IRS Form 8960 Instructions

If your income is above a certain threshold, the Internal Revenue Service may require you to pay an additional tax, known as net investment income tax, on the excess earnings. If this is the case, you will also have to file IRS Form 8960 to report this income and calculate your increased tax liability.

This article will walk you through the basics of net investment income tax and provide step-by-step instructions on how to complete IRS Form 8960.

Table of contents

How do I fill out IRS Form 8960?

IRS Form 8960 contains one page, with three parts.

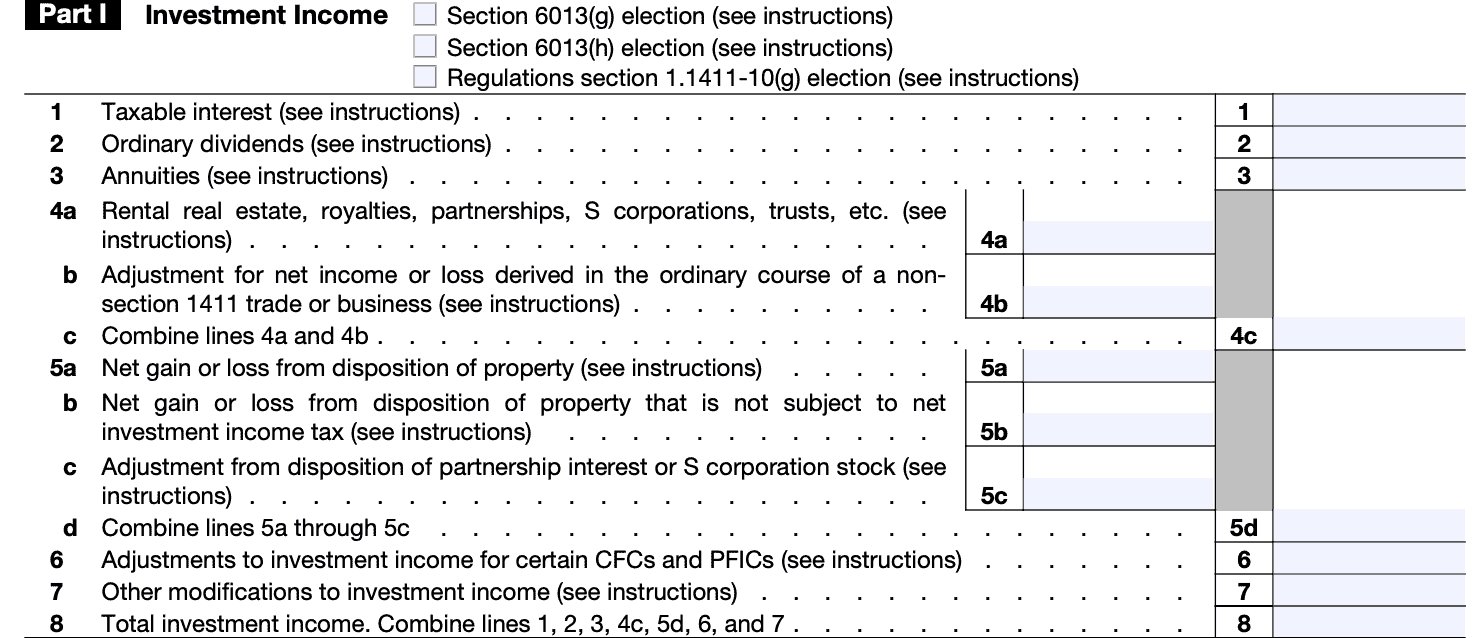

Part I: Investment Income

In Part I, we’ll go through lines 1 through 8 to determine total investment income.

Elections

At the top of the form, select any of the following elections that may apply:

- Section 6013(g): For a non-resident alien married to a U.S. resident or citizen by the end of the tax year

- Section 6013(h): Where at least one spouse was an NRA at the beginning of the tax year but became a U.S. resident or citizen by the end of the year

- Regulations Section 1.1411-10(g) Election: Applicable for taxpayers who own stock of a CFC or QEF

CFC-Controlled foreign corporation: A foreign corporation where 50% or more of the stock is owned by U.S. shareholders.

QEF-Qualified electing fund: A passive foreign investment company (PFIC) where the taxpayer has made an election under Section 1295(b) and the PFIC complies with IRS requirements for determining investment income and net capital gain.

