IRS Form W-4 Instructions

In 2020, as part of the Tax Cuts and Jobs Act, the Internal Revenue Service made major changes to IRS Form W-4, Employee’s Withholding Certificate. These changes are meant to help taxpayers ensure the proper amount of federal income tax is withheld from their paychecks.

In this article, we’ll walk you what you need to know about IRS Form W-4, including:

- How IRS Form W-4 works and how to complete it

- How to make adjustments based upon your tax return

- Frequently asked questions

Let’s start with a walkthrough of this tax form.

Table of contents

How do I complete IRS Form W-4?

There are 5 steps to completing IRS Form W-4:

- Step 1: Enter Personal Information

- Step 2: Multiple Jobs or Spouse Works

- Step 3: Claim Dependent and Other Credits

- Step 4: Other Adjustments

- Step 5: Sign Here

Let’s walk through each step, one at a time.

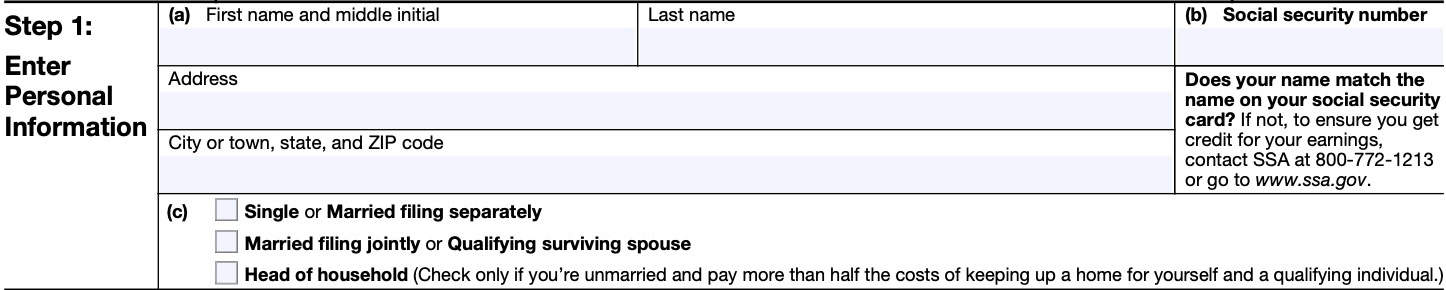

Step 1: Enter Personal Information

In this first step, you’ll enter your personal information.

Step 1(a)

Enter the following information

- First name & initial

- Last name

- Mailing address, including city, state, and zip code

Step 1(b)

Enter your Social Security number (SSN) as it appears on your Social Security card. If, for some reason, the name on your Social Security card doesn’t match your name, then you should check your earnings history with the Social Security Administration to make sure you’re receiving the appropriate credit for your Social Security withholding.

If you’re missing your Social Security card, you can request a new copy by filing Form SS-5, Application for Social Security Card.

Step 1(c)

Check the correct marital status. You can choose between:

- Single or married filing separately

- Married filing jointly or qualifying surviving spouse

- Head of household

- Only available if you are unmarried and you pay more than 50% of the costs to maintain a home for yourself and a qualifying individual

According to the form instructions, your selected marital status will be used to determine:

- Your standard deduction, and

- Tax rates used to calculate your tax withholding

Standard deductions for tax year 2026 are listed below.

2026 Standard deductions

According to the IRS, below are the 2026 standard deductions by tax filing status:

| Filing status | Standard deduction amount |

| Single | $16,100 |

| Married filing separately | $16,100 |

| Married filing jointly | $32,200 |

| Head of household | $24,150 |

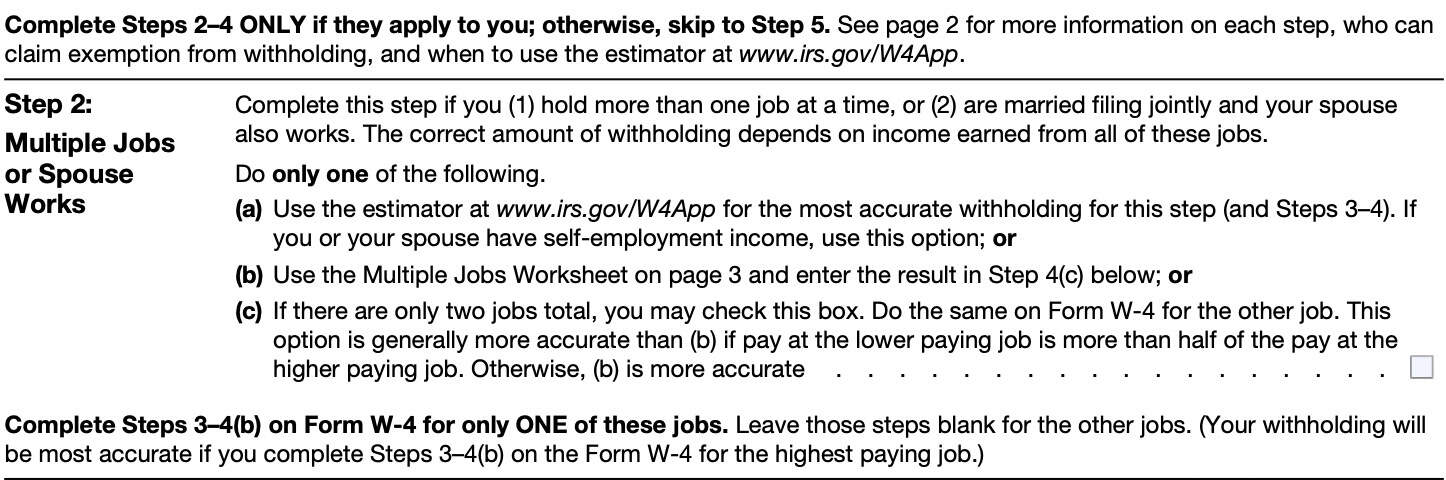

Step 2: Multiple Jobs or Spouse Works

The form instructions state that for Steps 2-4, you should only complete the ones that apply to your tax situation.

