You must attach a copy of your current Form I-94 if:

- You are a resident alien under the substantial presence test and

- You have not yet filed a U.S. income tax return for the year for which certification is requested

Enter the date (YYYYMMDD) your status changed on the line provided.

Dual-status U.S. resident

An individual is a dual-status alien for U.S. tax purposes if the individual is:

- A part-year resident alien and

- A part-year nonresident alien during the calendar year(s) for which certification is requested.

Dual-status generally occurs in the year an individual acquires status as a U.S. resident or terminates such status. For example, you may be a dual-status resident if you are a nonresident alien but due to meeting the substantial presence test become a resident alien during the same calendar year.

If you checked the dual-status box, enter the dates (YYYYMMDD) that correspond to the period that you were a resident of the United States during the year(s) for which you are requesting certification of U.S. tax residency.

Partial-year Form 2555 filer

Check this box if you filed a Form 2555 that covered only part of a year for which certification is requested. For each year that this applies, enter the 8-digit dates (YYYYMMDD) that correspond to the beginning and ending of the period you were a U.S. resident.

Sole proprietor

On Line 6, include the following:

- Type of tax return

- Name

- Taxpayer identifying number

- Any information that would be required for the individual that filed Schedule C

Special notes

Special instructions apply for students, teachers, and trainees. See the IRS Form 8802 instructions for specific details, based upon your situation.

Also, if you intend to make the first-year election under IRC Section 7701(b)(4), see the Form 8802 instructions for more details.

Line 4b: Partnership

U.S. income tax treaties do not consider partnerships to be U.S. residents within the meaning of the residence article. The federal government does not recognize a domestic partnership as a U.S. resident, even if all partners are U.S. residents, and none of the partners are residents of other countries..

Treaty benefits are only available to a partner who is a U.S. resident whose distributive share of partnership income includes the item of income paid to the partnership.

Check the appropriate box(es) and provide the following with your completed Form 8821:

- The name and TIN of each partner for which certification is requested as well as any additional information that would be required if each individual partner was requesting certification

- Written authorization from each partner, including all partners listed within tiered partnerships. Each authorization must explicitly allow the third party requester to receive the partner’s tax information and must not address matters other than federal tax matters.

- IRS Form 8821 can serve as written authorization

- Unless the requester is a partner in the partnership during the tax year for which certification is requested, authorization from the partnership must explicitly allow the third party requester to receive the partnership’s tax information. The authorization must not address matters other than federal tax matters.

Line 4c: Trust

For trusts, check the appropriate box(es), then follow the IRS form instructions for specific details, based upon the type of trust involved.

Line 4d: Estate

If you are requesting US residency certificates on behalf of the estate of a decedent, you must include proof that you are the executor or administrator of the decedent’s estate. Proof can include a court certificate naming you executor or administrator of the estate.

U.S. residency certification will be based on the tax information and residency of the decedent.

Line 4e: Corporation

Check the appropriate box, and enter the country (or countries) of incorporation. If included on a consolidated return, attach the following:

- Page 1 of IRS Form 1120

- IRS Form 851, Affiliations Schedule

In general, a corporation is a resident entitled to U.S. residency certification only if it is incorporated in the United States. An unincorporated domestic entity, such as an LLC, can be considered a resident for federal tax purposes if it is an association taxable as a corporation.

Certain foreign corporations can be treated as domestic corporations if they qualify as U.S. corporations under one of the following:

- IRC Section 269B: Stapled entities

- IRC Section 953(d): Foreign insurance company electing treatment as a domestic corporation

- IRC Section 1504(d): Subsidiary formed to comply with foreign law

- Only available to Canadian and Mexican corporations

Corporations requesting U.S. residency certification on behalf of their subsidiaries must also submit the following required attachments:

- A list of the subsidiaries

- IRS Form 851, Affiliations Schedule, filed with the corporation’s consolidated return

Line 4f: S-corporation

The U.S. government does not recognize S corporations to be U.S. residents within the meaning of the residence article of U.S. income tax treaties. Treaty benefits are only available to an S-corporation shareholder who is a U.S. resident for purposes of the applicable treaty.

You must include the following from each S-corporation shareholder with Form 8802.

- The name and TIN of each shareholder for which certification is requested

- Any additional information that would be required if certification were being requested for each shareholder

- Written authorization from each shareholder.