Line 1: Taxable interest

Enter the amount of taxable interest received. You’ll find this information in one of the following:

- Form 1040 or Form 1040-SR, Line 2b

- Form 1041, Line 1

- Form 1041-QFT, line 1a

- Form 1040-NR, taxable interest received for period of U.S. residency shown on attached statement

Adjustments: Interest income earned in the ordinary course of a non-section 1411 trade or business is excluded from net investment income. If this type of interest income is included on Line 1, you will use Line 7 to adjust your net investment income.

Line 2: Ordinary dividends

Enter the amount of ordinary dividends received. You’ll find this information in one of the following:

- Form 1040 or 1040-SR, Line 3b

- Form 1041, Line 2a

- Form 1041-QFT, line 2a

- Form 1040-NR, taxable interest received for period of U.S. residency shown on attached statement

Adjustments: You will use Line 7 to adjust your net investment income if you received dividends from an employer stock ownership plan (ESOP) that are deductible under Section 404(k), or Alaska Permanent Fund dividends.

Line 3: Annuities

Enter total gross income from all annuities here, except if paid from the following:

- Section 401—Qualified pension, profit-sharing, and stock bonus plans

- Section 403(a)—Qualified annuity plans purchased by an employer for an employee

- Section 403(b)—Annuities purchased by public schools or section 501(c)(3) tax-exempt organizations

- Section 408—Individual Retirement Accounts (IRAs) or Annuities

- Section 408A—Roth IRAs

- Section 457(b)—Deferred compensation plans of a state and local government and tax-exempt organization

- Amounts paid in consideration for services

How annuities are reported

You’ll find annuity income in IRS Form 1099-R. Annuity income subject to NIIT will contain Code ‘D’ in Box 7.

Line 4a: Rental real estate, royalties, partnerships, etc

You’ll find this information in one of the following:

- Form 1040, Schedule 1, Line 5

- Form 1041, Line 5

- Form 1041-QFT, the portion of line 4 that’s income and loss that properly would be reported by a trust filing Form 1041 on

- Form 1041, line 5.

- Form 1040-NR, the amount of income that would apply for the time that you were a U.S. resident

Line 4b: Adjustment for net income or loss derived in the ordinary course of a non-section 1411 trade or business

Enter any of the following adjustments that are not includible in NIIT:

- Net income or loss from a section 162 trade or business that’s not a passive activity and isn’t engaged in a trade or business of trading financial instruments or commodities

- Net income or loss from a section 1411 trade or business that’s taken into account in determining self-employment income

- Royalties derived in the ordinary course of a section 162 trade or business that’s not a passive activity.

- Passive losses of a former passive activity that are allowed as a deduction in the current year by reason of Section 469(f)(1)(A)

There may be adjustments that you report on Line 7 instead of Line 4b. Please refer to the IRS instructions for more detail.

Line 4c: Combine Lines 4a and 4b

Self-explanatory.

Line 5a: Net gain or loss from disposition of property

The IRS form instructions contain worksheets to help taxpayers calculate net gains and losses on Lines 5a through 5d.

As a general rule, the following are includible in net investment income if included in taxable income:

- Any net gain from the disposition of property not used in a trade or business

- Net gain or loss from the disposition of property held in a Section 1411 trade or business

You will find the net gain or loss from disposition of property by combining the following from your properly completed tax return:

- Form 1040 or 1040-SR, Line 7, and Schedule 1 (Form 1040), Line 4

- Form 1041, Lines 4 and 7.

- Form 1041-QFT, Line 3, and the portion of Line 4 attributed to ordinary gain/(loss).

- Form 1040-NR, the amounts that would be properly reported on Form 1040 or 1040-SR, and Schedule 1 for the period of U.S. residency

Line 5b: Net gain or loss from disposition of property not subject to NIIT

Include the net gain or loss from disposition of property not subject to net investment income tax. This might include:

- Gain or loss from the sale of property held in a non-section 1411 trade or business

- Gain attributable to net unrealized appreciation (NUA) in employer securities held by a qualified plan