This means that you should only complete Step 2 if:

- You have a second job, or

- You are married filing a joint tax return, and both spouses work

In this situation, you have the choice between one of 3 federal income tax withholding methods:

- Use the IRS tax withholding estimator

- Complete the Multiple Jobs Worksheet on Page 3 of Form W-4, or

- Check the indicated box

Let’s evaluate each option a little more closely.

Use the tax estimator on the IRS website

You can use the online tax estimator, located on the IRS website, to help calculate your tax withholding, which will also help you with Steps 3 & 4, below.

The form instructions state that this is the most accurate withholding method of the three options available to you, particularly if you have self-employment income.

Below is an instructional YouTube video on how to use the online tax withholding tool.

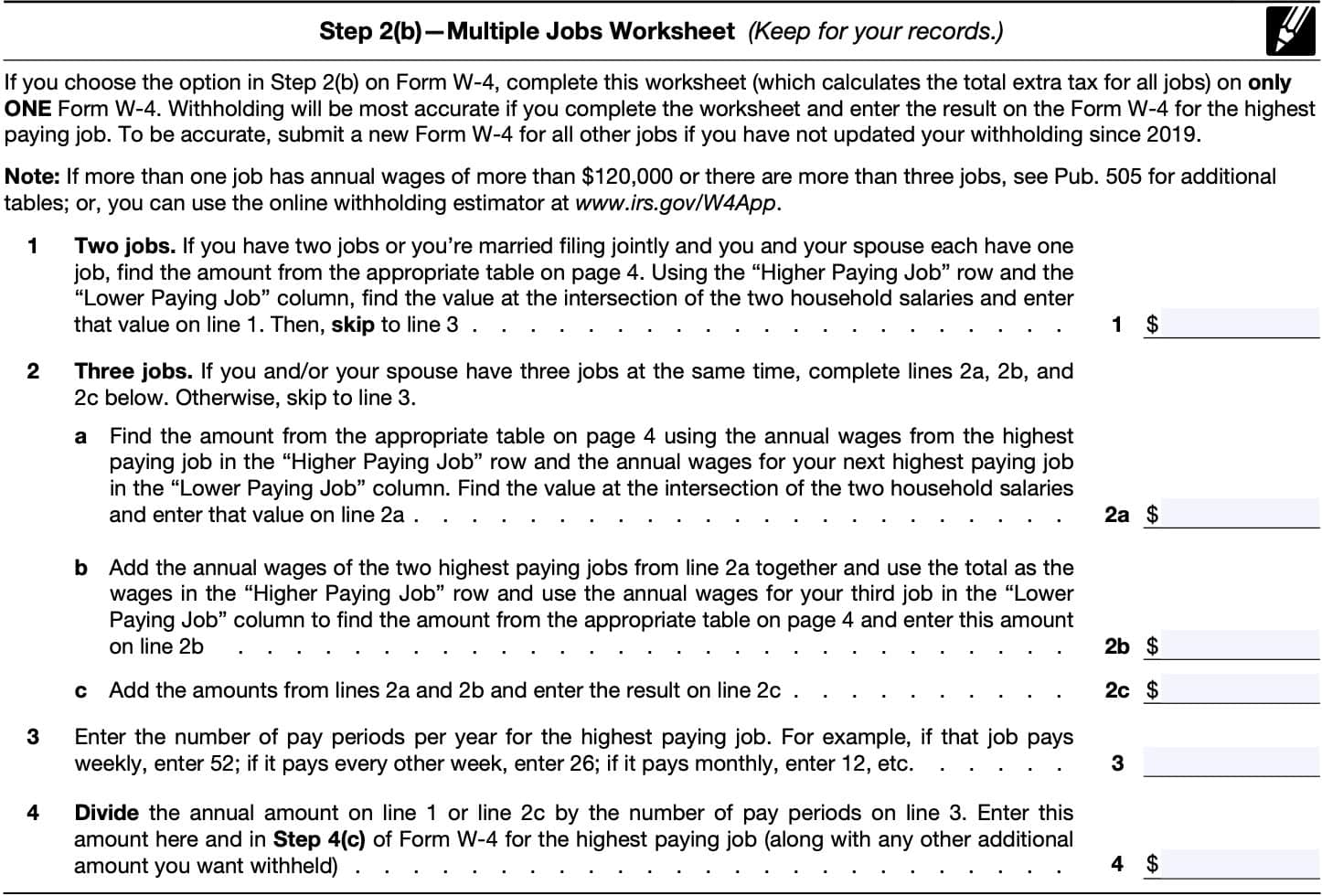

Complete the Multiple Jobs Worksheet on Page 3 of Form W-4

If you don’t have access to the online withholding estimator, you can complete the multiple jobs worksheet to determine how much federal income tax to withhold. Let’s take a closer look.