- Each authorization must explicitly allow the third party requester to receive the shareholder’s tax information and must not address any matters other than federal tax matters.

- IRS Form 8821 can be used

Additionally, unless the requester is a shareholder in the S corporation during the tax year for which certification is requested, authorization from an officer with legal authority to bind the corporation must explicitly allow the third party requester to receive the corporation’s tax information. The authorization must not address matters other than federal tax matters.

Line 4g: Employee Benefit Plan or Trust

Enter the plan number and check the appropriate box.

Trusts that are part of an employee benefit plan required to file Form 5500 must include a copy of the signed Form 5500 with their residency certification application.

An employee plan must also include a copy of the employee benefit plan determination letter if either of the following apply:

- The employee plan is not subject to the Employee Retirement Income Security Act (ERISA), or

- Is not required to file IRS Form 5500

An employee plan that is not required to file Form 5500 and does not have a determination letter must provide evidence that it is entitled to certification. It must also provide a statement, under penalties of perjury, explaining:

- Why it is not required to file Form 5500 and

- Why it does not have a determination letter

Line 4h: Exempt organization

Check the applicable box.

In general, an organization that is exempt from U.S. income tax must:

- Have met its Form 990 series information return filing requirements; and

- Attach either of the following:

- A copy of either the organization’s determination letter from the IRS or

- The determination letter for the central organization if the organization is a subordinate in a group exemption

For further guidance, refer to the form instructions for exempt organizations.

Line 4i: Disregarded entity

Specify the type of disregarded entity (DRE).

The IRS does not consider disregarded entities to be U.S. residents within the meaning of the residence article of U.S. income tax treaties. Treaty benefits will only be available to a DRE owner who is a U.S. resident.

You may need to include additional information regarding the DRE’s owner information that may be required to be included with Form 8802. See Line 5 for more information.

Line 4j: Nominee applicant

Specify the type of entity or individual that the nominee is representing. You must provide all certification information required for each individual or entity for which you are acting as a nominee.

See the Line 4j instructions for additional details.

