IRS Form 7249 Instructions

If you’re trying to craft an offer in compromise to settle your tax debt, you may consider researching other recently accepted offers. Accepted offers are reported on IRS Form 7249, which the IRS will make publicly available, upon request, for up to one year after acceptance date.

In this article, we’ll walk you through what you should expect to see when you receive a copy of the IRS Form 7249, including:

- A complete break down of the offer acceptance report

- Frequently asked questions

Let’s start with walking through a sample copy of IRS Form 7249.

Contents

Table of contents

How do I complete IRS Form 7249?

Although you won’t have to complete IRS Form 7249, we’ll go over this tax form step by step. For your convenience, we’ve broken the form down into the following sections:

- Taxpayer information

- Liability description

- Reason for acceptance of offer

- Amount payable in accordance with the terms of this offer

- Signatures

Let’s take a closer look at each area, starting at the top.

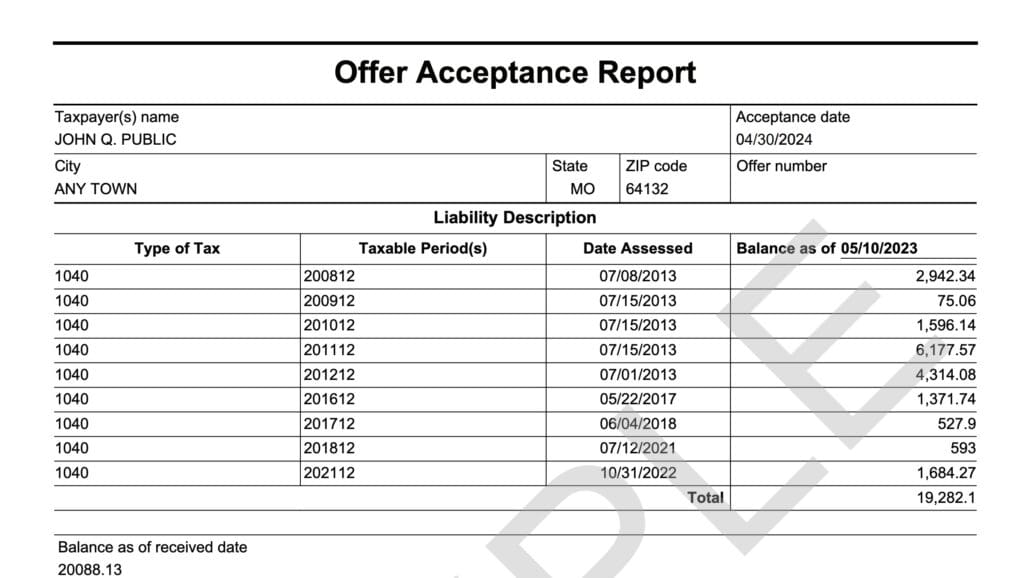

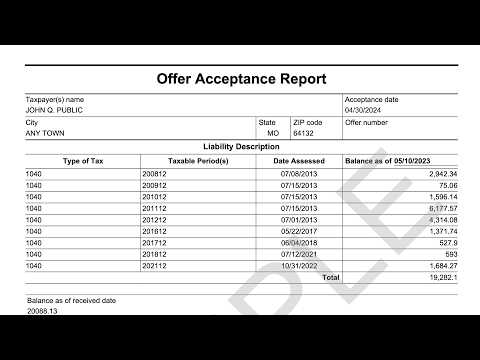

Taxpayer information

At the top of the acceptance report, you’ll see the taxpayer’s information. This includes:

- Taxpayer (or taxpayers) name

- Acceptance date

- City, state, zip code

- Offer number

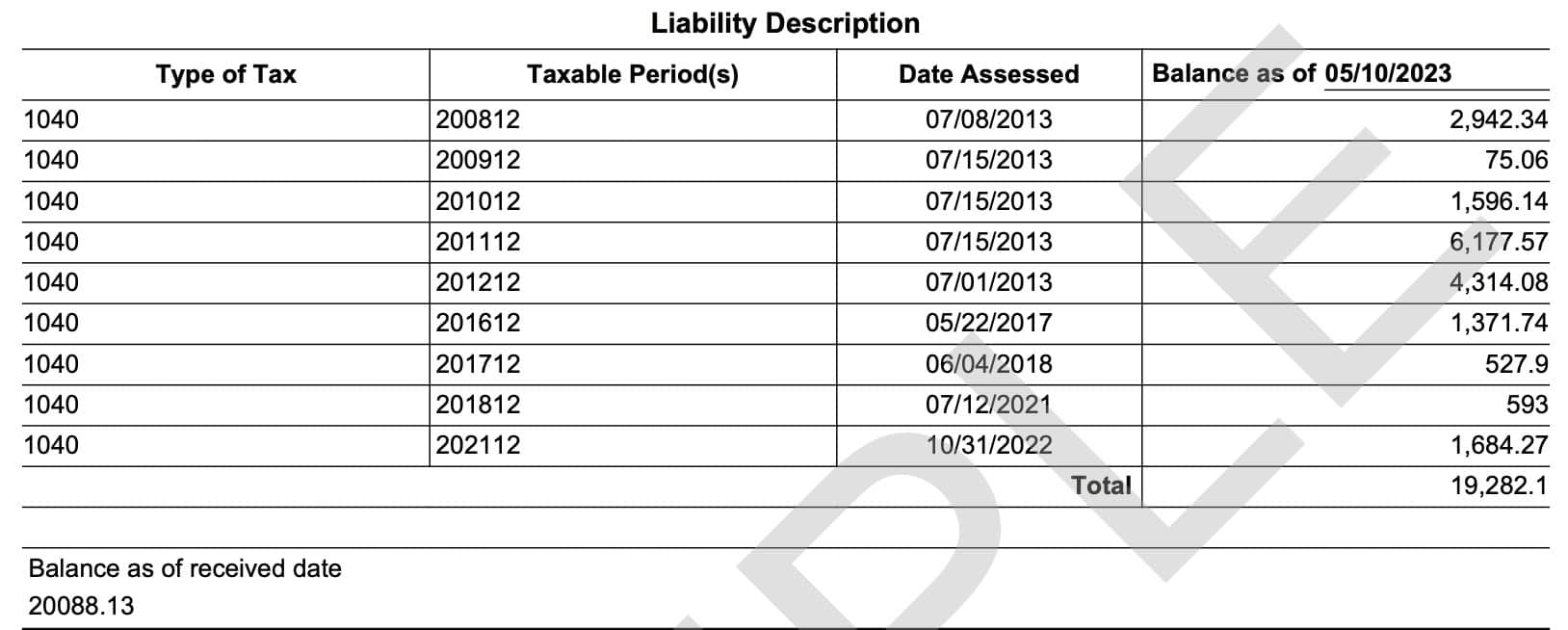

Liability description

In this part of IRS Form 7249, you should be able to see all of the tax information related to the offer in compromise. This includes:

- Type of tax

- Taxable period(s)

- Date of assessment

- Balance as of a specific date

At the bottom, there is also the balance as of the received date. This should be the date that the Internal Revenue Service received the proposed offer in compromise.