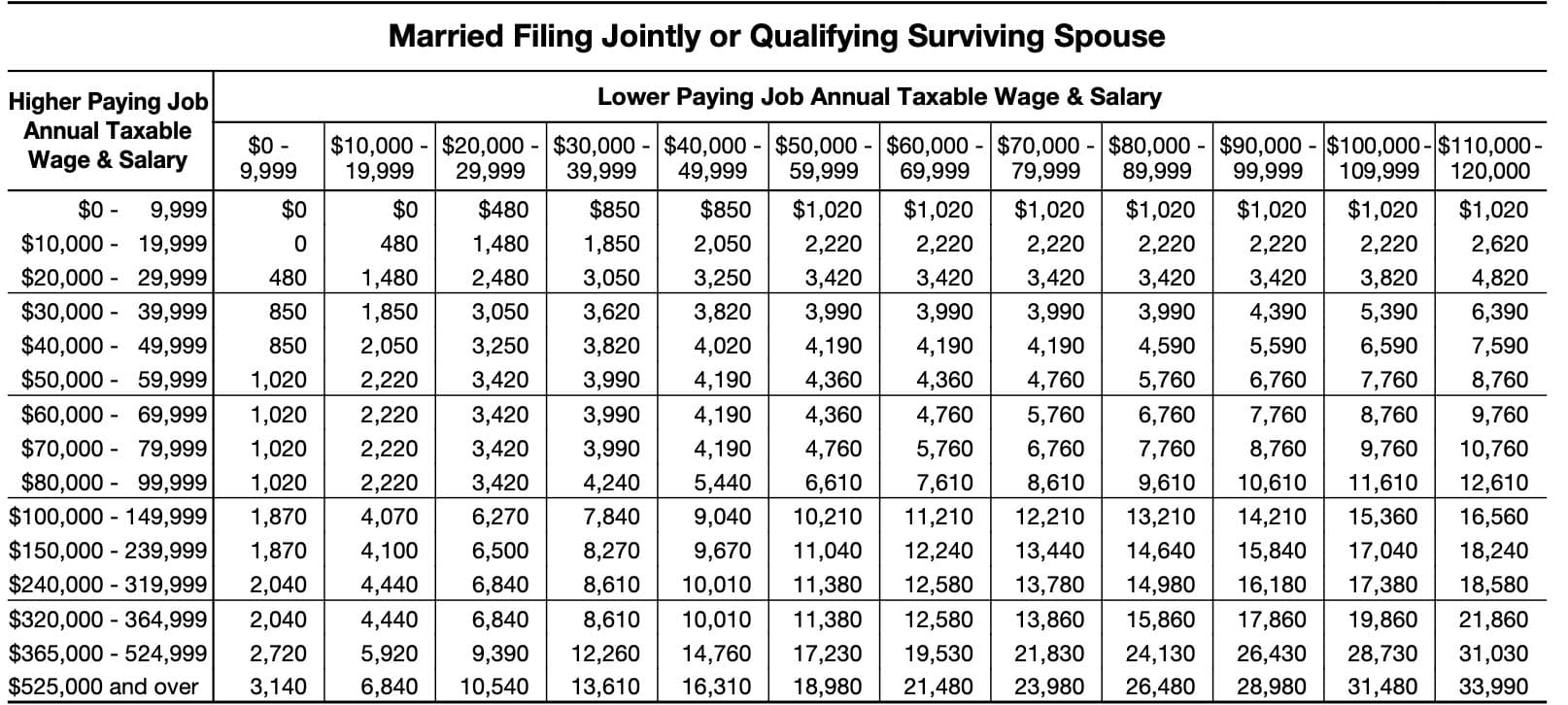

Line 1: Two jobs

You should use the appropriate withholding table, based upon your tax filing status if either of the following apply:

- You have two jobs, or

- You’re married filing jointly, and you and your spouse each have one job

Using the ‘Higher Paying Job’ row and the ‘Lower Paying Job’ column, you’ll find the correct dollar amount at the intersection of the two household salaries. Enter this value on Line 1, then skip to Line 3, below.

Below are the withholding tables by filing status.

Married filing jointly or qualifying surviving spouse

Use this table for married couples filing a joint tax return or for qualifying surviving spouses.

For example, if one spouse earns $75,000 per year and the other spouse earns $50,000 per year, the intersection of these two shows a value of: $4,760. You would enter $4,760 in Line 1 of this worksheet, then move on to Line 3.