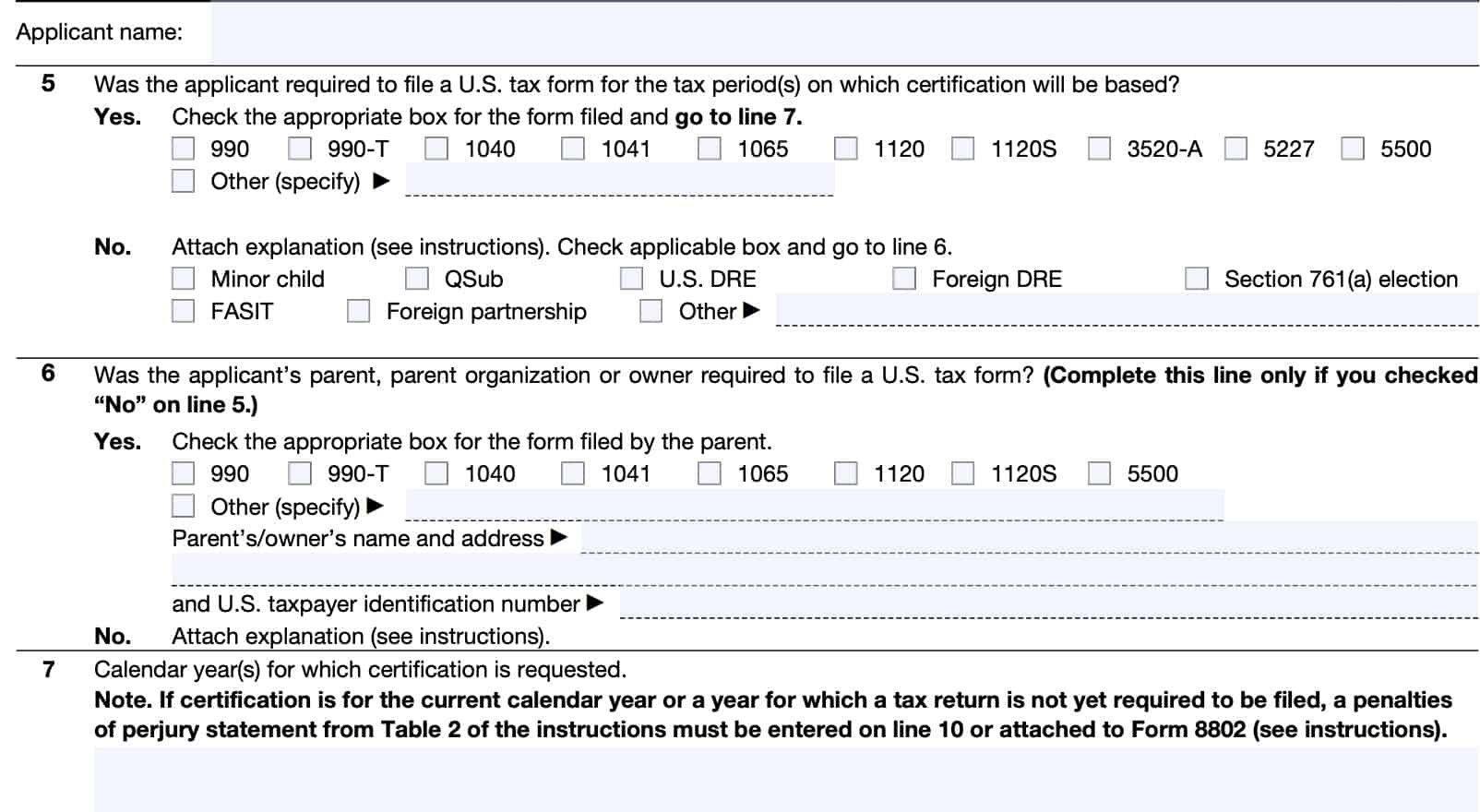

Line 5: Tax return information

If the applicant was required to file a U.S. tax form for the requested tax period(s), select ‘Yes,’ then specify the appropriate income tax return. Afterwards, go directly to Line 7.

If the applicant was not required to file a U.S. tax return, then select ‘No,’ check the applicable box, and attach a written explanation, based upon the specific circumstances. The IRS form instructions contain required statements for a variety of different tax situations.

Afterwards, proceed to Line 6.

Line 6: Owner, parent, or parent organization information

If you answered ‘Yes’ to Line 5, skip Line 6 and proceed to Line 7. If you answered ‘No,’ you must complete Line 6.

Answer whether or not the applicant’s parent, parent organization, or owner was required to file a U.S. tax form. If yes, check the appropriate box and enter the following information regarding the parent, parent organization or owner:

- Name

- Address

- Taxpayer identification number

For an application on behalf of a minor child, enter the name, address, and TIN of the parent who reported the child’s income.

If ‘No,’ then attach the following:

- Proof of the parent’s, parent organization’s, or owner’s income and

- A written explanation of why the parent is not required to file a tax return for the tax period(s) for which certification is based.

For disregarded entities, see the form instructions.

Line 7: Calendar years of requested certification

Select the certification year or years that you would like. You may request residency certification for the current year as well as any prior years.