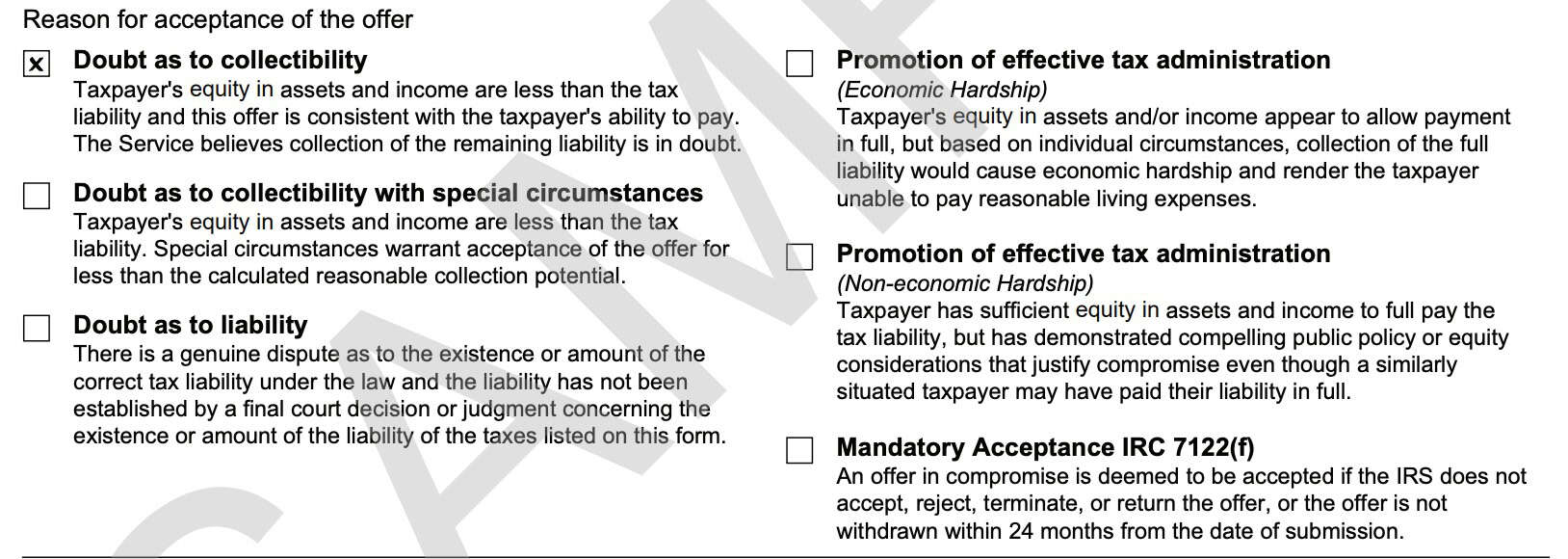

Reason for acceptance of offer

In this section, you should see a checked box next to one of the reasons for acceptance of the offer. There are six possible reasons that the IRS would accept an offer in compromise:

- Doubt as to collectibility

- Doubt as to collectibility with special circumstances

- Doubt as to liability

- Promotion of effective tax administration (economic hardship)

- Promotion of effective tax administration (non-economic hardship)

- Mandatory acceptance

Let’s take a closer look at each of these.

Doubt as to collectibility

Taxpayer’s equity in assets and income are less than the tax liability and this offer is consistent with the taxpayer’s ability to pay. The Service believes collection of the remaining liability is in doubt.

In other words

In other words, the IRS doesn’t believe that the taxpayer has enough income and/or assets to pay off the existing tax liability. The taxpayer has submitted an acceptable offer on IRS Form 656, and the income and assets determination were verified based upon collection information statement documentation submitted on either:

Doubt as to collectibility with special circumstances (DATCSC)

Taxpayer’s equity in assets and income are less than the tax liability. Special circumstances warrant acceptance of the offer for less than the calculated reasonable collection potential.

In other words

In other words, the taxpayer’s offer is less than the calculated collection potential, as determined by the Form 656. However, there are special circumstances that may compel the Internal Revenue Service to accept the taxpayer’s offer.

According to the Internal Revenue Manual, there are several factors that allow for establishing special circumstances. These factors, which are the same as the factors that are considered for effective tax administration, are the following:

- A liability has been or will be assessed against taxpayer(s) before acceptance of the offer in compromise.

- The sum of net equity in assets, future income, and the other components of collectibility making up the reasonable collection potential must be greater than the amount owed.

- The taxpayer presents exceptional circumstances, such as the collection of the tax would create an economic hardship, or compelling public policy or equity considerations that provide sufficient basis for compromise.