- Adjustments to capital loss carryforwards for items of excluded loss

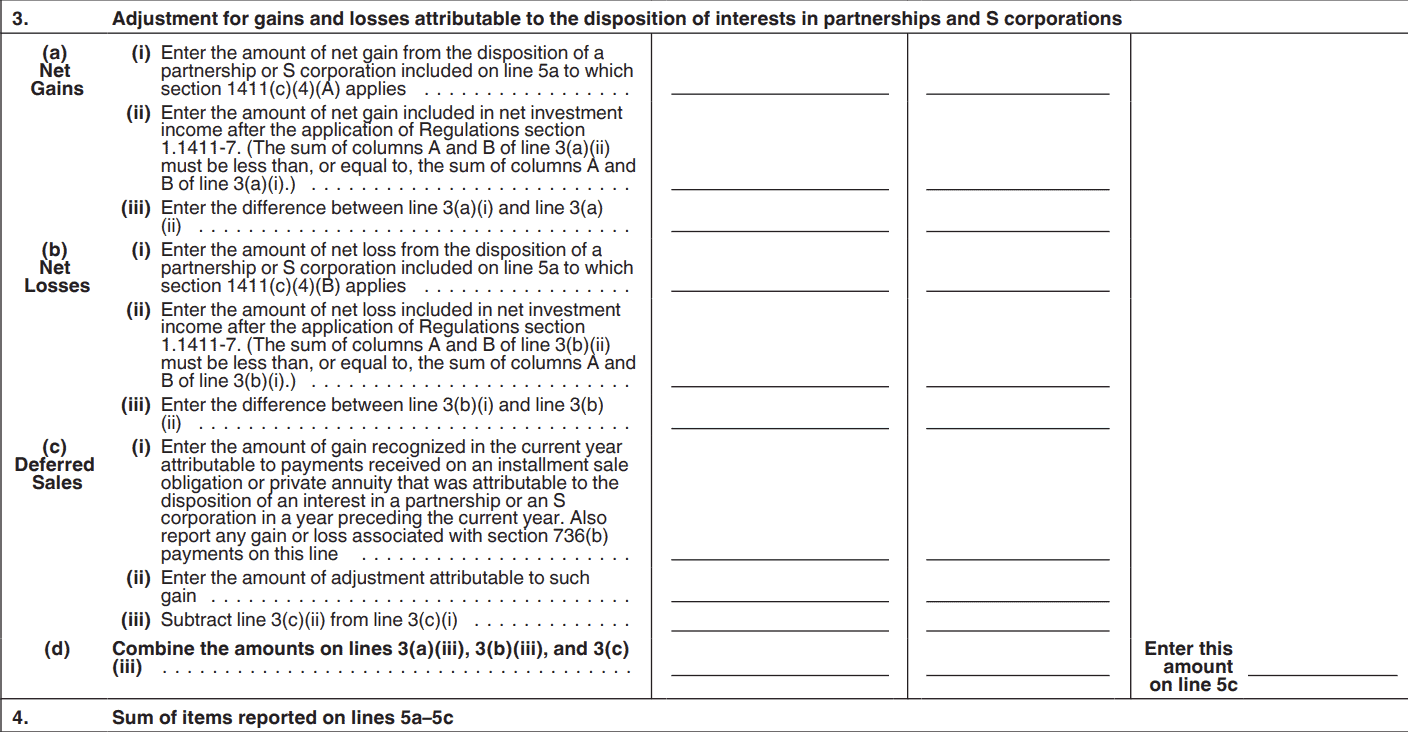

Line 5c: Adjustment from disposition of partnership interest or S corporation stock

Enter any adjustments from the worksheet in Part II, line 3d.

Line 5d: Combine Lines 5a through 5c

Self-explanatory.

Line 6: Adjustments to investment income for certain CFCs and PFICs

Might not apply to most taxpayers.

If you own stock, directly or indirectly, in a CFC or a PFIC, use line 6 for adjustments necessary to calculate your net investment income. This does not apply to holders of:

- Certain CFCs and PFICs held in a Section 1411 trade or business or

- PFICs marked to market under a provision of Code Chapter 1 other than Section 1296

Line 7: Other modifications to investment income

Use Line 7 to document modifications to investment income that are not already specified in Lines 1 through 6. This includes:

- Section 1411 net operating loss (NOL)

- Deductions described in Section 62(a)(1) not already taken in Line 4 or Line 5

- Adjustments for distributions from estates and trusts

- Section 404(k) dividends reported on Line 2

- Interest income reported on Line 1 received from certain nonpassive activities

- Recoveries of deductions taken on Form 8960 in a prior year

- Other items of net investment income reported on one of the following:

- Schedule 1 (Form 1040), line 8z

- Form 1041, Line 8

- Form 1041-QFT, Lines 4 and 9

- Form 1040-NR, amount on statement reporting tax items during U.S. residency

Line 8: Total investment income

Part II: Investment Expenses Allocable to Investment Income and Modifications

In Part II, there are 3 lines to help us arrive at total investment expenses allocable to investment income.