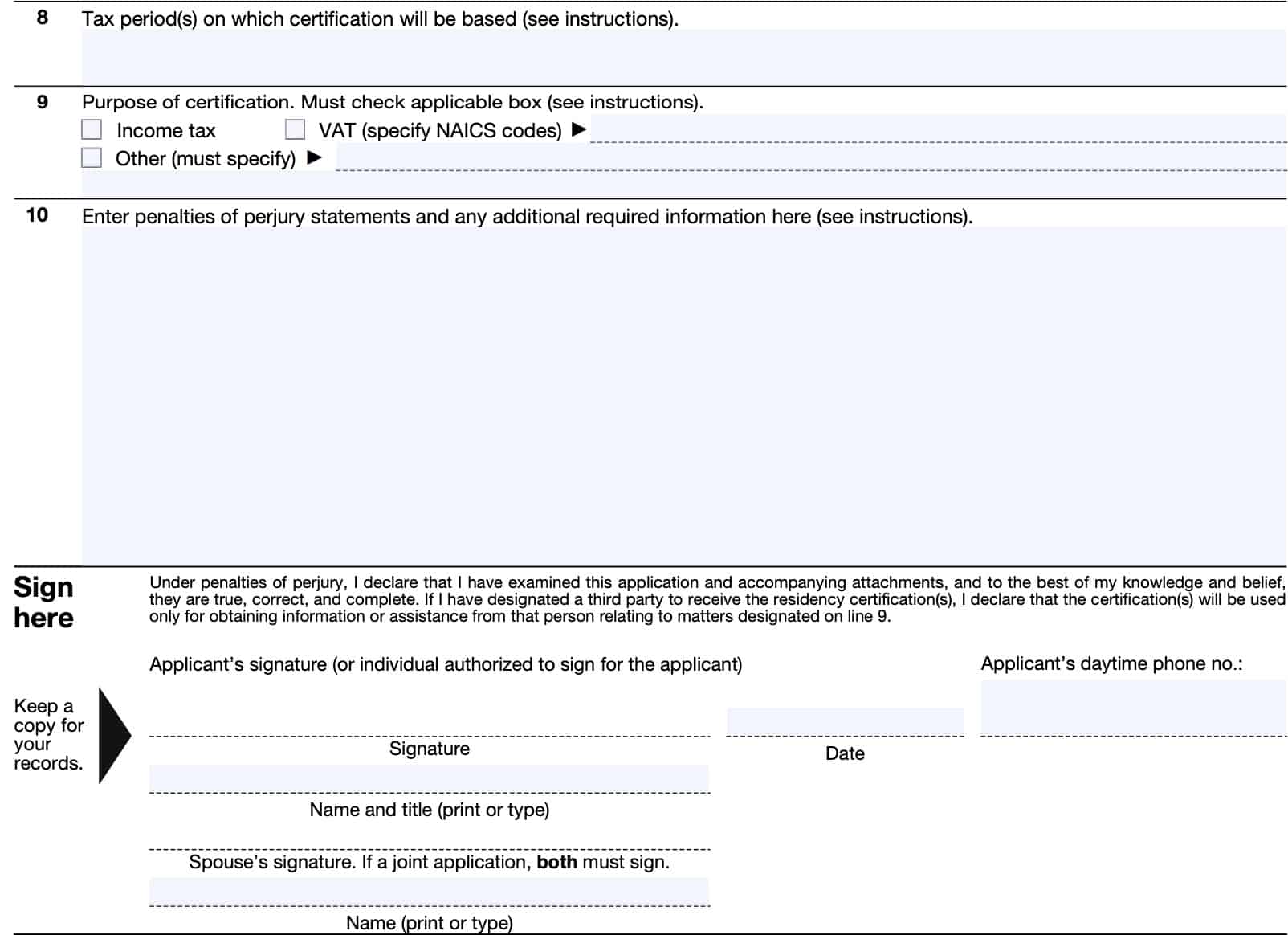

Line 8: Tax periods

In Line 8, enter the tax period or periods for which you need a letter of U.S. residency certification.

If you are requesting proof of residency for a tax period for which a tax return is not yet due, enter the 4-digit year and 2-digit month (YYYYMM) that correspond to the most recent return required.

If you are a fiscal year taxpayer, enter the year and month that correspond to the end of that fiscal tax year. For a prior year certification, the 4-digit year and 2-digit month should correspond to the end of the prior year tax period for which you are requesting certification.

Line 9: Purpose of certification

Indicate the purpose of your certification request.

Income tax treaty

If you are requesting certification to obtain benefits under an income tax treaty but you have requested certification for a nontreaty country, the IRS will return your application to you so that you can correct it.

Value added tax (VAT)

You can find the North American Industry Classification System (NAICS) codes in your tax return instructions.

If you do not provide an NAICS code on Form 8802 and one was not provided on the return you filed, the IRS will not automatically enter one. Form 6166 will only certify that you filed a return with a particular NAICS code if it matches the NAICS code on your application.

If you provide a code that does not match, Form 6166 will state that you represent that your NAICS code is as stated on Form 8802.

Line 10: Penalty of perjury statements

Enter the appropriate penalty of perjury statement, based upon your specific situation. A comprehensive list of penalty of perjury statement can be found in Table 2 of the form instructions.