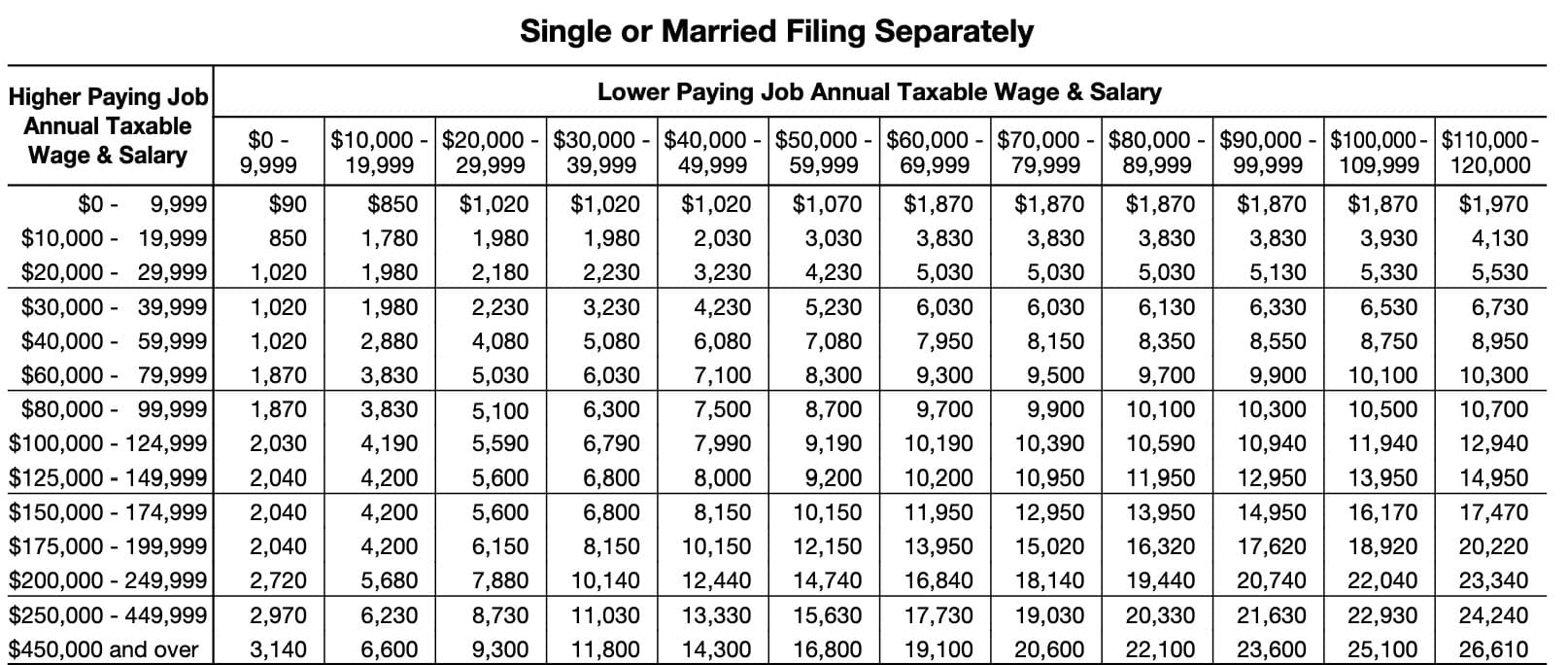

Single or married filing separately

Use this table for single taxpayers or married couples filing separate returns.

For example, if one spouse earns $75,000 per year and the other spouse earns $50,000 per year, the intersection of these two shows a value of: $8,300. You would enter $8,300 in Line 1 of this worksheet, then move on to Line 3.

Head of household

Use this table if you are a head of household.

For example, if you have one job earning $75,000 per year, and second job earning $50,000 per year, the intersection of these two shows a value of: $7,750. You would enter $7,750 in Line 1 of this worksheet, then move on to Line 3.

Line 2: Three jobs

If you and/or your spouse have 3 jobs, then you’ll need to complete Lines 2a-2c below. Otherwise, head directly to Line 3. Let’s start at Line 2a.

Line 2a

From the list below, use the appropriate table to determine the amount you should enter on Line 2a, with the values from your highest paying job and your next highest paying job.

- Married filing jointly or qualifying surviving spouse

- Single or married filing separately

- Head of household

Go to Line 2b.

Line 2b

Using the appropriate tables, add the annual wages of the two highest paying jobs from Line 2a together. Use this total in the ‘Higher Paying Job’ row. Use the annual salary for your third job in the ‘Lower Paying Job’ column.

Enter the amount from this intersection on Line 2b.

Line 2c

Add the amounts from Line 2a and Line 2b. Enter the total in Line 2c.

Line 3

Enter the number of pay periods per year for the highest paying job. Generally, pay periods follow one of the following patterns:

- Monthly: 12 pay periods per year

- Semi-monthly: 24 pay periods per year

- Bi-weekly: 26 pay periods per year

- Weekly: 52 pay periods per year

Helpful hint

Keep in mind the difference between biweekly pay period and a semimonthly pay period. Biweekly means that you are paid every two weeks. Semimonthly means that you are paid twice per month.

There are 2 additional pay periods for biweekly pay schedules (26) versus semimonthly schedules (24). Keeping this difference in mind can help you ensure the proper amount of taxes are being withheld.

Line 4

Divide either the Line 1 amount or the Line 2c amount by Line 3. This shows how much federal income tax you should add in the Extra withholding line in Step 4c for the highest-paying job, below.

If you had already calculated additional withholding to go into Step 4c, you may choose to add this result to the additional amount, then put the total in Step 4c.

Check the indicated box

If there are only two jobs, then you may check the box here. If there are two Forms W-4, then check the box on the other form as well.

What happens if you check the indicated box

If the box is checked, the standard deduction and tax brackets will be cut in half for each job to calculate withholding.

This option is accurate for jobs with similar pay, specifically if the lower paying job is more than half the pay of the higher paying job. Otherwise, more tax than necessary may be withheld. The extra withholding becomes larger as the difference in pay between the two jobs increases.

While withholding extra tax might result in a larger refund come tax time, you’re giving Uncle Sam an interest-free loan by doing so. You’ll likely receive a bigger paycheck (and a smaller tax refund) if you use the Multiple Jobs Worksheet when necessary.

Step 3: Claim Dependent and Other Credit

You should complete Step 3 for only one of your jobs. Leave the steps blank for the other jobs.

The Internal Revenue Service suggests that you complete Steps 3-4(b) for the highest paying job to ensure the most accurate tax withholding.

You only need to complete Step 3 if you are eligible for the child tax credit or credit for other dependents on Schedule 8812.

However, you may also enter other income tax credits that you may be eligible for at the bottom of Step 3. Below is a partial list of tax credits that you may enter here, as well as the associated tax form:

- Foreign tax credit: IRS Form 1116

- Education credits: IRS Form 8863

- Residential energy credits: IRS Form 5695

You can find a more comprehensive list of available tax credits on Schedule 3, Additional Credits & Payments.