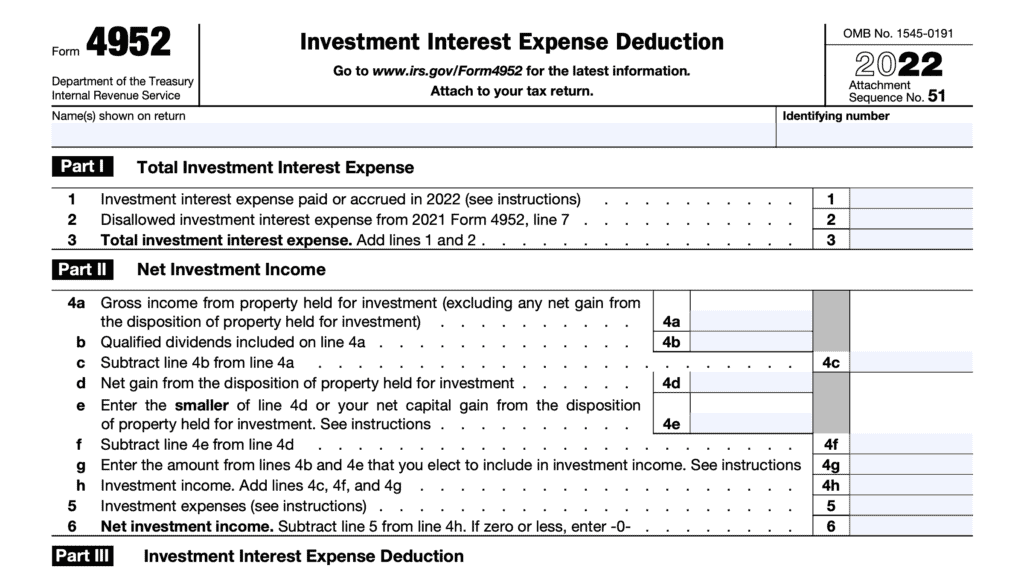

Line 9a: Investment interest expenses

Individual taxpayers will enter the interest expense paid or accrued during the tax year that was deducted on Schedule A (Form 1040), Line 9.

Estates and trusts enter the amount from Form 4952, Line 8.

Individuals filing Form 1040-NR will include only the amount of investment interest expense deduction for the period of U.S. residency.

Line 9b: State, local, and foreign income tax

Include the following income taxes you paid for the tax year that are attributable to net investment income:

- State income taxes

- Local government income taxes

- Foreign income taxes

Form 1040-NR filers will only include taxes attributable to their U.S. residency period.

Line 9c: Miscellaneous investment expenses

Investment expenses that are directly connected to the production of investment income are deductible expenses in determining your net investment income tax liability. Generally, taxpayers can find these amounts on IRS Form 4952, Line 5.

You may need to use the Line 9 and Line 10 worksheets if there are Line 9 expenses limited by Section 67 or Section 68. Consult the instructions page for more details.

Line 9d: Add Lines 9a, 9b, and 9c

Self-explanatory.

Line 10: Additional modifications

Use Line 10 to report additional deductions and modifications to net investment

income that aren’t otherwise reflected on Lines 1–9. A list of possible deductions and modifications is located in the form instructions.

Line 11: Total deductions and modifications

Combine Lines 9d and 10.