Doubt as to liability

There is a genuine dispute as to the existence or amount of the correct tax liability under the law and the liability has not been established by a final court decision or judgment concerning the existence or amount of the liability of the taxes listed on this form.

In other words

The taxpayer has submitted enough evidence for the IRS to determine that there could be a genuine dispute as to the existence or the amount of the correct tax debt under the Internal Revenue Code.

Since they are not based on the ability to pay the outstanding tax liability, these offers will be different from offers based on doubt as to collectibility.

Promotion of effective tax administration (economic hardship)

Taxpayer’s equity in assets and/or income appear to allow payment in full, but based on individual circumstances, collection of the full liability would cause economic hardship and render the taxpayer unable to pay reasonable living expenses.

In other words

Economic hardship occurs when a taxpayer is unable to pay reasonable basic living expenses.

The IRS will determine the reasonable amount for basic living expenses, which will vary according to the unique circumstances of the individual taxpayer. Unique circumstances, however, do not include the maintenance of an affluent or luxurious standard of living.

Promotion of effective tax administration (non-economic hardship)

Taxpayer has sufficient equity in assets and income to fully pay the tax liability, but has demonstrated compelling public policy or equity considerations that justify compromise even though a similarly situated taxpayer may have paid their liability in full.

In other words

While the taxpayer may have enough assets and income to pay their outstanding tax debt, there may be another reason why the IRS can choose to accept a submitted offer. According to the Internal Revenue Manual, below are some examples of reasons why the IRS would accept an offer, even if the taxpayer has the means to pay their tax bill:

- IRS error, erroneous advice or undue delay

- Wrongful acts of third parties

- Negative community impact

- Incapacitation

Mandatory acceptance

Under Internal Revenue Code Section 7122(f), an offer in compromise is deemed to be accepted if the IRS does not accept, reject, terminate, or return the offer, or the offer is not withdrawn within 24 months from the date of submission.

In other words

Under the tax code, if the IRS does not take any action within 24 months, then the submitted offer is deemed to be accepted.

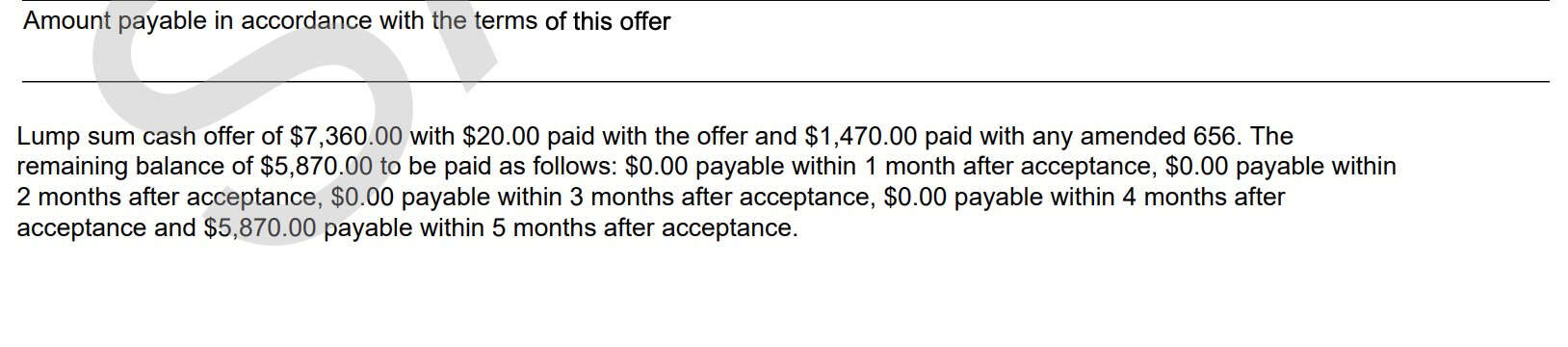

Amount payable in accordance with the terms of this offer

In this section, you should see the amount payable, as well as the payment terms.