Child tax credit or credit for other dependents

To qualify for the child tax credit, your child must:

- Be under age 17 as of December 31 of the current year

- Be your dependent who generally lives with you for more than half the tax year

- Have a Social Security number

You may be able to claim a tax credit for other dependents if you cannot claim the child tax credit. This could include an older child or a qualifying relative.

In Step 3, you’ll multiply the number of qualifying children by $2,000. Enter this amount in the top row.

Next, multiply the number of dependents that you can claim by $500. Enter the total in the next line.

Finally, add the total amount of tax credits (including any other tax credits you may be eligible for) in Step 3.

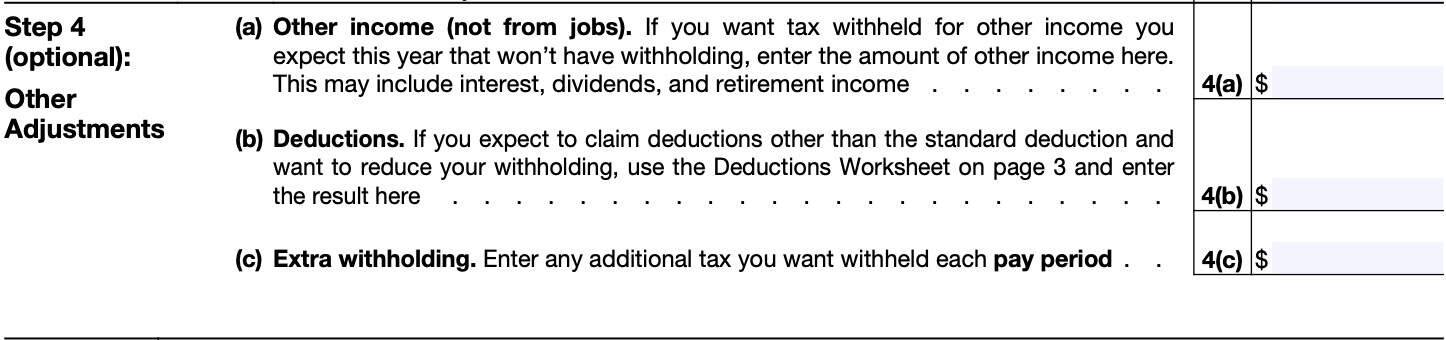

Step 4: Other Adjustments

These are optional fields.

You should only complete Steps 4a and 4b for one of your jobs. Leave the steps blank for the other jobs. The Internal Revenue Service suggests that you complete Steps 3-4(b) for the highest paying job to ensure the most accurate tax withholding.

Step 4(a): Other income (not from jobs)

Use Step 4(a) if you are expecting additional income that does not have withholding. This might include income items such as:

- Interest income (reported on IRS Form 1099-INT)

- Dividend income or capital gains distributions (from IRS Form 1099-DIV)

- Retirement income (from IRS Form 1099-R)

Before making any adjustments to your current tax withholding for these items, it’s a good idea to double check your 1099 forms from the prior year to make sure you’re not already having taxes withdrawn from these income sources.