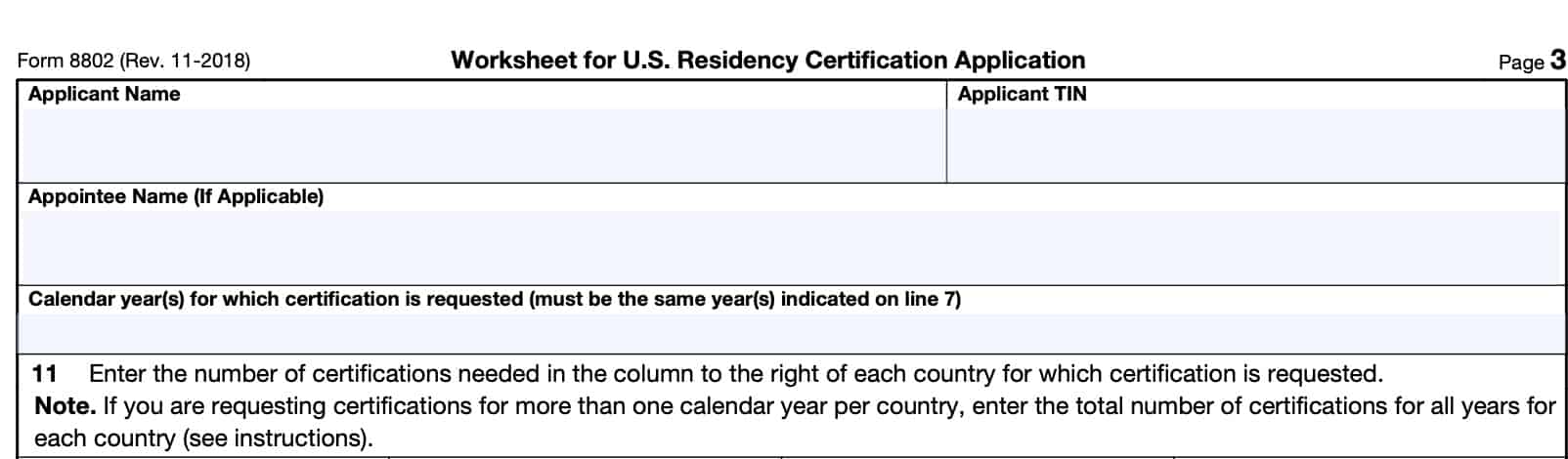

Line 11: Number of certificates for each country

On Page 3, you’ll need to complete the top of the form, containing the following information:

- Applicant name

- Taxpayer identification number

- Appointee name (if applicable)

- Calendar years requested

- Must reflect the same calendar year(s) as Line 7

Afterwards, there are four columns of foreign governments who are U.S. treaty partners.

Enter the number of residency certifications (Forms 6166) requested for each country listed in columns A, B, C, and D. For any country not listed, enter the country in the blank spaces at the bottom of column D.

If you are requesting certifications for more than one calendar year for a country, enter the number of certifications requested for all years to get the total number of certifications requested for that country.

For example, if you need 3 certifications for Germany each year from 2017 to 2020 (four total tax years), you would request 12 total certifications.

At the end of each column, enter the total certifications requested for all countries in that column.

| Column A | Column B | Column C | Column D |

| Armenia | Finland | Latvia | South Africa |

| Australia | France | Lithuania | Spain |

| Austria | Georgia | Luxembourg | Sri Lanka |

| Azerbaijan | Germany | Mexico | Sweden |

| Bangladesh | Greece | Moldova | Switzerland |

| Barbados | Hungary | Morocco | Tajikistan |

| Belarus | Iceland | Netherlands | Thailand |

| Belgium | India | New Zealand | Trinidad & Tobago |

| Bermuda | Indonesia | Norway | Tunisia |

| Bulgaria | Ireland | Pakistan | Turkey |

| Canada | Israel | Philippines | Turkmenistan |

| China | Italy | Poland | Ukraine |

| Cyprus | Jamaica | Portugal | United Kingdom |

| Czech Republic | Japan | Romania | Uzbekistan |

| Denmark | Kazakhstan | Russia | Venezuela |

| Egypt | South Korea | Slovak Republic | |

| Estonia | Kyrgyzstan | Slovenia |

Line 12: total number of certificates required

In Line 12, add the totals from all four columns. Enter the sum here.

Paying the user fee

The IRS charges a user fee for each IRS Form 8802 submitted for processing, not for each residency certification. The user fee ranges from $85 to $185 for each single form, depending on the type of taxpayer.

- Fee for individual applicants: $85

- Fee for non-individual applicants: $185

Users may pay this fee by check, money order, or electronic payment. Checks must be U.S. checks, as the IRS will not accept foreign checks.

Electronic payment

Taxpayers choosing to use electronic payment should go to the pay.gov website. This is different from the IRS website, so be mindful of this.