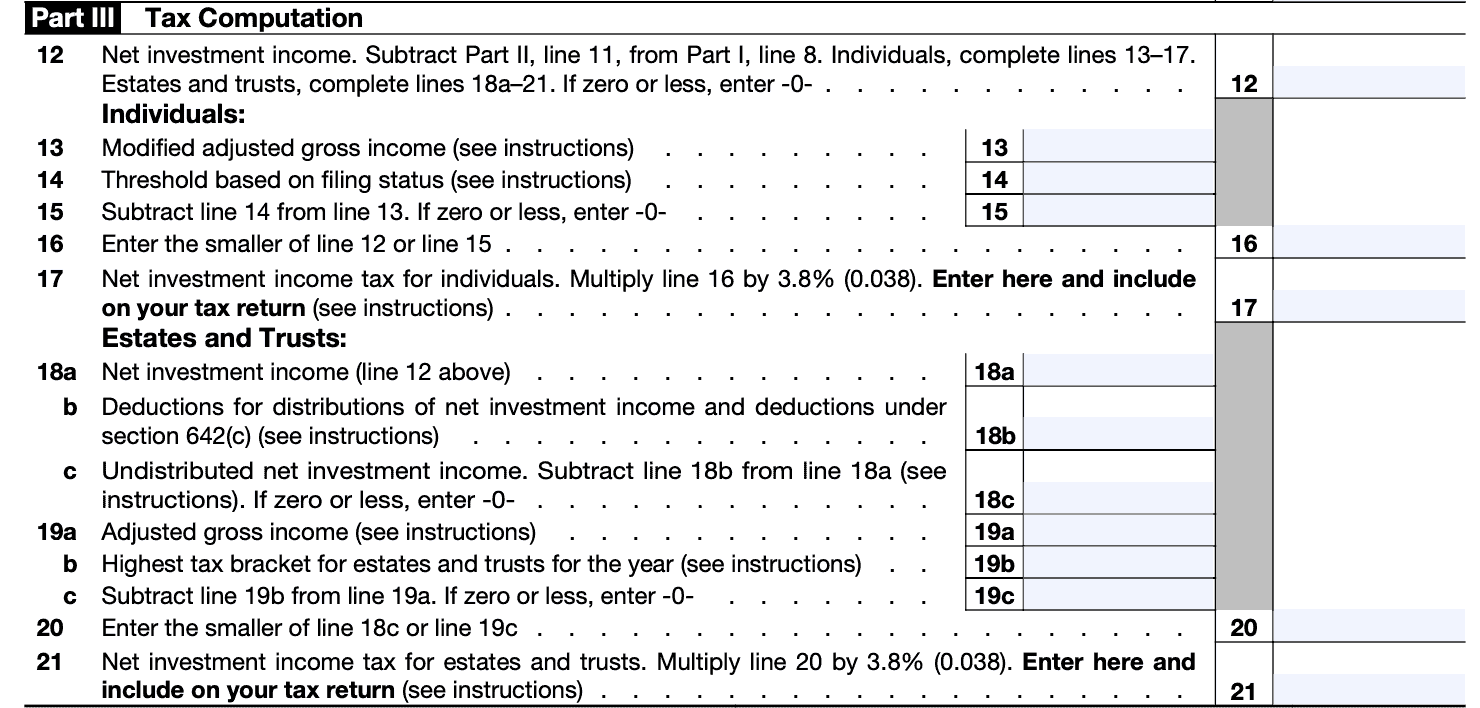

Part III: Tax Computation

Part III contains 14 lines used to calculate NIIT. However, some lines only apply to individual taxpayers, while other lines only apply to estates and trusts.

Line 12: Net investment income

Subtract Part II, Line 11, from Part I, Line 8. If this is not a positive number, enter ‘0.’

From here, individuals will complete Lines 13-17. Estates and trusts will complete Lines 18a-21.