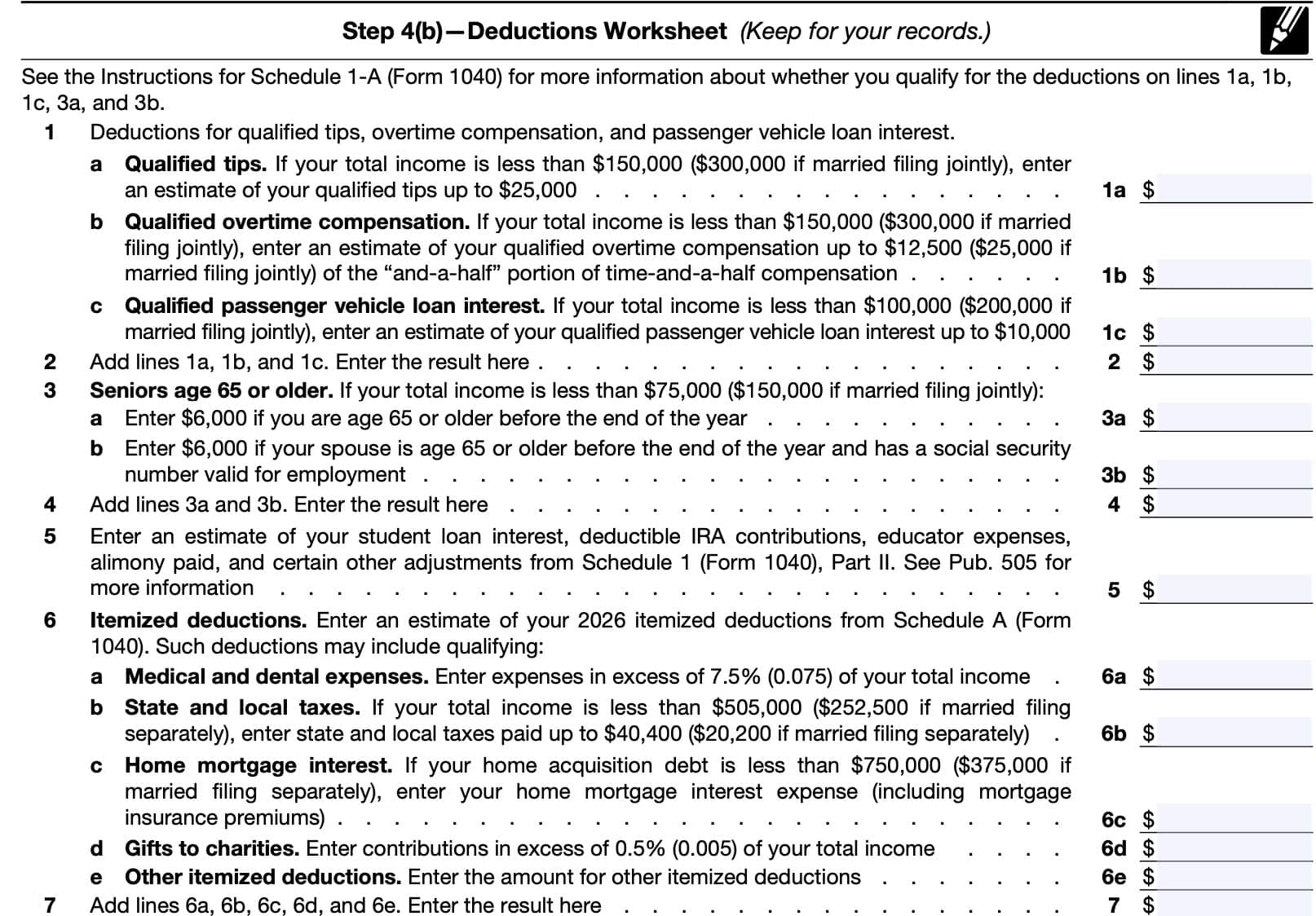

Step 4(b): Deductions

If you do not expect to claim the basic standard deduction (such as itemized deductions on Schedule A), then you can use the Deductions Worksheet to determine what to enter here.

Before beginning this worksheet, see the instructions for IRS Schedule 1-A to determine whether you qualify for deductions on any of the following:

- Qualified tips

- Overtime compensation

- Passenger vehicle loan interest

- Additional deduction for seniors age 65 and older

Line 1

This line contains deductions for qualified tips, overtime compensation, and qualified passenger vehicle loan interest.

In Line 1a, enter an estimate of your qualified tip income, not to exceed $25,000, if your total income is less than $150,000 (or $300,000 for married couples filing jointly).

In Line 1b, enter an estimate of your qualified overtime compensation, up to $12,500 (or $25,000 if married filing jointly). This only applies to taxpayers with total income of less than $150,000 (or $300,000 for married couples filing jointly.

In Line 1c, enter an estimate of your qualified passenger vehicle loan interest, up to $10,000, only if your total income is less than $100,000 ($200,000 for married couples filing a joint tax return).

Line 2

Add Lines 1a, 1b, and 1c. Enter the result here.

Line 3: Seniors age 65 and older

If your total income is less than $75,000 ($150,000 if you are married filing jointly), then enter $6,000 in Line 3a if you are age 65 or older by the end of the year. If your spouse is also age 65 or older (or will be by the end of the taxable year), and has a valid Social Security number, enter $6,000 in Line 3b as well.

Line 4

Add Lines 3a and 3b. Enter the total here.

Line 5

Enter an estimate of any income adjustments from Schedule 1 on your tax return:

- Deductible contributions to your individual retirement arrangement (IRA)

- Student loan interest, reported on IRS Form 1098-E

- Business expenses claimed on IRS Form 2106

- Health savings account deduction, from IRS Form 8889

- Moving expenses for members of the Armed Forces, from IRS Form 3903

- Deductible part of self-employment tax, as reported on Schedule SE

You may find additional information in IRS Publication 505, Tax Withholding and Estimated Tax.

Line 6: Itemized deductions

Enter your estimated itemized deductions. You may consider using estimates based on your Schedule A from last year. Deductions can include:

- Line 6a: Medical expenses (in excess of 7.5% of adjusted gross income)

- Line 6b: State and local taxes (up to a limit of $40,400 per year, if your total income is less than $505,000)

- $20,200 if married filing separately (if your total income is less than $252,500)

- Line 6c: Qualifying home mortgage interest

- Line 6d: Charitable contributions in excess of 0.5% of your total income

- Line 6e: Other itemized deductions. For example, certain taxpayers may also be able to include casualty and theft losses from IRS Form 4684.

Line 7

Add the following:

- Line 6a

- Line 6b

- Line 6c

- Line 6d

- Line 6e

Enter the total in Line 7.