In this example, you can see that the taxpayer’s accepted offer consists of:

- Lump sum cash offer of $7,360

- $20 paid with the offer

- $1,470 paid with an amended 656 form

- Remaining balance of $5,870 payable within 5 months of the offer acceptance

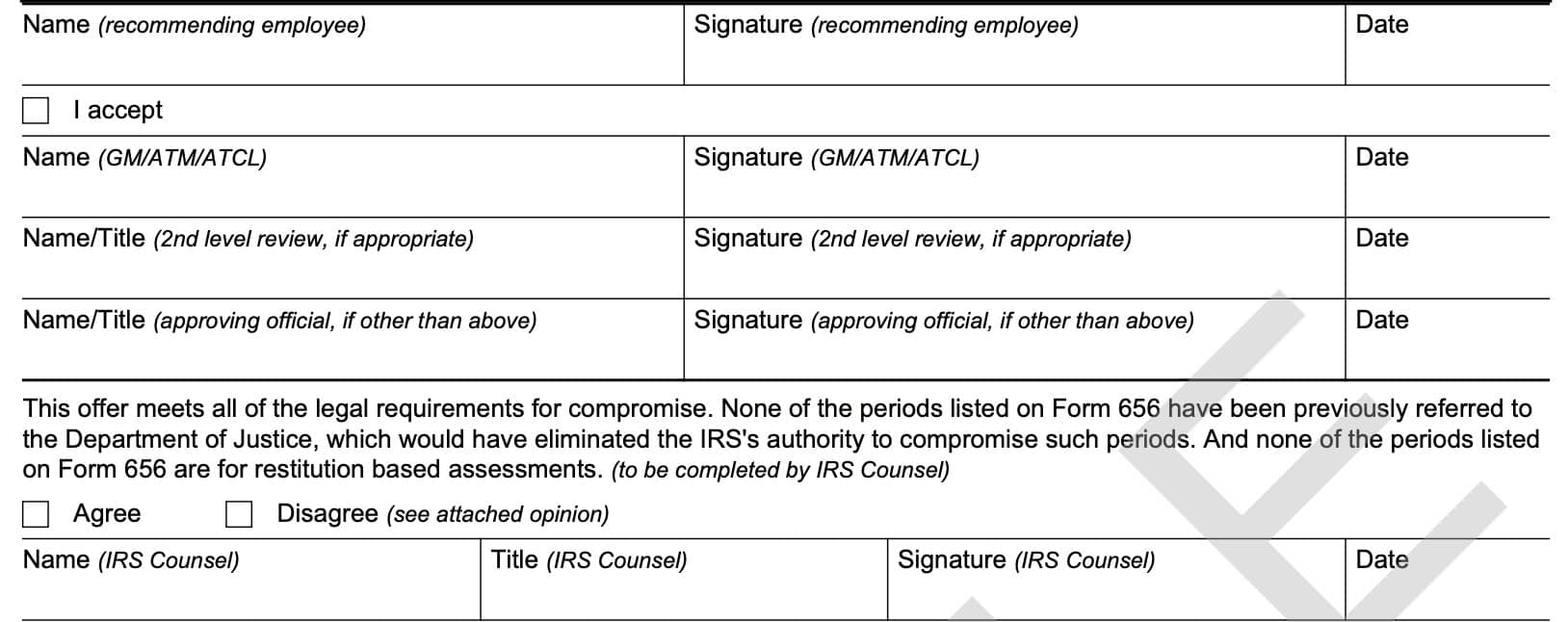

Signatures

This field includes signatures of the IRS employees involved in the approval process. This may include:

- First level review

- Second level review

- Approving official

- IRS counsel endorsement

Video walkthrough

Frequently asked questions

IRS Form 7249 is known as the offer acceptance report. This is the report that the Internal Revenue Service creates upon acceptance of an offer in compromise, and is made publicly available for inspection for up to one year after offer acceptance.

Any taxpayer may request a copy of an offer acceptance report by submitting a completed copy of IRS Form 15086, Offer in Compromise Public Inspection File Request. You may submit a copy of this request by fax, mail, or through the IRS website.