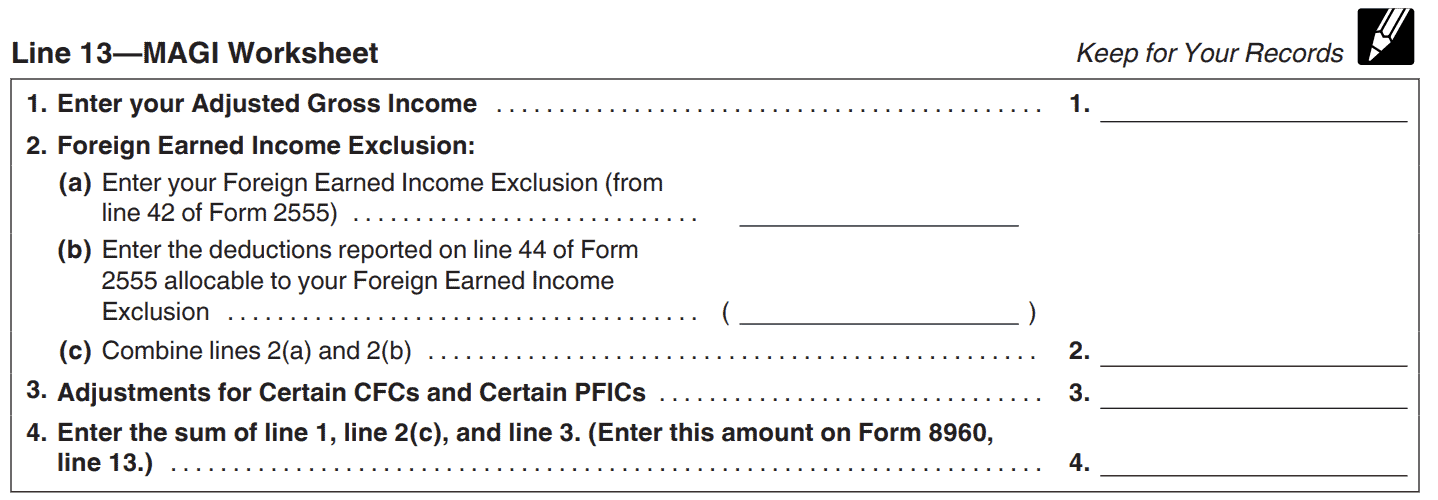

Line 13: Modified adjusted gross income (MAGI)

You’ll use the MAGI worksheet in the form instructions to calculate your MAGI.

Essentially, Line 13 will consist of your adjusted gross income (AGI) plus adjustments for the following:

- Foreign earned income exclusion from Line 42 of IRS Form 2555

- Deductions reported on Line 44 of Form 2555 allocable to foreign earned income exclusion

- Adjustments for certain CFCs and PFICs (see form instructions for more details)

Line 14: Threshold based upon filing status

For individuals, the threshold based upon filing status is below.

| Filing status | Dollar amount |

| Married Filing Jointly (MFJ) | $250,000 |

| Qualifying Widow(er) | $250,000 |

| Married Filing Separately | $125,000 |

| Single | $200,000 |

| Head of Household | $200,000 |

Line 15: Subtract Line 14 from Line 13

You’ll simply subtract the threshold from Line 13 (AGI plus adjustments)

Line 16: Enter the smaller of Line 12 or Line 15

In Line 16, you’ll enter the smaller of Line 12 or Line 15.

Line 17: Net investment income tax for individuals

Multiply Line 16 by 3.8%. the calculated amount is your net investment income tax liability, or the amount of net investment income tax individuals must pay in addition to their regular income tax.

Enter this amount on IRS Schedule 2, Line 12.

Line 18a: Net investment income

This is the same number as Line 12, above.

Line 18b: Deductions for distributions of net investment income and deductions under Section 642(c)

This line contains:

- Net investment income included in the distributions to beneficiaries that are deductible by the state or trust under Section 651 or Section 661, AND

- Net investment income for which the trust or estate was entitled to a Section 642(c) deduction

Refer to the IRS form instructions for more detail.

Line 18c: Undistributed net investment income

Subtract Line 18b from Line 18a. If zero or less than zero, enter ‘0.’

Line 19a: Adjusted gross income

Unless the estate or trust owns a CFC or PFIC, the AGI for NIIT purposes is the same number as the AGI reported on the tax return.

Line 19b: Highest tax bracket for estates and trusts for the given tax year

Use the dollar amount at which the highest income tax bracket for estates and trusts begins. For quick reference, this information is reported in the IRS form instructions for IRS Form 1041, Schedule G, Line 1(a). At the time of this writing, the highest tax bracket threshold for 2021 was $13,050.

Line 19c:

Subtract Line 19b from Line 19a. If zero or less, enter 0.

Line 20:

Enter the smaller of 18c or 19c.

Line 21: Net investment income tax for estates and trusts

Multiply Line 20 by 3.8%. This is the number you will include on your income tax return.

Real estate professionals

Your tax professional or accountant can help you understand which steps to take so you can exclude rental real estate income from NIIT calculations.

Who must file Form 8960?

Taxpayers whose modified adjusted gross income (MAGI) exceeds the threshold amount must file IRS Form 8960. For individuals, this is fairly straightforward. However, for estates and trusts, it might be a little less clear.

What is the applicable threshold?

The applicable threshold amount depends partially on filing status. Below are the current net investment income tax thresholds:

| Filing status | Dollar amount |

| Married Filing Jointly (MFJ) | $250,000 |

| Qualifying Widow(er) | $250,000 |

| Married Filing Separately | $125,000 |

| Single | $200,000 |

| Head of Household | $200,000 |

However, there is also a distinction of which filing status to use. This distinction depends on the immigration status of the taxpayer.