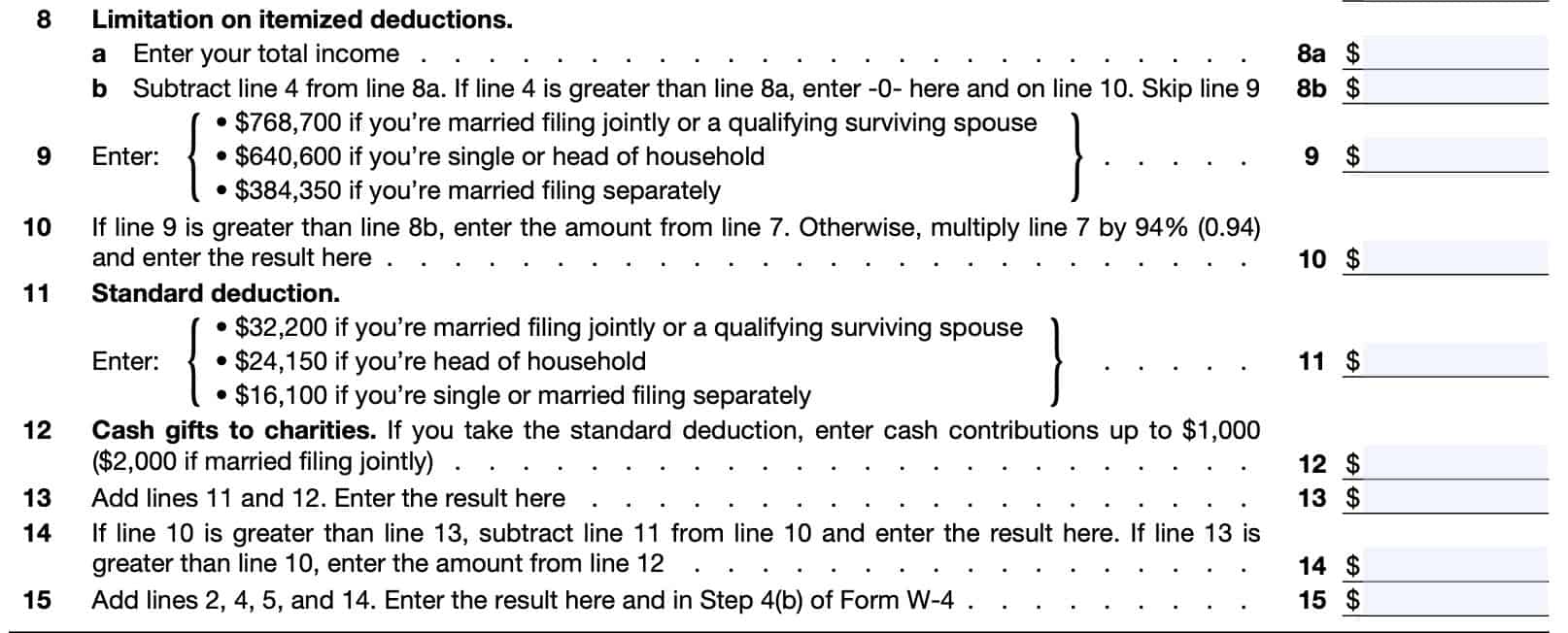

Line 8: Limitation on itemized deductions

In Line 8a, enter your total income.

Subtract Line 4 from Line 8a. Enter the result in Line 8b.

If Line 4 is greater than Line 8a, then enter zero here and on Line 10, below.

Line 9

Enter one of the following, based on filing status:

- Married filing jointly or qualifying surviving spouse: $768,700

- Head of household: $640,600

- Single or married filing separately: $384,350

Line 10

If Line 9 is greater than Line 8b, then enter the Line 7 amount here. Otherwise, multiply Line 7 by 94%, then enter the result here.

Line 11: Standard deduction

In Line 2, enter one of the following, based on your filing status:

- Married filing jointly or qualifying surviving spouse: $32,200

- Head of household: $24,150

- Single or married filing separately: $16,100

Line 12: Cash gifts to charities

If you take the standard deduction, enter cash contributions up to $1,000. Enter $2,000 if you are married filing jointly.

Line 13

Add Line 11 and Line 12. Enter the result here.

Line 14

If Line 10 is greater than Line 13, subtract Line 11 from Line 10 and enter the result here.

If Line 13 is greater than Line 10, enter the amount from Line 12.

Line 15

Add Lines 2, 4, 5, and 14. Enter the result here and in Step 4(b).

Step 4(c): Extra withholding

Enter the amount of federal income tax withholding that you calculated in Step 2 here. If you want to withhold additional federal taxes to avoid a big tax bill, you can increase this amount as you feel necessary.

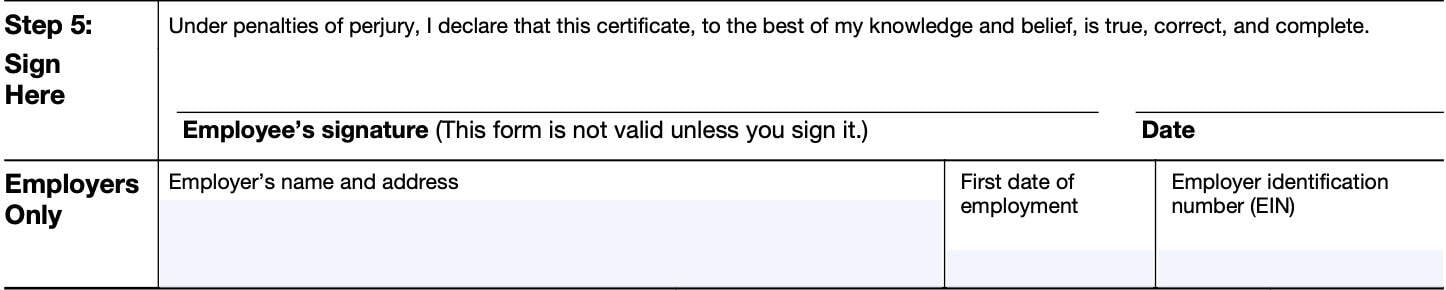

Step 5: Sign here

Sign in Step 5. If you don’t sign this part of the form, then your employer cannot withhold the correct amount of federal income taxes. Instead, your employer will have to rely strictly on guidance from IRS Publication 15-T, Federal Income Tax Withholding Methods.

Video walkthrough

Watch this instructional video to learn about IRS Form W-4.

Do you have the correct withholding form?

If you’re reading this section, perhaps you’re not sure if you have the correct withholding form. Before you leave, here is a brief overview of the other tax withholding forms and their purpose.