From there, type in “IRS Certs” in the search bar at the top right corner of the page. From there, select ‘Continue,’ then follow the prompts.

You will need to have the following information available:

- Applicant’s name

- Applicant’s TIN or EIN

- Submitter’s name

- Contact email address

- Contact phone number

- Number of Form(s) 8802 submitted

- Payment amount

- Selection of bank account or debit or credit card

- This will open a window for you to enter your account information

Your successful payment will provide an electronic confirmation number. You will need to enter this confirmation number at the top of the form, just above Line 1.

How do I file IRS Form 8802?

You can file IRS Form 8802 by fax, mail, or private delivery service (i.e. FedEx, UPS, etc.). The IRS recommends that you file your completed request no later than 45 days before you need the certification.

Below is guidance on how to file IRS Form 8802.

File by fax

You may fax your completed Form 8802 to one of the following fax numbers, depending on your location:

- 877-824-9110 (within the United States only, toll free)

- 304-707-9792 (inside or outside the United States, not toll free)

Keep in mind that you must use a fax cover sheet stating the number of pages in your fax submission. You can fax up to 10 separate applications (including all required attachments) for a maximum of 100 pages.

File by private delivery service

If using a private delivery service, use the following IRS address:

Internal Revenue Service

2970 Market Street

BLN# 3-E08.123

Philadelphia, PA 19104-5016

File by mail

There are two different mailing addresses. Choose the one that corresponds with your method of payment.

Electronic payment

Department of the Treasury

Internal Revenue Service

Philadelphia, PA 19255-0625

Check or money order enclosed

Internal Revenue Service

US Residency Certification

Philadelphia, PA 19255-0625

Video walkthrough

Watch this instructional video to learn more about obtaining a U.S. residency certification for tax purposes with IRS Form 8802.

Frequently asked questions

IRS Form 8802 is the Application for United States Residency Certification. Certain U.S. citizens and residents use Form 8802 to request proof of residency in the form of a tax residency certificate, also known as IRS Form 6166.

IRS Form 6166, Letter of U.S. Residency Certification, is a computer-generated letter printed on U.S. Department of Treasury stationery. Form 6166 certifies to U.S. treaty partners that the named individuals or entities are residents of the United States for income tax purposes. This helps U.S. residents avoid double taxation.

The Internal Revenue Service charges taxpayers a user fee to issue a certification of U.S. tax residency. This nonrefundable fee ranges from $85 to $185 per Form 8802 processed, regardless of the number of Form 6166 requests. Full payment of the user fee is required before the IRS will process Form 8802.

Where can I find IRS Form 8802?

You may find this form on the IRS website. For your convenience, we’ve attached the latest version to this article, below.

My husband and I are filling out the 8802 form requesting 6166 for the tax year 2023.

The example used for Line 10, Penalties of perjury statements, in the IRS instructions and in the video provided by teachmepersonalfinance.com is written in the present tense, i.e. “is” includes “the current tax year”.

Because we are requesting U.S. Residency Certification only for 2023, we would like to write:

10. “[His name & ss#] and [My name & ss#] were U.S. residents throughout the tax year 2023.”

Is this acceptable? Or do we use the suggested language provided and assume that “current” refers to 2023?

Thank you for your assistance.

I believe that you could use the past tense for this, although I couldn’t find a specific reference in the form instructions. The examples cited in the article and video were from Table 2 in the form instructions: “Current year penalties of perjury statements.”

Although I think this would be acceptable for a prior year statement, you can always confirm with the IRS before submitting your Form 8802.

Hello Mr. Baumhover,

Your website has saved my life. I was born in the US and hold a US passport.

I am living in Spain and hold a 2 year residence card.

I am volunteering with the American Red Cross on the US Navy Base; I am not being paid by the Red Cross.

I have a Base Post Office Box which is American that I can use for letters only.

I live off the base in the nearby town of Rota, Spain.

I live off my Navy pension.

In this situation, What address do I enter in Boxes 2 and 3 of form 8802?

Thank you,

Tanya

I would use your overseas mailing address. However, if you want a certificate to be mailed to a foreign country by express courier, you must provide a DHL prepaid label and envelope/box.

Since carriers require you to provide a pick-up address and a phone number on the pre-paid shipping label, the pick-up address and phone number is:

Internal Revenue Service

2970 Market St.

Philadelphia, PA 19104

267-466-1679