Individuals who must Form 8960

U.S. citizens and residents

Citizens and residents of the United States will pay 3.8% of the smaller of:

- Total net investment income

- Their MAGI minus the applicable threshold

Nonresidents

NIIT does not apply to nonresidents. If you are a resident married to a nonresident, you likely will use the filing status of married filing separately (MFS) for purposes of calculating any applicable NII tax.

You may be able to elect a joint filing for NII calculation if you file a joint return under one of the following IRC sections:

IRC Section 6013(g): Where a nonresident alien (NRA) is married to a U.S. citizen or U.S. resident at the end of the tax year

IRC Section 6013(h): Where at least one spouse was an NRA at the beginning of the tax year, but is a U.S. citizen or resident married to a U.S. citizen or resident by the end of the tax year.

Dual-resident individuals

You’ll generally be treated as a U.S. taxpayer for purposes of calculating NIIT. However, the IRS may treat you as an NRA if one of the following applies:

- You determine that you would be treated as a foreign resident for purposes of an income tax treaty between the United States and the other country

- You elect to be treated as a resident of the foreign country for purposes of calculating your U.S. income tax liability, and

- You file IRS Form 1040-NR, and IRS Form 8833

Dual-status individual

A dual-status individual may have been a U.S. resident for part of the year and a foreign resident for the remainder of the tax year. In this situation, a taxpayer is only responsible for NIIT for the period of time that they were a U.S. resident.

For additional tax implications based upon resident status, please refer to IRS Publication 519: U.S. Tax Guide for Aliens

Estates & trusts

For domestic estates and trusts, the NIIT is 3.8% times the lesser of:

- The undistributed net investment income for the current year

- Excess AGI (if any) over the applicable threshold amount

For estates and trusts, there exists a separate applicable threshold, based upon the highest tax bracket for estates and trusts. IRS Form 1041, Schedule G instructions currently indicate the following income thresholds:

However, there are also exceptions to this rule.

NIIT exceptions for certain trusts

The following trusts are not subject to NIIT rules:

- Certain charitable trusts that are exempt from federal tax

- A trust or decedent’s estate in which all of the unexpired interests are devoted to one or more of the purposes described in Section 170(c)(2)(B)

- Trusts that are classified as “grantor trusts” under Sections 671–679

- Electing Alaska Native Settlement Funds (described in Section 646)

- Perpetual Care (Cemetery) Trusts (described in Section 642(i)).

- Trusts that are not classified as trusts for federal tax purposes (i.e. real estate investment trusts)

For more complicated estate and trust situations, the IRS instructions contain additional details.

Video walkthrough

Frequently asked questions

IRS Form 8960-Net Investment Income Tax-Individuals, Estates, and Trusts, is the form that taxpayers use to report net investment income. Form 8960 accompanies the respective taxpayer’s income tax return.

Generally speaking, net investment income tax (known as NIIT) includes gross income from taxable interest, dividends, annuities, royalties, or rents.

There exists several exceptions to the NII tax. If derived from businesses that are not passive activities, or where the business trades in financial instruments or securities, then this income does not count as net investment income.

Real estate professionals may, or may not, be subject to NIIT on rental income depending on their circumstances. If the rental income isn’t derived in the ordinary course of a trade or business, then the taxpayer must generally include it as NIIT.

However, the taxpayer may be able to exclude the income from NIIT if:

-The rental activity is a Section 162 trade or business, or

-The real estate professional materially participates in the real estate rental activities

Excluded income consists of income from the following sources:

-Income excluded from gross income in Chapter 1 of the Internal Revenue Code;

-Income not included in net investment income; and

-Gross income and net gain specifically excluded by section 1411, related regulations, or other guidance published in the Internal Revenue Bulletin

Examples of excluded income include:

-Wages

-Unemployment compensation

-Alaska Permanent Fund dividends

-Alimony

–Social Security benefits

-Tax-exempt interest income

-Income from certain qualified retirement plan distributions

-Income subject to self-employment tax

Where do I obtain a copy of this form?

You can download a free copy of this form from the IRS website or by selecting the file below.

Related tax forms

This tax form is one of the fillable tax forms provided by the Internal Revenue Service, to help taxpayers reduce their tax preparation costs. To see more forms like this, visit our free fillable tax forms page, where you’ll also find articles like this.

Unlike the IRS, our articles contain step by step instructions for each tax form, as well as video walkthroughs. You can also check out all of our videos by subscribing to our YouTube channel!