IRS Form W-4P, Withholding Certificate For Periodic Pension Or Annuity Payments

Taxpayers complete IRS Form W-4P, Withholding Certificate for Periodic Pension or Annuity Payments to give their payer instructions on tax withholding for regular pension or annuity payments.

Watch this brief educational video to learn more IRS Form W-4P.

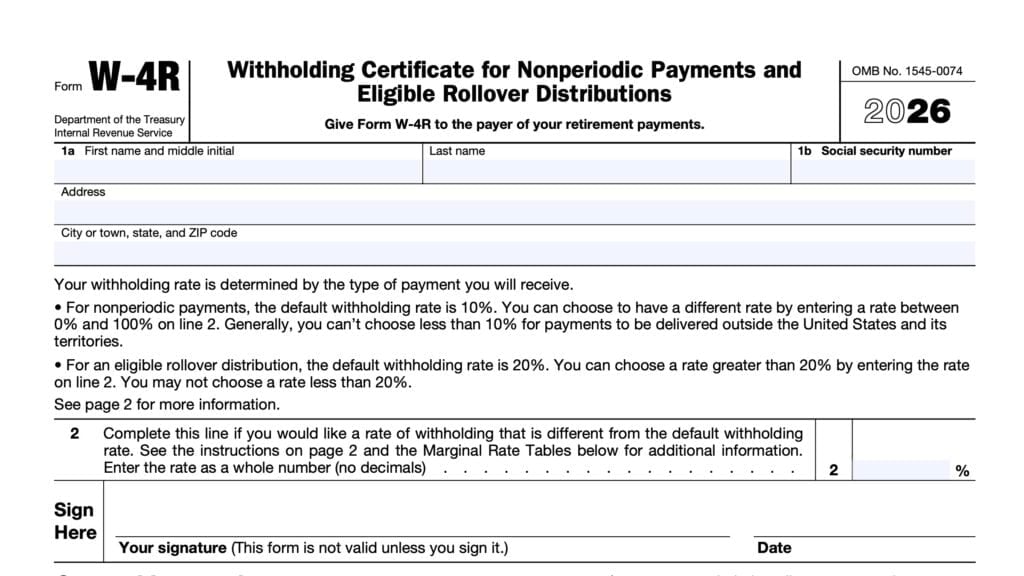

IRS Form W-4R, Withholding Certificate for Nonperiodic Payments and Eligible Rollovers

Taxpayers who wish to give instruction on nonrecurring payments, such as one-time IRA withdrawals, or eligible rollovers, can complete Form W-4R, Withholding Certificate for Nonperiodic Payments and Eligible Rollovers.

Watch this instructional video to learn more about how IRS Form W-4R works.

IRS Form W-4S, Request for Federal Income Tax Withholding from Sick Pay

Taxpayers who wish to have taxes withheld from sick pay issued by a third-party payer may complete IRS Form W-4S, Request for Federal Income Tax Withholding From Sick Pay.

For more detail on how IRS Form W-4S works, check out this video.

IRS Form W-4V, Voluntary Withholding Request

IRS Form W-4V, Voluntary Withholding Request, is the tax form that taxpayers may use to determine the amount of tax withheld from various government payments, such as:

- Social Security payments

- Tier 1 Railroad retirement benefits

- Unemployment benefits

- Payments from certain federal government benefit programs

Watch this video to learn more about how IRS Form W-4V works.

Are you tired of dreading tax season?

If you’re like most people, you push through the stress of filing, only to be hit with a bigger bill than expected—then put it all behind you until the same cycle repeats next year.

But what if you could change the game?

Tax planning puts you in control. It’s about being proactive, not reactive—taking small, smart steps throughout the year to reduce your tax burden, increase your savings, and keep more of your hard-earned money working for you.

Here’s what effective tax planning helps you do:

✅ Avoid the surprise of a high tax bill

✅ Understand how your income and decisions affect your taxes

✅ Strategically lower your tax liability over time

Ready to make smarter tax moves?

👉 Join my free weekly tax planning newsletter and get one actionable tip every week to help you reduce your taxes legally and effectively.

Start taking control—your future self will thank you.

Frequently asked questions

When you get a new job, your employer will usually offer a new W-4 form to complete. Otherwise, it’s a good idea to review your current tax withholding each year and file a new Form W-4 to make adjustments from the previous year as needed.

If a new employee doesn’t complete a Form W-4, then your employer may need to follow IRS guidance to employers. This generally will not provide the most accurate tax withholding. You may receive a much larger refund than expected, or owe more in federal income taxes.

I need help with completing IRS Form W-4!

You’ve had a chance to read the article and watch the self-help videos. Perhaps you’re still overwhelmed, or may be you’re still missing that one thing that puts everything together for you.

Either way, we can help!

If that’s the case, please use this link to schedule a one-on-one appointment with me to get unstuck!

Where can I find IRS Form W-4?

As with other tax forms, you may find IRS Form W-4 on the IRS website. For your convenience, we’ve enclosed the latest version here.

Hello if you file Form W-4P and don’t want Federal Tax withholding because you are U.S.A citizen living in Italy and paying all your taxes in Italy and reporting them yearly to IRS with your 1040 along with Form 8833(Treaty).. can your employer refuse to follow along with my choices? I have done it like that for 26 years and AT&T is refusing and still cannot get a formal answer from them and they are screwing my 2023….what could I do.. Sincerely & Desperate, Mercedes

According to the IRS instructions, “Generally, if you are a U.S. citizen or a resident alien, you are not permitted to elect not to have federal income tax withheld on payments to be delivered outside the United States and its territories.”

You can check with the IRS to see if there’s an exception, but I believe that AT&T is following the form instructions.